Many investors and advisors are unsure about the current financial market environment. They have been wrestling with how to weight equities and whether to include alternative investments. Although equities have performed well in recent years, many alternatives have lagged expectations. This should not be surprising: the financial world is operating just as the Fed has intended.

Over the past few years, analysts have pondered whether and when the Fed will start to change its intentionally distortive policies. Many hedged portfolios have remained diversified due to that uncertainty, and unfortunately they have often underperformed expectations.

The repeating pattern—and unprecedentedly long era—of interest-rate and bond-market interventions now has many investors capitulating to a new world outlook. As an analogy, it’s as though nine heads in a row from coin flipping has led to an expectation of perpetual heads. As irony would have it, this shift in attitude is gathering pace just as signs of change are appearing on the horizon.

In this article, we’ll review various reasons why equities have overperformed and alternative investments have underperformed in recent years. We’ll see that conditions are ripening for a reversal of that pattern. Changes and risks that have not been present for years are now on the market’s calendar. Portfolio diversification and risk hedging are more important now than they have been in quite a while. Yet the current momentum of the market is upward; thus portfolios should remain exposed while also sustaining protection from downside risks.

The convergence of numerous factors is beginning to raise a yellow flag of caution for the stock market. These are not definitive signals of an impending turn, but rather they represent dark clouds of risk on the near horizon. This outlook does not indicate that investors should retreat from stock market investments; instead, investors should consider a bias toward the “rowing” strategies that were conceptually presented in chapter ten of Unexpected Returns: "Row, Not Sail". Rowing strategies represent a more diversified, risk-managed approach to investment portfolios. The intended effect is to limit a portfolio’s participation in downside losses while capturing a portion of upside gains. The cumulative effect generates compounded returns that exceed the minimal equity returns of secular bear markets. An illustration of the benefits of rowing is discussed in "Half & Half: Why Rowing Works".

The evidence is compelling that current conditions in the stock market represent a secular bear period. Some prominent analysts have succumbed to the intoxicating effects of the ongoing cyclical bull market and now call for an extended secular bull run. Their charts, positions, and Crestmont’s exposé on the issues are included in the July 6, 2015 article “Are We There Yet?”.

Over the longer term, the stock market environment fluctuates from above-average-return secular bull markets to below-average-return secular bears. The most recent secular bull lasted from 1982 through 1999, yielding to the start of a secular bear in 2000. Secular periods includes numerous shorter-term cyclical cycles. These interim cycles are primarily driven by investor psychology and short-term factors—as a result, they are somewhat random and hard to predict.

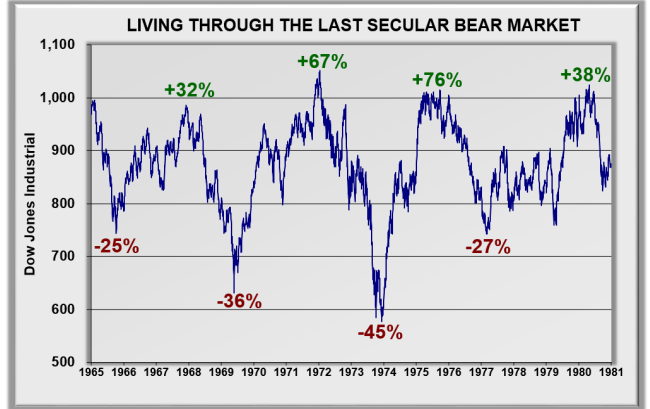

The current secular bear is progressing similarly to the previous secular bear of 1966- 1981. That notorious period consisted of dramatic cyclical cycles that churned upward and downward. Earnings grew over the period, yet P/E valuations declined, thereby stifling the market’s advance. Today’s secular bear includes all of the same elements. It also includes a cyclical bull that has reached new highs… just as in the early 1970s. Investors have been teased to expect a long-run launch. Figure 1 presents the cyclical bulls and cyclical bears for the current secular bear market; Figure 2 provides a view of history to contrast the current cycle with the previous one. Despite the apparent pattern of cyclical cycles, they are much more random and harder to predict than secular cycles.

Figure 1. Cyclical Cycles in the Current Secular Bear

Figure 2. Living Through the Last Secular Bear Market: 1966-1981

Yet randomness at times coexists with propensity. Although a tenth coin flip involves the same probabilities as the first, would you not bet differently following nine heads in a row?

CATALYSTS & CONDITIONS

Catalysts are fuses; they represent sparks that ignite unstable situations. Conditions are the fuels that lie vulnerable to ignition. Catalysts may give rise to an event, while the conditions determine what, if anything, happens next. Even as recently as a year or two ago, the catalysts for a change in the stock market environment were distant enough to bend away from visibility on the horizon. They were beyond the view in the headlights. The conditions were still evolving and had not reached the levels that exist today. But time passed and the catalysts of change have grown in strength, setting the stage for heightened risk, while at the same time they are preparing an environment of opportunity.

In a typical secular bear environment, investors will find that the more actively managed and skill-based rowing strategies tend to outperform the more passively managed and market-exposed sailing strategies. Not only can skill and value find opportunity, but passive market-based returns—across full cycles—are very limited in secular bears.

Nonetheless, the skill-based and value-oriented investments that are generally successful in naturally functioning markets have been distorted in recent years. With good intentions, the Fed and the federal government (“D.C.”) have imposed policies and programs that have led to misalignments and complacency in the markets and in the economy. The reversion back from such market distortions should create a foundation to restore conditions that will again enable those who are skillful to manage risk and deliver returns.

The financial markets are in the seventh year of the Fed’s zero interest rate policy (ZIRP). ZIRP is the artificial suppression of short-term interest rates to zero or near-zero percent. Its goals have been to stimulate the economy by lowering the cost of borrowed money and to motivate investors to allocate capital to the stock market in order to promote a wealth effect that drives economic growth. Regardless of whether ZIRP has achieved its laudable goals, it has intentionally distorted market relationships. Distorted markets alter the effectiveness of skill-based and value-oriented investment strategies. This occurs because such strategies rely upon the ability of managers to identify and select undervalued and overvalued investments. When markets experience dislocated or manipulated relationships, skill acts as though it is executing in Alice’s Wonderland.

Recent statements from the Fed indicate the likelihood of an increase in interest rates and an end to ZIRP during 2015. Keep in mind, however, that a major election year is approaching. That could create an excuse for the Fed to further delay the end of ZIRP. Regardless, ZIRP’s conclusion is clearly on the foreseeable horizon.

Around the same time that the Fed started ZIRP, they initiated a series of bond-buying programs known as quantitative easing (QE). The purposes of QE have been to lower longer-term interest rates, provide liquidity to the financial markets, and promote higher stock prices. Like ZIRP, QE intentionally distorts the markets for laudable purposes. After accumulating $4.5 trillion in assets, the Fed ceased QE in October 2014. They have indicated that a reversal of QE will not occur until the Fed ends ZIRP. Now that ZIRP’s end is forthcoming, the reversal of QE may not be far behind.

In addition to the Fed’s monetary policy actions of ZIRP and QE, D.C. implemented a series of fiscal policy programs that were intended to stimulate the economy. Although there have been a range of beneficiaries, many of the programs were ultimately counter-productive toward their intended goals. Other programs favored some industries at the expense of others. For the economy overall, such fiscal distortions cause a misalignment of resources and relationships. Regardless, the upcoming election year will change the leadership in the executive branch of government. It is unclear whether the effects will include a reversal of recent policies or an extension of them in new forms. Either way, a change in fiscal policy is now on the near horizon.

Although reversing and ending the distortive programs may initially roil the financial markets, the end result should be to restore market relationships, thereby leading to more naturally functioning conditions. The resulting investment environment should be much more favorable for skill-based and value-oriented strategies.

CONDITIONS ARE FUEL LOADS

Beyond the upcoming catalysts from the Fed and D.C., the current market environment is being affected by a series of market technical factors, economic issues, and the level of valuation. These are not the reasons to expect a change in the investing environment; instead, they are the conditions that will potentially facilitate or accentuate the change. Analogously, a long period without fire in a mature forest does not cause such an incident, but rather the long period builds fuel loads that are susceptible once the catalyst of lightning or irresponsible visitors creates a spark. Likewise for the market, the following series of elements represents market conditions that should be watched closely.

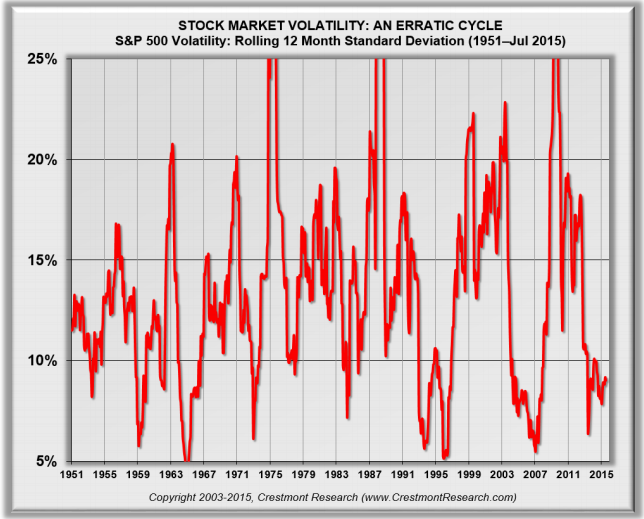

The first element is the technical factor of market volatility… or the lack of it! Low volatility and long periods without corrections don’t cause future changes in the market environment, but they do set up the conditions that can accelerate or accentuate them once they do occur. Keep in mind that low volatility is an indication of a recent and current good market; it is not an early indicator of a good market to come. High or rising volatility is an indicator of a declining market.

As shown in Figure 3, the current level of volatility in the stock market falls within the lowest 20% of all periods since 1950. Our present period of low volatility has lasted for more than two years. As reflected in the graph, volatility itself has an erratic cycle. Although market volatility could remain in the low zone for some time longer, the pressures and risks from low volatility are building.

