Introduction

After an exhaustive search of the dividend growth stock universe I identified 20 dividend growth stocks that I felt were currently worthy of consideration for retirement portfolios based on valuation. In part 1 of this 2-part series found here I discussed the current level of the S&P 500, and offered some important principles about valuation. Additionally, I offered the first group of 10 of what I consider the highest quality members of the 20 screened research candidates I uncovered. In this part 2, I will present the final 10 of 20 attractively-valued dividend growth stocks that I felt were currently worthy of consideration based on attractive or fair valuation relative to the overall market.

My search criteria were rather simple and straightforward. My primary objective was to identify a group of attractive or soundly-valued dividend growth stocks from which a portfolio could possibly be constructed. Since my focus was on retirement portfolios, my additional objective was to put together a portfolio that in the aggregate would offer a current dividend yield greater than 3%. I also screened for investment grade quality and a consistent record of both paying and increasing dividends. In addition to above-average dividend yield and dividend growth, I was also looking for a conservative group of companies that as a group might produce a reasonable level of future capital appreciation.

Clarifications on the Importance of Valuation

Before I present the second group of 10 research candidates, I would like to offer some clarifications on the importance of valuation. Part 1 of this 2-part series generated a lively comment thread of more than 280 comments at last count. Although I appreciate everyone’s contributions, there were 2 comments in particular that I felt missed the primary thesis of this series. Consequently, I decided to share those comments in this article and take the opportunity they provided to offer some important insights on the significance of valuation.

The first comment came from Buyandhold 2012 who regularly contributes comments to my articles and many others. His position is that since we are in the seventh year of a strong bull market, no stock should be bought. My retort to that position is one that I often make: “it is a market of stocks, not a stock market.” In other words, I believe in building portfolios one company at a time with a primary focus and discipline on fair valuation.

Regardless of the market level, I am primarily interested in the valuation level of the individual company I am interested in investing in. Even if the market was extremely low, I would not invest in any company if I did not consider it fairly valued based on fundamentals at the time. I consider this especially true for retired investors in need of current income to live on.

To these investors, I believe that time in the market is significantly more important and relevant than attempting to time the market. My point is that every dividend that you forgo is one that you will never get back. Stock prices will constantly fall and rise, but eventually move into alignment with fair valuation. However, they tend to fall less from fair valuation than they would when the company is overvalued. I will illustrate that more fully next, but first here is the full comment from Buyandhold 2012:

“Buyandhold 2012

Chuck, I agree with you that we are in the seventh year of a strong bull market. That is the reason that I will not by buying any of the 20 dividend growth stocks on your list of stocks to buy today.

It seems to me that I am stating the obvious when I point out that the seventh year of a strong bull market is not the best time to buy any stocks.

The difference between buying a stock at the right time versus the wrong time can add up to thousands and even millions of dollars over the long term.

Those who forget history are condemned to repeat it. Look back at the history of the stock market and you will see that the seventh year of a strong bull market was never the best time to buy any stocks.”

The second comment that I wanted to clarify came from an anonymous commenter that calculated the price drops of the 10 research candidates I presented in part 1. Although I believe his calculations were correct, they were not accurate if they were made based on how far those same stocks dropped from fair valuation. Therefore, utilizing the calculating function of the F.A.S.T. Graphs™ research tool I ran the same calculations on the 10 research candidates based on how far they fell when their stock prices were at fair value. Here is his comment, followed by my calculations based on fair value:

“ 266697213

I am wondering how many people who say that it is only income that matters not value when it comes to DG stocks, went though the Great Recession holding DG style stocks.

Here is how much each of the 10 stocks discussed in the article dropped during the Great Recession:

JNJ -30% -

WMT -22%

CSCO -55%

IBM -37%

PG -37%

RY -55%

CMI -70%

QCOM -40%

ADM -55%

AFL -75%

That's an average of -53%

Imagine if you had a 1M portfolio and it then went down 500k. Add to it the possibility that in these kind of conditions some of the companies are probably going to cut their dividend as did PFE despite its long history of increasing dividends. How sure would you feel about your strategy at that point. To simply say, "Well it bounced back so alls well that ends well." is to ignore the psychic pain involved in this kind of drop which can cause people to make poor decisions. It also smacks of a false bravado borne out of a raging bull market.”

Price Drop from Fair Value Dividend Cut: Yes or No

The calculations of how much the 10 stocks presented in part 1 dropped during the Great Recession were not made from fair value. They were made from highs coming into the recession which coincided with overvaluation for most of the 10 companies. I made those same calculations from when the stocks were, in fact, at fair value and the short-term price damage was much lower as follows:

JNJ -30% 18.49% no

WMT -22% 00.00% no

CSCO -55% 35.42% no dividend at that time

IBM -37% 32.97% no

PG -37% 14.10% no

RY -55% 50.54% no

CMI -70% 70.00% no

QCOM -40% 00.00% no

ADM -55% 47.78% no

AFL -75% 71.47% no

That’s an average of -38.18% not - 53%, and all of the companies did, in fact, recover quickly (within 18 months) except for Aflac, which was a US financial, and Cummings Inc, which as I referenced in part 1, a cyclical. I acknowledge that a 38% drop is still large, but clearly exercising the discipline to only invest at fair valuation is a risk reducer. But more importantly, none of these 10 companies cut their dividend, but instead, increased their dividend at rather large rates.

