|

IN THIS ISSUE: 1. 2Q GDP Report Was Better Than Expected at 3.9% 2. The Problem With How the Government Measures GDP 3. Janet Yellen’s Supposed “Flip-Flop” on Monetary Policy 4. Fed’s Latest Uncertainty Leads to More Turmoil in Stocks Overview Today we look at last Friday’s better than expected final report on 2Q GDP, which was revised from 3.7% to 3.9%. Best of all, this increase was largely due to increased consumer spending which accounts for almost 70% of GDP. Following the paltry 0.6% increase in GDP in the 1Q, this means the economy grew by 2.25% in the first half of this year. While a 3.9% jump in economic growth in the 2Q was welcome news, there is a growing consensus that such reports from the government may not be remotely accurate. The problem is, many agree, that the government’s “seasonal adjustments” to the monthly and quarterly data have gotten out of control, and the numbers reported are no longer reliable. We’ll talk about this below. Next, we’ll look into what many are calling a “flip-flop” on the part of Fed Chair Janet Yellen in the last two weeks on the subject of when short-term interest rates are likely to be raised. At the Fed’s latest policy meeting on September 17, they decided to postpone the first rate hike in nearly a decade, seemingly indefinitely. But then last Thursday, Yellen said lift-off will happen before the end of this year, and this sparked the latest selloff in the equity markets. So, what gives? I will close today with a few thoughts about the SuperMoon, BloodMoon and lunar eclipse we saw on Sunday night. I hope you got to view it. And finally, our latest WEBINAR with ZEGA Financial is now available for viewing on our website. ZEGA’s strategy for using options is one of the most interesting I have ever seen. 2Q GDP Report Was Better Than Expected at 3.9% The US economy expanded more than previously estimated in the second quarter on stronger consumer spending and construction, the second upward revision in a row. The Commerce Department said on Friday that Gross Domestic Product rose at a 3.9% annual pace in the April-June quarter, up from the 3.7% pace reported last month. This was the third and final estimate of 2Q GDP. The rise to 3.9% beat the pre-report consensus of 3.7% and was driven by growth in consumer spending, mainly on services like health care and transportation. Consumer spending, which accounts for more than two-thirds of US economic activity, was revised up to a 3.6% growth pace in the 2Q from the 3.1% rate reported in August, helped by cheap gasoline prices and relatively higher house prices which are boosting household wealth.

