“The effect of years of zero interest rate policies has been to progressively drive investors toward securities of greater and greater risk, in the belief that “There Is No Alternative” (TINA). In every other market cycle across history, once an “overvalued, overbought, overbullish” syndrome emerged in the stock market, market internals were either already deteriorating, or collapsed in relatively short order – meaning that investors became more risk averse. When overvaluation was joined by increasing risk aversion, air-pockets, panics and crashes typically followed”. – John Hussman

“Dammit Janet”. It’s astounding; time is fleeting; madness takes its toll. But listen closely… Not for very much longer. I’ve got to keep control. I woke up early this morning and somehow Janet Yellen and the lyrics to the Rocky Horror Picture Show jumped into my mind. Don’t tell my wife.

When I was young, the movie played every weekend at the local theater in my hometown. Do you remember how people would dress up in costume, shout out every line, throw rice during the wedding scene and sing to every song?

It appears that pressure from the likes of Christine Lagarde, head of the International Monetary Fund, and the Bank of International Settlements played a role. Don’t do it they messaged. Yesterday’s surprisingly dovish statement was notable for its introduction of “international developments” as ongoing input into the Fed’s rate decision process.

“Whatever you can do, or dream you can… begin it; boldness has genius, power and magic in it.” – Johann Wolfgang von Goethe

I’m on record saying the Fed won’t hike in 2015 and that perhaps their next move will likely be QE4, not the 25 bps hike that is built into our collective thinking. The immediate issue is the $9.6 trillion in U.S. dollar denominated loads. American banks, bond investors (mutual funds), and hedge funds loaned a record trillions in dollars to foreign companies and individuals. Foreign banks and bond investors have lent trillions more in “dollar loans” to foreign companies. The total is approximately $9.6 trillion. Put into perspective, the Fed expanded its balance sheet to $4.5 trillion buying many of the riskiest mortgage and other assets off the books of U.S. banks. $4.5 trillion was no small bail out.

It was the sub-prime mortgage crisis that triggered the last avalanche. In 2008 alone, the United States government allocated over $900 billion to special loans and rescues related to the U.S. housing bubble, with over half going to Fannie Mae and Freddie Mac (both of which are government-sponsored enterprises) as well as the Federal Housing Administration. On December 24, 2009, the Treasury Department made an unprecedented announcement that it would be providing Fannie Mae and Freddie Mac unlimited financial support for the next three years despite acknowledging losses in excess of $400 billion so far. Source: TARP, QE1, QE2, Operation Twist, QE3. You get the picture.

One of the great instabilities in the system today is the $9.6 trillion in U.S. dollar denominated debt owned by non-U.S. borrowers. With the U.S. dollar strengthening and thus the payback cost to those foreign borrowers rising, it is the trillions in emerging market “dollar loans” that is now in view. Strong dollar periods in the 1980s and 1990s caused emerging market financial crises.

In comparison, the U.S. high yield bond market is approximately $2 trillion in size. $1 trillion in new loans added since 2009. Many not so healthy corporations were funded. Let’s say 20% or so default. Call that a $400 billion problem (or future opportunity as I see it). The sub-prime trigger was approximately $1 trillion.

The dollar is up nearly 25% since 2012. Every 10% move higher in the dollar is another $1 trillion ($9.6 trillion times 10%) that must be paid back by the foreign individuals and corporations. Dollar down they win, dollar up they lose. Bad bets were made. It’s just a step to the right, then a jump to the left. The point I’m trying to make is that this one risk is bigger than sub-prime and it is not the only debt risk out there. Defaults are coming. Perhaps Claudio Borio, head of Bank of International Settlements “BIS” economic department says it best,

“We are not seeing isolated tremors, but the release of pressure that has gradually accumulated over the years along major fault lines.”

Dammit Janet – Boldness has genius, power and magic in it. I was secretly hoping for a rate hike. Having painted themselves into a corner, the Fed is stuck.

