|

IN THIS ISSUE: 1. Global Chaos Erupts, Worries About China, Fed, Etc. 2. China’s Economy Shows More Signs of Weakening 3. Note to Donald Trump: Get Your China Facts Straight Overview There is so much to write about today it’s hard to know where to start. Equity markets around the world are plunging on worries about China, a possible Fed interest rate hike next month, the worsening bear market in commodities, economic and currency weakness in emerging markets, etc., etc. I will touch on each of these concerns today. Plus, I have a message for Donald Trump who needs to get his facts straight on China, among other things. Following that discussion, we’ll look at crude oil prices and other commodities which have fallen to new lows over the last week. And, of course, we will discuss the Fed’s next move in light of the latest carnage in the markets. It should make for an interesting discussion, so let’s get started. Global Chaos Erupts, Worries About China, Fed, Etc. The US and global equity markets can only ignore so much bad news for so long. Inevitably, there is always a tipping point. I warned about this in April and May and advised readers to reduce long-only equity exposure significantly. I was a little bit early, given that the Dow and the S&P 500 managed to hit new record highs in the second half of May. But it’s been all downhill since then, and the wheels really fell off last week. Stocks took their worst pounding in four years last week with the Dow Jones plunging by 530 points on Friday, reaching a 10% correction for the first time since October 2011. The S&P 500 Index also fell sharply last week, blasting through key support levels to 1970, for a one week decline of 5.8%. As of the end of last week, the S&P 500 was 7.7% off its recent record high above 2130 in May. The selling actually intensified yesterday when the Dow Jones opened over 1,000 points lower and the S&P 500 plunged to near 1,900 on the open – in response to another huge selloff in Chinese stocks. This selling is not likely to subside until there are some clear signals from both China and the Fed. While the US stock markets rallied strongly today, those gains were reversed late in the session to close lower on the day. The Dow Jones Industrial Average has now plunged from around 18,200 in May to well below 16,000 by the close today – a decline of over 14%. The S&P 500 Index has a similar picture – a new all-time high in May above 2,130 only to plunge to below 1,900 at today’s close. And more carnage may yet lie ahead.

As I warned earlier this year, global markets have finally decided to worry about weakness in China and whether it will continue to spread into other emerging markets, hurting their currencies even more. Emerging market currencies have fallen sharply lower in recent weeks, hurt by falling commodity prices and fears of further currency devaluation by China just ahead. Those markets have also been hit hard by the prospect of a rising dollar, which makes their dollar-denominated debt larger. However, the US dollar has moved lower since the beginning of August which should begin to bolster emerging market currencies if this new trend continues. On the other hand, if US interest rates rise next month, assuming the Fed goes ahead with “liftoff” in September, that could strengthen the US dollar again and be a further setback for emerging market currencies and commodities (more on this below). We’ll have to see. China’s Economy Shows More Signs of Weakening It’s no secret that China’s blistering economy has slowed significantly this year, with its official estimate of GDP growth now down to 7% for 2015. Until last week, most forecasters believed that China’s real growth rate was probably closer to 3-4%, but of late, new reports suggest it may be even lower. China’s manufacturing index has plunged since last summer, and last week’s report was even worse than expected.

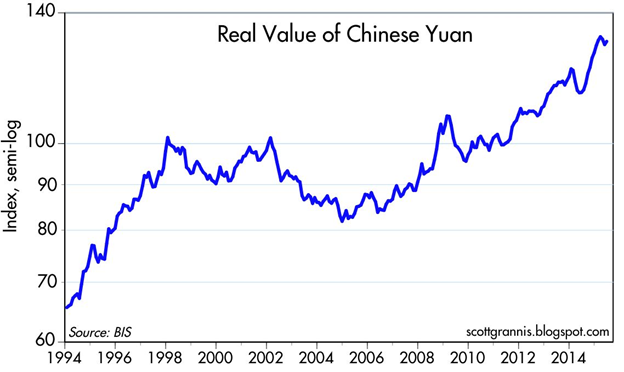

It’s not that China is expected to fall into a recession this year, but evidence from both shipping (exports) and factories suggest that the economy is contracting rather rapidly. Fortunately, other reports suggest that the current contraction will stabilize soon and begin a modest rebound, thus avoiding the so-called “hard-landing.” That remains to be seen. The other China issue that is rattling global equity markets is the recent two-day devaluation of the yuan (also called the renminbi). The 4% devaluation over August 11-12 was the largest single move since 1994. However, as I explained in my Blog on August 13, the yuan has risen sharply since 2005 (see chart below), so the latest devaluation is probably not significant overall. Chinese authorities don’t want the yuan to devalue much further because the country is already experiencing enormous capital outflows. It was widely reported last month that some $800 billion has fled China this year. The Telegraph (of London) reported over the weekend that another $100 billion has fled the yuan so far in August. It goes without saying that China is facing major problems: its decelerating economy; the recent plunge in its stock markets; and the surprise devaluation of its currency. It remains to be seen how these problems will be resolved. In the meantime, expect more pressure in the global equity markets. Note to Donald Trump: Get Your China Facts Straight On August 11 at a campaign event in Michigan, Mr. Trump said the following about China: I think you have to do something to rein-in China. They devalued their currency today. They’re making it absolutely impossible for the United States to compete, and nobody does anything… Well, you have to take strong action. How can we compete? They continuously cut their currency. They devalue their currency. And I have been saying this for years. They have been doing this for years. This isn’t just starting. This was the largest devaluation they have had in two decades. Mr. Trump, I doubt that you read my work, but for the record, I would like to set you straight on the subject of China devaluing its currency. You need to know this and get your facts straight. Just take a look at this chart on China’s currency.

China has consistently appreciated its currency for the last 20 years – by more than 100% over the last three decades. Your assertion that “They devalue their currency…They have been doing this for years.” is simply wrong, as the Bank for International Settlements confirms above. Mr. Trump, I like that you are in the race for the GOP nominee. In general, I like how you are shaking up the political landscape. I doubt I could vote for you in the GOP primary, but it would help me a lot if you got your China facts (and others) right. Oil Plunges to New Lows – Adds to Global Uncertainty Oil was lower for an eighth consecutive week in its longest weekly losing streak since 1986. West Texas Intermediate (WTI) futures first fell below $40 per barrel last Friday but closed at $40.45 per barrel. WTI was down 4.8% for the week. The slide continued yesterday with WTI falling to near $38 at one point. That’s down from just above $60 in July. This is the first time WTI crude futures traded below $40 since 2009. Oil forecasters, who predicted early in the year that prices would recover in the second half of 2015, now say a rebound is unlikely before the second half of next year or even 2017. US government forecasters last week cut their oil price estimates and see oil holding below $60 a barrel, on average, through 2016. Of course, no one really knows the future. Investors expected last year’s 46% plunge in oil prices to prompt a wave of bankruptcies and acquisitions across the US energy sector this year. Yet many companies avoided such measures by raising money from investors, cutting costs and focusing on their most-productive wells. The shift in sentiment is partly due to the resilience of US oil producers, who are continuing to pump crude at near-record levels despite months of spending cuts, thanks to new efficiencies in drilling technology. An unexpected price rally in the 2Q of this year allowed some companies to lock in (hedge) profitable prices for the next year and add new drilling rigs.

The dip below $40 on Friday occurred after oil-field-services company Baker Hughes Inc. reported that the number of rigs drilling for oil in the US rose for the fifth straight week. The renewed drop in oil prices has sent energy stocks skidding, weighing on global market indexes, and adding to the uncertainty. Some worry that falling energy prices indicate that global growth is slowing, and cheaper import costs have sparked concerns about low inflation, or even deflation, in some regions around the world. Crude prices below $40 a barrel could further destabilize oil-producing nations, which are suffering from low revenues and currency volatility. The International Energy Agency forecast last week that world oil production would outpace consumption by 1.4 million barrels a day in the second half of the year and by 850,000 barrels a day in 2016. This forecast does not take into account the possibility that the nuclear deal with Iran will allow the country to increase its oil exports, further flooding the global market. As a result, we’re now hearing predictions that WTI crude could fall to $20 a barrel in the next year. The sharp decrease in oil prices this month should lead to significantly lower gasoline prices in the weeks ahead. Persistently low oil prices could result in another wave of savings to US drivers, who saw the national average retail gasoline price fall to nearly $2 a gallon in January. Savings at the pump have been widely expected to translate into higher consumer spending, but consumers thus far have opted to put the extra money in savings or to pay down debt, partly because they didn’t think the lower prices would last. Retail gas prices averaged $2.63 a gallon on Friday, the lowest price for this date since 2009, according to AAA. Meanwhile, Commodity Prices Continue to Slump The Thompson Reuters CRB Index continues to plunge and is threatening to fall below the double-bottom lows seen in mid-2013. The CRB Index (Commodity Research Bureau) is made up of 19 core commodities including grains/foods, cattle/hogs, heating oil/crude oil/gasoline and base metals/precious metals. Commodities prices have been trending sharply lower since mid-2011 as you can see in the chart below. The Index enjoyed a modest rebound in early 2014 but has declined sharply since the middle of last year.

The plunge in commodities prices is in-part due to supply and demand but is also a reflection of macro forces. In this case, falling prices are partly a result of the slowing global economy, especially China, and partly due to the stronger US dollar earlier this year. A broad-based decline in commodities prices is deflationary. It is devastating for those emerging market economies that depend on commodities exports, not to mention that it weakens their currencies. Plunging commodities prices can also be a harbinger of a global recession. We’ll see. Fed Rate Hike September 17, Or Will Yellen Blink Again? As I have written in these pages often this year, the most likely time for the Fed to raise its key short-term interest rate has been at its September 16-17 policy meeting. Of course, few anticipated the stock market rout we’ve seen over the last few days. So the question is whether the Fed is so intent on raising rates that it will go ahead with “liftoff” on September 17, or wait until the next meeting in December or even later, in light of the recent market meltdown. Despite what Fed Chair Janet Yellen may personally prefer, she has only one vote on the powerful Fed Open Market Committee (FOMC). As best I can read the FOMC meeting minutes, about half of the Committee wants a rate hike this year, and about half are content to delay it until early next year. Based on what we think we know about Ms. Yellen, I would speculate that she would be happy to wait until early next year, based on the market turmoil we have seen in recent days. That remains to be seen, of course. I will keep you posted as always. Interesting Articles of the Last Week The first is an article that appeared in Fortune Magazine online last Thursday. The piece is actually a parody on the US economy, suggesting that while Americans are worried, better days may lie ahead.http://fortune.com/2015/08/20/american-economy-worries/ The second article is an editorial from Investor’s Business Daily which laments the fact that economic freedom in the US is on the decline. The “Human Freedom Index” now has the US ranked at #17 in the world and falling. They argue that the decline in freedom in recent years explains why the economic recovery has been so weak. Very interesting. Hoping you’re surviving these crazy markets, Gary D. Halbert |

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |