On The Economy, Inflation, China & Odds For Fed Liftoff

IN THIS ISSUE:

1. August Unemployment Rate Fell to Seven-Year Low

2. US Economic Outlook For the Second Half of 2015

3. Inflation Still Running Well Below the Fed’s 2% Target

4. Stronger Dollar Could Hamper Growth This Year & Next

5. New China Economic Data Point to Further Slowdown

6. Fed Funds Rate Futures Show Odds For Sept. Rate Hike

Overview

The investment markets remain fixated on whether the Fed will hike interest rates for the first time in almost a decade on September 17. Stock market volatility spiked in late August and so far this month, with most global equity markets in “correction” territory. It remains to be seen if the latest stock market chaos will cause the Fed to delay lift-off until December or later.

Other than global equity market weakness and below target inflation, other factors that would lead the Fed to tighten are in-line, although last Friday’s unemployment report for August could have been stronger. Today, we will examine the August jobs report, the strength of the US economy in general, inflation trends and the outlook for the US dollar. We’ll also take a look at the latest disappointing economic news out of China.

We’ll end today with a look at the Fed Funds rate futures market to see what the probability is for a rate hike next week. At the end of last week, Fed Funds futures indicated an 81% chance of a rate hike on September 17, up from a 74% chance in August.

It’s a lot to pack into one E-Letter, so let’s get started.

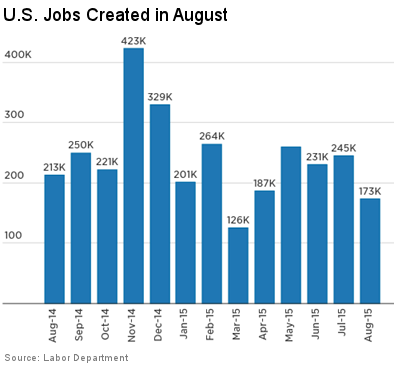

August Unemployment Rate Fell to Seven-Year Low

The Bureau of Labor Statistics (BLS) reported on Friday that the unemployment rate fell to 5.1% in August, down from 5.3% in July. This was lower than the pre-report consensus which called for the rate to remain unchanged. While the drop to 5.1% was a surprise, that level falls squarely within the Fed’s range for “full employment” which is 5.0%-5.2% (more on this below).

While the jobless rate fell more than expected, the US economy added only 173,000 jobs in August, well below the pre-report consensus for 220,000 new jobs. New jobs created in June and July were revised up by a combined 44,000 and most forecasters believe that August jobs will be revised higher over the next couple of months as well. We’ll see.

According to the BLS, the main reason why the unemployment rate tumbled to the lowest level since April 2008 is because another 261,000 Americans dropped out of the labor force in August. This pushed the total number of US working-age, available workers who are not in the labor force to a record 94 million, an increase of 1.8 million in the past year. That’s a whopping 14.9 million who dropped out since the start of the Great Recession in December 2007.

The Labor Force Participation Rate remained unchanged in August at 62.6% for the third consecutive month – a level not seen since the 1970s.

Average hourly earnings of private-sector workers rose by 8 cents to $25.09 last month. That’s a 2.2% increase from a year earlier. Wages had been advancing at a modest 2% pace during most of the expansion. Many economists point to the slow gains in wages as a reason that consumer spending and the broader economy aren’t growing more rapidly.

The average workweek also increased by 0.1 hour last month to 34.6 hours. The number of Americans working part-time because they can’t find full-time jobs (also called “involuntary part-time workers”) was little changed in August at 6.5 million. A study earlier this year by Rutgers University found that 63% of involuntary part-time workers are struggling financially.

A broader measure of unemployment – the U-6 rate – that includes people looking for work, stuck in part-time jobs or discouraged about finding a job dropped to 10.3% in August, down from 12% a year earlier. While headed in the right direction, that number is still very high.

In conclusion, the August unemployment report was a mixed bag. While the drop to 5.1% in the headline unemployment rate is welcome news, it also falls into the range which the Fed considers to be full employment – which could result in a Fed Funds rate hike. On the other hand, the much weaker new jobs at only 173,000 last month might give the Fed a reason to pause yet again.

