“This Fed, massively dominated by academic Keynesians, has demonstrated that the conditions for normalizing rates are far more stringent than many of us had been led to believe from the speeches of the FOMC members themselves. This is a Federal Reserve with hundreds of staff economists who create numerous models to guide their actions. The fact that none of these models have been anywhere close to right for decades should give us pause. Indeed, in her press interview Yellen admitted that the models don’t appear to be working.”

– John Mauldin, Thoughts From The Front Line

The great Yogi Berra passed away a few days ago. His famous disjointed sayings, known as Yogisms, have been quoted by many and are fixtures of the American lexicon.

While having a coffee with my daughter yesterday, I asked if she knew about Yogi Berra. She paused, “Do you mean Yogi Bear as in ‘is that a pick-a-nick basket booboo’?” I smiled and said no, Yogi Berra the great NY Yankee. Knowing I was aging myself, we laughed at our generation gap.

Most of his Yogisms are either paradoxical or obviously redundant. Here are just a few of the memorable Yogisms that came from the Hall of Famer:

- “It ain’t over till it’s over.”

- “When you come to a fork in the road … take it.”

- “I didn’t really say everything I said.”

- “I always thought the record would stand until it was broken.”, and

- “It’s déjà vu all over again.”

Janet Yellen backpedaled a little this week stating she expects to raise rates this year. Perhaps it was the unexpected negative message the market sent her way after last week’s surprisingly dovish Fed comments. The Fed is losing credibility. From Greenspan to Bernanke to Yellen, it sure feels to me like “déjà vu all over again”.

I’m in NYC at ETF Trends annual “ETF Boot Camp”. I have many notes and hope to share some of the high level highlights with you next week. Much learned!

Today, let’s zero in on recessions and Trade Signals. There are a number of charts but it’s a short read.

Included in this week’s On My Radar:

- Recession Watch – Some Valuable Indicators (Recession is Nearing)

- Trade Signals – HY, S&P and DJIA Support Levels, Sentiment and Trade Signals

Recession Watch

“What scares me, or what worries me, is what the next downturn in the economy looks like, with asset prices where they are and a lesser ability of central banks to ease monetary policy.” – Ray Dalio with Bloomberg’s Tom Keene

There are two charts I favor that look at timing the start of recessions that I share with you today. Why are recessions so important to get in front of? Because the most serious market declines happen during recessions.

Chart 1: Global Recession Probability Model

There have been 10 recessions since 1970. The model, with a current reading above 70 is currently signaling global recession. With a current reading of 79.5, we are in the zone where recessions have happened 86.62% of the time. That is roughly 9 out of the last 10. We should stand alert. Here are the statistics (data 1950 to present):

Model vs. Actual Recession

- Readings above 70. Recession has happened 86.62% of the time. No recession when above 70 happened 13.38% of the time.

- Readings Between 30 and 70. Recession happened 47.73% of the time. No recession 52.27% of the time.

- Readings below 30. Recession happened 13.97% of the time. No recession 86.03% of the time.

Not perfect but I don’t like the odds. Global recession looks highly probable right now.

This from NDR on the model: The model is based on the Amplitude-Adjusted Composite Leading Indicators (CLIs) created by OECD for 35 countries. Each CLI contains a wide range of economic indicators such as money supply, yield curve, building permits, consumer and business sentiment, share prices, and manufacturing production. There are usually five to ten indicators, which vary by type and weight, depending on the country, and are selected based on economic significance, cyclical behavior, and quality.

The NDRG Global Recession Probability Model uses a logistic regression method incorporating both the CLI level and trend data of all 35 countries to predict the likelihood of a global recession. A score above 70 indicates high recession risks while a score below 30 means low risks.

The CLIs are normally released on the second Friday of each month for two months prior, or about a six-week lag. Meanwhile, the NDRG Global Recession Probability Model is a forward-looking model using a two-month lead in the CLI data. Source NDR.