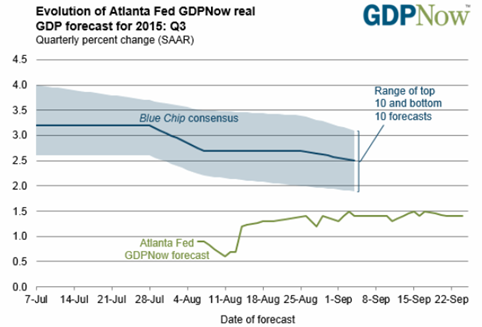

Revised construction spending data helped to push up the headline figure, with non-residential fixed investment expanding 4.1% in the quarter. The revisions to 2Q growth also reflected a smaller accumulation of business inventories than earlier estimated. Private-sector inventories grew by $127.5 billion in the second quarter, close to the growth in the first quarter. Most forecasters expect slower inventory accumulation to shave off one percentage point from the 3Q growth rate, leaving it slightly above 2%. It now looks like the economy will do well to record 2.5% growth for the whole year. After-tax corporate profits were also stronger in the 2Q than previously thought. Profits after-tax with inventory valuation and capital consumption adjustments were revised to show a 2.6% rebound from a slump in late 2014 and early 2015, instead of the 1.3% increase reported last month. The better than expected performance in the 2Q followed the paltry 0.6% pace in the 1Q. In the first three months of the year, a harsh winter and a port slowdown on the West Coast forced many companies to keep their products on the shelf rather than selling them. As a result, the economy grew at only a 2.25% pace in the first half of the year, a slightly higher pace than in the first half of last year. The Problem With How the Government Measures GDP More and more analysts are questioning how the Commerce Department measures GDP (as well as other important government economic reports). Economists are questioning how it is that we’ve had paltry 1Q GDP followed by a surge in the 2Q for several years now. As a result, more analysts are questioning the Commerce Department’s statistical methods that are used to estimate the output of America’s 320 million people. One explanation is that the numbers we are shown are not in fact the numbers which the statistical offices actually collect. The numbers we are shown often include large “seasonal adjustments” and variations. Seasonal adjustments are intended to smooth-out the data to reflect that there are, for example, more lifeguards working in the summer months than in the winter, and more ski-lift operators in the winter than in the summer. Likewise, there are hundreds of thousands of temporary workers hired around the Christmas holidays to work in stores and do holiday deliveries, who then get laid off around January 1. The government tries to account for these distortions and many others and seasonally adjust for them throughout the year. The problem, many now believe, is that the government’s seasonal adjusting is out of control, so much so that the data we see may be far from close to the actual measurement. For example, a recent Brookings Institute research report found that with the correct amount of seasonal adjustment based on weather, the lousy 0.6% growth in the 1Q would have improved to 1.4%. That, in turn, would have made the 2Q come in at 2.8% instead of 3.9%. In addition to the GDP reports, seasonal adjustments apply to many government economic reports we receive including jobs, housing, etc. As a result, it is very hard to make serious decisions when we know the numbers can change significantly from one report to the next. Finally, before we leave the subject of GDP, let’s take a look at the Atlanta Fed’s latest GDPNow estimate of where the economy stands as of last week. We can see that most analysts have lowered their 3Q GDP forecasts since late July but their median expectation is still around 2.5%. Yet the Fed’s estimate now stands at only 1.4%.

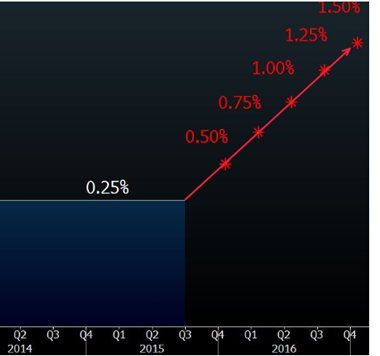

The latest decline occurred last week when the model’s forecast for 3Q real residential investment growth fell in response to the existing home sales report from the National Association of Realtors. We don’t get the first Commerce Department GDP report for the 3Q until late October. Janet Yellen’s Supposed “Flip-Flop” on Monetary Policy The Fed surprised a lot of people around the world on September 17 when its policy committee decided to keep interest rates near zero for a while longer. In the press conference following that meeting, Yellen said, “In light of the heightened uncertainties abroad and a slightly softer expected path for inflation, the Committee judged it appropriate to wait for more evidence.” That decision led a lot of Fed-watchers to conclude that the first Fed Funds rate increase was on hold, perhaps indefinitely, maybe not until next year. I didn’t see it that way, and I certainly didn’t take a rate hike at the Fed meeting on December 15-16 off the table. So I was not surprised when Yellen said in a speech last Thursday: “Most of my colleagues and I anticipate that it will likely be appropriate to raise the target range for the Federal Funds rate sometime later this year.” Yet apparently a lot of Fed-watchers took that as a ‘flip-flop.’ One theory to explain this goes as follows. For several years now, the US stock markets have rallied strongly whenever the Fed announced a delay in raising short-term interest rates. Yet this time stocks went down instead. Some theorized that the Fed may know of some really bad news on the horizon that it’s not telling anyone. As this theory goes, Yellen then felt compelled to warn last week about a likely rate hike by the end of this year to dispel such rumors. Are you confused yet? I certainly am! While Ben Bernanke and Yellen and their peers have come a long way since the days when setting policy was a deliberate exercise in secrecy, they’re guilty of flip-flopping so often that their efforts to direct expectations (ie – forward guidance) have become discredited. To be fair, the current economic backdrop to monetary policymaking is even more uncertain than usual, what with China in a funk, emerging markets looking vulnerable and the outlook for higher inflation non-existent. Nevertheless, the ‘forward guidance’ policy adopted in recent years by many central banks is in tatters, and is probably doing more harm than good. In any event, in light of Yellen’s latest suggestion of a rate hike before the end of this year, economists polled by Bloomberg are now predicting a continuous path of interest rate increases, with a one quarter-point move per quarter between now and the end of next year.

