Introduction

Choosing the most appropriate stocks for the common stock portion of your retirement portfolio is vitally important. In part 1 of this series I presented the 6 broad categories of stocks (businesses) that renowned mutual fund manager Peter Lynch presented in his best-selling book "One Up On Wall Street." I contend that the 6 categories that Peter Lynch wrote about establish a solid foundation of understanding of what’s generally available in the common stock universe. Additionally, I pointed out that these categories were very broad, and suggested that there were significant differences between the individual companies in each broad category.

In this part 2, I will elaborate on a few of the major differences in order to illustrate ways that investors can match the most appropriate stocks to their specific individual investment objectives. However, what I will be offering is more strategic in nature than specific. In other words, my objective will be to provide common stock investing strategies that investors can utilize and implement that are consistent with their specific goals, needs, objectives and risk tolerances. In my personal opinion, the idea that a stock should be chosen in accordance with specific investment objectives is paramount.

Is Your Primary Investment Objective Income or Growth?

In a similar fashion with which Peter Lynch presented his 6 broad categories of businesses, there are 2 primary but broad investment objectives that are generally appropriate for specific portfolios. These 2 broad investment objective categories are income and/or growth. However, these investment objective categories are usually not exclusive. In other words, for most every investor, both investment objective categories are often required. But, they will be appropriate at varying degrees or levels of importance for each individual investor.

For example, an investor already in retirement and thereby living off the income their investments are generating would obviously be more concerned with maximum income. In the same vein, it would be prudent to the already-retired-investor to also be concerned with having their income grow in order to keep up with inflation. Consequently, future income growth might take precedence over growth of capital. Of course, growth of both income and capital would be ideal.

In contrast, an investor planning for retirement, but with several years to go might be more concerned with both growth of capital and growth of income. The primary objective would be towards having the potential of a greater level of future income when it would be needed. And of course, there would be many unique investment objectives in between. Therefore, in my opinion, the key to choosing the most appropriate stocks is to choose those with the characteristics that offer the potential to meet your unique, individual and specific goals.

Moreover, in order to successfully accomplish your goals, the most critical first step is to clearly define them. Once your investment objectives and goals are clearly defined, it becomes much easier to focus only on common stocks that possess the appropriate characteristics consistent with those goals.

Help and Perspectives from Readers Comments

Serendipitously, I received a couple of comments on part 1 of this article series that I feel contribute greatly to the content of this part 2. The first comment I received shared the 8 stock types that MorningStar utilizes. Although MorningStar provided a couple of additional categories, for the most part, their stock types were consistent with what Peter Lynch wrote about.

Consequently, I offer the following comment, and as I did in part 1 and I present an example of each through the lens of F.A.S.T. Graphs™ that closely reflect the commentary following each MorningStar stock type. Importantly, these examples are not recommendations. These examples are only offered to illustrate examples of the various stock types that MorningStar suggests. Here is the comment with examples:

“For those interested in evaluating the diversification of their portfolios, as Chuck suggests, Morningstar utilizes eight Stock Types:

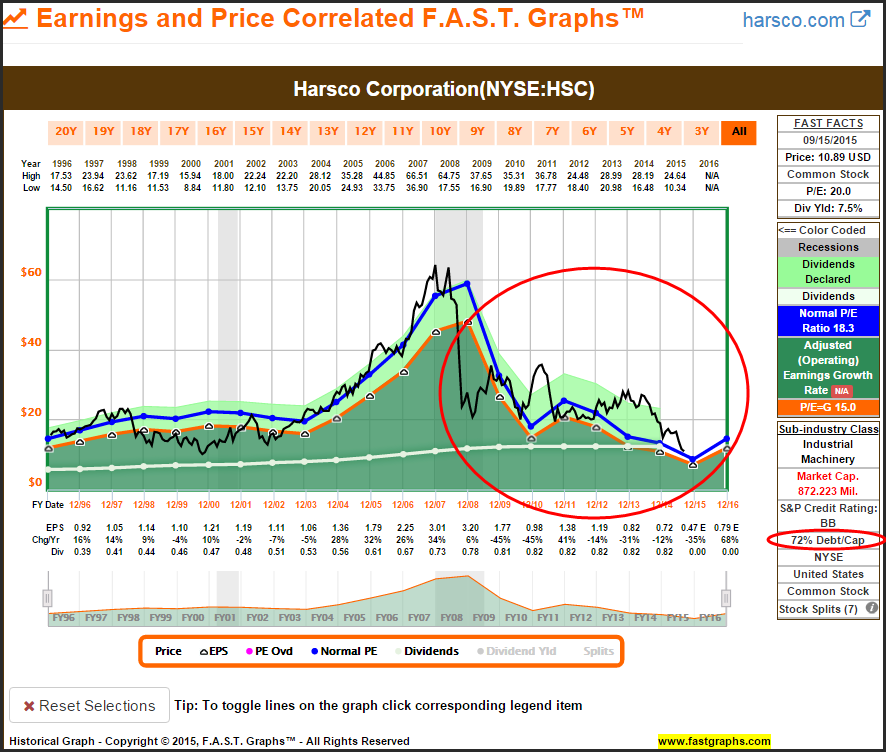

Distressed - Companies that are having serious operating problems. This could mean declining cash flow, negative earnings, high debt, or some combination of these. Such "turnaround stocks” tend to be highly risky, but also harbor some intriguing investments.”

Harsco Corp (HSC)

Harsco – Cash Flows

Harsco – Earnings

“High Yield - Companies whose stocks offer a high dividend yield. These tend to be mature companies that choose not to reinvest the bulk of their earnings. For investors interested in income, this is where to look.”

(Author’s note: I elected to provide 2 Dividend Aristocrat examples in this high yield stock type. However, because the focus here is on dividend yield, I present the first utilizing cash flows and the second which is a REIT utilizing funds from operations.)

Procter & Gamble (PG)

HCP Inc (HCP)

“Hard Asset - Companies whose main business revolves around the ownership or exploitation of hard assets like real estate, metals, timber, etc. Such companies typically sport a low correlation with the overall stock market, and have traditionally been where investors look for inflation hedges.”

(Author’s note: just as I stated in part 1, I found it difficult to find a hard asset play. Therefore, I offer the following example as a result and suggestion from another comment I received in part 1 of this series.)