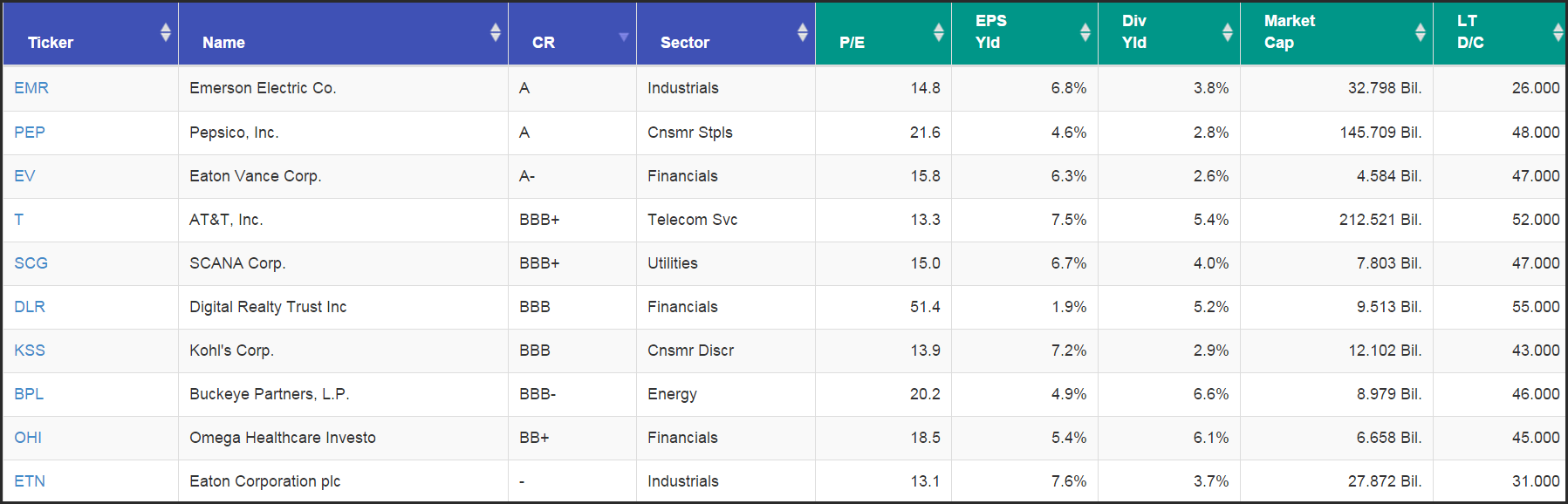

Final 10 Research Candidates with an Average Current Yield Of 4.3%

Although most of the final 10 research candidates have investment-grade credit ratings, I would suggest that they are not of the same quality of the 10 candidates presented in part 1. However, that is not to suggest that they are not all high-quality dividend growth stocks. For example, Omega Healthcare is a REIT with a BB+ S&P credit rating, which is healthy for a real estate investment trust. Eaton Corporation is headquartered in Ireland, and has no S&P credit rating, but a strong balance sheet and a low debt to capital ratio of 31%.

Therefore, these candidates could technically be thought of as a little more risky, but I do not consider them high risk. On the other hand, greater risk should come with greater opportunity for profit and/or higher income. Most of the 10 research candidates in this group either offer higher income, higher capital appreciation, or a combination of both than what was found with the 10 higher quality candidates presented in part 1. Consequently, when combined with the first 10 research candidates, the complete group potentially offers risk control, high-yield and above-average capital appreciation potential.

The following portfolio review presents the final 10 fairly-valued research candidates in order of highest S&P credit rating to lowest. The table presents the following important metrics: S&P credit rating, sector, P/E ratio, earnings yield, dividend yield, market cap and long-term debt to capital. Just as I did in part 1, I will present an earnings and price correlated F.A.S.T. Graphs™ since calendar year 2007 on each individual candidate, followed by a near-term earnings forecasting calculator and an analyst scorecard illustrating the historical record of analysts making forecasts on each company.

Also, just as I did in part 1, this is offered as the first step prior to a more comprehensive research effort. Just like I did in part 1, I will present a brief commentary on each company to get the investor started. There is a significant amount of fundamental research contained in each of the earnings and price correlated F.A.S.T. Graphs™ presented in both parts 1 and part 2 of this series.

Therefore, I strongly suggest that the reader spend some time analyzing and evaluating what these fundamental oriented graphs reveal. The primary points I suggest focusing on are the earnings and price correlation over time (the orange and black lines), and especially how price eventually responds to earnings when they get disconnected. I also suggest focusing on the dividend line (the white line in the dark green earnings) and notice how it continuously rises in spite of price volatility.

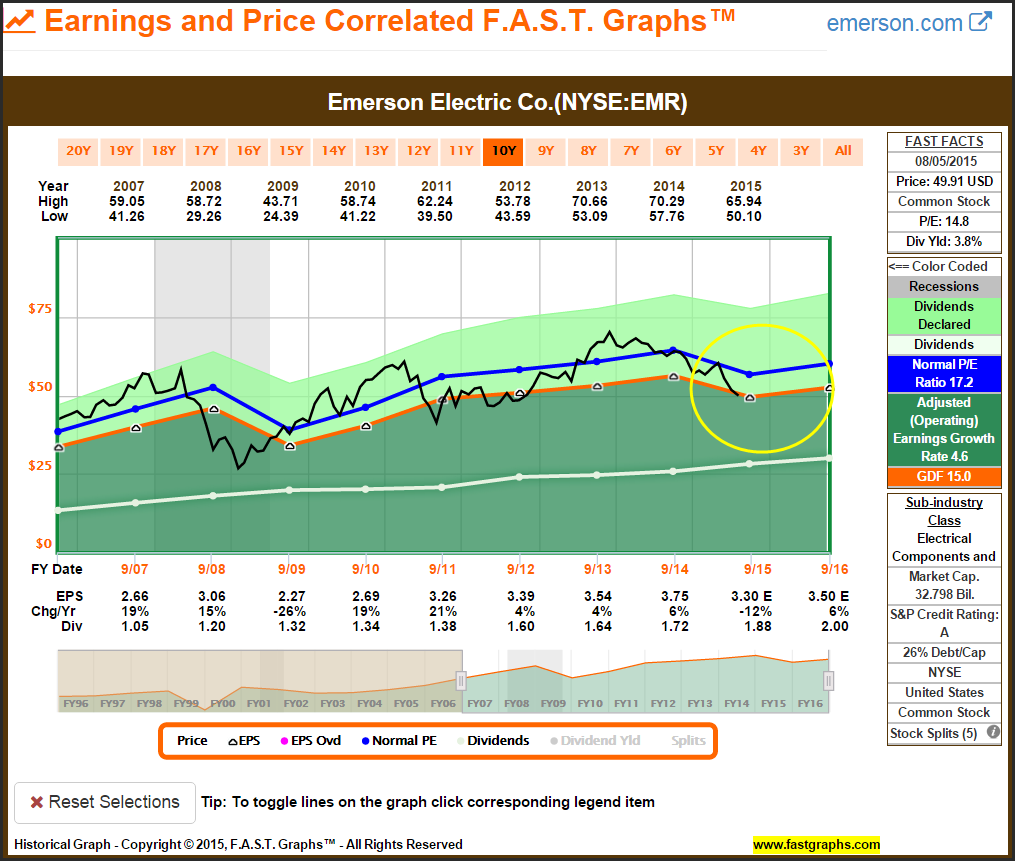

Emerson Electric Co. (EMR)

Emerson Electric is a high-quality industrial company engaged in the electrical components and equipment subsector. As such, its operating earnings history is what I would call quasi-cyclical. In other words, it is not a deep cyclical; instead, it is a company that experiences occasional periods of earnings weakness typically followed by longer periods of earnings growth and strength. Emerson is a Dividend Champion that has increased its dividend for 58 consecutive years.

This recent earnings weakness has caused the stock to come off of previous highs into fair valuation territory. Emerson is A rated, offers an above-average current yield of 3.8%, and is expected to return to historical earnings growth levels in the future. Consequently, I believe the company is an excellent opportunity for the conservative long-term dividend growth investor to consider today.