I presented this past Wednesday on a Morningstar Webinar titled, Navigating the Current Macroeconomic Environment Using Global All-Asset Strategies. In the preparation, I provide a link to a stat sheet of sorts on the current state of global GDP growth, various country Debt-to-GDP, valuations and probable forward returns, etc. I share the link with you below and hope you find it helpful in your work. You will also find a link to the webinar. Ok, grab a coffee and let’s jump in.

Included in this week’s On My Radar:

- Morningstar Webinar – CMG Economic Stat Sheet

- Hussman’s Forward 10-year Returns Calculation (0%) – Lower than My 2% to 4%

- Oil and Dollar Toll on Earnings Due to Rise

- Trade Signals – Cyclical Bear Trend In Place, Sentiment Remains Extremely Pessimistic (ST Bullish) – 09-16-2015

Morningstar Webinar – CMG Economic Stat Sheet

I was invited to participate on a Morningstar webinar this week which was sponsored by Vanguard. It was titled, Navigating the Current Macroeconomic Environment Using Global All-Asset Strategies. Following is the stat sheet that bullets a number of thoughts and data. Here is the link to the webinar replay.

CMG Economic Stat Sheet. Included are a number of quotes, link to the most recent BIS report, GDP data, Debt-to-GDP data and valuation and forward return information. There is a great chart showing China’s actual GDP growth closer to 1.1% vs. the 7% the central government has been proclaiming… and much more.

