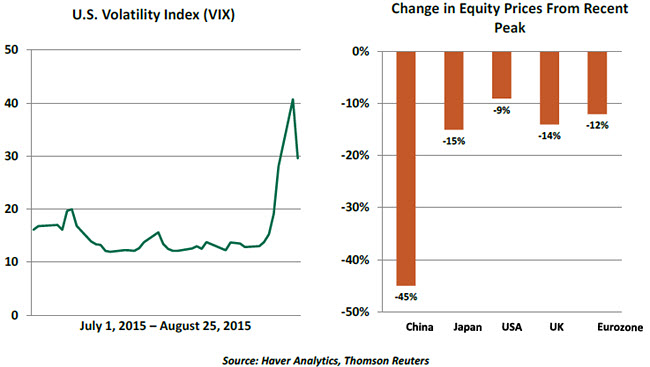

It has been an unsettling month for the financial markets. The challenges faced by China, which have been amplified by inconsistent responses from policy makers, have heightened uncertainty. At times like this, it is very important to retain contact with long-term fundamentals. For the moment, this more measured perspective remains reasonably constructive.

Chinese equities had rallied to an unsustainable peak by the start of the summer, fueled by readily available margin lending and government promotion of stock ownership. In June, rumors that the government wanted to rein in the equity rally initiated a sell-off that continues to this day.

For a time, Chinese authorities were able to engineer artificial stability by ordering equity purchases and suspending trading in certain shares. But it is very difficult for any government, no matter how well financed, to stand in front of bearish sentiment. It appears that officials have stepped aside for the moment, and Chinese equities have resumed a free fall.

The situation with equities illustrates a core concern. Chinese policy makers seem to have gone back and forth on how they want to address their financial markets. (We’ve also seen this inconsistent behavior in their management of the Chinese currency.) All of this has left investors wondering what China’s true goals are. This uncertainty has led to a sharp increase in market volatility and equity price declines across the globe.

We do not think that China is in imminent danger of an outright economic crash. There are portions of the Chinese economy that continue to perform well, and China has substantial reserves that can be used for economic stimulus. An adjustment to a lower level of growth has been expected, even by the Central Committee.

China’s recent travails will have only a limited direct impact on the United States. As we discussed in our August 7 commentary, U.S. exports to China are modest and direct financial linkages are limited. The declines in energy and commodity prices that have resulted from concerns over China’s growth path should be a net positive for American consumers. And the flight to the quality of U.S. Treasury securities has lowered long-term interest rates here.

It is the indirect effects that will bear watching. Those emerging economies that sell to China, or which are reliant on commodities, are under additional pressure. The profits of large multinational companies may be hindered, and investor psychology may be challenged.

Another potential indirect effect involves the September Federal Reserve meeting. Absent international unrest, we would have a high degree of confidence in our call for a rate hike at that time. But if market conditions remain unsettled, the Fed will be reluctant to add to them by tightening when world markets seem fragile.

Corrections are often a healthy element of market cycles. We’d gone a very long time without a 10% equity market decline, which happens twice per year on average. And market volatility had remained very low, in spite of myriad international challenges, including the Greek crisis. Shocks to the system can enhance focus, and ultimately pave the way to continued advance.

There is certainly a possibility that the situation will become more severe and the consequences more dire. We’ll discuss this further in Friday’s weekly. Until then, let’s all try to take a deep breath.