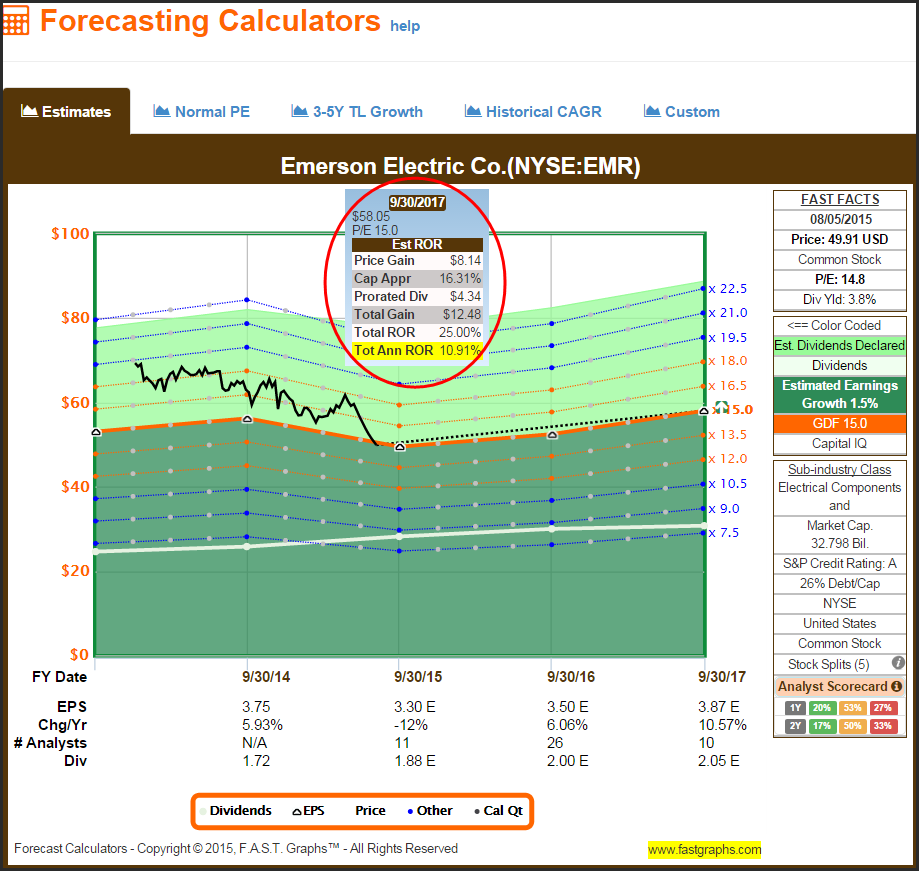

As evidenced by the earnings and price correlated graph, Emerson Electric is a high-quality Dividend Champion that has a legacy of the market placing a premium valuation on its stock. Nevertheless, the following forecasting calculator suggests that Emerson would offer close to a 9% total annual return out to fiscal year-end September 2017, assuming analyst forecasts are correct and the company maintains its current P/E ratio of 15. If the market capitalized Emerson’s earnings at its historical normal P/E ratio of 17.2 the total annualized rate of return out to fiscal year-end 2017 would be greater than 15% per annum.

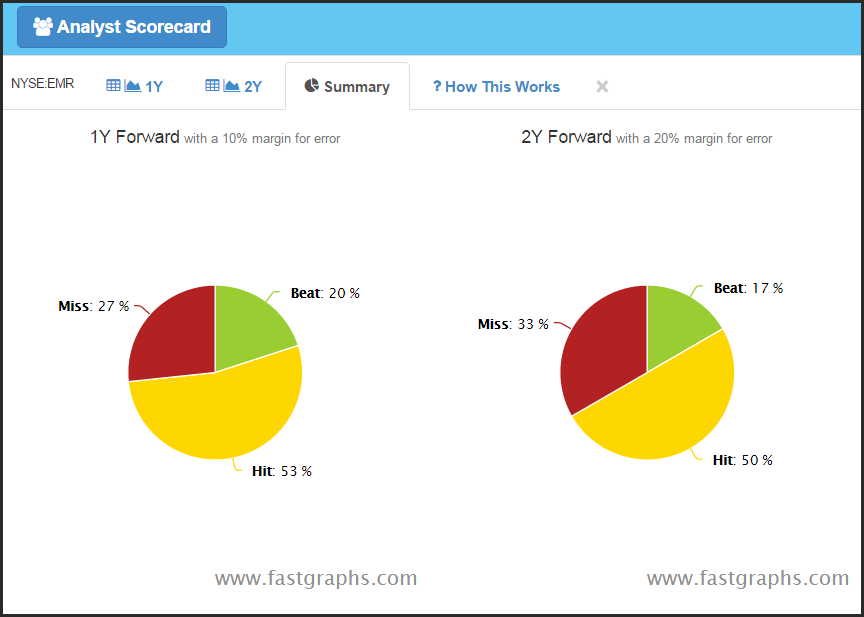

Analysts have been reasonably accurate forecasting Emerson’s earnings in the past. However, due to the quasi-cyclical nature of the company’s earnings, prospective investors should be aware that when analysts have missed in the past, the misses have been large.