Figure 3. The Volatility Cycle

The eerie calm in the market is evident not only in the graph’s measure of volatility but in other signs of a mounting fuel load. Just as mild forest fires help to reduce fuel loads and prevent major fires, market corrections (well-named) help to correct a variety of unhealthy factors. Many market analysts use a ten-percent threshold to designate a healthy correction. As of August 2015, the S&P 500 is experiencing its third longest period without a ten-percent correction. It would need to make it to mid-April 2016 to move into second place.

In summary, market volatility has been fairly low for a relatively extended period, and the S&P 500 Index has gone a long time without a healthy correction. Both issues reflect conditions of latent risk; they are not foundations that support a continuation of the current cyclical bull market.

The second element of market conditions to watch is a series of economic issues. Although economic growth is not a significant cause of secular market cycles, it can be a driver within shorter-term cyclical cycles. The cycles of economic expansions and recessions tend to provide a relatively stable economy over the long term. As a result, their impact on long-term market cycles is relatively limited. In the shorter run, however, the surges of expansions and pauses of recessions can create psychological and statistical drivers in the market. The average economic expansion over the past six decades has been about 62 months. The current expansion has exceeded the average by almost a year and is now the fourth longest among eleven. Although the economy could continue to expand for years to come, the extended length of this expansion and growing risk of recession acts as another condition of vulnerability for the market.

Also, as the Fed raises interest rates it is likely that the U.S. dollar will strengthen against foreign currencies. A stronger dollar makes U.S. goods less competitive internationally. As a result, a strong dollar can create economic headwinds. Recession risk (or fear) and economic headwinds thus represent a second element of adverse conditions for the market.

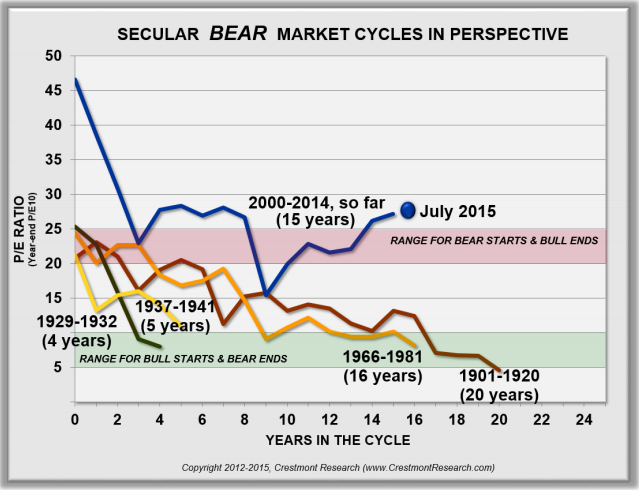

The third element is the relatively high valuation of the stock market. This was discussed in more detail in “Are We There Yet?”, published on July 6, 2015. Rather than reiterate all of the points from that piece, let’s review one chart that emphasizes the high level of market valuation and the related comments from the article.

Figure 4 presents P/E during secular bear market periods. Since bears start where bulls end, the starting level for P/E in secular bear markets is generally in the red zone on this chart. The obvious exception is the most recent secular bull, whose dramatic end in a bubble gave our current secular bear quite an extra distance to travel.

Figure 4. Secular Bear Market P/E

The current secular bear market has lasted a long time. It’s reasonable that investors want to return to a secular bull market environment, but the reality is that the level of stock market valuation (i.e., P/E) is not low enough to provide the lift to returns that drives secular bull markets. As a matter of fact, P/E is at or above the typical starting level for a secular bear market.

The current situation is not the result of P/E hibernation over the past 15 years. P/E has declined by nearly the same number of points as it has historically in a typical secular bear. This secular bear, however, started at dramatically higher levels due to the late 1990s bubble. The market’s work of the past 15 years has been to deflate the excesses that preceded it.

Currently, valuations are high and vulnerable. Many analysts have confirmed this in a variety of ways, yet others are more optimistic. One of the more credible statements recently about high valuations in the stock market came from Fed Chair Janet Yellen on May 6, 2015: “I would highlight that equity market valuations at this point generally are quite high.” Although she avoids using the artful words of a previous Fed Chair (i.e., “irrational exuberance”), the message is clear that stock market values are high. As a result, without another bubble period, future returns are limited and the market is more vulnerable to negative surprises than it is poised for positive outcomes.

CONCLUSION

The blissful market environment of the past few years is now being disturbed by elements of change in the air. Although new directions by the Fed and D.C. are inevitable at this point, they are not necessarily imminent. Nonetheless, they are known, likely, and significant… and they are on the market’s and the economy’s radars over the upcoming quarters and year.

Invoking a baseball analogy, these changes are not the fastball surprises of a financial crisis like 2008, but rather they are a slow knuckleball from a particularly unpredictable pitcher. In response to 2008, the Fed implemented a policy of softball pitches to promote base hits and home runs. In recent years, skill was less relevant than simply swinging the bat of overweighted allocations. Going forward, policy will soon change and other environmental conditions will shift. Skill should be on deck and ready to prove itself.