An initial increase in short-term interest rates is apparently still on the table at this week’s Fed policy meeting, but it’s more likely that we’ll see a delay. That may not ease the stock market’s concerns, as officials are expected to remain committed to raising rates at some point in the near future.

Fed arguments fall into four camps. The first believes that the economy has reached full employment and that the Fed is behind the curve. This is largely the same group of people who have been crying wolf on inflation the last few years. This time, they believe they are right. The second group sees more slack in the job market. The lackluster pace of wage growth suggests that the recovery has a lot more room to run before the Fed has to start reining it in. The third and fourth groups share a common belief – that is, that the timing of the initial move doesn’t really matter much. Group 3: “so why not start raising rates now?” Group 4: “so why not delay for a little longer?”

There is widespread agreement that short-term interest rates will have to be raised at some point and a consensus view that the pace of subsequent rate hikes is likely to be very gradual. The Fed has made public its normalization plans. The only question is the timing. We’ve seen a substantial reduction in the amount of slack in the labor market over the last couple of years. The Fed needs to set policy based on where the economy is expected to be 12 to 18 months from now, and there should be a lot less slack. The Fed doesn’t have to be at neutral at that point, but it ought to be closer to neutral than it is now.

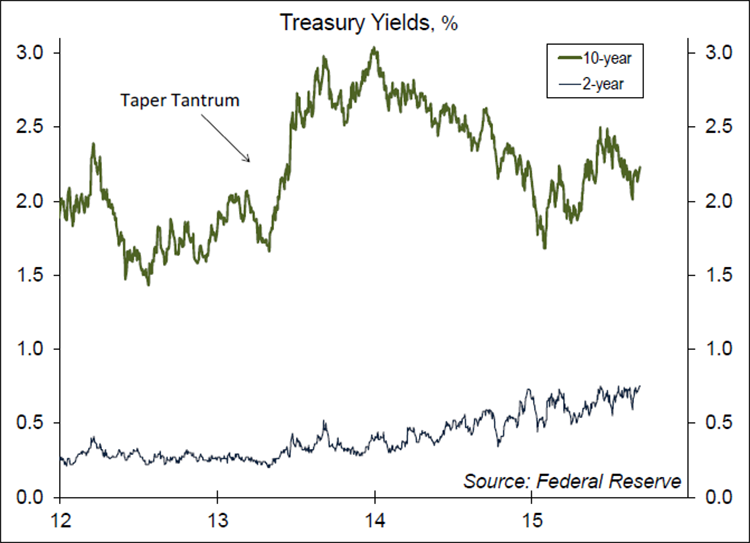

If not for the recent global financial turbulence and concerns about growth in emerging economies, the Fed would almost certainly have begun raising rates this week. The direct impact of slower growth abroad on the U.S. economy should be relatively limited, but it depends on the magnitude. Consumers and businesses should benefit from the decrease in commodity prices (as we saw in the Asian financial crisis in the late 1990s). In 2013, the financial markets experienced a “taper tantrum” when the Fed began talking about reducing the monthly pace of asset purchases in QE3 ($85 billion at the time). Bond yields rose and emerging markets experienced volatility. The Fed ended up delaying the taper, but it did eventually taper.

As Fed tightening approaches, the bond market has been relatively calm. However, emerging economies have stumbled and experienced capital outflows. Strains may pick up and capital outflows may get worse if the Fed hikes. The Fed has to set policy based on the domestic economic outlook, but does consider possible feedback from the rest of the world.

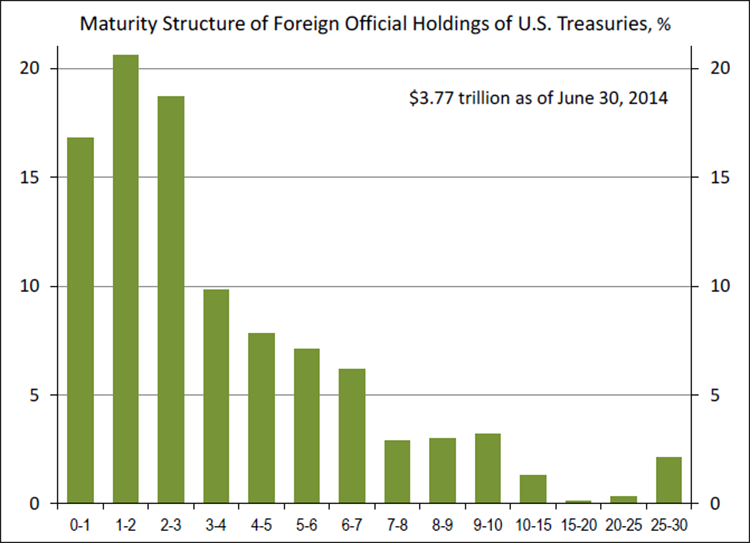

Some fear that emerging economies, China especially, will dump Treasuries, putting upward pressure on bond yields. However, foreign central bank holdings of U.S. Treasuries are concentrated at the short-end of the yield curve. Long-term rates ought to move higher as the economy strengthens, but central bank selling should not be an issue.