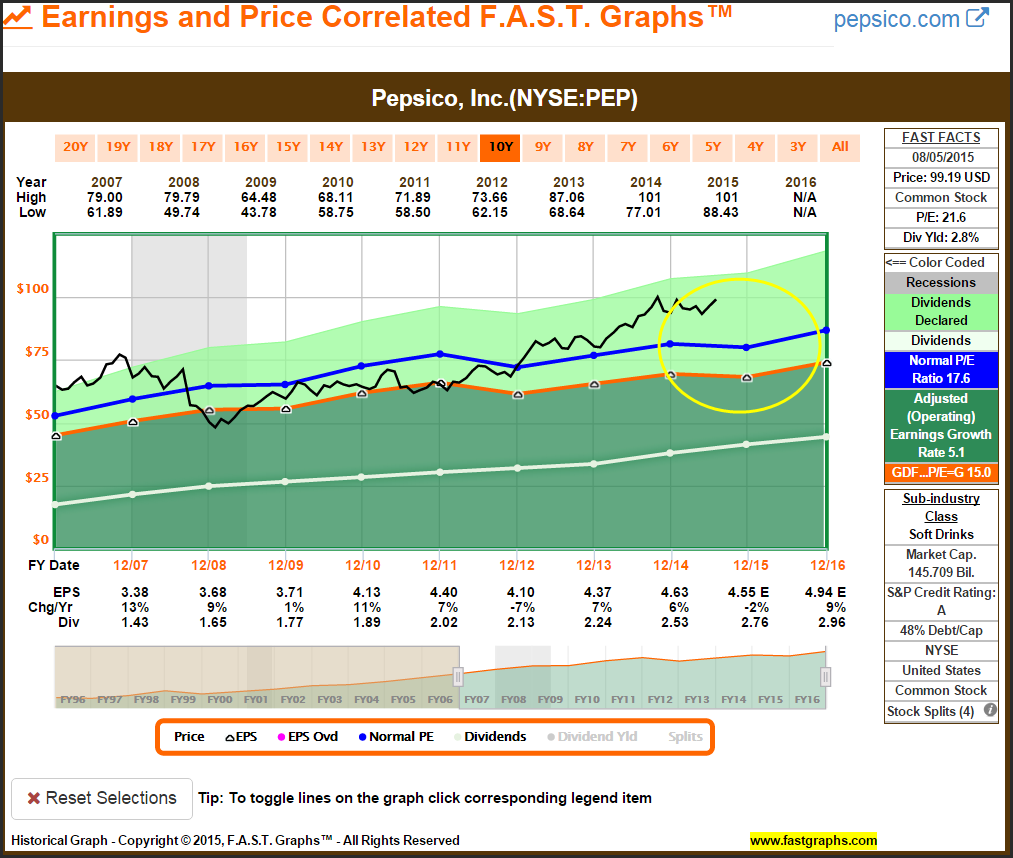

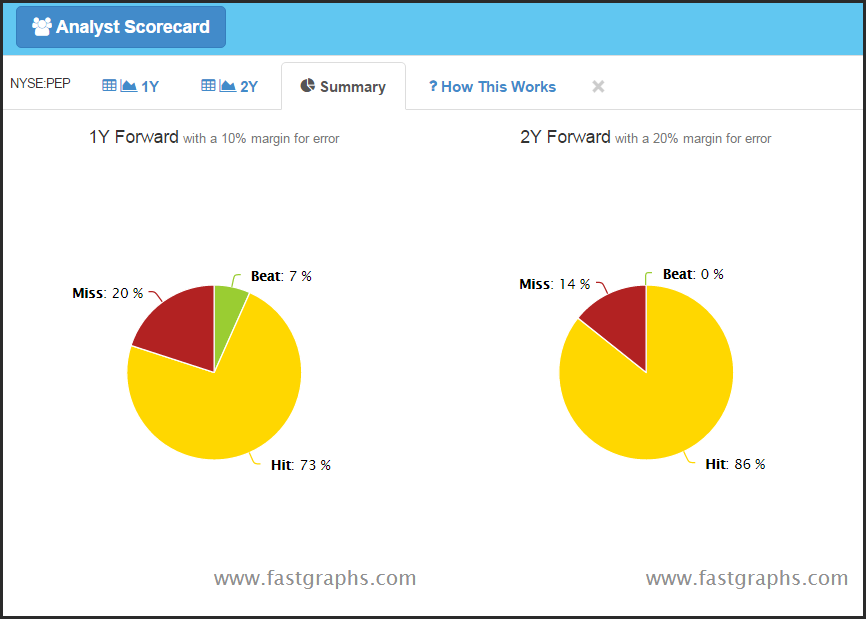

PepsiCo Inc. (PEP)

In a similar fashion to Emerson, PepsiCo has enjoyed a history of the market placing a premium valuation on its stock. Nevertheless, the company’s current blended P/E ratio is higher than the normal P/E ratio the market has applied since 2007. However, after reviewing a longer term graph since 1997, PepsiCo’s historical normal P/E ratio has been 21.6.

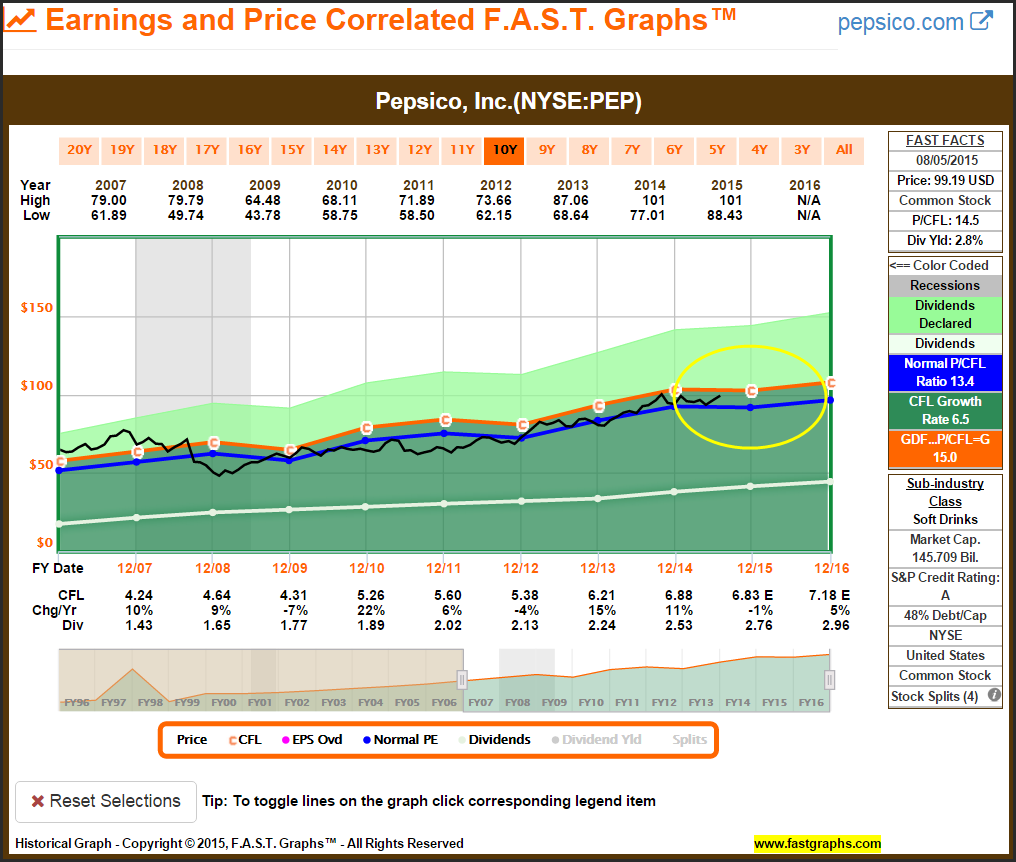

Interestingly, when you evaluate PepsiCo’s valuation based on cash flows, you discover a very high correlation. Consequently, on the basis of cash flow to stock price, PepsiCo currently appears fully but fairly valued. I leave it up to the discretion of the reader to decide.

