At the National People’s Congress in Beijing in March 2015, China’s Premier Li Keqiang announced a growth target of 7 percent, acknowledging that “deep-seated problems in the country’s economy are becoming more obvious.”

Three months later and thousands of miles away in Washington, the World Bank lowered its growth forecasts across the board and asked the US Federal Reserve Bank to delay any contemplated rate hikes. The World Bank’s chief economist said that it had “just switched on the seat belt sign. We are advising nations, especially emerging economies, to fasten their seat belts.”

So it’s going to be a bumpy ride? How bumpy? And for how long? (Source: McKinsey Global Institute. They address these questions. You’ll find the link below.)

And the Fed? Jeffrey Lacker, president and CEO of the Richmond Fed said this morning, the “real side” of the economy is calling for a higher interest rate. Adding that, “It’s time to align our monetary policy with economic progress.” The market is under pressure again today.

Will they, won’t they? They have created a bipolar market. What is clear, at least to me, is that the global economy is in a deflationary stranglehold. Debt and demographics are the immediate enemy.

“To be clear, while we might see a tiny tightening akin to what was experienced in 1936, we doubt that we will see anything much larger before we see a major easing via QE,” Ray Dalio

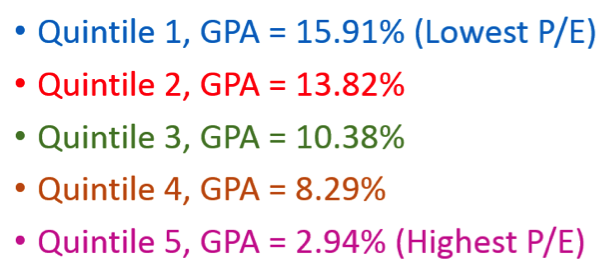

Sorting valuations into 5 categories ranging from 1 (least expensive) to 5 (most expensive) and looking at the 10-year returns you would have received if you bought “when the hamburgers” were cheap (see Buffett Burgers and The Hallelujah), category 1, or if you bought when the burgers were expensive, category 5, you can get a good sense of what your stocks are going to do for you over the coming ten years. Here are the stats (source – NDR):

Give me 1, 2, 3 or even 4. We are in quintile 5. The data says we should expect the equity market to return close to 3% over the coming ten years. That’s before inflation. It is hard to get excited about equities. It is also hard to get excited by bond yields at 2.15%. I wish I could but I can’t. Think differently we must.

Therefore, underweight equities (and hedge), underweight fixed income (tactically managed) and overweight alternative strategies (defined as anything other than traditional buy-and-hold). That category is not dependent on a one directional up market to make money. Broaden your set of combined risks. In this regard, send me an email if you’d like a free copy of our white paper on Correlation and Diversification.

Back to McKinsey – McKinsey believes there will be three sets of forces shaping the global economy over the coming decade. 1) Stimulus policies and shifting energy markets. These are near-term forces whose effects are felt on a daily basis. 2) Urbanization and aging are powerful, inexorable trends aggravating ongoing structural challenges and 3) Technological innovation and global connectivity.

The report is well done. I summarize some of their findings below and provide you with a link to the full piece.

Volatility and uncertainty are nothing new in financial markets. In my latest Forbes piece, “Welcome To The Opening Round Of The New Bear Market”, I share a few ideas around hedging. QE4 may right the ship but that is the bet. No guarantees in this game.

Finally, we conclude this week’s letter with a look at the technical evidence. The charts are updated in Trade Signals and suggest a new cyclical bear has begun.

Included in this week’s On My Radar:

- Shifting Tides – Global Economic Scenarios for 2015-25, McKinsey Study

- Welcome To The Opening Round Of The New Bear Market, Forbes

- Trade Signals – Extreme Pessimism Supports ST Rally. Trend is Bearish. Sell/Hedge on Rallies.

Shifting Tides – Global Economic Scenarios for 2015-25, McKinsey Global Institute

McKinsey is perhaps the world’s most respected global corporate consulting firm. Though I note that I am a biased fan.