Not perfect on predicting global recession but pretty darn good. I like to use the global recession model as it relates to my thinking around global equity exposure. Price momentum data is also helpful and to that end we have not been seeing EM or developed market equities showing up on our radar.

Let’s next take a look at the U.S. economy.

Chart 2: U.S. Recession Watch – My favorite U.S. recession forecasting chart: Currently Signaling No Recession

This is a systematic (rules based) process that looks to the stock market as a leading economic indicator. Data is updated monthly. Through the most recent full month-end, 79% of its signals, dating back to 1948, have been correct. My favorite U.S. recession forecasting chart is currently signaling no U.S. recession.

The U.S. model is currently signaling No Recession.

This is something you can track on your own (though I’ll continue to update the monthly results in this piece). Here is how to calculate:

- Signals are generated based on where the S&P 500 index is relative to its five-month smoothed moving average

- Economic Expansion is signaled when the S&P 500 index rises by 4.8% or more above its five-month smoothing

- Economic Contraction is signaled when the S&P 500 index falls by 3.6% or more below its five-month smoothing

- There have been 15 contraction signals generated since 1950 accurately predicting 9 of the 11 recessions. Missed were the 1953/54 and 1960 recessions. There were six false signals. Expansion signals fairly quickly reversed those contraction signals.

- There have been 14 expansion signals generated since 1950 accurately timing the end of 8 of the 11 recessions.

- In summary, the equity market is a very good leading economic indicator.

What you can do is reduce your equity exposure on sell signals. There are also a number of ways you can hedge your downside risk exposure. Remember that it requires a 25% return to overcome a 20% loss and a 100% return to overcome a 50% loss. The largest losses tend to come during times of recession.

It will be interesting to see what the September month-end data looks like. Stay tuned.

