On My Radar: Defaults Will Breach the Historical High Next Year – The Fed is the “Wild Card”

Learn more about this firmInvestor Behavior – “You can bury your head in 10q’s and 8k’s and memorize a thousand facts about a company. You can become an expert on a given stock sector and establish relationships with all of the executives who run the show. You can build your own DCF models and outguess the other guessers on earnings estimates and forward guidance. But until you accept that market mood and behavior is as big a factor as the fundamentals, you won’t ever be completely honest with yourself. The E is only half of the PE. No matter how good you are at understanding and predicting the E, you’ve still only got half the story. The P is determined entirely by psychology.”

(The Reformed Broker)

I was in Chicago this week attending the Morningstar ETF conference. Jason Hsu from Research Affiliates was a keynote speaker and I loved his presentation on investor behavior. On the topic of who is supplying your excess return, he said, “People make bad decisions all the time… everywhere”.

At the end of his presentation, Jason was asked if bad investor behavior can be corrected. “It is impossible to overcome”, he answered. “Bad behavior will persist and this is the advantage to those with a discipline to take advantage of others bad behavior.” Amen brother.

The bargains in the U.S. will show up when the equity market is 30% to 40% lower. My two cents is to stay hedged, stay alert and prepared to act. Just like 2008, it won’t feel like a bargain. Oh but can we see the opportunity.

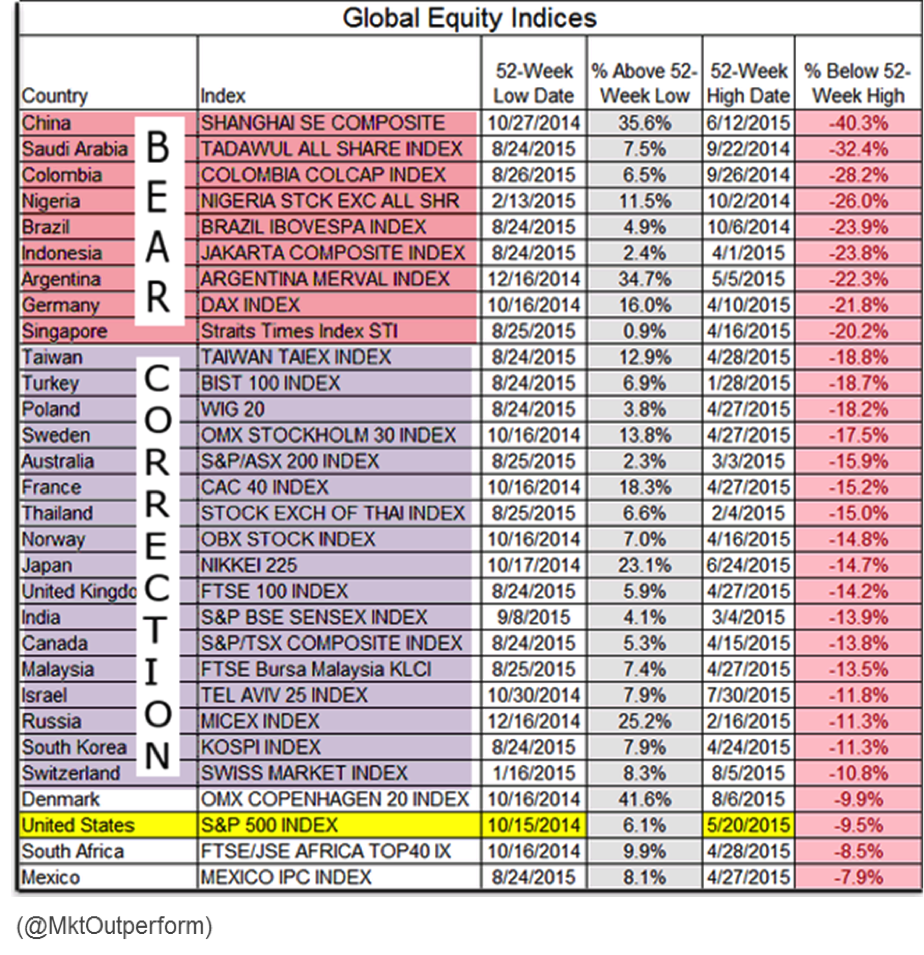

I always find it helpful when I view a summary of the various markets and asset class performance. Hope you find the next two charts helpful (a score card summary of the recent market performance).

