China’s economic slowdown may not be much of a direct drag on U.S. growth. While U.S. exporters will have a tougher time, the drop in commodity prices should help consumers and domestic producers. However, the country’s difficulties need to be considered in the broader view of emerging market troubles.

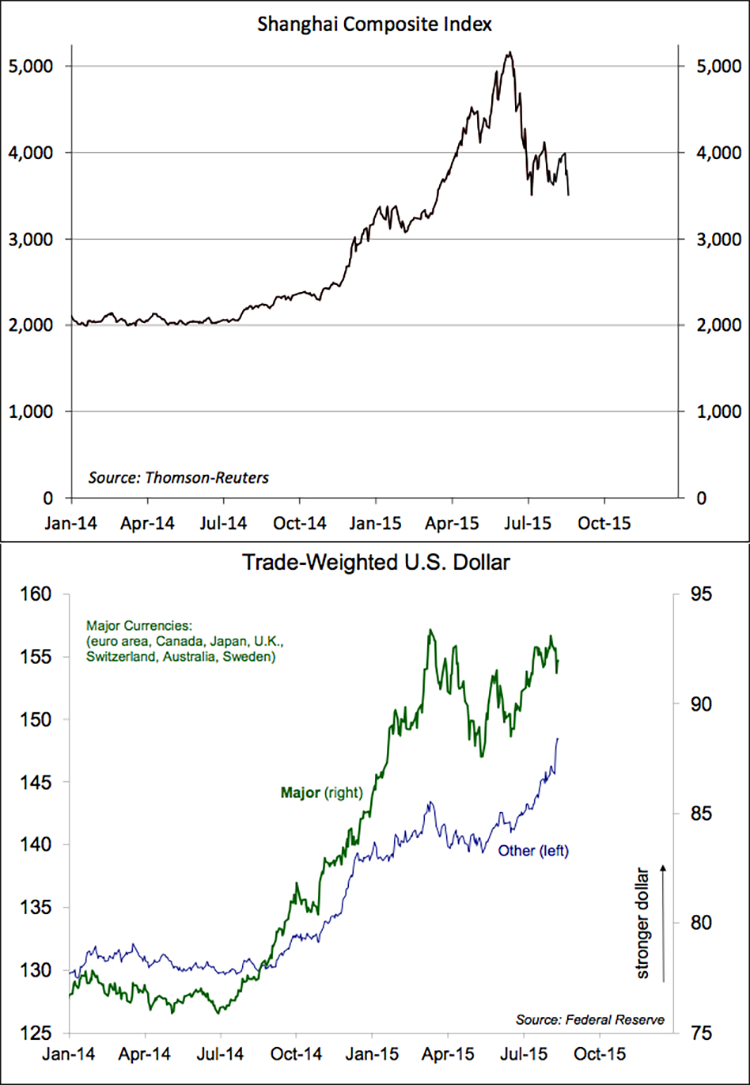

China’s stock market appeared to be undervalued in early 2014. The housing market collapse encouraged investors to put money back to work in the stock market. The Shanghai Composite Index rose more than 150% y/y, before beginning a 32% correction on July 8. Most companies in the index are partly state-owned, and the government has made a number of efforts to prevent the market from falling. The drop in Chinese equities does not seem to be related to the slowdown in economic growth (which was apparent when share prices were rising), nor is the market correction likely, by itself, to dampen economic growth. However, China’s economy has slowed, adding to worries about emerging economies in general.

U.S investors typically concentrate on the dollar index, which is based on a basket of six currencies (euro, Canadian dollar, yen, pound, Swiss franc, and Swedish krona). The Federal Reserve constructs another trade-weighted dollar index, which covers the other currencies. While the dollar has been essentially range-bound against the major currencies since mid-March, it has rallied more than 6% against the other currencies in the last three months (up more than 14% y/y). These countries account for about 51% of U.S. exports and about 57% of U.S. imports. Hence, while corporate earnings from the major-currency countries may be stabilizing, we should see a hit to those exporting to the “other” countries (bear in mind that earnings from abroad depend on growth as well as currencies).

The U.S. domestic economy stands to benefit from the drop in commodity prices. Gasoline prices should fall (refinery damage and maintenance may limit that in the near term). Lower costs of raw materials are likely to help shore up manufacturer profits.

China’s ham-handed attempt to prevent its stock market from unraveling and its clumsy, ill-fated attempt to move to a more market-based exchange rate regime have not done much to instill confidence in the country’s leadership. Capital outflows often lead to a worsening of conditions, creating more incentive for capital to flee (a vicious cycle). The direct impact on the U.S. economy may be relatively limited. However, China’s difficulties only add to worries about a broader slowdown in global growth. The longer-term outlook for these countries remains promising, but they’ve all stumbled badly recently. Moreover, China’s slowdown is likely to have a greater impact on other countries (for example, those exporting raw materials) than on the U.S.

These developments complicate the Fed policy outlook. The Fed does need to begin moving toward a less accommodative policy position at some point, but global worries and downward pressure on commodity prices should delay the initial move.