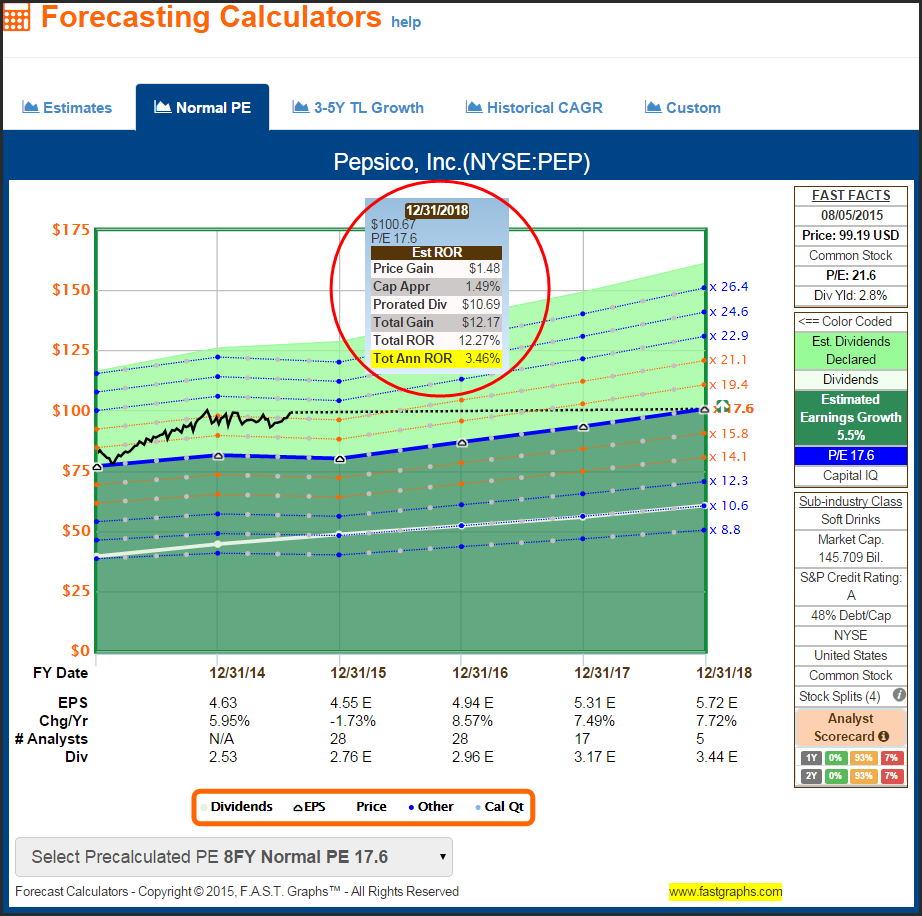

When you evaluate PepsiCo based on forward earnings forecasts and value it at its historical normal P/E ratio of 17.6, its prospects are not that exciting. The company does pay a 2.8% dividend, which would represent the bulk of any future return basis utilizing earnings and the premium historical normal P/E ratio since 2007.

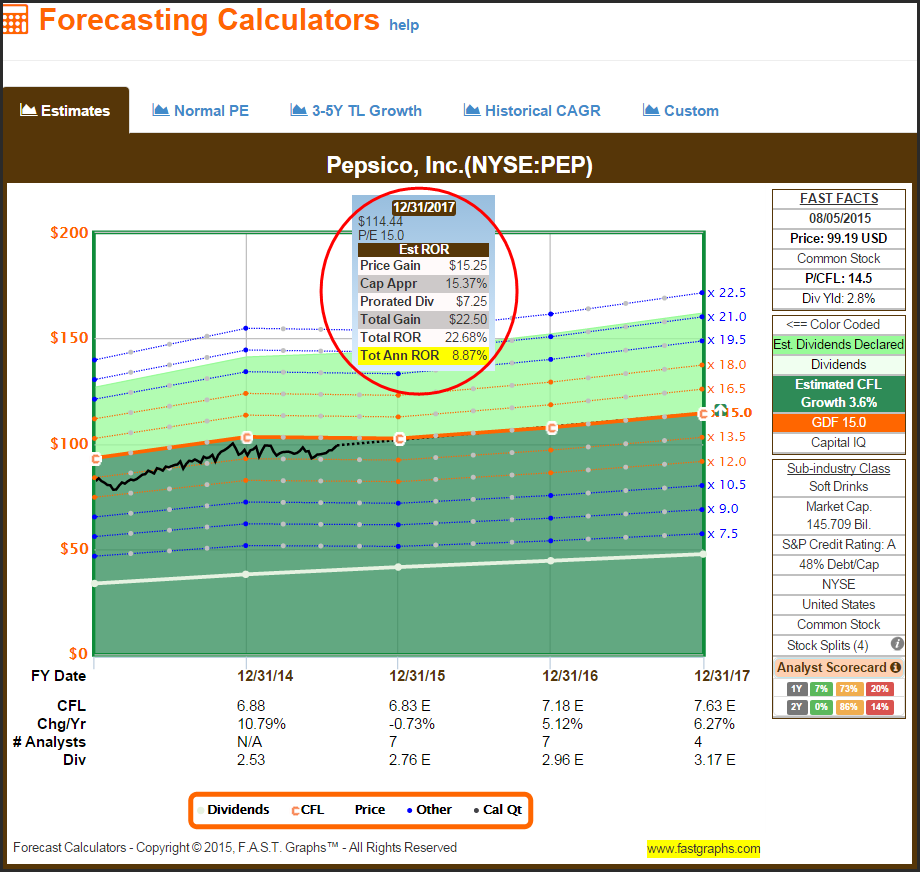

On the other hand, if you evaluate PepsiCo’s future return potential based on cash flows, the total rate of return potential is significantly better. Under this scenario, dividends would still produce a major contribution to total return, however, capital appreciation would be greater based on cash flow than earnings.

Analysts have been very accurate when forecasting PepsiCo’s future earnings.