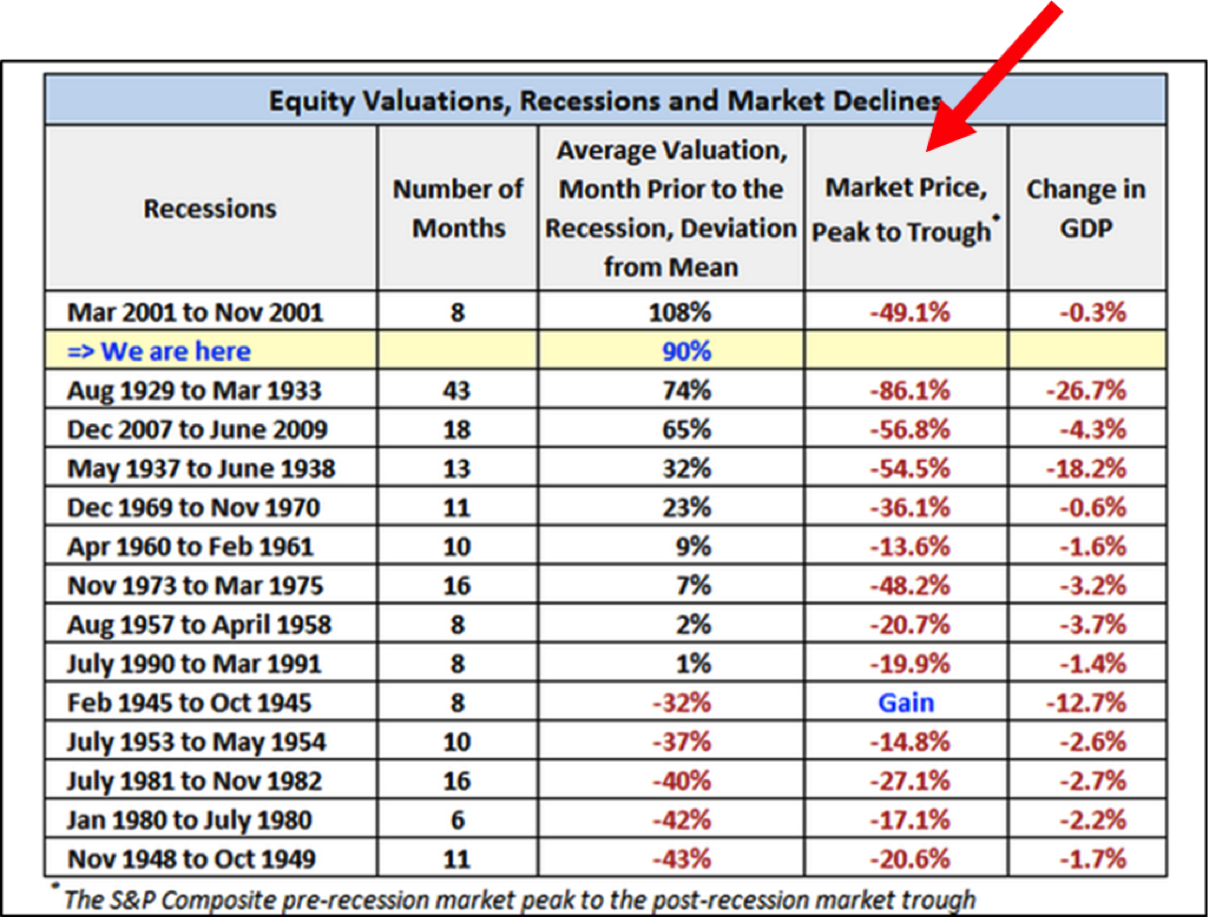

Next is data I have shared with you previously. In short, it details the market declines during a recession. Note that while there is correction during all recessions, the largest declines come when your starting point is an overvalued, expensively priced market.

