Financial market participants were beset with a number of worries in August. However, as a general theme, investors often worry about things they shouldn’t worry about and don’t worry about the things that they should worry about.

The drop in China’s stock market is essentially an unwinding of a speculative bubble. As such, it’s not necessarily a sign of weaker economic growth in China, nor will the market’s decline lead to economic weakness. However, there are plenty of signs that the Chinese economy has slowed. That’s the real worry. History has shown that preventing a bubble is problematic. Efforts to stop the bubble from collapsing are almost always futile, but policymakers should be prepared to deal with the unpleasant aftermath when it bursts.

China’s “devaluation” has been described as an effort to spur exports, a first salvo in “a currency war.” However, according to the People’s Bank of China, the move was meant as a transition to a more market-based exchange regime. China’s leadership wants the country to play a larger role in global finance and the yuan to be among the major currencies in the world. The IMF indicated that it would consider adding the yuan to its benchmark basket (along with the dollar, the euro, the pound, and the yen). However, to do that, the exchange rate would have to be determined by market forces instead of set at the whim of Chinese officials. After two sharp drops in the yuan against the dollar, the PBOC had had enough and declared that the currency adjustment was “essentially complete.” The currency has depreciated by about 2.8% – not a huge move. A number of U.S. presidential candidates have railed against China’s manipulation of its currency. However, the PBOC is acting to keep the yuan from weakening, not strengthening.

Again, the real worry about China is slower growth. The official economic figures (7% GDP growth) are suspect. While the country has grown rapidly is recent decades, it faces a tough transition to a better-balanced, demand-driven economy. In coming years, we’re likely to see 4-6% growth, but it could be even lower if problems increase. The country needs more consumer spending. The collapse of housing and stock market bubbles, and a contraction in the country’s shadow banking system make that a challenging goal in the near term. The ham-handed efforts to prop up the stock market and the PBOC’s clumsy attempt to move to a new exchange rate regime haven’t done much to instill confidence in the country’s leadership.

The direct impact of China’s slowdown on the U.S. economy should be small. However, one concern is that China’s woes will lead to contagion to other nations. China accounts for a large percentage of exports from a number of “commodity countries.”

The other major market worry is the Fed. Officials have made it clear that conditions are expected to warrant the first step in policy normalization – that is, an initial increase in short-term interest rates – by the end of this year. The stock market’s fear of the Fed is not well-founded. It shouldn’t really matter whether the Fed begins to raise rates in September, late October, or mid-December. The important thing is the pace of tightening beyond that first move. Officials have repeatedly indicated that conditions are expected to warrant a gradual pace of tightening.

Much of this appears to mirror the “taper tantrum” of 2013. Amid QE3, Fed officials began to talk about reducing the monthly pace of asset purchases. Markets freaked out. Bond yields rose. The Fed delayed its decision to start tapering, but when the Fed did begin to taper, long-term interest rates drifted lower, not higher. We may be seeing on over-reaction now in equities.

If not for August’s financial market turmoil, the Federal Open Market Committee would very likely have begun rising short-term interest rates at the September 16-17 policy meeting. While apparently still on the table, a September move is a lot less likely now. The economy has made enough progress and is strong enough that it can easily withstand a small increase in rates.

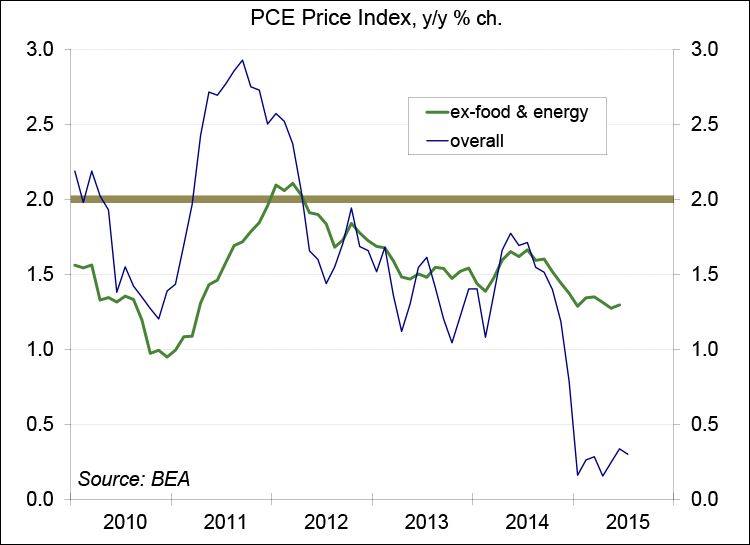

Inflation has remained low. The core PCE Price Index, the Fed’s chief inflation gauge, rose 1.2% in the 12 months ending in July, a long way from the Fed’s official goal of 2%. Inflation has been pushed lower in recent months by the drop in oil prices and the stronger dollar. Oil prices aren’t going to fall forever and the dollar should stabilize – and inflation should move somewhat higher – but the near-term inflation outlook should allow the Fed to take its time before beginning to raise rates.

Still, the stock market need not worry about the Fed raising rates. A hike would signal that the recovery has progressed sufficiently and the Fed is confident that growth will continue.