The McKinsey model incorporates more than a dozen major international databases from such institutions as the United Nations, the World Bank, the International Monetary Fund, and the Bank for International Settlements. Selection of data sources is based on their authoritativeness, comparability, extended time series, and country and concept coverage. The result is a historical database that provides complete time series data for more than 150 concepts and 110 countries over 30 years.

Following I share a number of bullet points that attempt to get to the heart of the piece (13 pages). I provide a link to the full piece below.

- Of immediate concern is the persistent problem of weak aggregate demand relative to overall economic capacity. The International Monetary Fund estimates that production in the ten largest advanced economies was 2 percent below potential in 2014. This gap was smaller than it had been in 2009 (3.3 percent) but significantly worse than the surplus of 0.8 percent that prevailed in the early 2000s.

- All major economies except China experienced significantly weaker demand in the aftermath of the global financial crisis. Many governments and central banks responded with fiscal and monetary stimulus programs that fostered the low real interest rate environments which have endured for over five years.

- The McKinsey Global Institute reviewed the recent performance of advanced economies and found that they had all increased rather than reduced their overall debt levels—in some cases, by more than 50 percent. (SB: emphasis mine)

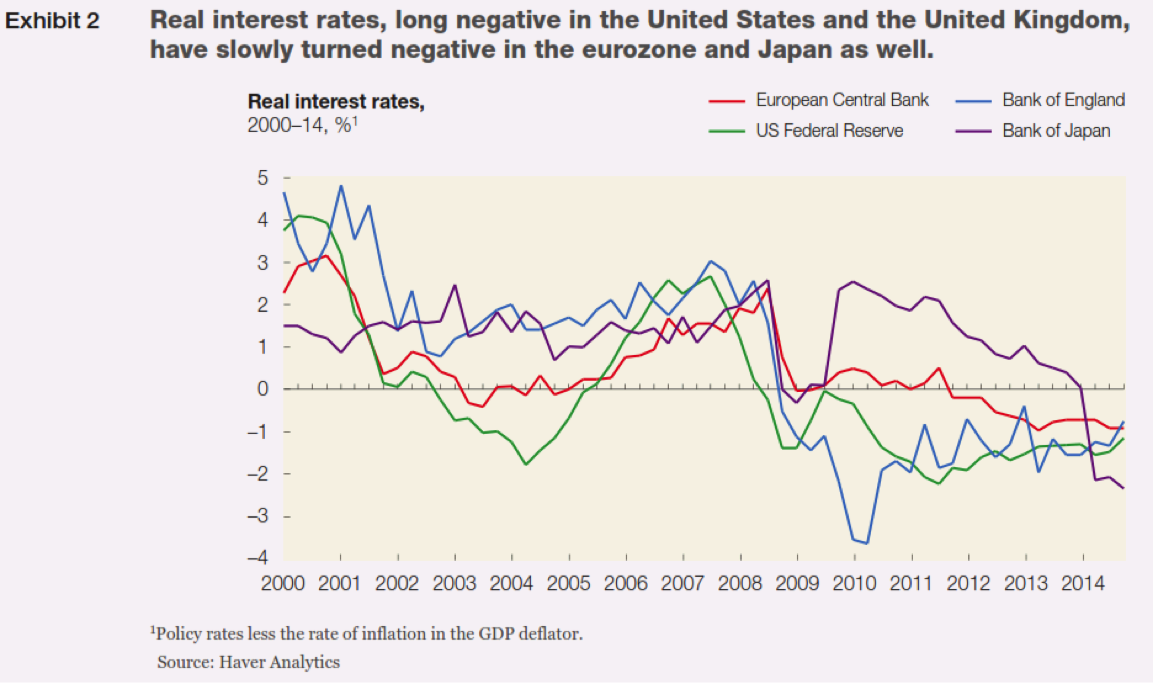

- Complicating the picture is the question of whether real interest rates will remain low (Exhibit 2). (SB: The real interest rate is the current rate less inflation. Europe, England, Japan and the US are all negative. Put Germany in that camp as well.)

- Persistently low interest rates encourage investors to search for yield and safety, creating the preconditions for asset bubbles and further volatility in international financial flows.