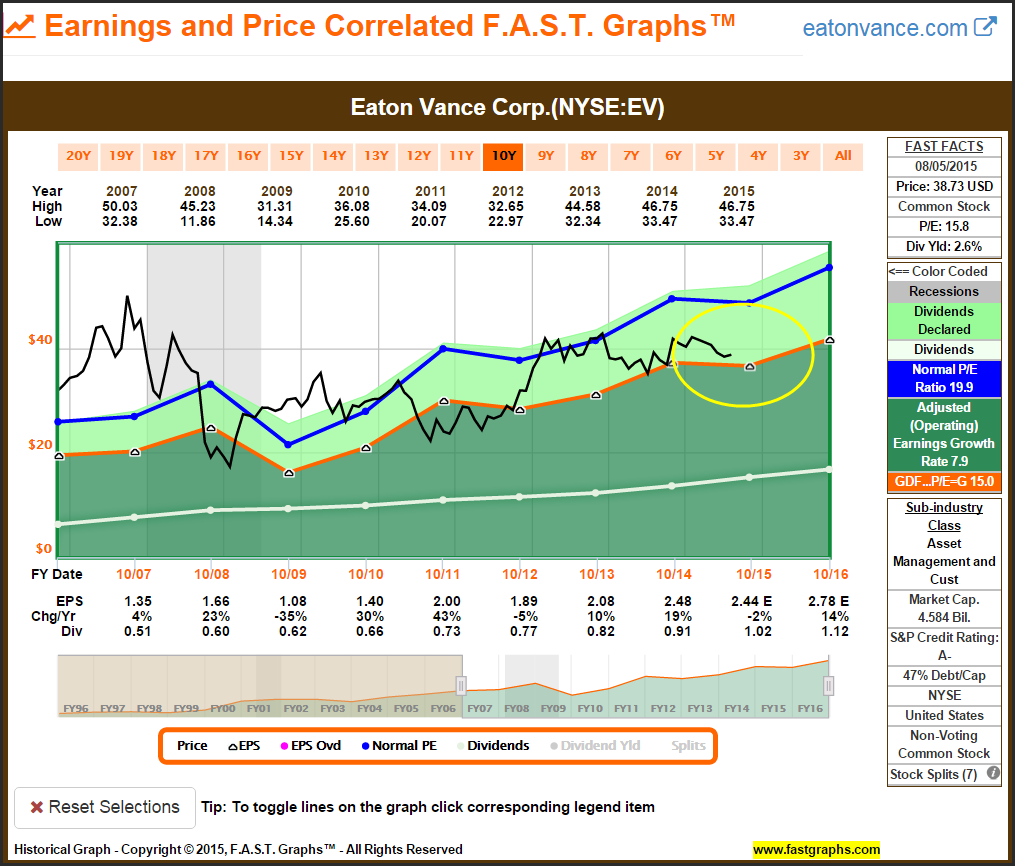

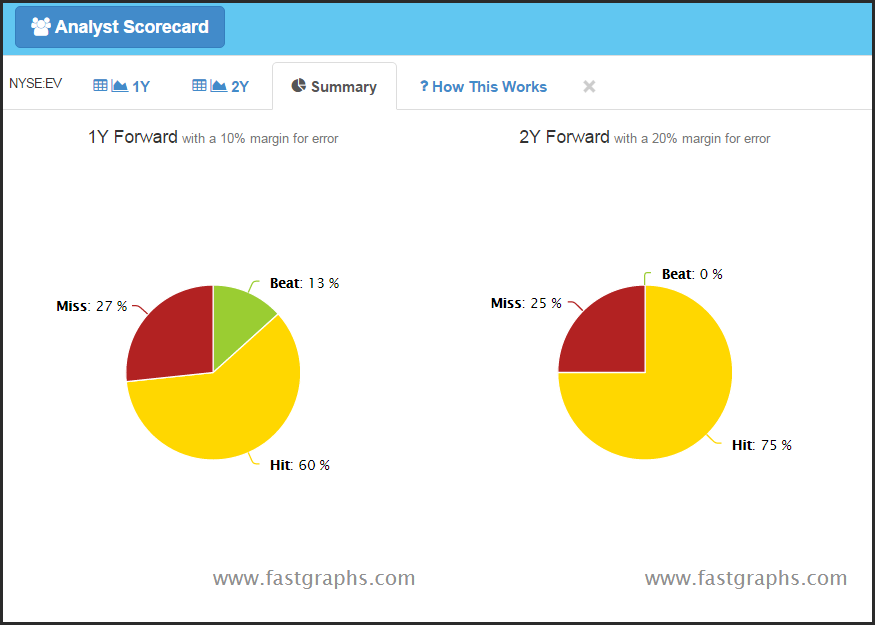

Eaton Vance Corp. (EV)

Eaton Vance is a Dividend Champion that has increased their dividend for 34 consecutive years. When analyzing their historical earnings and price correlated graph, we discover that the market often places a premium valuation on its shares. Consequently, its current blended P/E ratio of 15.8 appears sound on that basis. The company’s current dividend yield of 2.6% is modestly above the S&P 500 index.

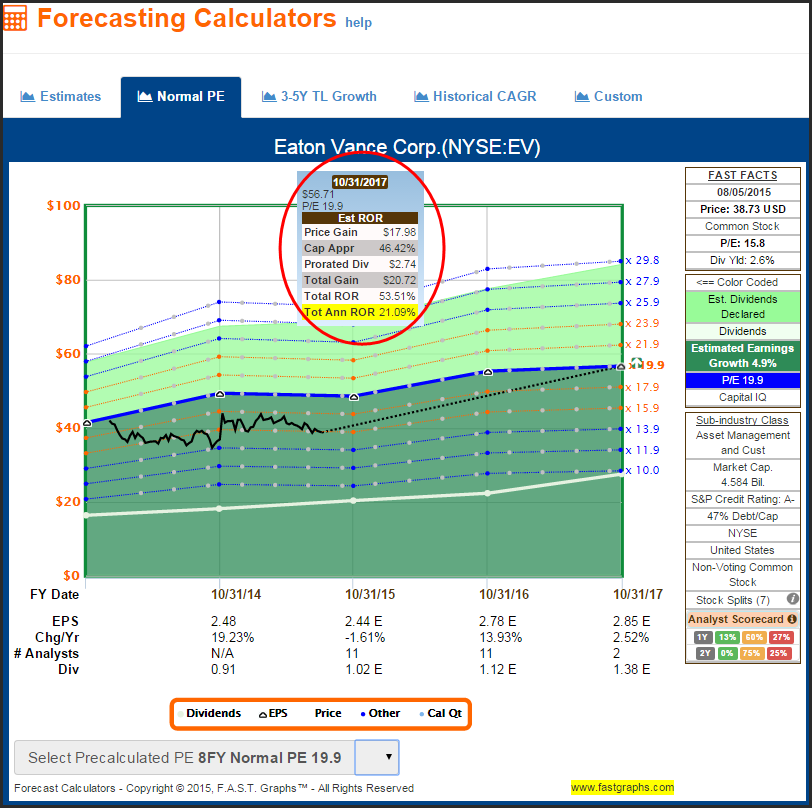

What attracted me to Eaton Vance besides its reasonable valuation was the opportunity for future P/E expansion if the market again applies the normal premium P/E ratio of 19.9. If that were to occur and analysts’ forecasts are correct, this research candidate provides the opportunity for total annual returns in excess of 21% out to fiscal year-end October 2017.

Analysts have been approximately 75% accurate with their 1 year and 2 year forward forecasts.

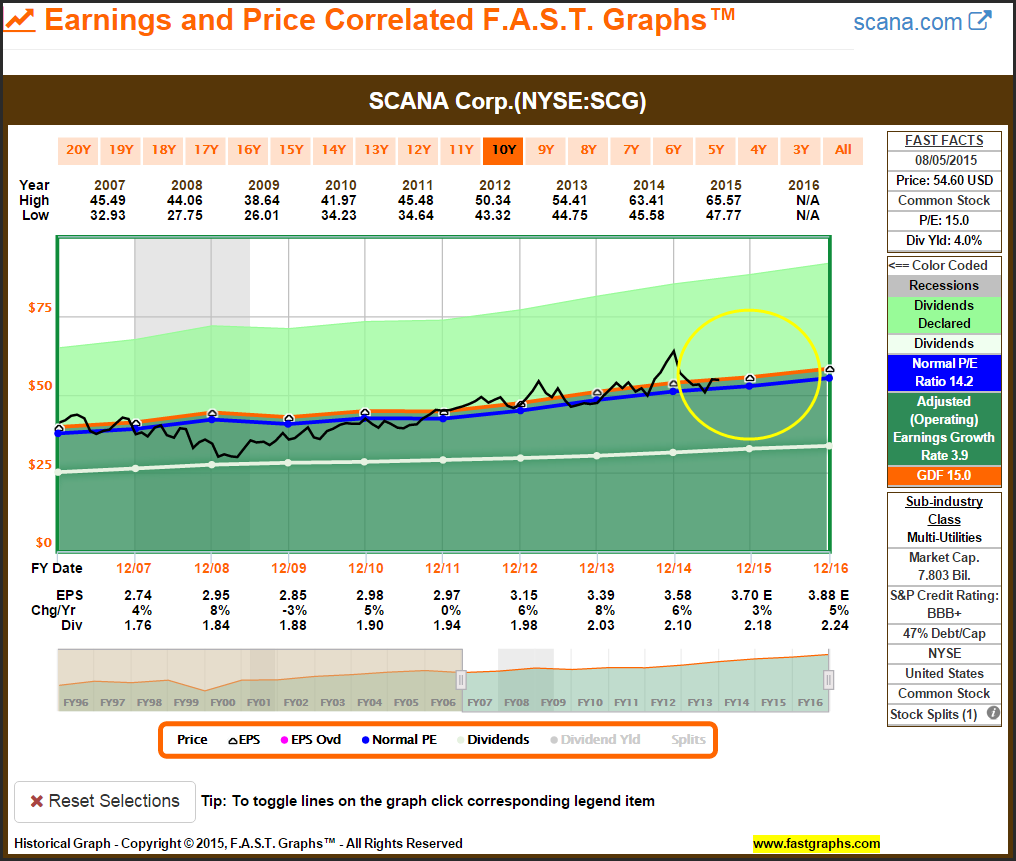

The primary attraction for including SCANA was its current dividend yield of 4%, coupled with its fairly valued blended P/E ratio of 15. Utility stocks are typically low-growth high-yield investments, and SCANA is no exception. Coming in to 2015, most utilities were trading at premium valuations. However, several utilities, including SCANA, have subsequently moved back to attractive valuation.

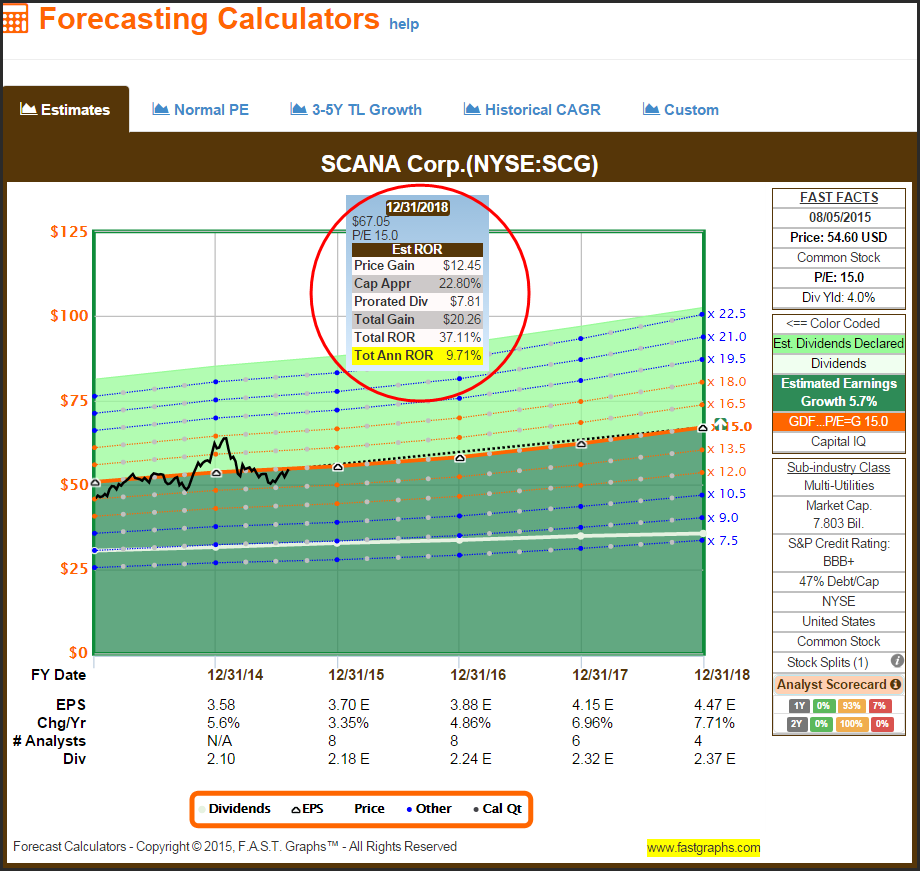

Above-average current yield and expectations for above-average earnings growth out to fiscal year-end 2018 makes slow-growing high-yielding SCANA an intriguing dividend growth stock opportunity. However, even if earnings growth only comes in at its typical 3% range, SCANA’s dividend makes it attractive in today’s low interest rate environment.

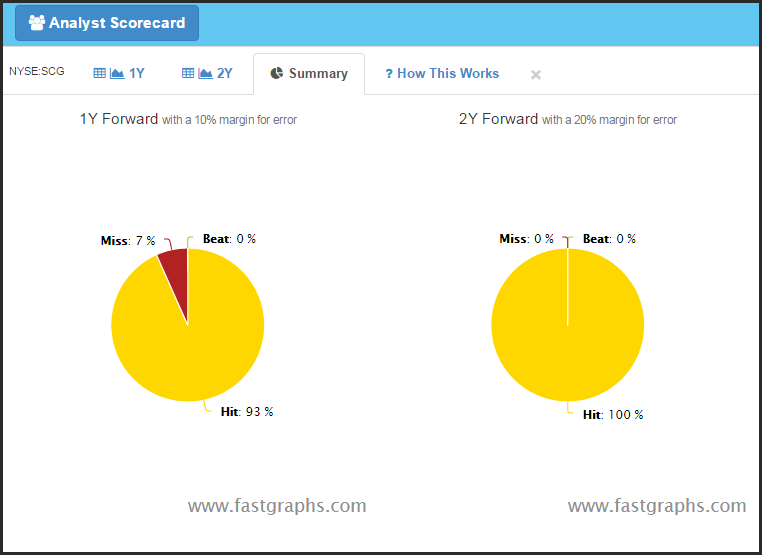

Analysts have been very accurate forecasting SCANA’s earnings in the past.