“Asset play - look at Macy's (NYSE:M), a well run department store chain. They are sitting on $billions in real estate and an activist investor (Starboard Value) is pushing to divest. The downside of doing that would be to put a huge rent expense burden on future earnings. It will be interesting to see how it plays out.”

Macy’s Inc (M)

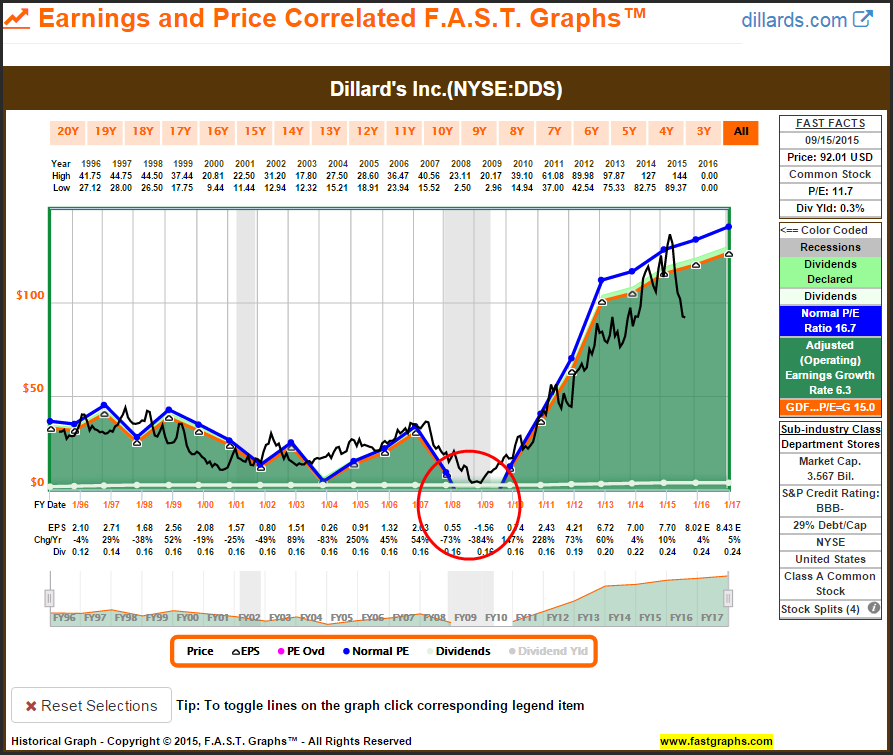

“Cyclicals - Companies whose core business can be expected to fluctuate in line with the overall economy. In a booming economy, such companies will look excellent; in a recession, their growth stalls and they might even lose money.”

Dillard’s Inc (DDS)

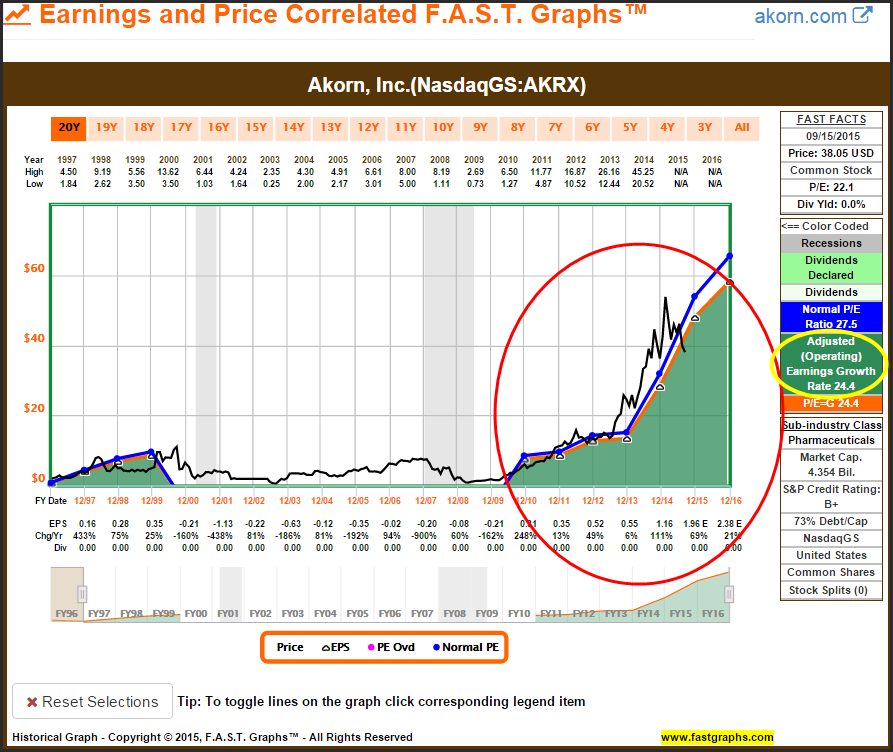

“Speculative Growth - Companies whose sales have grown very rapidly over the trailing five-year period, but whose earnings growth has been spotty. These tend to be companies in the early phase of their growth cycle.”

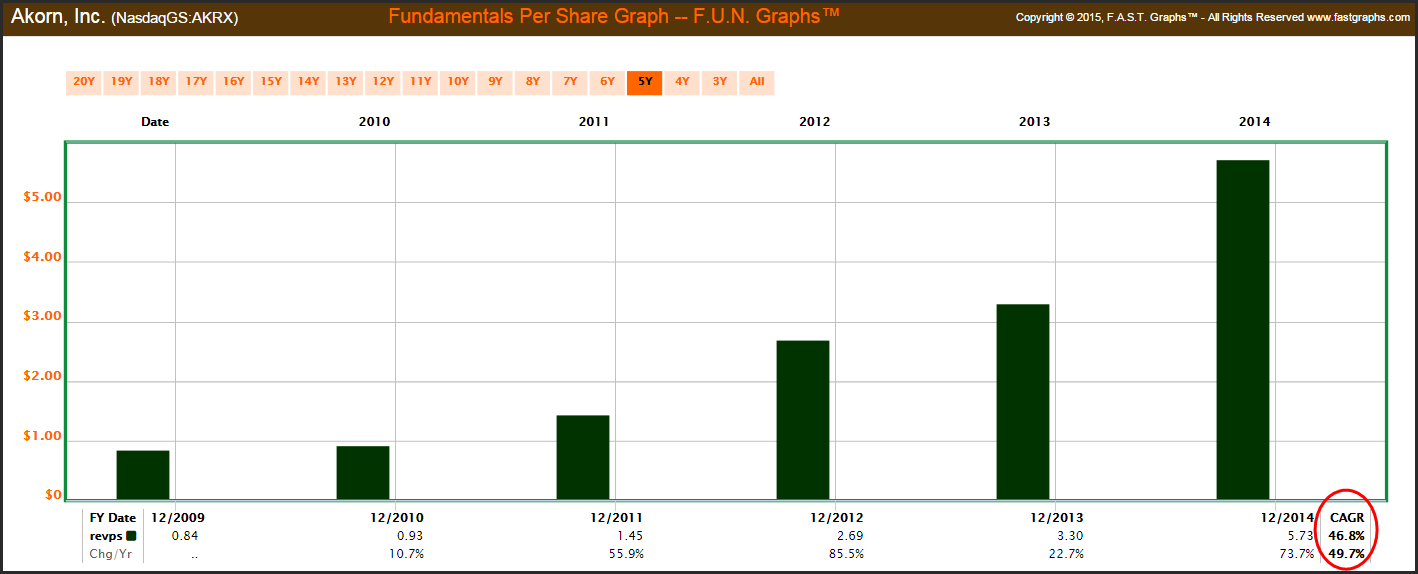

Akorn Inc (AKRX)

Akorn Inc revenues (sales) per share last 5 years:

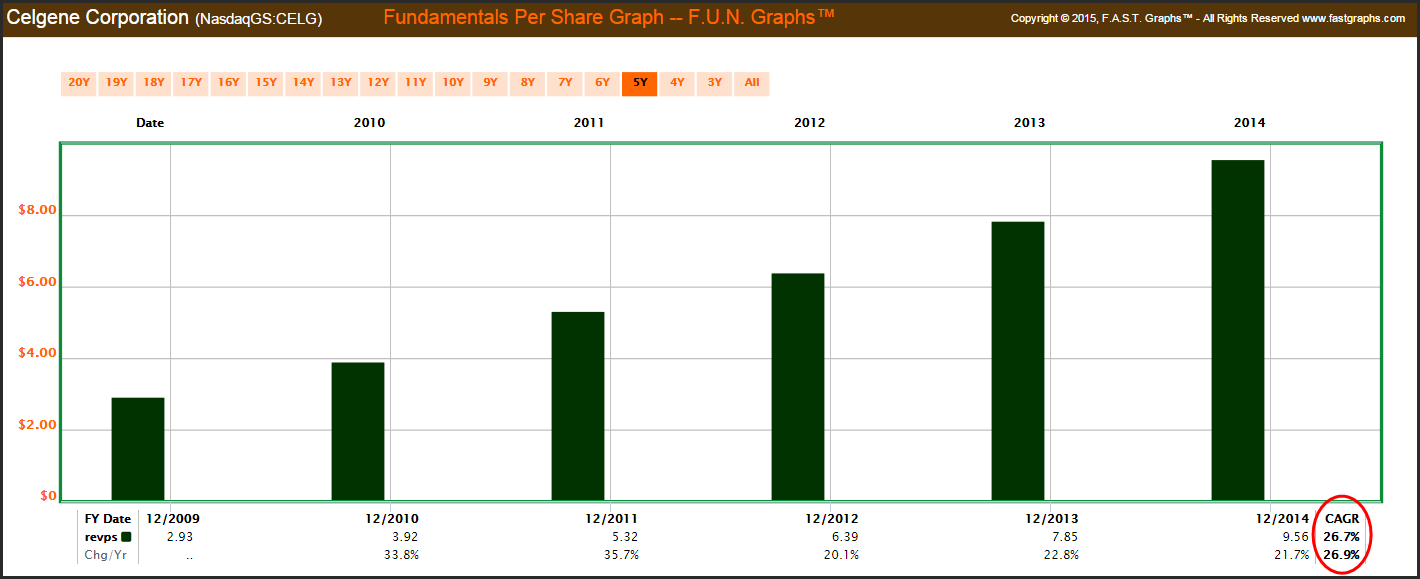

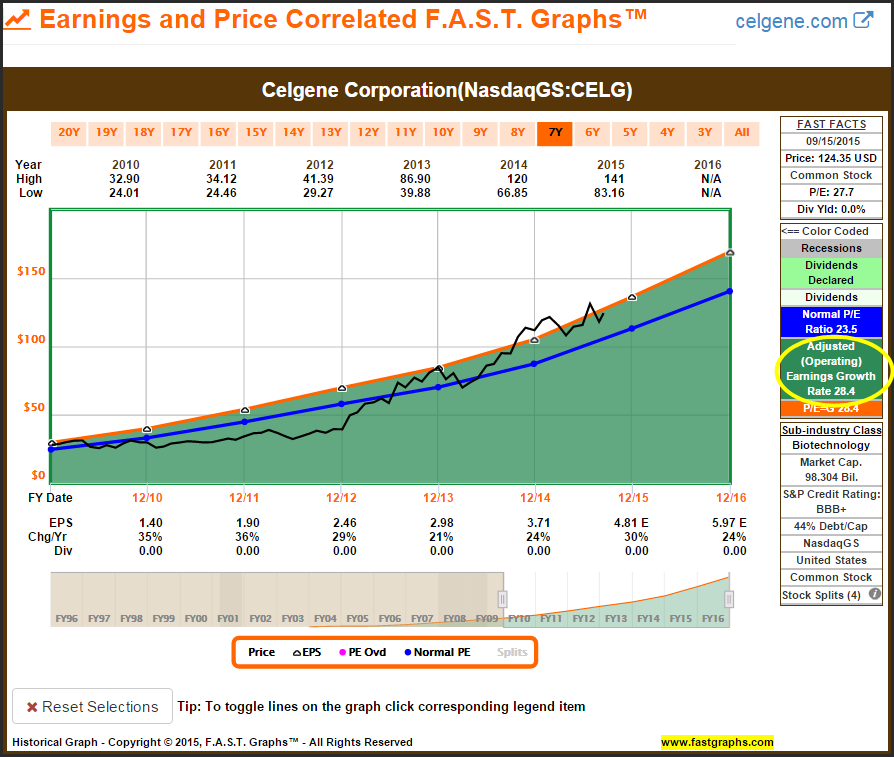

“Aggressive Growth - Companies whose sales and earnings have grown very rapidly over the trailing five-year period. These firms tend to be a step up the quality ladder from speculative-growth firms.”

Celgene Corp (CELG)

Celgene-revenues (sales)

Celgene-earnings

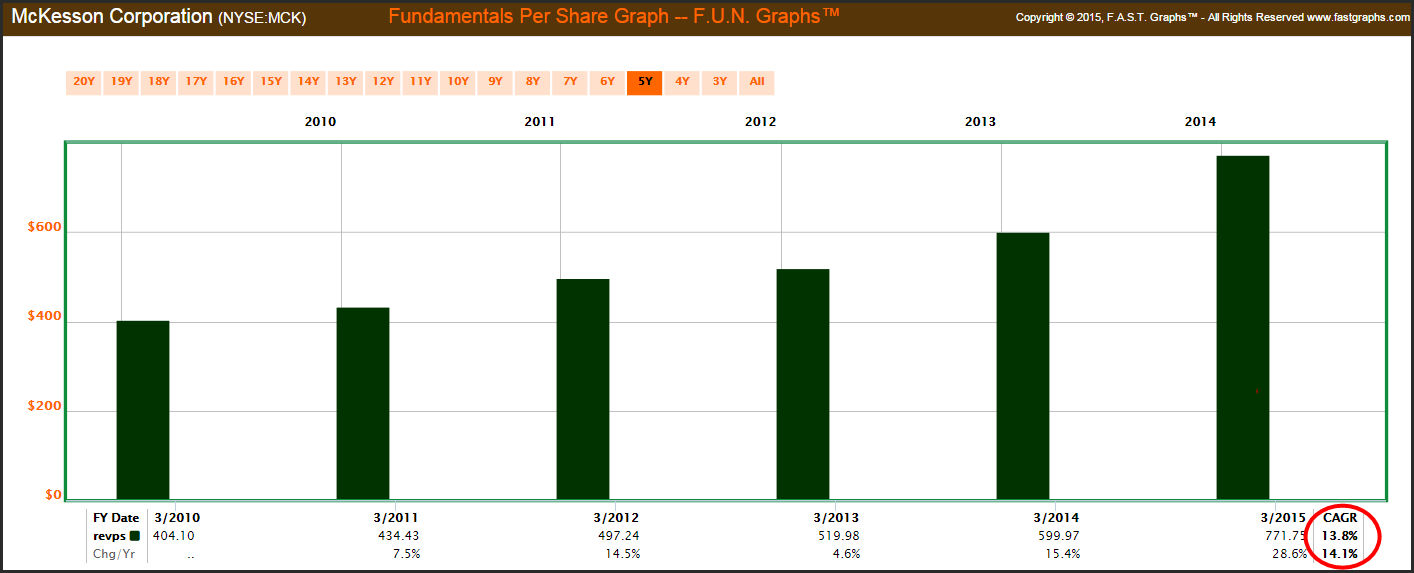

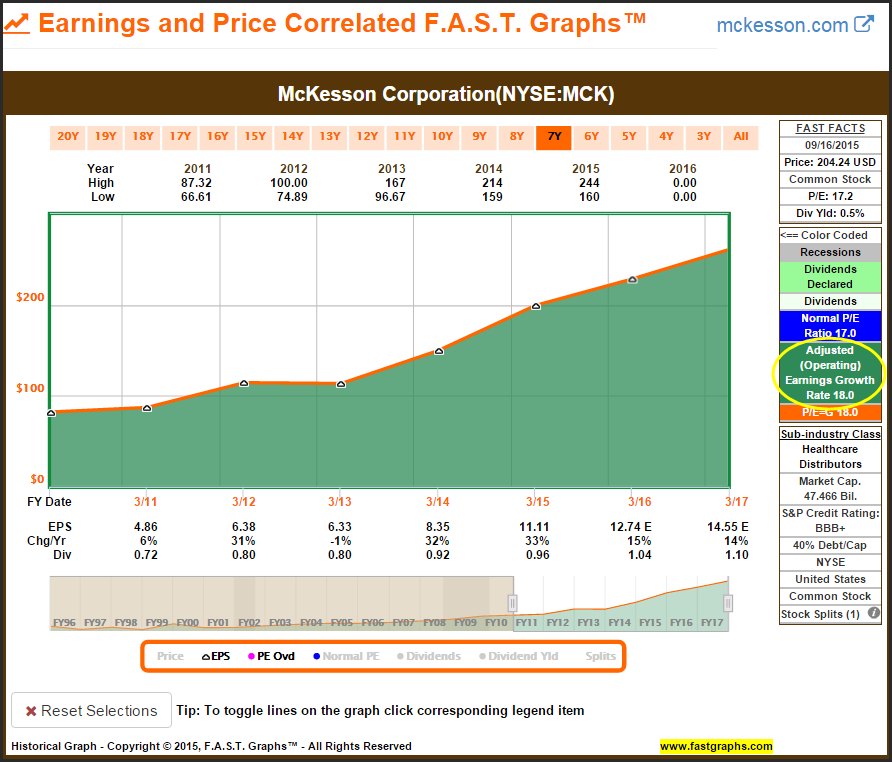

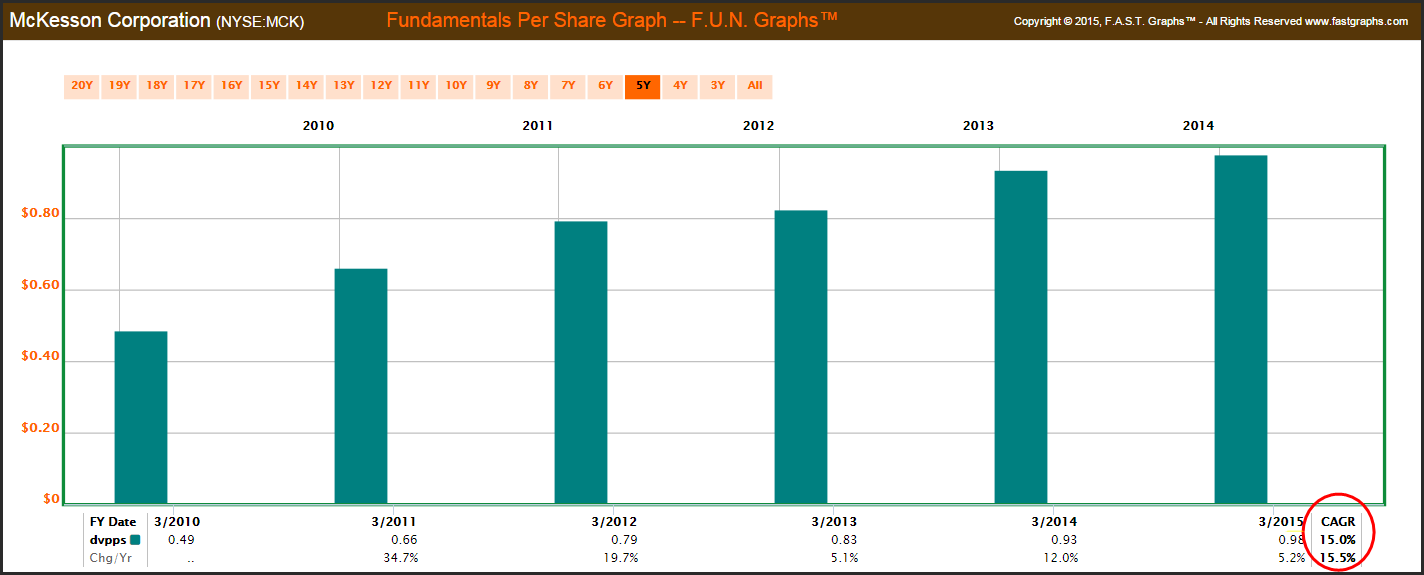

“Classic Growth - Companies that show moderate to rapid growth over the trailing five-year period in two of the following three categories: sales, earnings, dividends. These tend to be fairly mature firms, but ones that are still generating steady growth.”

McKesson Corporation (MCK)

McKesson revenues (sales)

McKesson Corporation-earnings

McKesson Corporation-dividends

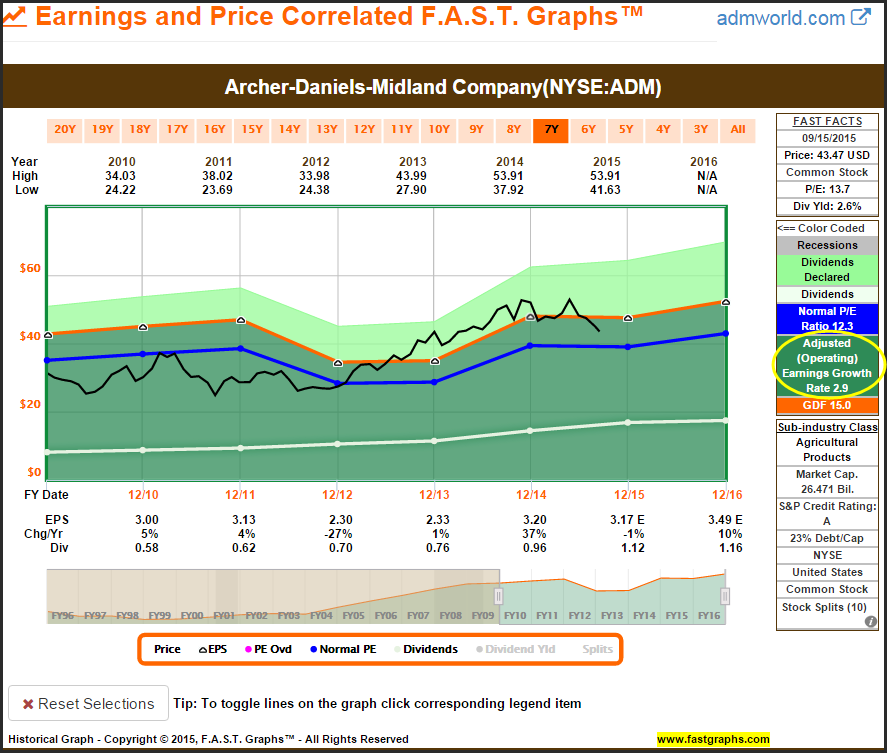

“Slow Growth - Companies that have grown slowly, if at all, over the trailing five-year period. These companies tend to be mature firms.”

Archer-Daniels-Midland Co (ADM)

The above 8 stock types from MorningStar with examples are offered to provide additional insights into what types of stocks are available for investors to choose from. Now that we have a perspective on what types of stocks are generally available, it’s time to move on to how they might fit into a retirement portfolio.

Ancient Portfolio Reality

My entry into the financial industry predated the ubiquitous acceptance of modern portfolio theory (MPT). Consequently, the way I was originally taught to construct portfolios was significantly different than what is being taught in the modern MPT era. Instead of designing portfolios by diversifying across numerous asset classes, I was taught to design portfolios based on meeting specific investment objectives. Therefore, I refer to what I originally learned as “Ancient Portfolio Reality.”

However, I do want to be clear before I go on any further. This series of articles relates solely to the equity portion of an investor’s portfolio. In other words, the focus is on how to construct a common stock portfolio in order to meet specific goals, objectives and needs. The equity portion could be a small or large percentage of an individual’s portfolio according to their own beliefs and risk tolerances. Nevertheless, this series of articles is only about strategies for building equity portfolios that make sense.

Getting back to my early teachings, I was schooled to think in terms of investment objectives and how they related to risk tolerances. Today equities are more often discussed in terms of value or growth and cap-size. For example, equity mutual funds are now given names such as US large-cap core, large-cap growth or value, mid-cap growth or value, etc.

In my early days, equity mutual funds were named more in accordance with their investment objective and risk. As I indicated earlier, the primary objectives that funds were named for related to income or growth. Consequently, equity funds oriented towards growth were often classified as conservative, moderate or aggressive growth funds. Likewise, equity funds oriented towards income were often classified as high, moderate or low yield offerings.

In the same vein, funds that were focused on both growth and income were also classified according to risk and/or their emphasis on either growth or income. These would be called something like aggressive growth and income, moderate growth and income or conservative growth and income.

The same investment objective orientation also applied to classifying individual common stocks. Personally, I found the old method of categorizing equities more rational because of the investment objective focus it provided. In other words, when I invested in an aggressive growth stock, I realized that I was investing aggressively and that my objective was for maximum growth.

Similarly, when I invested in conservative growth and income, I realized I was taking on less risk and that there was a dividend income component associated. Furthermore, I also recognize that I should expect a lower rate of growth because I was assuming less risk. The end result was that I felt I had a better perspective and understanding of what I was investing for as well as where my returns were coming from. With this invest by objective perspective, investing just seemed more logical and more appropriately focused.

This takes me to the second comment I received on my part 1 of this article series that I felt contributed to the theme of this part 2. With this comment, the reader shared his approach to how he picks his stocks. However, he referred to the fact that he used 3 categories, but in my mind he was discussing picking stocks by investment objectives as I discussed above rather than categories. Therefore, below I offer his comments and also include examples utilizing F.A.S.T. Graphs™ with an emphasis on the investment returns and their source:

“I use three categories for my stocks Income, Growth and Income, and Growth.”

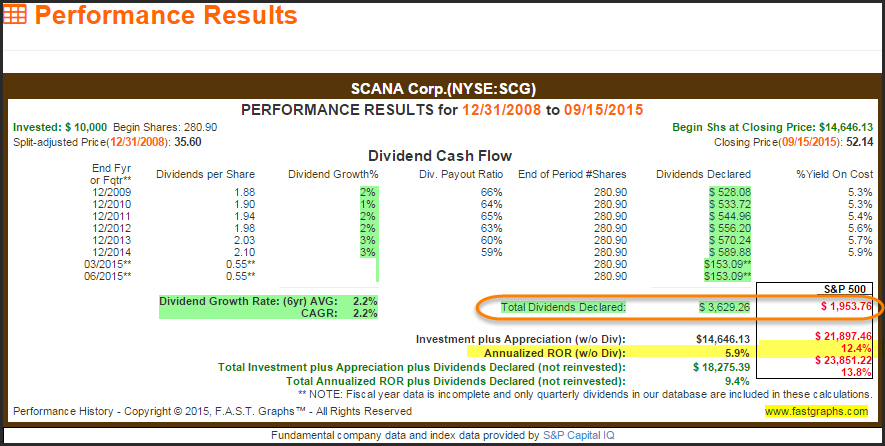

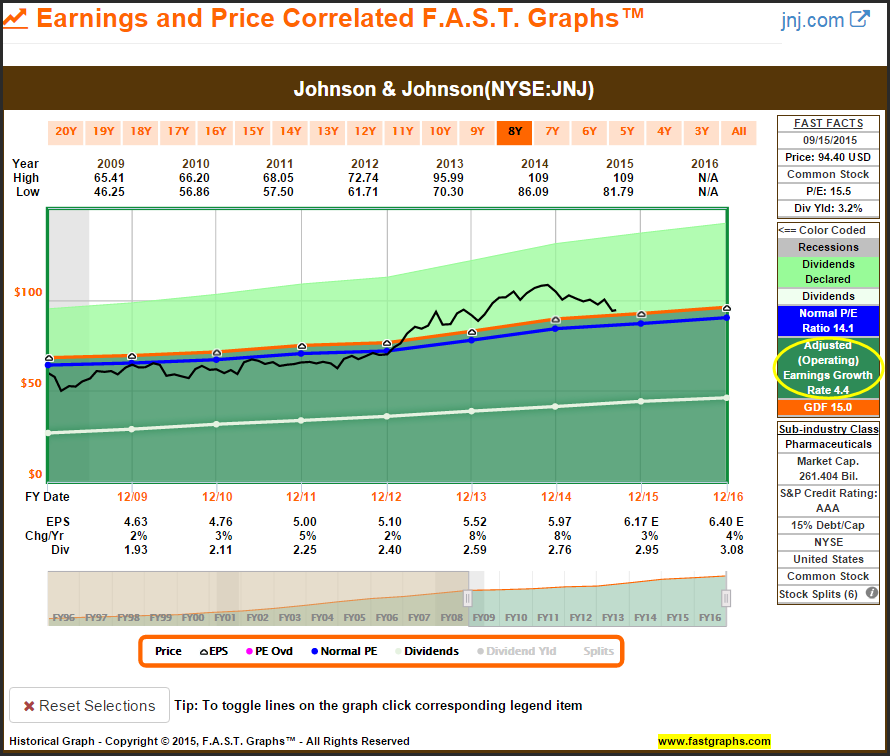

“Income Stocks (Slow Growers) are the stocks that I don't sell, have the dividends/distributions paid in cash (or reinvested) and collectively they produce a monthly cash flow when combined with social security and pensions to pay all the essential retirement expenses and what discretionary expenses that I have each month (call it minimum life style). Usually they would be higher yield say 2.8% and above. I do not have bonds so these are the reliable Cash Flow for me. These stocks may very well under perform the SPY index.”

Examples of Income Stocks (Slow Growers)

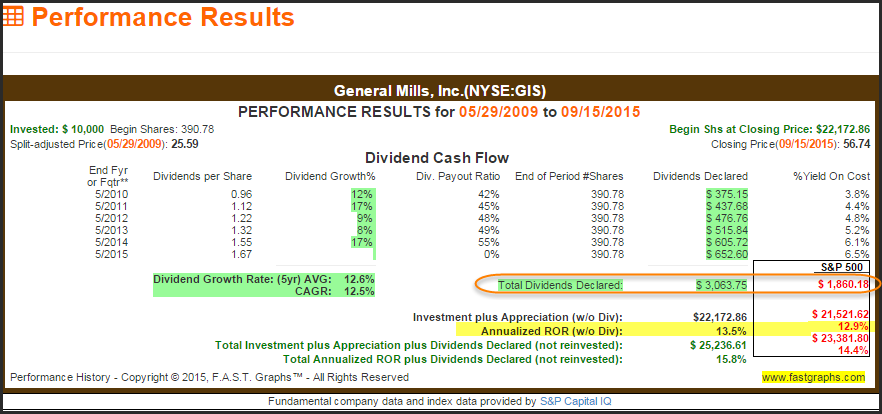

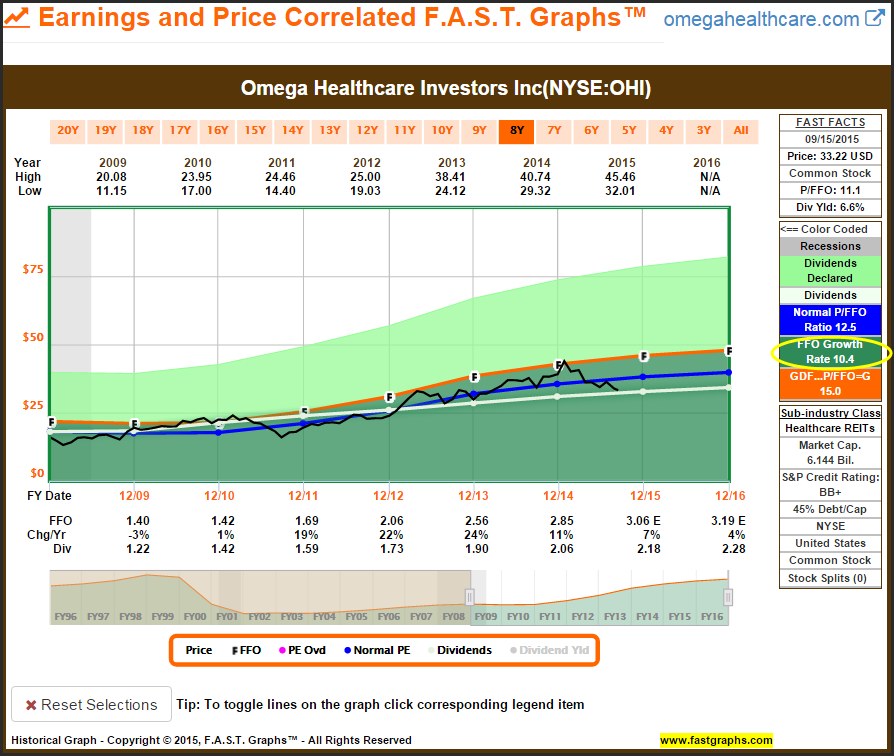

I believe the following examples reflect the “income stocks (slow growers)” that the above portion of the comment referred to. However, the emphasis here is on income, because not all of the following examples are necessarily slow growers. Note that most of them do underperform the S&P 500 as suggested on a capital appreciation basis, but also notice how they all outperformed the S&P 500 on a total dividends paid basis.

Scana Corp (SCG)

Johnson & Johnson (JNJ)

General Mills (GIS)

Omega Healthcare Investors Inc (OHI)

“Growth and Income Stocks would have a yield of 1% to 2.7%. They produce and add to the income but grow in value so if need be you can cover inflation on the pensions and extra discretionary expenses by selling some shares for cash or to buy more income stocks (expanded life style). Or just use the cash flow from the dividends for cash, reinvestment or other stock purchases. These stocks often beat the SPY index performance.”

Examples of Growth and Income Stocks

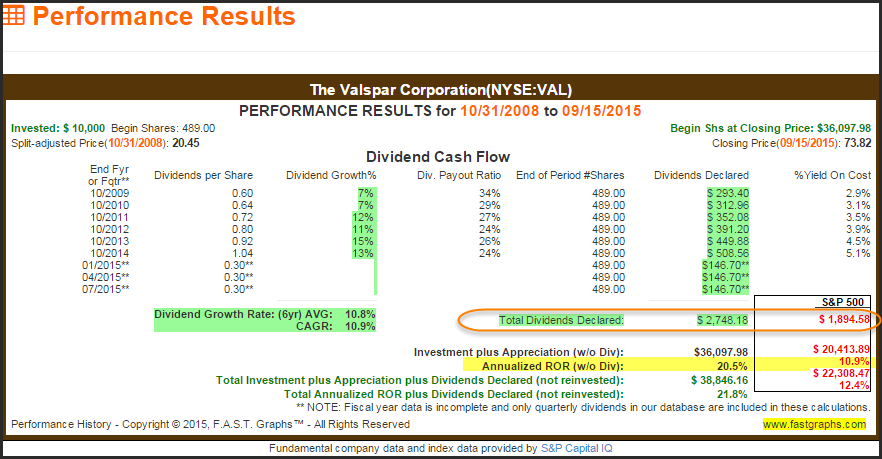

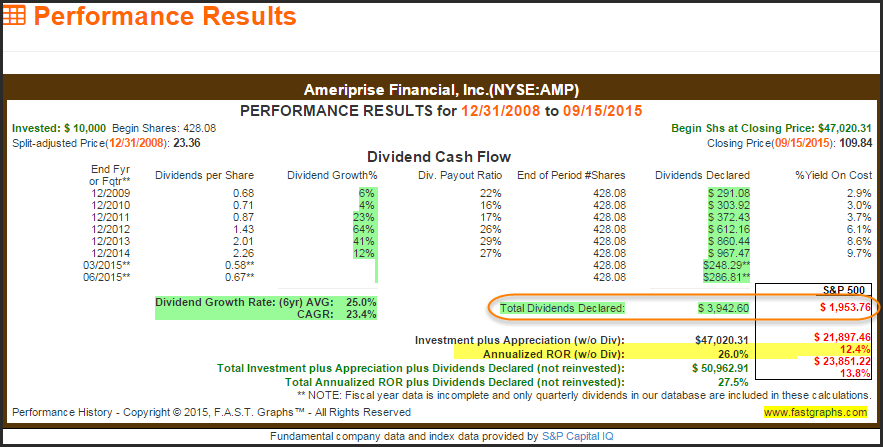

With these examples notice how the current yields are lower than the income stocks presented above, but also notice the higher rates of growth that each possesses. But even more interestingly, notice that they did beat the S&P 500 on a total return basis as suggested. However, I also found it significant that they also produced more total dividend income than the S&P 500.

Valspar Corp (VAL)

Ameriprise Financial Inc (AMP)

For anyone interested in seeing more examples of growth and income stocks, I recently wrote an article found here where I presented 12 that were also attractively valued.

“Growth Stocks yield 0% to 0.9% for wealth accumulation and emergencies such as medical bills, new car, maybe a big vacation, new roof for the house, etc. Because of volatility this may not produce reliable income exactly when I need it because for the most part they have to be sold to have any return (luxury life style). These stocks often beat the SPY index performance.”

Examples of Growth Stocks

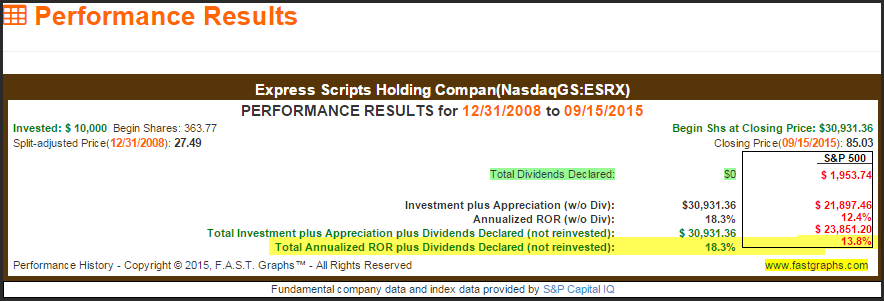

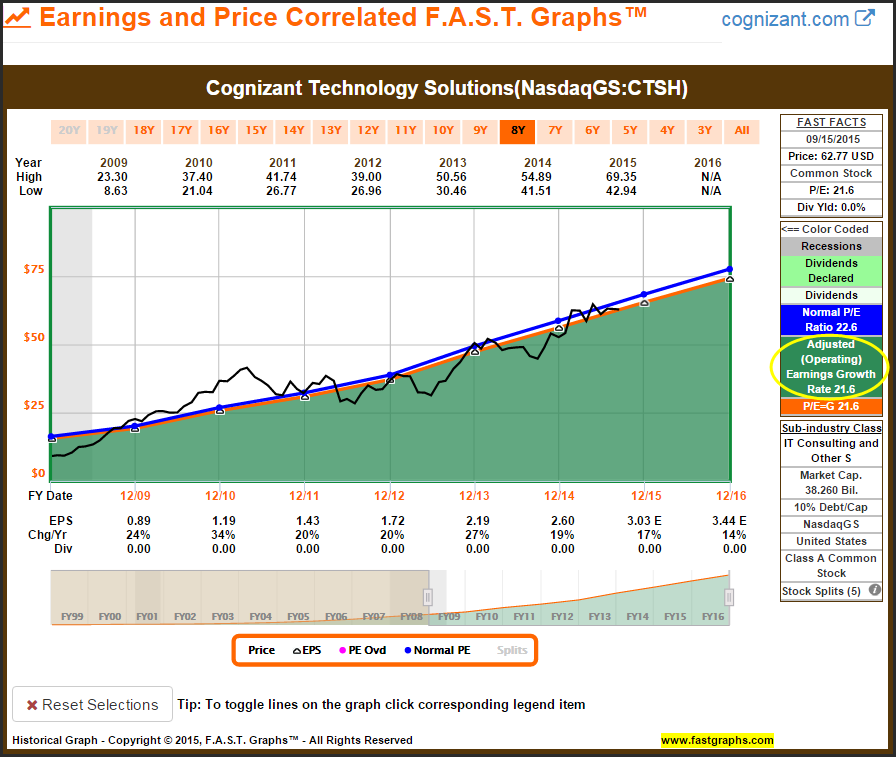

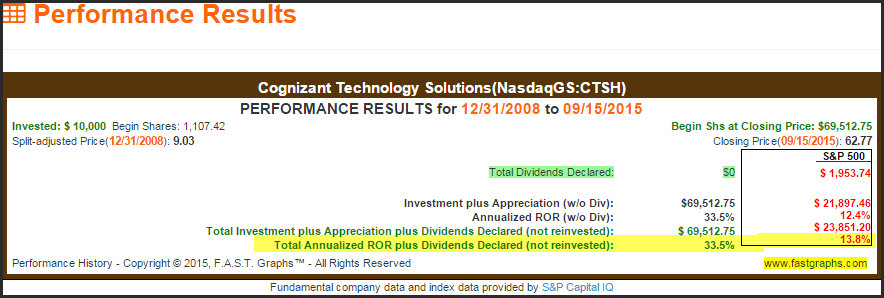

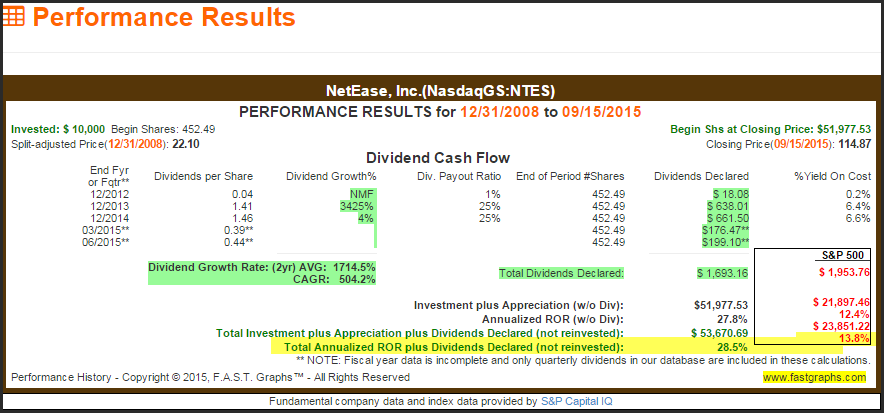

I generally agree with how the above comment depicted growth stocks. However, I would add that they are clearly riskier but the potential total returns they are capable of producing are often worth it. Each of the 3 examples below significantly outperformed the S&P 500 since the Great Recession. I consider this especially noteworthy considering that this period of time represents one of the S&P 500’s best performance achievements.

Express Scripts Holding Co (ESRX)

Cognizant Technology Solutions (CTSH)

NetEase Inc (NTES)

This final portion of the comment from part 1 of this series serves as a segue into what I will be covering in part 3. Here the reader offers some insights into what proportions of income stocks, growth and income stocks and growth stocks that he includes in his own portfolio. He also offers some insights into stock categories that he tends to avoid.

“So just guessing I might be 70% cash flow high yield dividend Income Stocks, 20% Growth and Income Stocks, and 10% Growth Stocks. Whereas the typical DGI person might be 90% high yield dividend stocks and maybe as much as 10% growth and income, and 0% growth stocks.

I see some subcategory classifications within my stock categories such as Stalwarts, Cyclicals and Turn-arounds. I am shying away from the Cyclicals and Turn-arounds and focusing more on Stalwarts with constantly growing earnings.”

Summary and Conclusions

In part 1 of this series I primarily focused on describing the primary categories of stocks available for investors to choose from. In this part 2 I elaborated more on the primary categories, but also offered some perspectives on how they fit specific investment objectives. In the next, part 3, I will present several examples of specific strategies on how these categories can be utilized and implemented towards building successful long-term equity portfolios. But most importantly, I will be presenting various strategies that accommodate different levels of risk tolerance as well as objectives and needs.

Obviously I will not be presenting every possible portfolio construction strategy that exists. That would be impossible, because the options are virtually infinite. However, I will be sharing strategies that I have personally utilized successfully, as well as strategies that many of the world’s most renowned and successful investors recommend. At the end of the day, my primary objective for presenting this series of articles is to assist the reader in thinking logically about how they construct the equity portion of their portfolios.

Disclosure: Long OHI,CTSH,ESRX,AMP,HCP,PG,SCG,ADM,JNJ,GIS at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.