- Economists are concerned that unconventional monetary policies have distorted rather than bolstered the demand picture. (SB: see Fed comments here)

- In the United States, for example, the Federal Reserve signaled for months that it would raise rates by the end of 2015, heralding a return to a more conventional, interest rate–driven monetary policy. In the interim, however, results were tepid and now a rate hike may be further delayed.

- Europe and Japan are in the same situation. McKinsey adds, “Demand in major markets remains weak enough, furthermore, that a misstep in any one of them will be felt by the others.”

- Oil prices fell by 50 percent in the latter half of 2014. Even after a slight rebound, they remained well below average levels of the past five years. For energy consumers, the lower energy prices have provided a welcome respite; for producers, they challenge fiscal stability.

- The breakeven oil price—the price at which a fiscal surplus turns into a deficit—is estimated at $57 for Kuwait and $119 for Algeria. Countries have so far managed the crunch by drawing down reserves and through exchange-rate movements, but these are short-term actions and direct fiscal adjustment lies on the horizon. (SB: emphasis mine)

- Persistent demand weakness and falling oil prices are the stuff of daily headlines, but associated effects could drive alternative economic outcomes for the next decade. The complication is that deeper forces are at work.

- The effects of urbanization and aging are predictable and are tilting the global economy in one general direction: toward emerging markets.

- Increasing urban congestion and an aging labor force impose burdens—among them, lower productivity, falling demand, and rising health and pension loads—on all economies. The challenges are clear.

- McKinsey research indicates that 46 of the world’s 200 largest cities will be in China by 2025, a sign too of the eastward migration of the global economy’s center of gravity.

- On China’s demographic pressures. The labor force, on which economic activity depends, is both aging and shrinking. It is expected to contract by 11 percent in China by 2050, even as the country’s economy expands.

- The shrinkage in continental Europe is expected to be even more dramatic.

- As life spans are growing and birthrates falling, furthermore, an aging working population in advanced and emerging economies will be supporting ever-higher numbers of retirees.

- Among the major economies, only the United States has a demographic profile favorable to long-term economic growth.

- For the rest of the leading economies, expected productivity improvements will not bridge the gap.

- Without a fundamental economic and cultural shift, favoring continued participation of older workers and the introduction of more women workers and immigrant labor, many economies would face serious growth constraints within ten years.