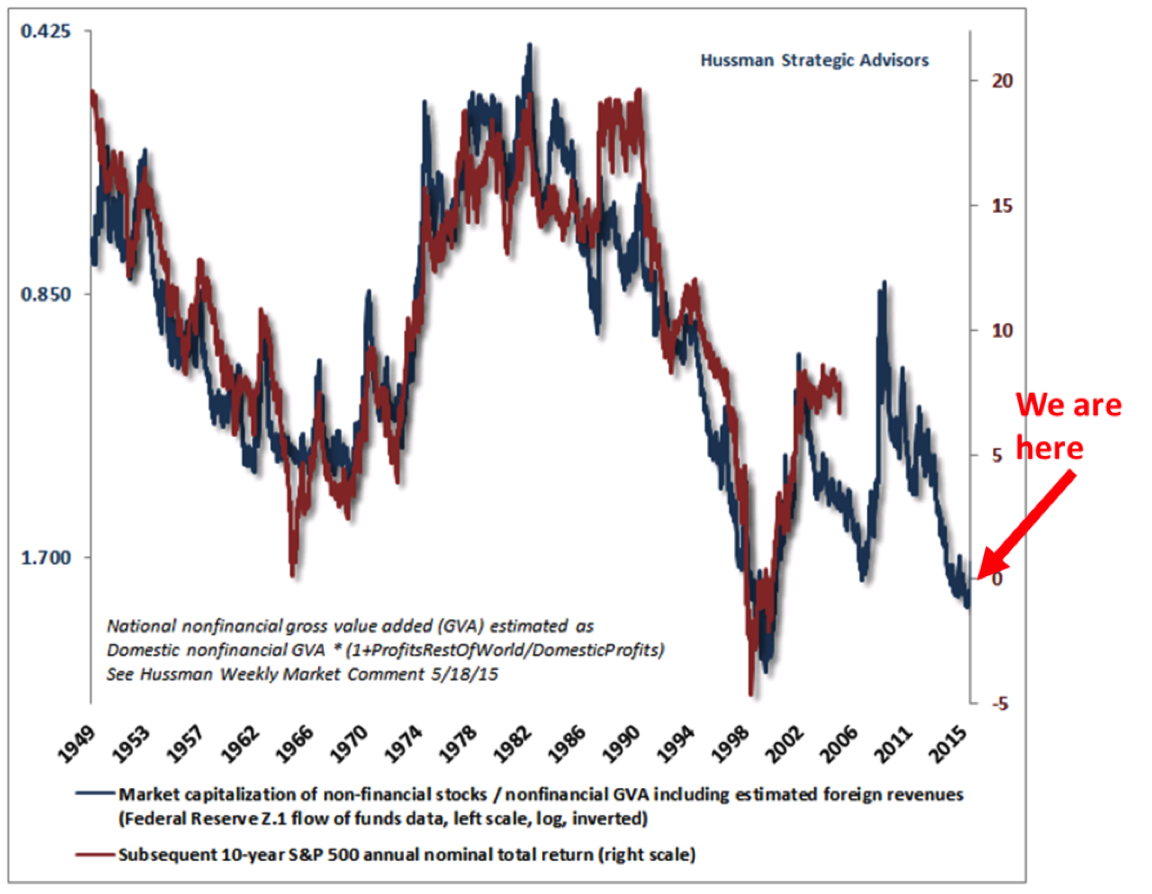

Hussman’s Forward 10-year Returns Calculation

John Hussman, “Currently estimate a 10-year nominal expected total return for the S&P 500 close to zero – much the same as we projected in real time at the market peak in 2000. The Federal Reserve seems to have no idea what it has done. Poor long-term market returns and severe interim losses are now baked in the cake as a result of obscene valuations. There is no way to undo this outcome – only to manage the consequences.”

Oil and Dollar Toll on Earnings Due to Rise

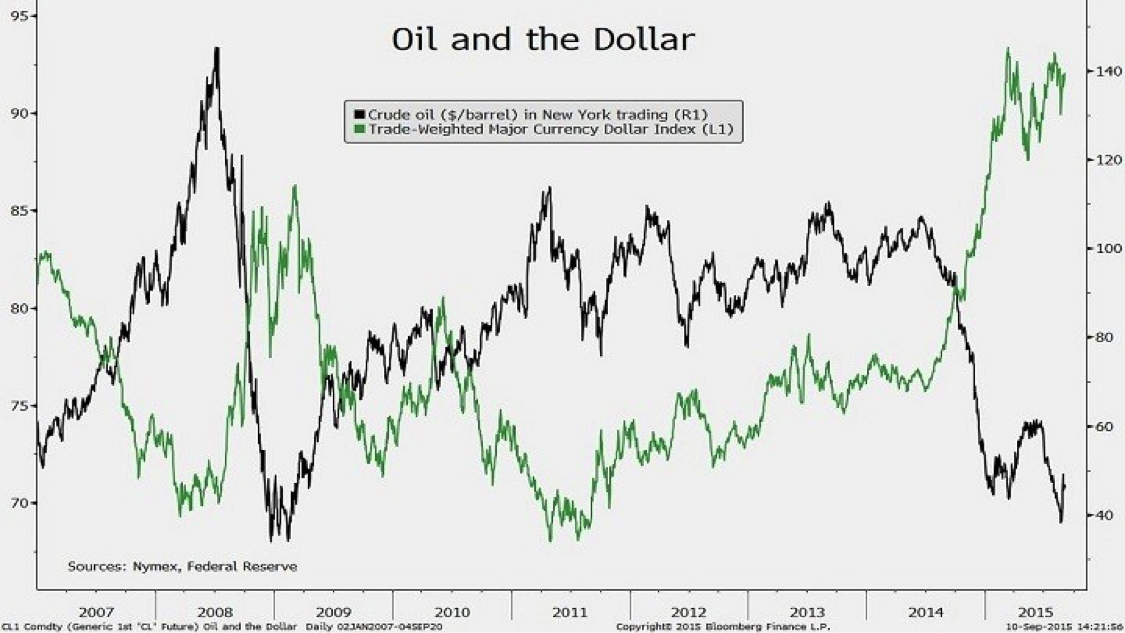

(Bloomberg) — Falling oil prices and a strengthening dollar suggest earnings estimates for next year may be too high, according to David Bianco, chief U.S. equity strategist at Deutsche Bank AG.

The chart below shows the price of oil in New York trading and the Trade-Weighted Major Currency Dollar Index, an index compiled by the Federal Reserve of the dollar’s value against seven other major currencies. Since last year’s third quarter, crude has dropped as much as $67.13 a barrel and the dollar index has climbed as much as 23 percent.

Every $5 a barrel decline in oil reduces net income for Standard & Poor’s 500 Index companies by about $7.5 billion, or $1 a share, Bianco estimated in a September 4 report. A 10 percent advance in the dollar’s value trims profit by about $20 billion, or $2.50.

Higher interest rates and slower economic growth may also hurt earnings, the New York-based strategist wrote. Each 0.25 percentage point increase in the Federal Reserve’s key rate has the potential to reduce S&P 500 net income by 50 cents a share, the report said, adding that the global economy’s expansion may matter more for companies in the index than U.S. growth.

Bianco now expects S&P 500 earnings of $128 a share next year, up from $120 this year. For 2016, he wrote that $125 “is very possible” because of the effects of the dollar, oil and other influences even if U.S. gross domestic product, the value of goods and services produced within the country’s borders, rises 3 percent.

“The worst of these drags should pass in 2015,” the strategist wrote, adding that a valuation of 18 times earnings for the S&P 500 is justifiable because rates are low by historical standards. He reaffirmed that he sees the index reaching 2,300 next year, up from 2,150 this year. The latter prediction is below the median of 2,200 among 21 strategists as of August 31 in a Bloomberg survey. A grateful hat tip to Bloomberg’s David Wilson (September 11, 2015)

The message here is for us to be cautious around the current period of peak earnings. They are likely to come under pressure.

Trade Signals – Cyclical Bear Trend In Place, Sentiment Remains Extremely Pessimistic (ST Bullish) – 09-16-2015

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: Sell Signal

- CMG NDR Large Cap Momentum Index: Sell Signal

2. 13/34-Week EMA on the S&P 500 Index: Sell Signal

3. NDR Big Mo: Neutral – Nearing a Sell Signal

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- Weekly Investor Sentiment Indicator:

NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for stocks)

Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for stocks)

- Don’t Fight the Tape or the Fed: Indicator Reading = -1 (Negative for Equities)

- S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

- The Zweig Bond Model: Buy Signal

Click here for the link to all of the charts.

Concluding thoughts

As I mentioned in the last several OMR posts and again today with the Hussman data, valuations are high and forward 10-year annualized returns look to be in the 2% to 4% range (returns annualized before inflation is factored in). Hussman sees 0% forward 10-year annualized returns. Close enough for horse shoes – either way not what your client is looking for. Along that bumpy path, the S&P 500 is likely to decline significantly during the next recession. Is it different this time? Not a bet I’m willing to take.

China, Japan, Europe, EM: All of these economies matter to our collective prosperity. I found interesting the comment from a Japanese-based research firm: “Of all the possible risk scenarios the meltdown scenario is, realistically speaking, the most likely to occur. If China’s economy, the second largest in the world, twice the size of Japan’s, were to lapse into a meltdown situation such as this one, the effect would more than likely send the world economy into a tailspin. Its impact could be the worst the world has ever seen.” Daiwa Institute of Research – Japan’s Economic Outlook

Sounds a bit apocalyptic yet my hope is you do not receive it that way. There is really good news in all of this. Just as the corrections in 2000 and 2008 provided outstanding buying opportunities, the next recession will do so as well. Let’s just not get run over by the bus on the way to that opportunity. Now is the time to play defense, be forward looking and prepared to act on the opportunity the next recession will create. Patience is required. Of course, some large speculative opportunities, like sub-prime in 2007/08, exist. Short EM, short high yield, short sovereign debt. It takes lots of guts, conviction and the ability to be wrong before you may ultimately be right. It was painful for those sub-prime shorts before they made a handful of aggressive hedge fund managers millions. Standing in your way today are some very creative central bankers. As my grandmother “Cookie” used to say, “it ain’t easy kid.”

Kick the can will continue until a point that it cannot. That tipping point is nearing. The next opportunity, born in recession, will be just as great as the last two but like the last two, it will not feel like opportunity when it presents. For now, allocate to a number of low-correlating investment strategies that are far more flexible/tactical in nature (see each as a unique diverse risk), hedge that equity exposure and remain mentality prepared to adjust your exposure back to an equity overweight when equity valuations are once again attractive with 10-year forward return probabilities of 10% to 15%.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group