The Federal Open Market Committee (FOMC) concluded its meeting today with no change in interest rates. International influences were a clear deterrent, and featured prominently in the committee’s statement and in Chair Janet Yellen’s remarks at her post-meeting press conference.

We expect that conditions will support a 25 basis point change in overnight rates at the Fed’s December meeting. But the tone of today’s communication hints that such action may come later rather than sooner.

Conditions leading up to today’s meeting did not provide the clarity the FOMC needed to take such a momentous step. Some note that a 25 basis point hike is hardly momentous, but after seven years near zero, it would be a significant departure. The Fed’s ability to form an outlook has been challenged by a series of “adverse global economic and financial developments (which) may restrain economic activity.”

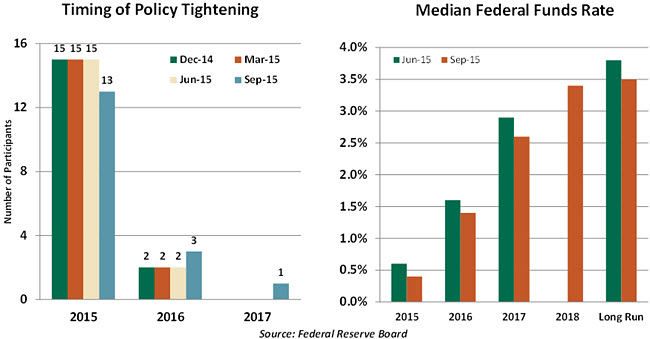

While a vast majority of participants still expect a change before the end of the year, the path of the funds rate is expected to be gentler than June FOMC forecast summary projected. Yellen counseled observers not to overstate the importance of the first movement, but rather to focus on the longer path of policy. We’d certainly concur with this recommendation.

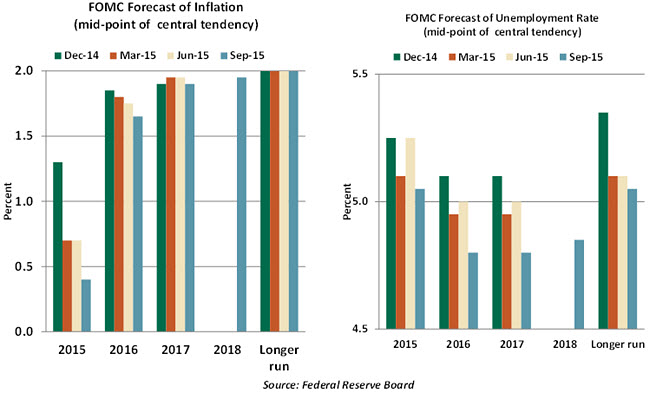

Future policy will continue to center on confidence that inflation will eventually approach the Fed’s 2% target. That confidence may be difficult to acquire, given the near-term influence of low oil prices and the strong dollar.

These elements may be somewhat transitory, but recent global events suggest that they may be with us for longer than previously thought. The median reflected in the collective forecasts published today reflected a lower path for inflation over the next several years.

The FOMC slightly lowered its view of what constitutes full employment, dropping its long-run unemployment rate a tick to 4.9%. Actual unemployment is forecast to run below that level for the next three years.

In the post-meeting press conference, Yellen pointed out several lingering pockets of unemployment. She noted that the labor force participation rate remains below the level consistent with the nation’s demographics, and highlighted elevated levels of part time work.

She highlighted further improvement in the labor markets as something the FOMC will be watching for in the intermeeting period, noting the link between this outcome and the goal of feeling more confident about the path of inflation. The link between the two is wage gains, which have been centered at around 2% annually since the beginning of 2011 despite a four percentage point drop in the unemployment rate.

Phillips Curve debates that were part of the recent Jackson Hole program are central to some of the Fed’s thinking.

Longer-run growth prospects were revised down a shade to a range of 1.8% to 2.2%. Actual forecasts of growth from 2015 to 2017 exceed that level, suggesting reduced resource slack and upward pressure on inflation.

There was one dissent to the decision, from Richmond Fed President Jeffrey Lacker. Lacker has dissented frequently in the past, favoring higher rates, and gave a speech earlier this month making “The Case Against Further Delay.” It is unlikely that others will join him on that end of the FOMC spectrum.

Yellen emphasized that the next Fed meeting on October 27-28 is a “live” meeting, meaning that a policy change could certainly occur at that time. But we continue to think the first move would best be accompanied by a press conference to offer context.

The next scheduled press conference follows the December 15-16 FOMC gathering; while the Fed could announce additional briefings, doing so next month might be taken by market participants as signal that a hike was coming.

Further, there is only one employment report before the next FOMC meeting. It seems unlikely that the uncertainty highlighted in today’s statement will be resolved in six weeks. Waiting until December affords the opportunity to digest three more unemployment reports and to assess any collateral economic damage that the slowing in Asia has produced. It also will allow a bit more communication from Fed officials to prepare markets for any change.

The Fed will therefore remain “data dependent.” While this is the most honest characterization of the Fed’s approach, it is also the least instructive for markets. As a result, the uncertainty surrounding monetary policy remains elevated.