Source: Equity Valuations, Recessions and Market Declines

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

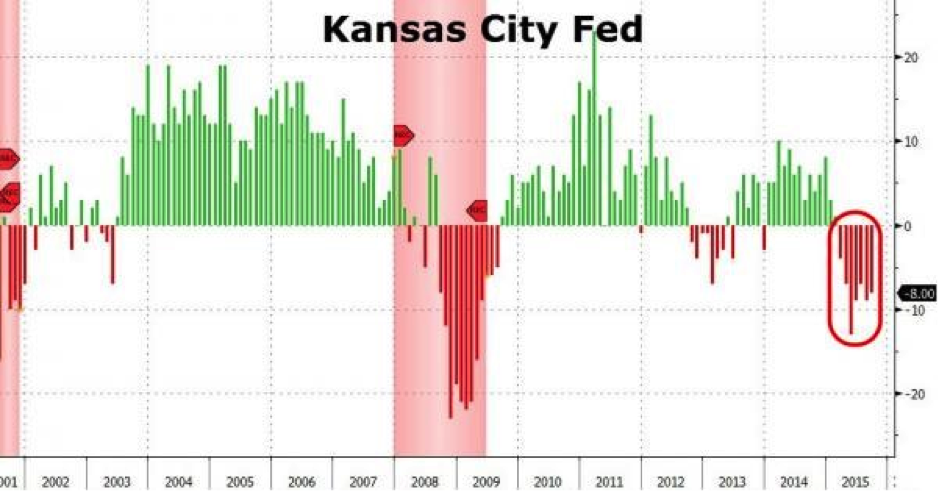

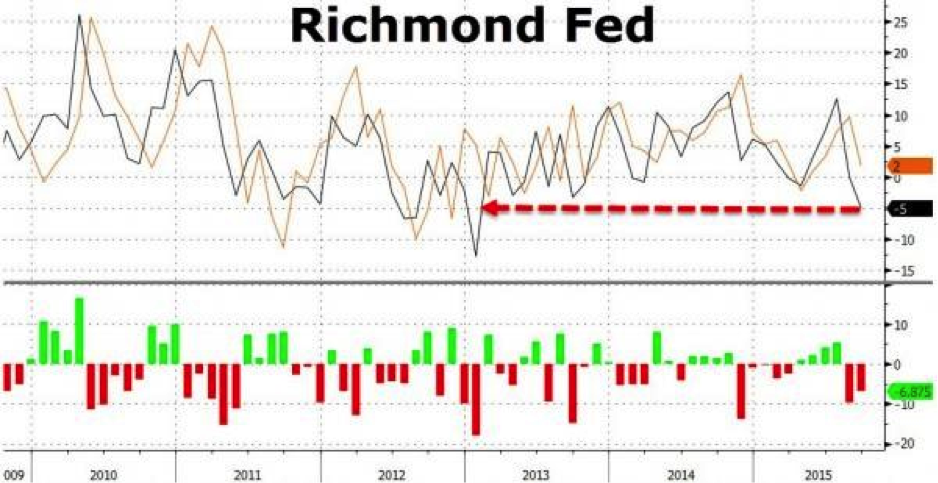

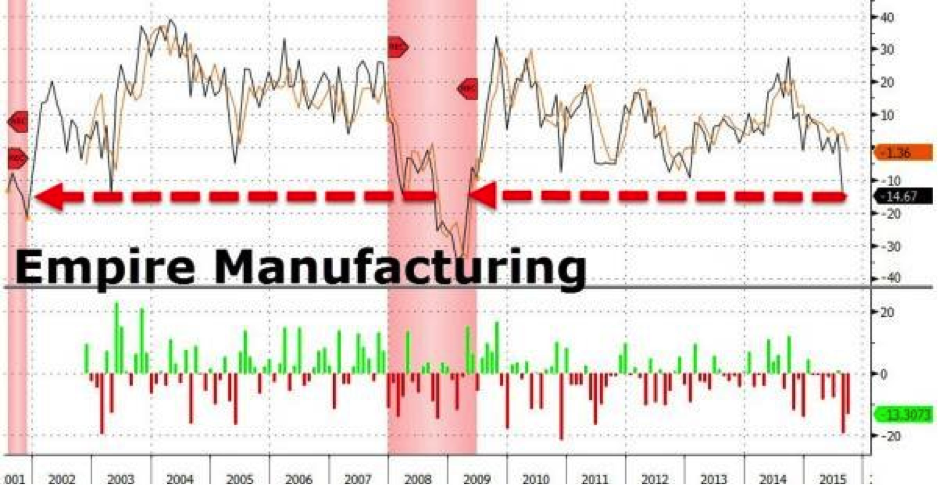

The following is just a few more data snapshots on recessions (sourced from the various regional Fed banks):

- Kansas Fed prints -8 (missing expectations of -6), now negative for the seventh month in a row…something not seen outside of a recession.

- Dallas…

- Richmond…

- Philly…

- Chicago…

- And Empire Fed…

Zerohedge Charts: Bloomberg

Look – we get recessions. It is always unwelcome but ultimately healthy for the long-term successful growth of an economy. Another recession is in our near future. My best guess is 2016. Much depends on the creativity of the central banks. QE4, which I predict is coming, will kick the can farther down the road. Structural reform? Not without crisis.

The largest equity market declines occur during periods of recession; thus, the above data bears watching.

It looks like a recession storm is nearing.

Trade Signals – HY, S&P and DJIA Support Levels, Sentiment and Trade Signals – 09-23-2015

Our CMG Managed High Yield Bond Program is back in a Sell signal. One of the things I’ve learned over my 20+ years of trading HY is that the HY bond market tends to be a good forward leading indicator for the stock market. I came across this chart from the Leuthold Group earlier this week. It shows the peak in credit and the subsequent peak in the S&P 500 Index (red arrow 2007). The chart on the right shows the peak in credit on June 23, 2014.

When yield spreads (or the difference in the yield that HY bonds yield compared to yields on safer bonds) widen, it represents an increase in the risk environment and a correction in the equity market typically follows. In this regard, the HY bond market is a pretty good leading indicator.