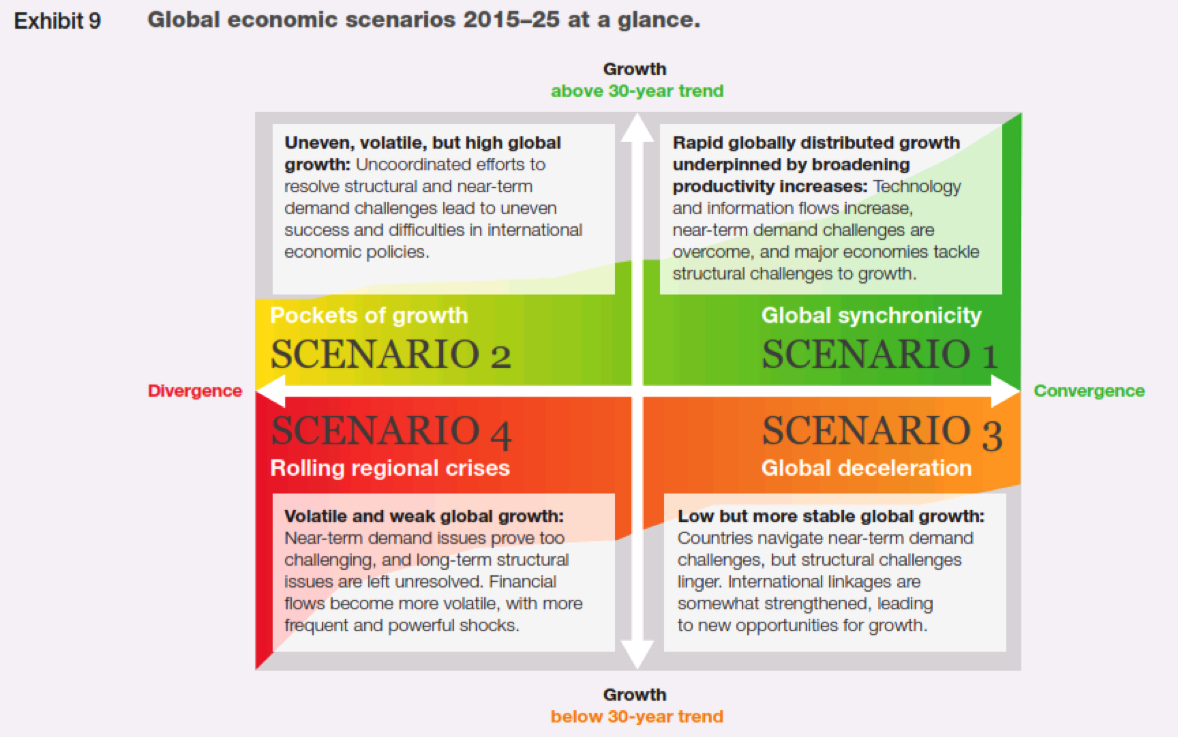

The report takes a well thought out look at the interconnected nature of the global economy. There is so much more in the paper and I don’t want to do a disservice to their research so I’ll jump to the conclusion on potential global economic scenarios 2015-2025 (Exhibit 9) and encourage you to click on the link to the full piece below.

“Global synchronicity” (scenario 1) describes a world where most major economies tackle their structural challenges, and are able exit from aggregate demand stimulus smoothly. “Rolling regional crises” (scenario 4) describes the opposite outcome.

My personal view is we must somehow move through the debt and coming pension mess. Promise more, tax more, spiral lower. Some form of restructure is in our not too distant future. We have choices yet what we chose will set the path. I’m praying for Scenario 1 yet we seem to be in Scenario 3. Let’s hope the worst case is Scenario 3. Scenario 4 is deflation that moves to depression.

The end game is inconclusive for our path is yet to be determined. Overall, the McKinsey report does a great job in laying out the possible outcomes between 2015 and 2025.

Here is the link to the full piece:

Welcome To The Opening Round Of The New Bear Market, Forbes

I believe we are in a modest correction period – a new cyclical bear cycle has begun. If we do not experience a U.S. recession, the downside should be limited to less than 20%.

Another QE, from my view, is in the cards. That may stem the fall. I hold less hope in structural reform. Unfortunately, we’ll need another crisis to goose our leaders in that direction.

As you’ll see in the charts posted in Trade Signals, I believe we are now in a cyclical bear market. How long and how much, in my view, depends on the response of global central bankers or our collective loss in the confidence we have placed in them.

Read the piece and let me know what you think. On page 4 you’ll find several ideas that may help you hedge your equity exposure and I mention a fund that has almost zero correlation with both the stock and bond markets. That can help with diversification.

Click here for the Forbes article.

Trade Signals – Extreme Pessimism Supports ST Rally. Trend is Bearish. Sell/Hedge on Rallies.

Since last week’s post, the S&P 500 Index has rallied 77 points off of last week’s Investor Sentiment Extreme Pessimism low. A gain of 4.11%. Following are several charts that look at the 2011 correction and today. Let’s see if we can get a sense for reasonable bounce targets (levels to either raise cash or re-establish hedges).

Sentiment remains Extremely Pessimistic which is short-term bullish for stocks. The overall trend is bearish for equities. I also note that the Zweig Bond Model is back to a sell signal which is bearish for bonds.

Along with the usual weekly charts, I share several technical charts that reflect near-term upside and downside price targets for the S&P 500 Index.

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: Sell Signal

- CMG NDR Large Cap Momentum Index: Sell Signal

- 13/34-Week EMA on the S&P 500 Index: Sell Signal

- NDR Big Mo: Neutral – Nearing a Sell Signal

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- Weekly Investor Sentiment Indicator:

NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for stocks) Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for stocks)

- Don’t Fight the Tape or the Fed: Neutral signal

- S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

- The Zweig Bond Model: The Cyclical Trend for Bonds is Bearish

Click here for the link to all of the charts.

Concluding thoughts

All ‘bout that Fed. If the Fed raises rates in September. Look out. I remain of the view that they will not raise rates in 2015.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group