The September Employment Report was disappointing, but not horrible. Some of the recent softening in the pace of job growth may reflect seasonal issues. Stronger seasonal hiring in May and June should naturally lead to more seasonal layoffs in August and September. That is unlikely the only explanation. Concerns about global growth and financial market volatility may have made firms, especially smaller firms, reluctant to hire. Estimate of 3Q15 GDP have been declining, while underlying domestic demand have remained strong. All of this complicates the Fed’s decision to begin normalizing monetary policy.

Nonfarm payrolls rose less than expected in September, while figures for July and August were revised lower. That is disappointing, to be sure, but not a disaster. One artifact of the financial crisis was a sharp drop in summer jobs. Labor force participation rates for teenagers and young adults fell sharply. The economy has been improving and the drop in gasoline prices was an enormous tailwind for tourism this summer. As teenagers and young adults head back to school, we should see more seasonal layoffs than usual.

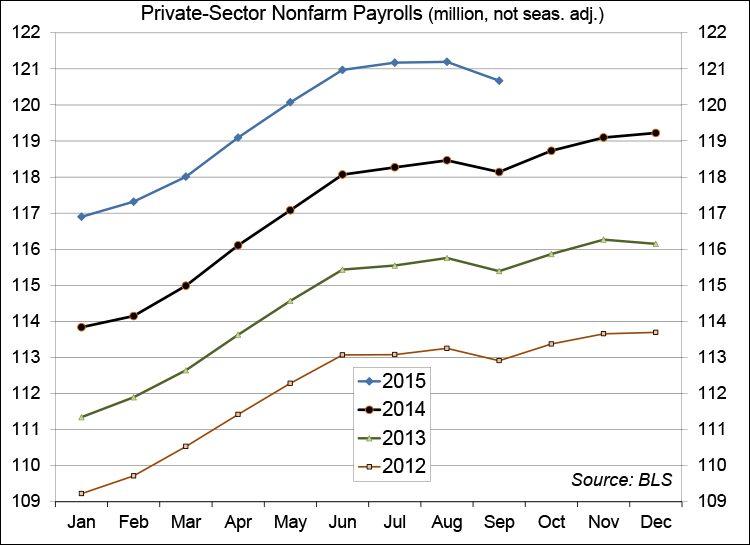

Prior to seasonal adjustment, the economy added 1.5 million jobs in education (public and private), about the same as in September 2014. However, we shed 958,000 jobs outside of education, compared to 812,000 a year ago. Labor force participation fell 0.2 percentage points in September, but not for the key cohort (those aged 25-54).

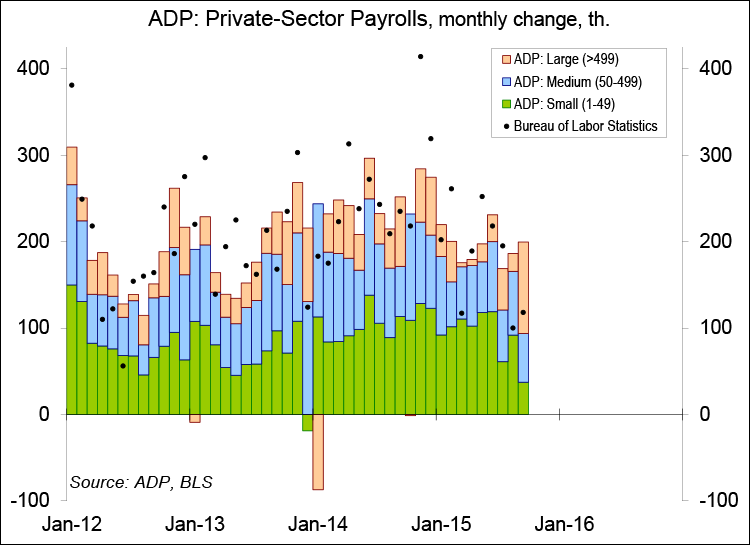

There are issues beside the seasonal adjustment. Slower global growth has had an impact on U.S. manufacturing. The ISM Manufacturing Index was close to zero in September, reflecting mixed conditions. Recent volatility in global financial markets has likely reduced business confidence. The ADP estimate of private-sector payrolls showed slower gains at small and mid-sized firms in recent months. Job growth at smaller firms had been a key factor in job market strength.

With the third quarter now behind us, we still don’t have a complete picture. However, we’ll get a better focus as the economic data roll in. At this point, recent reports remain consistent with the general theme of domestic strength and global weakness. A wider trade deficit and slower inventory growth are expected to have subtracted significantly from 3Q15 GDP growth. How much is hard to say. We have foreign trade and inventory data for July. However, we have consumer spending figures for August and unit auto sales results through September. Inflation-adjusted consumer spending (70% of GDP) appears to be on track to have risen at a 3.5-4.0% annual rate.

Where does this leave the Fed? Since the FOMC meeting in mid-September, officials have been making the case for an initial rate increase by the end of the year. The September Employment Report would seem to put that in doubt. The federal funds futures contracts dipped after the report, with a 25-basis-point rate increase not fully factored in until March. Still, the Fed sees a further reduction in labor market slack over the next several months and it is appropriate to consider a very gradual path back to a normal policy position.

It’s worth pointing out that the payroll figures are often revised. The “softening” in private-sector payroll growth may not hold up in revisions, or it could appear worse. While corporate layoff announcements continue to make headlines, when you add them all up, the monthly totals have remained relatively low. Moreover, weekly claims for unemployment benefits have continued to trend low (note that this is entirely consistent with large seasonal job losses for teenagers and young adults, who typically don’t file claims when they go back to school). Job destruction is not an issue.

For the financial markets, the key takeaway is that the upcoming economic data will be important. Plenty of reports will arrive before the Fed policy meeting in mid-December.

© 2015 Raymond James Financial, Inc. All rights reserved.