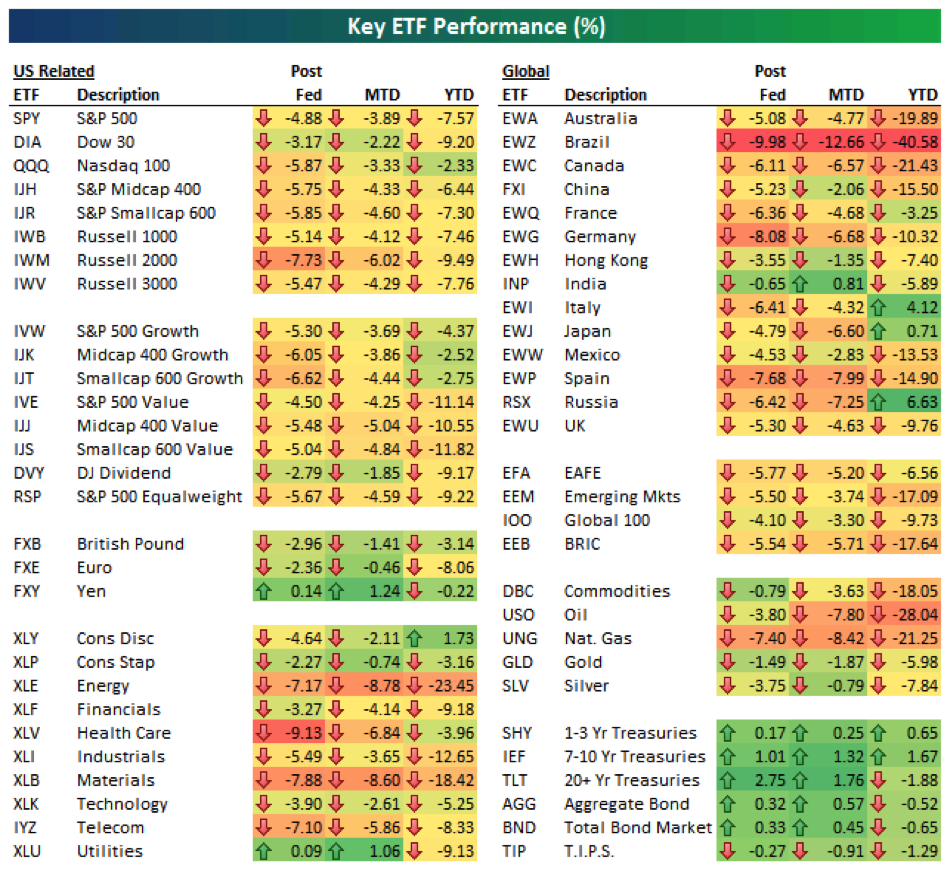

Next is a quick look at various asset class performance after Fed announcements, September, and year-to-date:

September, Post Fed and 2015 year-to-date Source: Bespoke https://www.bespokepremium.com/think-big/

Ok, grab your favorite beverage and let’s dive in.

Included in this week’s On My Radar:

- Update On The August 25, 2015 Dow Theory Sell Signal

- Harvard – “Lower Future Returns” and Yale’s – Alternatives Overweight

- High Yield – Rising Defaults

- Trade Signals – Weight of Evidence Bearish, Sentiment Extreme, Sell/Hedge Market Rallies (9-30-2015)

Update On The August 25, 2015 Dow Theory Sell Signal

DEFINITION of ‘Dow Theory’

A theory which says the market is in an upward trend if one of its averages (industrial or transportation) advances above a previous important high, it is accompanied or followed by a similar advance in the other. The theory also says that when both averages dip below previous important lows, it’s regarded as an indicator of a downward trend. Source: Investopedia

On August 25th the Dow Industrials and the Dow Transportation Index simultaneously made closing lows below the mid-October lows of last year and triggering a Dow Theory sell signal.

In the past 18 years, there have only been on inaccurate Dow Theory sell signal. That was the Flash Crash in May 2010 and it was quickly reversed four weeks later.

For now the August 25 low at 15,666 is holding. A break below that low would suggest a point to get very defensive though I favor hedged exposure today. We are in a cyclical bear market period (see Trade Signals below).

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Harvard – “Lower Future Returns” and Yale’s – Alternatives Overweight

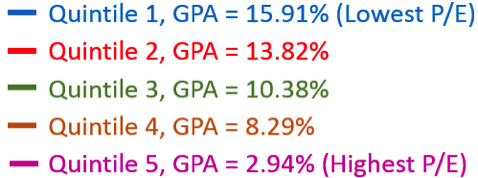

The market is expensively priced. We are in Quintile 5 (most expensive). Past periods of overvaluation have historically lead to 10-year annualized returns of approximately 3%. I’m setting my sights on Quintiles 1 and 2 (even Quintile 3 is attractive) with probable forward 10-year annualized returns in the 14% to 16% range.

Better to wait, as Buffett might say, for the hamburger prices to become cheap (Buffett Burgers and the Hallelujah Chorus). I believe we will see that opportunity occur. Liquidity will disappear, leverage will be forced to unwind, and investors will panic. When? Now? 2016? Later? Who knows, but when it happens it will happen fast. Here are the stats (source - NDR):

- From Harvard:The debate about highly-valued assets continues to get louder: private equity valuations are now, on average, at higher levels than in 2007. This environment is likely to result in lower future returns than in the recent past.

-

From Yale:Note that David Swensen has the Yale Endowment positioned into Alternatives (absolute return, leveraged buyouts, venture capital, real estate and natural resources). Also note the small 4% domestic equity weighting and the larger foreign equity exposure at 14.5%. The university said its fiscal 2016 asset allocation targets are as follows:

- Absolute return: 21.5%

- Leveraged buyouts: 16%

- Foreign Equity: 14.5%

- Venture Capital: 14%

- Real estate: 13%

- Natural resources: 8.5%

- Bonds and cash: 8.5%

- Domestic equity: 4%

Source: MarketWatch via 361Capital

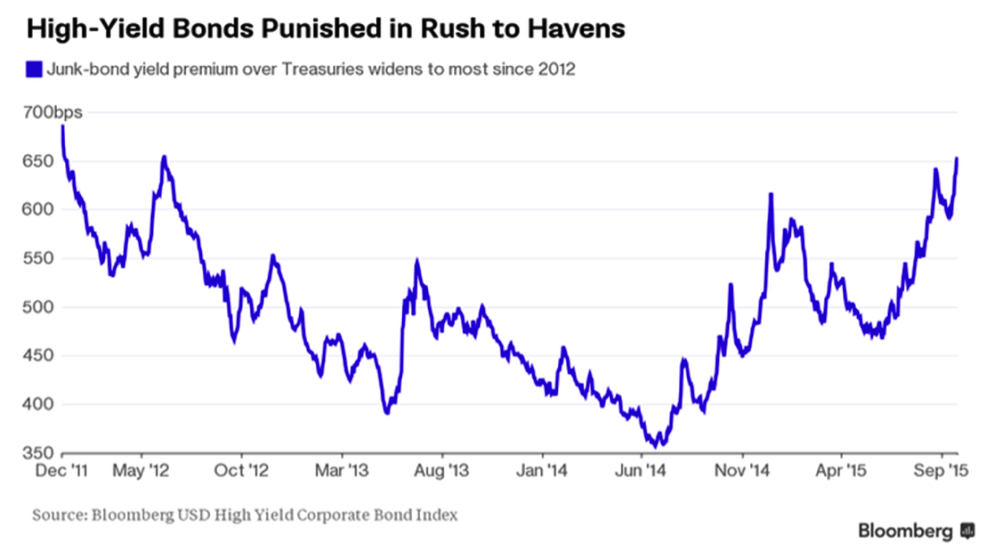

High Yield – Rising Defaults

Edward Altman, the New York University professor who developed the Z-Score method for predicting bankruptcies, says “defaults will breach the historical high next year and the Fed is the “wild card” that has the power to determine how quickly the current credit cycle ends.” Bloomberg

“We have blamed the wider Junk Bond spreads on Energy issuers, but last week there was a buyer’s strike. If this continues, you can say goodbye to easy financing for M&A which will remove one large pillar of support from stock prices”. 361 Capital

- Altice on Friday sold $4.8 billion of junk bonds to fund its $10 billion purchase of Cablevision Systems Corp., according to S&P Capital IQ LCD. When the deal was shopped earlier this month, Altice expected to sell $6.3 billion of debt, investors said. A 10-year bond was priced to yield 10.875%, compared with yields as low as 9.75% that were suggested by bankers initially, according to S&P Capital IQ.

- Olin on Friday sold $1.2 billion of bonds to pay for its pending acquisition of Dow Chemical Co.’s chlorine-products unit. Earlier in the month, Olin was expected to sell $1.5 billion of bonds, fund managers and analysts said. The annual interest rate on Olin’s 10-year bonds sold Friday was 10%, up from 7% expected earlier in the month, according to S&P Capital IQ.

- Companies have announced $3.2 trillion of M&A this year, according to Dealogic, emboldened to merge by cheap debt and the long stock rally that began after the financial crisis.

- That puts 2015 on pace to rival 2007 as the biggest year ever for takeovers. Issuance of junk bonds backing M&A deals hit a year-to-date record of $77 billion through Friday, according to data from Dealogic.

- A souring of investors on junk bonds could limit the availability of financing for deals that require a lot of borrowing. Banks have been under pressure from federal regulators to reduce their loans to such companies, and a pinch in the bond market could leave those deals struggling for financing. (WSJ)

- After investors snapped up more than $37.5 billion of bonds issued by junk-rated energy companies in the first six months of 2015, just $5.9 billion has been raised since then, according to data compiled by Bloomberg. Bloomberg

- Junk-bond investors are bracing for a surge in corporate defaults that would exceed the most pessimistic forecast from credit raters as the Federal Reserve contemplates its first interest-rate increase since 2006.

- A measure of distress in the market is suggesting investors have priced in a default rate of 4.8 percent during the next 12 months, according to Martin Fridson, a money manager at Lehmann Livian Fridson Advisors LLC.

- That’s almost two percentage points higher than the pace being projected for June next year by Standard & Poor’s, the world’s biggest credit rater, as concern mounts that energy companies that loaded up on cheap debt are going to struggle to refinance.

- “Unless there is a miraculous turnaround in oil prices there is likely to be a lot of defaults,” Fridson said. “The rating agencies’ approach isn’t capturing the fact that a large part of the economy is far out of step with the overall picture of the mark” Bloomberg

- On HY fair valuation from Martin Fridson this week: Now that the sector has sold off sharply, it’s finally at fair value, finds Fridson, chief investment officer at Lehmann Livian Fridson Advisors. He uses a model that includes current economic and market conditions to judge valuations. Barrons

- Note that fair value can move to significantly undervalued as happened in 1991, 2002 and 2008. Recessions are a bear (no pun intended).

- The S&P U.S. High-Yield Corporate Bond Index posted a yield to maturity of 7.51% on Tuesday, up from a recent low of 6.21% in late February. Morningstar data shows that the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) has lost 3.6% in the past six months.

Remain tactical with your HY exposure. We are seeing liquidity issues in the market. CNBC’s Cramer is advising listeners to get out of HY. Our tactical program is in a sell signal.

Corrections create the next great opportunity. As prices decline, yields move higher. Defaults are only a bad thing if you sit on the bus as it falls over the ledge. It will be higher defaults and declining prices and higher yields that will bring us returns like those achieved after the prior crisis.

7.51% yields look pretty appealing, but I think we will ultimately see 15% or higher at the depth of the next recession. Cash or short-term treasury bills can be attractive alternatives in the interim. My best advice on HY is to have a systematic process that gets you out and gets you back in. Not every trade will win but with a high probability trading process in place you’ll have a rules-based way to position for the next great opportunity.

- Important to remember that yields widened to nearly 2000 bps or 20% over Treasures in the 2008/09 financial crisis.

Ok – enough on HY. My two cents continues to recommend that you stay tactical with your HY portfolio exposure.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Trade Signals – Trade Signals – Weight of Evidence Bearish, Sentiment Extreme, Sell/Hedge Market Rallies – 09-30-2015

Here is a summary of this week’s Trade Signals:

- Cyclical Equity Market Trend: Sell Signal

- CMG NDR Large Cap Momentum Index: Sell Signal

2. 13/34-Week EMA on the S&P 500 Index: Sell Signal

3. NDR Big Mo: Neutral – Nearing a Sell Signal

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- Weekly Investor Sentiment Indicator:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for stocks

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for stocks)

- Don’t Fight the Tape or the Fed: Indicator Reading = -1 (Negative for Equities)

- S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

- The Zweig Bond Model: Buy Signal

Click here for the link to the charts.

Concluding thoughts:

The jobs number came out this morning. The results were sharply lower than expected, showing that U.S. employers have not been hiring over the last two months. Wages also fell in September.

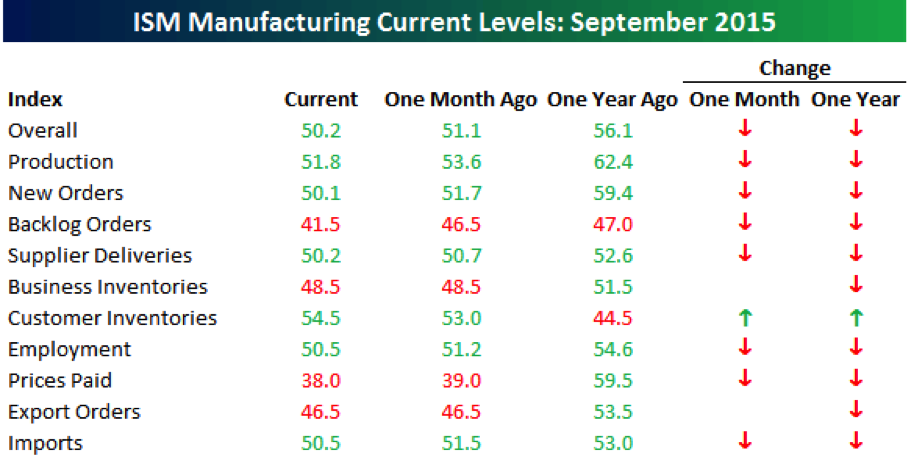

She’s slowing down folks. Take a look at the year-over-year industrial production numbers:

More and more, deflation is becoming a global central theme. It is my view that recession is in our near future. Best guess 2016. As Ed Altman said in the quote above, “the Fed is the “wild card” that has the power to determine how quickly the current credit cycle ends.”

Companies like Caterpillar Inc. benefited from the great China build out. Caterpillar said it would slash thousands of jobs and cut manufacturing space by 10%, as it expects weakening demand from resource and construction companies will continue to drive down sales of its heavy equipment through at least next year. It aims to reduce annual costs by roughly $1.5 billion.

Caterpillar said it now expects 2015 revenue to be about $48 billion which would mark a decline of about 27% from a peak of nearly $66 billion in 2012. And it said 2016 revenue likely would fall a further 5% from 2015, which would be the first time in Caterpillar’s 90-year history that sales declined for four consecutive years. (WSJ)

Combine slowing global growth with peak earnings and a richly priced market and something has to give. Expect earnings to continue to disappoint. The stage is set for the next great correction.

Triggers range from a sovereign debt crisis, the $9.6 trillion in EM dollar denominated debt, systematic counter party risks (remember these words: hypothecation and re-hypothecation), recession, and a severe HY default wave. Pick your snowflake – the risk of avalanche is high.

Ok – enough on risk. Let’s clear our heads and see the opportunity in all of this. Especially the opportunity it brings you to provide exceptional value to your clients. Hedge your equity exposure (or find funds that do) and overweight to a set of non-correlating risk exposures. We want you to be in a position to buy when everyone else is selling.

Bright minds with great investment management experience are signaling concern. Carl Icahn was out this week with his Danger Ahead video. Watch the 14 minute video – it’s good.

“Fill your life with worries and there is little room for dreams.” – Beth Mende Conny

Let’s not worry.

Personal note

Dallas is up next on October 8 (I’ll be speaking at a Bloomberg-sponsored advisor event). Dinner follows with my good friend John Mauldin. We’ll do some brainstorming on the economy, investment strategy, and portfolio structure. Should be fun.

Trust Company of America is hosting its annual “Focus on the Future” advisor client event later this month, so Denver is in sight.

Hard to believe it is already October. Every October the kids and I joke about Susan’s all-things-pumpkin craze. From soup, to various dishes, to seeds we all smiled last night at dinner when she mentioned it is time for pumpkin season. Rain is in the weekend forecast. The soccer fields are drenched so kids are likely sidelined. It looks like I’ll take a good crack at the “to do” list. It is so nice to be home.

Hope your weekend is filled with some fun plans.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group