So don't be surprised if, in the coming quarters, this chart bears no resemblance to the reality of what happens to the US Fed Funds rate. No one knows what the Yellen Fed will do going forward. With that said, I predict lift-off in December. Fed’s Latest Uncertainty Leads to More Turmoil in Stocks Stock markets around the world have been suffering from growing uncertainties and worries about the global economy this year. Yet the US equity markets have held up surprisingly well, that is until recently. In late August, when China unexpectedly devalued the yuan, US stocks took a serious hit – with the first 10% correction in several years. The rebound from the late August lows has not been impressive, and the latest uncertainty from the Fed has only made matters worse. The rebound ended in mid-September and it now looks like a retest of the August lows is coming soon. The Standard & Poor’s 500 Index finished last week with a loss of 1.4%. It lost another almost 2% yesterday. The Index has tumbled over 8% so far in the 3Q, headed for its worst slide in four years. A rally last Friday, sparked by Yellen’s reassurance that turbulence in emerging markets won’t harm growth in the US, was snuffed out by the late-day selloff in biotechnology shares.

The Nasdaq Biotechnology Index tumbled into a bear market after falling 13% last week, its worst reading since 2011. The rout was sparked in part by a tweet from Democratic presidential hopeful Hillary Clinton suggesting there may be “price gouging” in the market for prescription drugs. Healthcare shares in the S&P 500 tumbled 5.8%, the most of 10 sectors last week. The latest selloff refocused attention on the volatility in markets that have been roiled in the six weeks since China’s shock devaluation of its currency. The Chicago Board Options Exchange Volatility Index (VIX) climbed over 6% to 27.63 yesterday, including a one-day jump last Tuesday of 11% that was the biggest since last month’s rout. The gauge has closed above 20 for 26 straight days, the longest stretch since January 2012. With the S&P 500 ending down for a second straight week, one pattern of back-and-forth was eliminated: a string of 10 weeks of alternating gains and losses. Disparity in trading volume highlights the risk of more losses. Volume on days when the S&P 500 falls has been 27% heavier than volume on the up days in September. That’s about eight times the average gap in the past decade. Now over 10% below its May high of 2,130.82, the Index has gone 90 days without setting a new high, the longest stretch since August 2012. The bad news just keeps piling up. And above it all loomed the Fed, whose officials fueled the debate over whether the American economy is robust enough to withstand higher interest rates this year amid the recent turmoil – and then a week later indicated that liftoff would still take place before the end of this year. The equity markets don’t like this uncertainty, and how could we blame them? Janet Yellen needs to figure this out! Sunday’s Rare SuperMoon, BloodMoon & Lunar Eclipse As I alerted you in last week’s E-Letter, the rare occurrence of a “SuperMoon,” a “BloodMoon” and a lunar eclipse occurred on Sunday night. I hope you got to view it. A number of friends and subscribers thanked me for giving them the heads-up in advance. From our viewing point here in Central Texas, just outside of Austin, it was not as impressive as I had hoped. We had wispy clouds Sunday night which obscured our view at times. But we could see the eclipse clearly. What was not as visible to us was the “BloodMoon” following the eclipse. We could see a faint orange-red moon at times after the eclipse when the clouds were not obscuring, but it was not a vivid BloodMoon for us. Even so, I’m glad we got to see it. I’m interested to know what you saw where you live. Since we have clients all across America, let me know what you saw on Sunday night. Was it really orange-red when you saw it? I’m curious. Photos anyone? Hoping to see the next one in 2033, Gary D. Halbert |

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |