For some time, analysts have suspected that China’s economic performance was trending well below targeted levels. The equity market correction that began earlier this summer seemed to confirm these concerns; only a substantial amount of official intervention prevented an outright crash. Now we can add exchange-rate uncertainty to the list of things that China will have to manage very carefully.

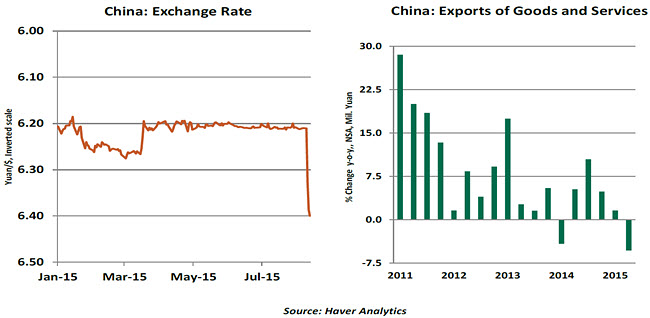

The People’s Bank of China (PBOC) took global markets for a wild ride this week when it allowed the currency renminbi (RMB) to move more freely than it had before. The details are technical, but the PBOC is essentially moving toward implementing a managed float where the RMB can move 2% in either direction on a trading day. The target for the new day will now be set at the previous day’s close instead of being re-set to some long-run objective.

This, in itself, is not a controversial practice. Regular currency intervention is the norm in the region, with only Australia and Japan meeting the International Monetary Fund’s (IMF) definition of a free-floating currency. In fact, it is rare for a country at China’s level of institutional development to utilize a free float. Thus, it should not come as a surprise that Beijing has elected to take baby steps toward liberalization.

But what raised eyebrows was the immediate RMB devaluation that occurred after the new procedures were announced. The RMB lost 2.8% of its value against the U.S. dollar in the first two days after the change before stabilizing during the balance of the week.

Questions abound about the reasoning behind the move. The party line highlighted a desire to move to a more market-based setting for the currency, which would be responsive to IMF concerns about adding the currency to its Special Drawing Rights (SDR) basket. But cynics suggested that Beijing simply wanted to boost Chinese exports, which have flagged in the face of weak global demand and strong regional competition.

Regardless of the real reasoning for China’s recent currency market movements, it is becoming increasingly clear that the government struggles with market signaling. The PBOC initially announced that it was implementing a one-time adjustment to more closely align the RMB with supply-and-demand dynamics. But after allowing the currency to be more market-driven for two days, authorities proceeded to intervene heavily in the market. The PBOC’s failure to adequately explain its strategy confused observers. Markets were only partially assuaged when the PBOC called an out-of-character press conference late in the week to clarify its stance.  As with all Chinese moves toward market liberalization, there are questions about policymakers’ resolve to carry out their own reforms. There is evidence that the PBOC intervened to stop the RMB from falling by the relatively modest limit of 2% multiple times this week. What happens if market forces want to push the RMB in either direction by the maximum of 10% per week? The uncertainty about how much (or little) market forces will be allowed to work will challenge those whose fortunes depend on the Chinese exchange rate.

As with all Chinese moves toward market liberalization, there are questions about policymakers’ resolve to carry out their own reforms. There is evidence that the PBOC intervened to stop the RMB from falling by the relatively modest limit of 2% multiple times this week. What happens if market forces want to push the RMB in either direction by the maximum of 10% per week? The uncertainty about how much (or little) market forces will be allowed to work will challenge those whose fortunes depend on the Chinese exchange rate.

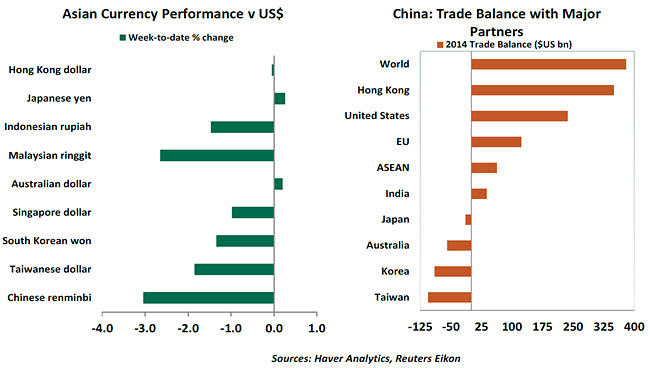

This week’s announcement had a dramatic impact on exchange rates across the Asia-Pacific area. Currencies in the region depreciated across the board, including regional stalwarts Australia and Singapore.

The news out of Beijing added to the malaise of the Malaysia ringgit and Indonesian rupiah, both of which are at levels not seen since the Asian Financial Crisis. Countries in this position are hurt two ways: a weak currency diminishes their ability to repay debt denominated in dollars and has the potential to scare away international capital.

A weak RMB will pressure trading partners at a time when lower demand from China has already clouded near-term growth prospects. Falling export demand would be felt acutely in Taiwan and Malaysia. Meanwhile, cheaper Chinese goods imports could add to deflationary pressure in the likes of Singapore. Longer term, markets in the region are vulnerable to Chinese economic instability and its impact on exports and commodity prices around the region.  At the outset, markets wondered how far the RMB depreciation would be allowed to go. The stability that was regained at the end of the week suggests the move could be modest. This suggests that Beijing has limited appetite for any kind of currency war. And if the PBOC is successful at inviting more market-driven forces in without inviting new criticism of currency manipulation, it will enhance the RMB’s chances of inclusion in the IMF’s SDR basket.

At the outset, markets wondered how far the RMB depreciation would be allowed to go. The stability that was regained at the end of the week suggests the move could be modest. This suggests that Beijing has limited appetite for any kind of currency war. And if the PBOC is successful at inviting more market-driven forces in without inviting new criticism of currency manipulation, it will enhance the RMB’s chances of inclusion in the IMF’s SDR basket.

But there could be some very nervous moments in the weeks ahead. If the real driver behind the RMB’s depreciation is further weakness in the Chinese economy, the consequences will be felt far beyond the currency markets.

The Productivity Puzzle – A New Understanding

Productivity growth in advanced economies was slowing before the Great Financial Crisis and has remained muted since. The Organization for Economic Cooperation and Development (OECD) presents a new view on why productivity slowed and offers solutions to correct the problem.

Why does productivity growth matter? Over the long run, standards of living will improve only if people get better at producing goods and services. In addition, the challenges of fulfilling pension obligations and honoring sovereign debt obligations to investors can be met only if productivity continues to advance.

There are different explanations for slowing productivity growth. Pessimists blame a dearth of good ideas, while optimists believe that there are plenty of good ideas that simply need to be leveraged. The OECD report focuses on this latter aspect – the diffusion of productivity.

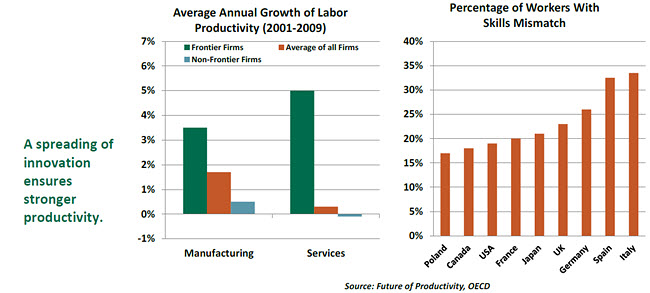

Detailed research of the OECD countries shows that businesses are still involved in productivity- enhancing processes, but some are doing significantly better than others. “Frontier firms” are more productive, more profitable, likely to belong to a group, and patent more intensively than other firms. In the manufacturing sector, frontier firms (the 100 most-productive firms globally) saw output per worker increase at an annual rate of 3.5% during 2001-2009. That compares with only a 0.5% gain for “non-frontier firms” (average of all other firms). In the service sector, the gap was larger; frontier firms raised productivity by 5% each year versus only 0.3% among non-frontier firms.

The key finding of the OECD research is that “the main source of productivity slowdown is not so much a slowing of innovation by the globally advanced firms, but rather a slowing of the pace at which innovations spread out throughout the economy.”

Diffusion of innovation is determined by four key factors. First, experimentation by firms, particularly new entrants, with new technology and business models promotes a spreading of innovation. By and large, the share of start-up firms during the period of investigation dropped among all OECD members, including the United States.

Second, global connectedness through trade with frontier firms results in higher productivity as innovation is diffused. This research found that during 2001-2009, Austria traded very little with frontier firms, which prevented capturing innovation from such firms. In the same period, the experience of Canada’s global connections with frontier firms raised productivity in Canada.

Third, a large skill mismatch (the gap between job requirements and the capabilities of candidates) impedes the diffusion of innovation and labor productivity growth. The study shows that better human talent can boost the level of productivity. Italy and Spain, in particular, could benefit from reducing their skill mismatches (about 35% of workers in those countries are affected, according to the OECD).

Fourth, investment in knowledge-based capital (such as software, patents, managerial quality) enables economies to learn, adapt and secure the full benefits of new technologies. The research findings show that a noticeable decline in investment of knowledge-based capital across all major OECD countries during 1995-2010 led to a slower diffusion of innovation.

The OECD identified a few options that might enhance the diffusion of innovation and change the outlook for productivity. These include reforms in product markets to enable adoption of new technologies; closer collaboration between firms and universities; and reducing barriers to entrepreneurship. They also include minimizing costs of bankruptcy and reducing misallocation of human skills.

The hot debate about productivity growth will continue. The OECD research project has identified a core of the productivity problem, but it may take some political will to solve it.

Prodding Along

I was frantically threshing through a stack of household invoices before leaving on vacation a couple of Fridays ago. Amid all the requests for payment was a letter from the power company that, happily, did not ask for money. Instead, it lined up our electricity usage with the rest of the neighborhood, and praised us for being more efficient than average.

On the drive out of town, I was wondering why a utility would send such an analysis to homeowners. Ultimately, I concluded that it was a subtle prompt to encourage conservation. The letter had framed consumption as a kind of competition, where using fewer megawatts got you ahead. Our family was being nudged to lower our carbon footprint.

As it happened, my main summer reading was entitled “Nudge,” by University of Chicago economists Richard Thaler and Cass Sunstein. Thaler and Sunstein are students of behavioral science, which has consistently revealed that consumers are not the efficient, rational actors that we read about in textbooks. “Nudge” is about recognizing these imperfections and trying to steer people in a manner that is helpful to them.

Neoclassical perspective assumes that profit-maximizing agents synthesize information quickly and correctly, bringing efficiency to transactions and self-discipline to markets. If you believe this premise, any attempt to regulate or steer the process is viewed as intrusive and bound to produce sub-optimal outcomes.  However, a growing body of evidence is finding that rationality among consumers is the exception rather than the norm. We are often fooled by clever pricing and marketing and do not always process information well. The more complex the question, and the more choices we have, the worse we tend to perform.

However, a growing body of evidence is finding that rationality among consumers is the exception rather than the norm. We are often fooled by clever pricing and marketing and do not always process information well. The more complex the question, and the more choices we have, the worse we tend to perform.

One reason we perform so poorly in complicated situations is that our decision-making process has two stages. The first, which Malcom Gladwell has described as “thin slicing,” tries to reach a conclusion quickly and intuitively. The second stage goes into deeper analysis but takes a much greater physiological toll. Subjects engaged in more-advanced contemplation have elevated heart rates, dilated pupils and are often so focused that they lose the capacity to see and hear things. This video is a classic illustration of what happens when we get too locked in.

So even if we are smart, the way we are wired leads us to try to simplify or defer tough decisions. This can have deleterious effects in a number of arenas. Thaler and Sunstein highlight personal finance as one of them. This is a subject that is hard for both sophisticates and laymen (“econs” and “humans” in the book’s vernacular), leading to poor decision-making. Many habitually make bad investment choices and fail to take advantage of opportunities to save.

To correct for our inherent imperfections, Thaler and Sunstein advocate “paternal libertarianism,” a system in which people are nudged to do things which are in their best interests. Examples in the financial arena include automatically enrolling beneficiaries in retirement plans unless they opt out of them. They also include creating default contribution rates and asset allocations that take some of the guesswork out of the process. This kind of “choice architecture” helps start plan participants on the right foot and will continue serving them well even if they fall back into inertia.

Nudging strategies are being used in a range of areas, from the mundane to the significant. The book’s enumeration of these is illuminating; the reader comes to understand that we are being pushed along in ways that we don’t appreciate. Nudging is not universally endorsed, however; choice architecture can sometimes work against consumers (auto renewals of those magazines we never read is a good example).

As one who was trained in classical economics, allowing for the imperfections of human beings was initially difficult. Today, one cannot understand market function without accounting for the behavioral aspects that “Nudge” does an excellent job of illustrating. It is certainly worth taking along on your next vacation.

(c) Northern Trust