The August employment figures were mixed. Payrolls rose less than anticipated, but with an upward revision to the two previous months. The unemployment rate fell more than expected, while average hourly earnings ticked a little higher than anticipated – providing the Fed’s hawks some ammunition in arguing for a September 17 rate hike. The Fed is not going to react to any one economic report, but the jobs data fall in line with the broader range of indictors that suggest that slack is being reduced. Looking ahead to where the economy is likely to be 12 to 18 months from now, there are strong arguments for the Fed to begin the process of policy normalization. Global market volatility may lead the Fed to delay, but the Fed can’t wait until all the seas are smooth and the weather clear.

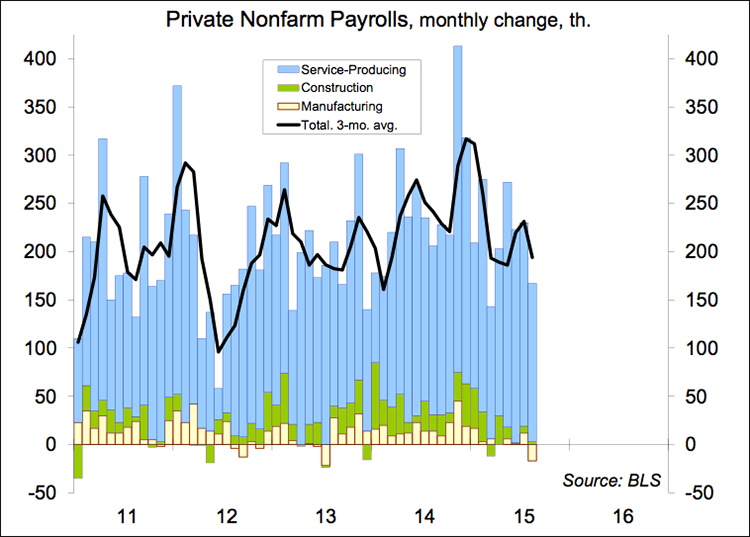

Nonfarm payrolls averaged a 221,000 monthly gain for June, July, and August (vs. a +250,000 average over the previous 12 months). Payroll figures can be choppy from month-to-month due to difficulties in seasonal adjustment. The three-month average reduces (but does not eliminate) that noise.

Employment in manufacturing fell by 18,000 in August. While there is a fair amount of noise in the monthly figures, factory sector jobs have trended roughly flat this year (after rising 1.8% in 2014), apparently reflecting the impact of a strong dollar and softer global growth. The ISM Manufacturing Index has been low, but still above the breakeven level in recent months.

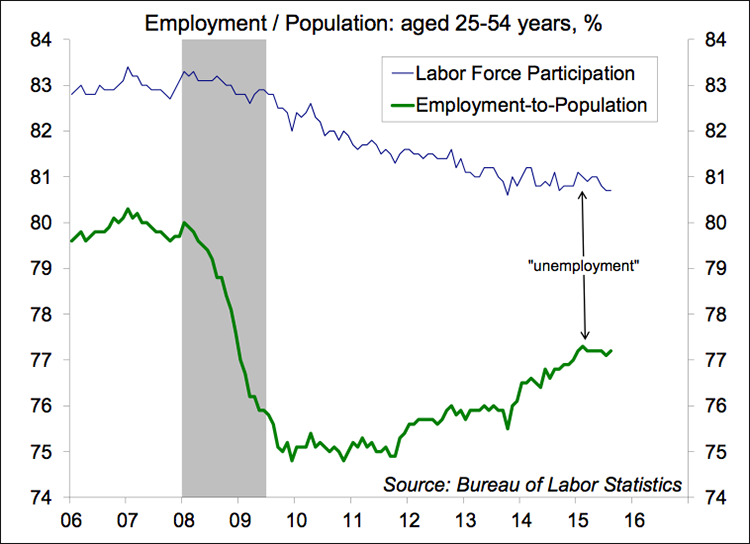

The unemployment rate fell to 5.1% in August, the lowest since April 2008, and a level once considered to be the natural rate of unemployment. Since peaking at 10% in October 2009, much of the drop in the unemployment rate has reflected a decrease in labor force participation. Some of that is due to discouraged workers, who have given up looking for a job and are no longer officially considered as “unemployed.” However, the Fed believes that most of the decline is demographics.

As the population ages, labor force participation should decline. However, lower participation is also apparent in the key age cohort (25-54), which should be less susceptible to changing demographics. The employment/population for the key age cohort has been trending higher in the last few years, but has been trending roughly flat in recent months – at odds with the continued strength seen in nonfarm payrolls.

Other labor market indicators have remained consistent with improving labor market conditions and a reduction in slack. Weekly claims for unemployment benefits have continued to trend at a low level and short-term unemployment rates are low, both consistent with normal labor market conditions. Long-term unemployment and the percentage of people working part time but preferring full-time employment are still relatively high, but have been improving.

The Fed sets monetary policy not on the past, but on the expected future. At the current pace of improvement, the job market will be a lot tighter in 12 to 18 months. The entire path of interest rates matters more than the timing of the initial move. That pace (of rate hikes) is expected to be gradual, but can be adjusted if growth is stronger or weaker than expected.

“I am well aware that, when the Federal Reserve tightens policy, this affects other economies. The Fed's statutory objectives are defined in terms of economic goals for the economy of the United States, but I believe that by meeting those objectives, and so maintaining a stable and strong macroeconomic environment at home, we will be best serving the global economy as well.” – Vice Chair Fischer, August 29

Fischer’s Jackson Hole speech (and his interviews with the press) made it clear that central bank officials remain intent on starting the normalization process this year. As with the 2013 taper tantrum, adverse conditions may lead to a delay in policy action, but not a permanent postponement.