Global Economic Perspective: September

US Federal Reserve Moves Toward Gradual Policy Normalization

With the US gross domestic product (GDP) growth rate for the second quarter raised significantly higher to an annual rate of 3.7%, the US economy is showing renewed signs of vigor. The revision was largely thanks to consumer spending, but business and residential investment were also stronger than previously estimated. Various other data points suggest that growth has continued in many parts of the US economy during the summer months. Consumer spending rose solidly in July as households stepped up automobile purchases. Job report figures have remained buoyant, which, along with low oil prices, are ensuring that consumer sentiment is strong. As for business investment, durable goods orders for July significantly exceeded consensus expectations. Other positive signs abound, ranging from a seven-year high for construction spending in July to a rebound in labor productivity in the second quarter.

Of themselves, recent figures would almost certainly enable the US Federal Reserve (Fed) to begin to normalize monetary policy. The Fed has a dual mandate to achieve maximum sustainable employment and stable prices. Initial estimates for job gains in August were relatively disappointing—but figures for June and July were revised upward, and August numbers in previous years have tended to be revised higher. Just as importantly, with unemployment now down to 5.1%, the Fed is very close to fulfilling the first of its mandates. A broader measure of labor market slack, the number of people who are in part-time employment but would like a full-time position (the U-6 underemployment rate), has also been drifting lower (to 10.3% in August).

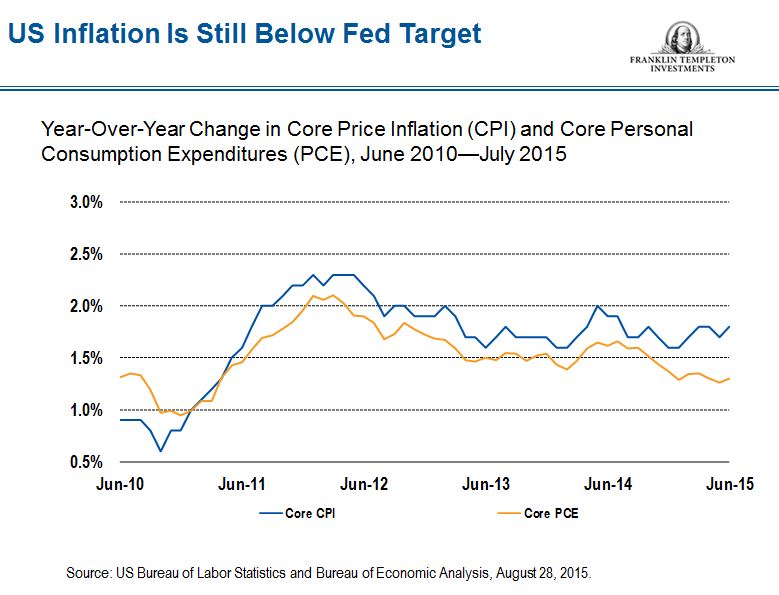

The picture is a little hazier regarding the other part of the central bank’s mandate. Inflation and inflation expectations overall remain well below the Fed’s target. Wage inflation in particular has been notable by its absence. However, the August nonfarm payroll numbers saw hourly earnings accelerate at an annual pace of 2.2%, well up from 2.1% in July. As for inflation in general, Fed Vice Chairman Stanley Fischer has said that there is “good reason” to believe that inflation will move back up to the Fed’s annual target of 2% as the US economy’s untapped capacity gets used up and as the effect of the big dip in oil prices in the second half of 2014 wears off. It is worth noting that the core Consumer Price Index (excluding food and energy) stood at a year-on-year rate of 1.8% in July, and that the Fed may be content to see inflation at least trending upward—without necessarily hitting 2% in the near term—before deciding to act. So, with the US economy now expanding at a reasonable, albeit unspectacular, rate, now may be the time to nudge interest rates up from near zero, thus providing some room for policymakers to lower them again should circumstances warrant. And how better for the Fed to underline its confidence in the US economy’s prospects?

However, while the Fed’s mandate does not extend to reacting to the vagaries of the currency market or the dynamics affecting other economies, recent US dollar strength and wobbles in risk assets caused by concerns over the state of the Chinese economy cannot be entirely ignored. The volatility seen in recent weeks means that rate tightening is a fretful decision to take. However resilient the US economy, the slowdown being experienced in Asia and Latin America may force the Fed to lower its growth outlook (in June, the central bank announced a reduction in its so-called “central tendency for growth” through 2017) and could dent confidence that inflation will accelerate toward the Fed’s target within a reasonable time frame. Data from the Institute for Supply Management, along with other statistics, suggest the US economy continues to be driven by the services sector, whereas growth in manufacturing (outside the buoyant auto sector) showed signs of slowing in August, possibly due to dollar strength and weakening economic prospects outside the United States.

Nonetheless, while the Fed is facing an extremely delicate task—and the job of effectively communicating its intentions will be even more delicate—it is still our belief that the US economy remains sufficiently strong to be able to bear a gradual increase in short-term rates in the coming months. While the growth outlook for the United States looks comparatively subdued compared with historical trends, we further doubt whether expansionary monetary policy can do much more to improve prospects. While base rates kept at or close to zero for almost seven years and three massive asset-buying programs by the Fed have undoubtedly helped stabilize the US (and world) economy during and after the recession that followed the global financial crisis, the continuation of expansionary monetary policies is now supporting a growing excess of global liquidity that has been distorting the market signals sent by stock and bond prices and thus contributing to the growing volatility seen in recent weeks.

A Nuanced View of Global Prospects

The volatility of recent weeks would seem to make it a less-than-auspicious time for the Fed to consider raising interest rates, at least from a global perspective. Thoughts of a rate rise in the United States have contributed to the selloff in a range of currencies and to capital outflows from emerging markets. And global sentiment has not been helped by developments in China. The Chinese economy is slowing (worryingly, opinion differs as to how much), maintaining downward pressure on commodity prices, while Chinese stock prices continued to tumble in August in spite of huge intervention by the authorities. Markets were also taken aback by an August decision to allow the yuan to float more freely against other currencies, effectively amounting to a devaluation.

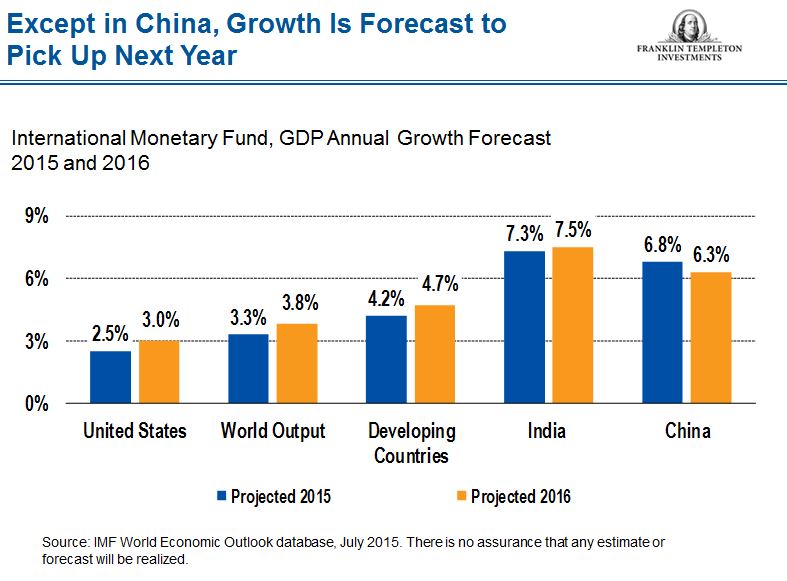

The combination of depressed commodity prices, a Chinese devaluation and the growing possibility of a rise in US base rates has meant that emerging-market assets in general have been having a rough time. Conditions have also contributed to a declaration from the International Monetary Fund’s (IMF’s) managing director, Christine Lagarde, that global economic growth this year is likely to be weaker than the IMF’s July forecast of 3.3%.

Emerging markets certainly find themselves in a dilemma. Stumbling growth in a number of countries plus Beijing’s decision to devalue its currency might dictate policy easing in response. And yet the prospect of Fed tightening makes this difficult for countries that are already facing significant drops in the value of their currencies. At the same time, having abandoned currency pegs, the most significant emerging markets have (so far at least) managed to avoid raising rates in the teeth of slowing growth. While there has been a somewhat indiscriminate run on the currencies and stocks of emerging markets, fundamentals remain intact in many countries where currency reserves have grown exponentially since the Asian crisis of 1997–1998. Learning from previous crises, countries such as Mexico, Brazil and India have transformed their government debt markets, inuring themselves to global economic shocks by limiting their borrowing in non-domestic currencies. According to research carried out by Moody’s across the world’s biggest emerging markets, the share of debt held in a country’s own currency has jumped from just over 50% to just under 75% in the past 15 years.1

That still leaves a number of countries facing issues. The ones suffering most from the present bout of market angst are those that have deep-rooted political problems and/or large current account deficits with large external funding needs funded through dollar-denominated debts. Some concerns surround US dollar-denominated corporate debt, which has risen steeply over the past two years in emerging markets to benefit from low US interest rates. This may indeed be an area that bears extra attention. A tightening of emerging-market credit is already under way and corporate borrowing costs show signs of rising, adding further to the downward pressure on global growth. But the IMF forecasts better growth in 2016, and even its forecast for global GDP growth of over 3% this year is still not far off long-term trends, with annual real GDP growth hovering around 3.5% throughout the mid-1980s and again in the mid-1990s, according to the IMF Data Mapper.

We also believe it pays to keep the situation in China in perspective. It remains our view that China’s economy is in the midst of a transition to a new, more domestically and market-focused economic model that is leading to slower but more sustainable growth than in the past. While this transition—together with official attempts to unwind the risks built up in recent years in the form of industrial over-investment, banks’ bad debts and property bubbles—is proving complex and unsettling, China continues to grow at a rate well superior to that of any of the leading developed economies. Its official figure for manufacturing activity in August (49.7) was the worst for three years and caused renewed anguish in markets. However, the equivalent gauge for the increasingly important nonmanufacturing part of the economy came in at 53.4 in August, well above the 50 mark that separates expansion from contraction.

In substance, we believe that China is facing an uneven economic trajectory but that growth is far from collapsing. Certainly, the housing sector has declined as the authorities have clamped down on speculation (although there are signs the housing sector might be bottoming), while local government and manufacturing-related sectors are having to face the consequences of years of overspending and overinvestment. At the same time, changing labor and demographic dynamics are pushing wages higher. This is having a negative effect on China’s competitiveness at the very low end of the value chain, but higher wages are feeding into higher consumption, while the authorities continue to target transportation and environmental infrastructure for investment. These elements are turning China into a more sophisticated, more domestically focused economy and will have a far bigger effect on China’s prospects—and indeed on world prospects—than the short-term gyrations of the much-manipulated Chinese stock market.

Furthermore, the People’s Bank of China has slashed interest rates several times since November and progressively eased banks’ reserve requirements to enable them to lend more freely. At the same time, the authorities in recent months have rolled out a series of tax breaks and accelerated approvals for infrastructure projects. We believe that it is reasonable to expect that the effect of all these measures will be felt progressively in the coming months and help contribute to improving global sentiment.

Europe Faces Up to Lackluster Growth

Having gotten through yet another Greece-related institutional crisis (at least provisionally), the eurozone economy continues to grow, albeit modestly. Second-quarter GDP growth came in at a quarter-over-quarter rate of 0.4% in the three months to end-June, the same as in the previous two quarters. Spain has continued to shine and Italy has improved, but France has stagnated. Overall, some other measures suggest a general improvement in the eurozone’s economic prospects. Year-on-year growth rose to 1.5% in the second quarter from 1.2% in the first. Unemployment unexpectedly fell to its lowest level in more than three years in July, with a sharp decline in Italy, where important reforms to the labor market are beginning to kick in.

Eurostat stated that eurozone unemployment was 10.9% in July, the first time it fell below 11% since February 2012, while a range of leading indicators (such as the Markit composite purchasing managers’ index, the European Commission’s Economic Sentiment Index and money supply data) suggest growth has continued apace in the third quarter. The strength of lending demand is especially encouraging and has been met by a drop in borrowing costs for businesses and households in countries such as Italy and Spain, while a further downturn in oil prices in July and August should help to boost spending.

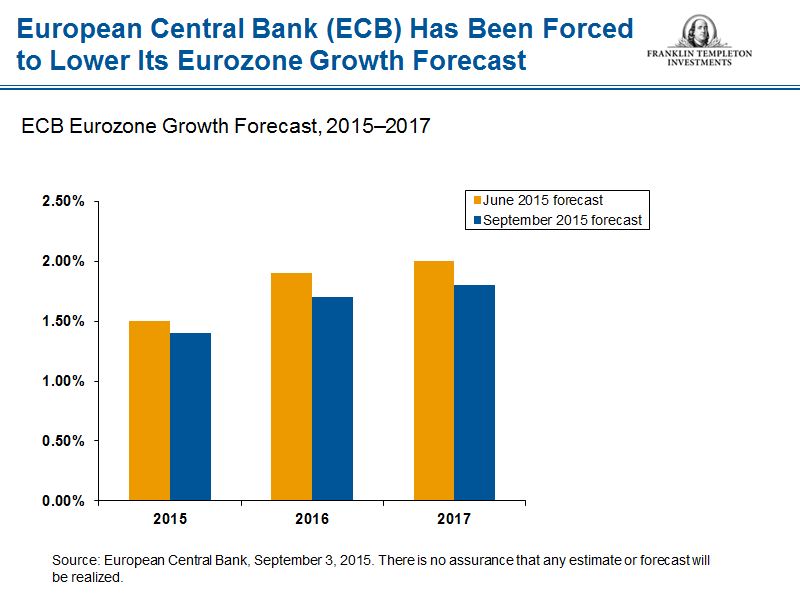

However, annual growth of 1.2% must be considered disappointing when seen in light of the various forms of stimulus provided by the European Central Bank (ECB) and by the drop in energy prices. While Europe’s prospects have been hurt by sluggish global growth, questions are being raised about the effectiveness of the ECB’s quantitative easing (QE) program, which has seen it acquire about €60 billion in assets each month since March. Not only were the second-quarter GDP figures somewhat disappointing, but inflation has remained quite low even though the eurozone pulled its way out of a short period of deflation seen at the beginning of this year. Headline inflation in the 19-country eurozone was just 0.2% in the year to end-August, according to Eurostat, while core inflation (excluding food and energy) was 1%, well off the ECB’s inflation target of just below 2%. Until recently, the ECB had been relatively relaxed about inflation.

As recently as June, its belief in Europe’s economic revival led it to forecast that core inflation would move up to 1.5% in 2016. However, in early September, this prognosis was pared back significantly to just 1.1%—still nowhere near the ECB’s 2% target. The ECB explained this downgrade to its inflation forecast by citing global growth uncertainties, the general tightening of financial conditions and falling oil prices. Low inflation and uncertainties about the global economy also forced the ECB to revise its forecast for 2015 eurozone growth from 1.5% to 1.4%. Concerns about emerging markets also fed into a short-term spike in the value of the euro against the currencies of its main trading partners, threatening the export-led recovery of the major eurozone countries.

The ECB has come under pressure to respond to all of these negative dynamics. Thus, its president, Mario Draghi, committed the bank to beefing up its QE package through an extension of the program’s “size, composition and duration” should the global market turmoil and emerging-market slowdown threaten the eurozone’s recovery. But, as things stand, the jury is still out on the effectiveness of monetary policy alone in heading off the disinflationary forces imported from China and its ability to push growth in any meaningful way beyond the present trajectory. Much more of the burden for improving Europe’s growth prospects looks to be falling on national governments.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

_________________________________________________

1 Source: Moody’s Investors Service, September 1, 2015.

© Franklin Templeton Investments

© Franklin Templeton Investments