As we have been noting for several months, risk remains high. Overall, the weight of trend evidence remains bearish. Here is a summary of this week’s Trade Signals:

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: Sell Signal

- CMG NDR Large Cap Momentum Index: Sell Signal

2. 13/34-Week EMA on the S&P 500 Index: Sell Signal

3. NDR Big Mo: Neutral – Nearing a Sell Signal

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- Weekly Investor Sentiment Indicator:

NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for stocks)

Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for stocks)

- Don’t Fight the Tape or the Fed: Indicator Reading = -1 (Negative for Equities)

- U.S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

- The Zweig Bond Model: Buy Signal

Click here for the link to the charts.

Personal note

Recession talk is a bit depressing; yet, I believe it all depends on which lens we choose to view it through. There are a vast array of tools that enable you to build truly diversified portfolios. Not all investment risks drive return in the same way. ETFs are one example of a very liquid and diverse tool. Today the plan is to participate and defend. The next recession will bring great opportunity unless your portfolio is overweight equities and ultra-low yielding bonds. Stay tactical and prepared to act when a recession sets the stage for the next great opportunity. Unfortunately, many won’t be in a position to strike.

Separately, I found the below articles to be very exciting from an innovation prospective. I hope you find them as interesting as I did.

What it is: DARPA researchers were able to restore near-natural human sensation in a 28-year-old man who was paralyzed for over a decade using robotic prosthetics, brain implants and sophisticated neural technologies. Researchers placed electrode arrays on the paralyzed volunteer’s motor cortex and sensory cortex, tying those arrays to a mechanical hand. In testing, he performed with nearly 100 percent accuracy.

Why it’s important: Traditionally, robotic arms wired to brain implants have enabled paralyzed individuals to act, but without sensory information. DARPA program manager Justin Sanchez says that this innovation “completes the circuit,” enabling “seamless biotechnological restoration of near-natural function.”

What it is: University of British Columbia physicists have created single-layer superconducting graphene — a world first — by coating the graphene with lithium atoms in ultra-high vacuum conditions. They hope to eventually use this superconducting graphene to produce super-fast transistors, transparent electrodes, semiconductors and sensors.

Why it’s important: As KurzweilAI points out, superconductive graphene wires would have “zero resistance at ultra-low temperatures (at a critical temperature of about 5.9K), so a current flowing through it would generate no heat.” This development enables nanoscale quantum devices and graphene electronics that don’t overheat.

What it is: Qualcomm has debated Quick Charge 3.0, which can charge a smartphone to 80 percent of its capacity in 35 minutes — which means that it can charge most devices to a full battery in under an hour. The key is Qualcomm’s Intelligent Negotiation for Optimum Voltage, which supports new voltages in 200mV increments and makes the overall charging process more efficient.

Why it’s important: As our lives become increasingly gadget-centric, battery life is everything (ABC = Always Be Charging). When mobile users can charge their dead phones in minutes, they can do more resource-intensive work without battery anxiety. Source: Abundance Insider.

I’m walking away from my friend, Tom Lydon’s, ETF Boot Camp with a wealth of new information- Branding and Messaging, Digital Marketing and Social Media, The Shape of ETFs to Come, Regulatory issues, ETF Strategists and the Rise of the No Transaction Fee Platform and perhaps most importantly, new relationships – Blackrock, Bloomberg, State Street, Powershares, Fidelity, Schwab, TD, NYSE, NASDAQ. I learned a great deal.

I’m also going visit and do some brainstorming with my good friend John Mauldin.

The Morningstar ETF Conference is next week and Dallas follows on October 8 (I’ll be speaking at a Bloomberg sponsored advisor event). I’m also going to visit my good friend John Mauldin.

Here is a toast to the opportunities the next recession will present to us and a toast to being in a strong position to act. I’m working hard on a new white paper titled, The Total Portfolio Solution. It is about combining a number of diverse low-correlating assets and strategies and knowing when to tactically overweight and underweight various exposures. Stay tuned!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal C

hairman & CEO

CMG Capital Management Group, Inc.

Philadelphia – King of Prussia, PA

[email protected]

610-989-9090 Phone

610-989-9092 Fax

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group