US Economic Outlook For the Second Half of 2015

So far, we know that GDP increased by a wimpy 0.6% in the 1Q. Most forecasters believe that was due to yet another extremely cold winter in many parts of the US. Initially, the Commerce Department reported that 2Q GDP rose by 2.3%; however, on August 27 the government revised that estimate all the way up to 3.7%. So, overall growth for the first half of 2015 was 2.15%, if the 3.7% estimate for the 2Q holds.

So what was driving the big bounce in the 2Q? Pent-up demand from the 1Q was one part, but strong consumer spending played a big role in fueling the economic resurgence, helped by strong gains in disposable income and lower gasoline prices. Also helping was a ramp-up in construction activity, including home building. The housing market is having a good year, propelled by a stronger job market, low interest rates, slowly rising wages and an increase in household formations.

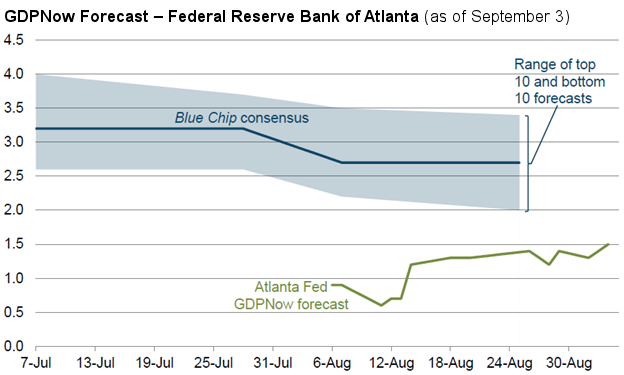

So how about the 3Q? We won’t get our first glimpse at 3Q growth until the end of October when the Commerce Department’s advance estimate of 3Q GDP will be released. However, most forecasters agree that 3Q GDP growth will not match the 2Q.

3Q growth should slow from the strong 2Q as inventories grow more slowly and state and local government spending slow from an unsustainable pace. As of last week, the Atlanta Fed’s GDPNow reading forecasts growth of just 1.5% in the 3Q. On the other hand, most forecasts I’ve seen for the 3Q are in the 2.5-3.0% range. We’ll see.

Most forecasters expect similar growth in GDP in the 4Q. The consensus currently is that GDP growth will average about 2.7%-3.0% for the second half of this year, resulting in an overall pickup of just 2.5% or less for the full year, only slightly ahead of 2014’s pace – still not impressive.

Inflation Still Running Well Below the Fed’s 2% Target

The thing central bankers fear the most is deflation. While the US economy is not experiencing deflation, our inflation rate is very low. According to the Bureau of Labor Statistics, the Consumer Price Index rose just 0.2% for the 12 months ended July. The Fed, however, prefers to gauge inflation by watching the Personal Consumption Expenditures Price Index (PCE), and specifically the Core PCE which excludes food and energy prices.

Personal consumption expenditures are the primary measure of consumer spending on goods and services in the US economy. It accounts for about two-thirds of domestic spending, and thus it is the primary engine that drives future economic growth.

The Fed believes that US core inflation needs to be at least 2% to keep the economy growing. Yet CPI and PCE are both well below the Fed’s target, and trending lower, as we can see below.

The PCE Price Index has fallen significantly since late 2011 and with the help of falling gasoline prices, it is now hovering just above 0%. Core PCE stands at just 1.24%. The Fed has admitted that inflation is below its target of 2%, but has also said that it could initiate lift-off if it were confident that Core PCE would increase to 2% in the near future.

Yet Core PCE has not been at 2% since early 2012 and is trending lower. If the FOMC does not raise the Fed Funds rate next week, this will likely be the key reason, along with the significant increase in equity market volatility and sharp moves lower in recent weeks.

Stronger Dollar Could Hamper Growth This Year & Next

Most Americans are not greatly affected by the typical fluctuations in the US dollar. Yet even moderate shifts in the value of the greenback can have positive or negative impacts on those who travel overseas extensively, and even more on those involved in the export or import trade.

The US dollar has gained in value against a basket of foreign currencies over the last year, especially in the six months from October 2014 to March 2015. Since then, the dollar has been in a broad trading range.

While the dollar fell rather sharply in the August stock market turmoil, most analysts expect the dollar to resume its uptrend later this year, especially if the Fed begins to raise US interest rates. If that proves to be true, the dollar could be a further drag on the US economy in terms of international trade.

Exports are discouraged and imports encouraged by a rising US dollar, and by the strength of the US economy relative to other nation’s economies. Stronger exports (not likely if the dollar continues to rise) are a boost to GDP, while rising imports are a negative for GDP.

Likewise, the slowdown in China will be a drag on US exports if it continues, and will hurt its suppliers such as South Korea, Japan and other trading partners. But at this point, it is impossible to know just how much China’s economy will slow down. With that said, let’s look at the latest economic reports from China.

New China Economic Data Point to Further Slowdown

Activity in China’s manufacturing sector shrank at its fastest rate in at least three years in August as domestic and export orders tumbled, hitting global markets hard and increasing fears that the world’s second-largest economy may be heading for a hard landing.

Even more worrying, China’s services sector, which has been one of the lone bright spots in the sputtering economy, also showed signs of cooling. News of deteriorating business conditions set off fresh selling in Chinese shares last week, which also hurt our equity markets.

Hurt by soft demand, overcapacity and falling investment, China’s economy has been further buffeted by plunging share prices and a surprise yuan devaluation – in what some have called a “perfect storm” of factors that is rattling global markets and could strain relations with China’s major trading partners.

China’s official manufacturing Purchasing Managers’ Index (PMI) fell to 49.7 in August from 50.0 in July, the National Bureau of Statistics said. That was in line with a Reuters poll, but was the lowest since August 2012 – and below the 50-point mark separating growth from contraction. Still, China’s economy is expected to grow around 6.5% in the second-half of the year, easing to 6.2% in 2016. While that is disappointing, most countries would kill for that level of growth.

Nevertheless, the Shanghai Composite Index, the most widely-followed Chinese stock index, has plummeted in recent months by about 40%, following a 150% rally from the middle of 2014 to the middle of this year. Here’s a look at what this Index has done over the last five years.

Most analysts said the latest bleak economic reports and continued plunge in stocks means that the Chinese government must lower interest rates even further and loosen monetary policy again soon to avert a sharper economic downturn that could weigh on global growth. The good news is that China’s services index remained in expansion territory at 53.4 last month.

Fed Funds Rate Futures Show Odds For September Rate Hike

The Chicago Mercantile Exchange (CME) has an actively traded Fed Funds rate futures market which predicts the likelihood of a Fed interest rate change. Traders can buy and sell futures based on the Fed Funds rate and expectations for changes in that rate.

If you think the Fed will raise rates in the near future, you would sell these futures, and if you think the Fed will lower rates, you would buy these contracts. Fed Funds rate futures are one way for institutional traders to hedge interest rate risk and speculate on changes in the future.

In August, the Fed Funds futures put the odds of a rate hike on September 17 at 73.4% on average. As of last Friday’s close, the odds of a rate hike next week had climbed to 81.1%. Apparently most traders of Fed Funds futures believe the Fed will hike rates next week even though inflation is well below its 2% target.

Finally, there is growing talk ahead of next week’s Fed policy meeting about a rate hike of less than 0.25%. Larry Kudlow of CNBC called on the policy committee to raise the Fed Funds rate by 1/8% (0.125%) at the September 17 meeting.

Others including Mike Shedlock of Townhall Finance and (long-time friend and former business partner) John Mauldin have called on the Fed to raise rates by 1/8% at each policy meeting going forward. They argue that by announcing such a “baby step” policy the Fed would be giving some much needed certainty to the markets. I wonder if Chair Yellen is listening.

At the end of the day, I believe the Fed’s decision on lift-off next week will depend on what is happening in the US and global equity markets.

If the Dow and S&P hold above their late-August lows between now and September 16 (when the next policy meeting begins), I believe the Fed will vote for a rate hike of 25 bps or less.

On the other hand, if the Dow and S&P are at new lows by September 16, I believe the Fed will vote to delay lift-off until some later date when the equity markets are more stable.

Wishing you profits in these crazy markets,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.