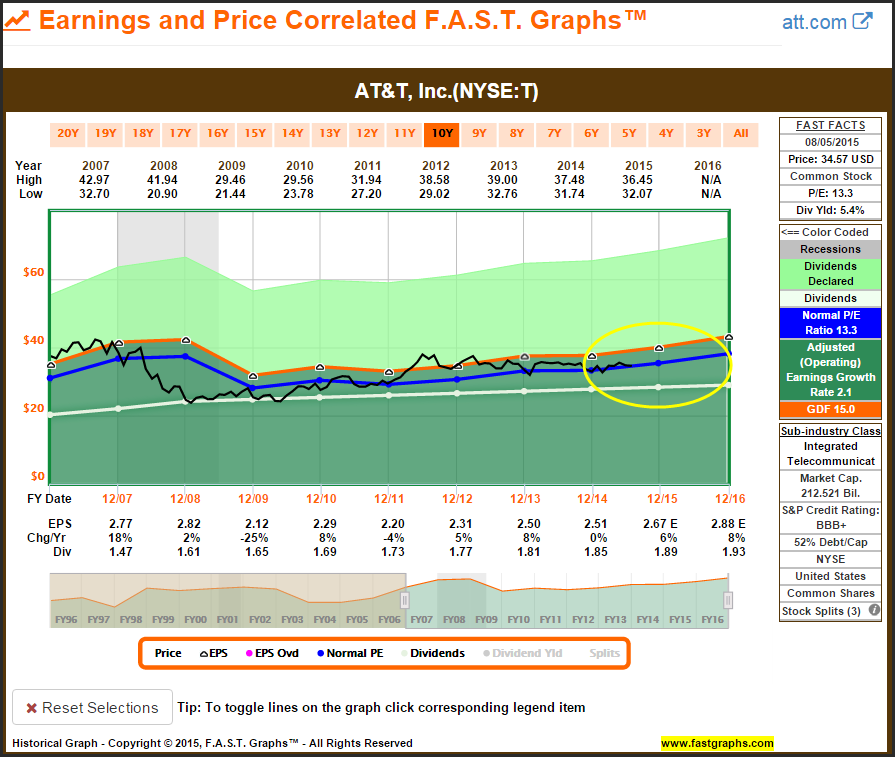

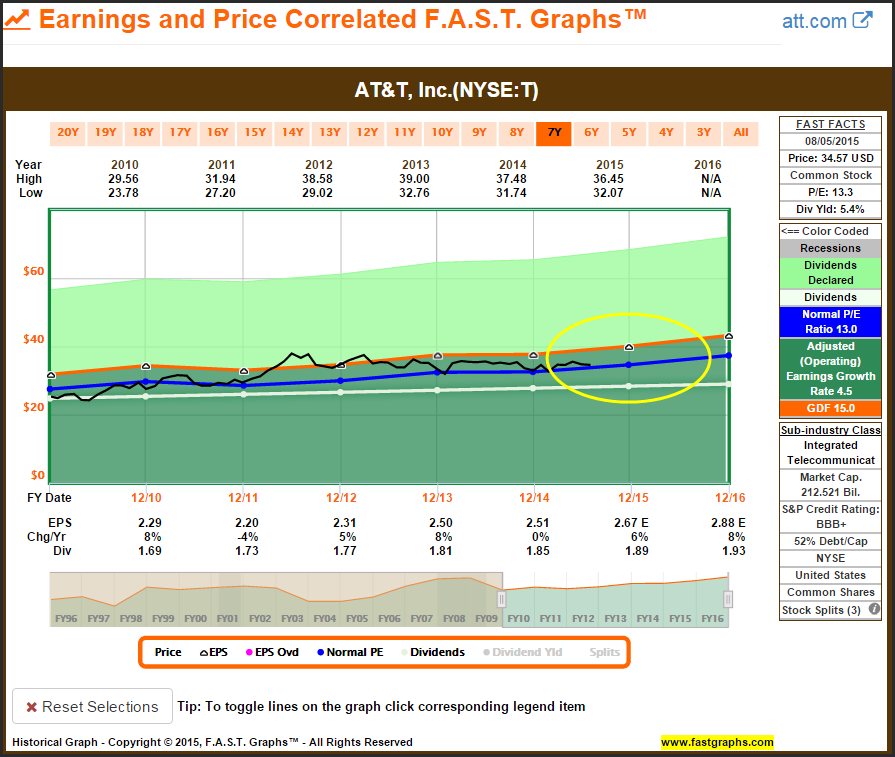

AT&T, Inc. (T)

AT&T is presented for its high yield and low valuation. Although the historical price and earnings correlated graph indicates earnings growth of only 2%, I don’t believe it tells an accurate picture.

If you review AT&T since fiscal year 2010, you discover that growth has averaged 4.5%. This rate of earnings growth is consistent with many large-cap blue-chip dividend stocks such as PepsiCo or Procter & Gamble. However, the big differentiator for AT&T is its high current yield.

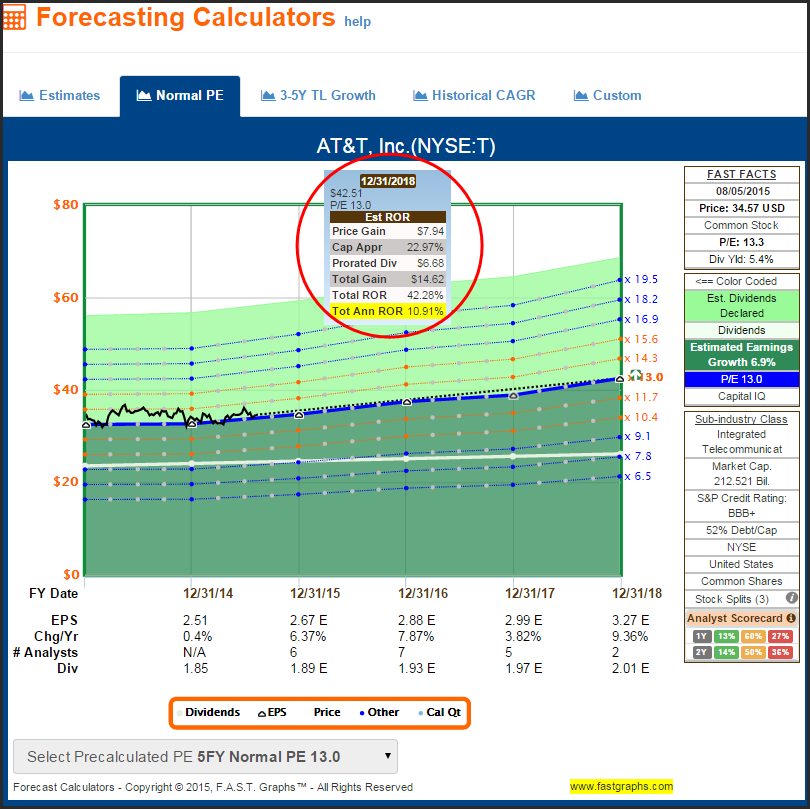

Analysts are currently forecasting AT&T to grow earnings at the rate of 6.9% per annum out to 2018. In order to be conservative with my calculation, I assume that AT&T would still trade at its current P/E ratio of 13. Even with this more conservative valuation estimate, AT&T offers the potential for double digit annual returns approaching 11% per annum.

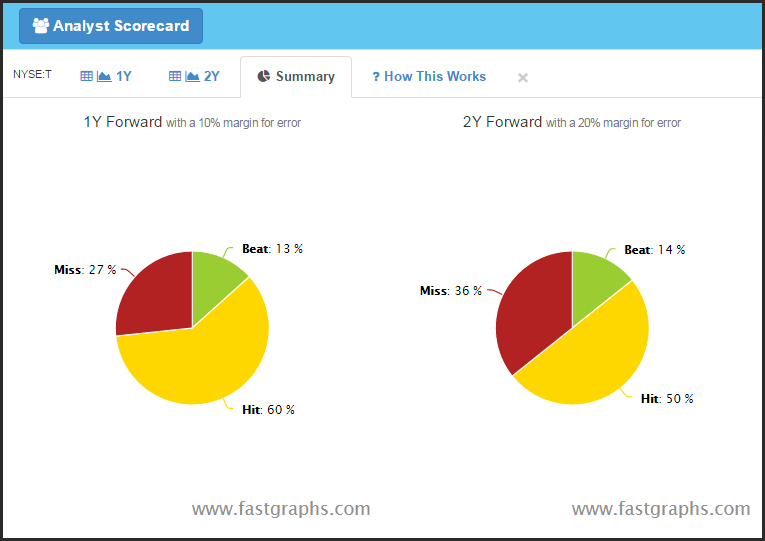

The analysts’ record for forecasting AT&T’s earnings 1 year and 2 years forward is solid, but not exceptional.

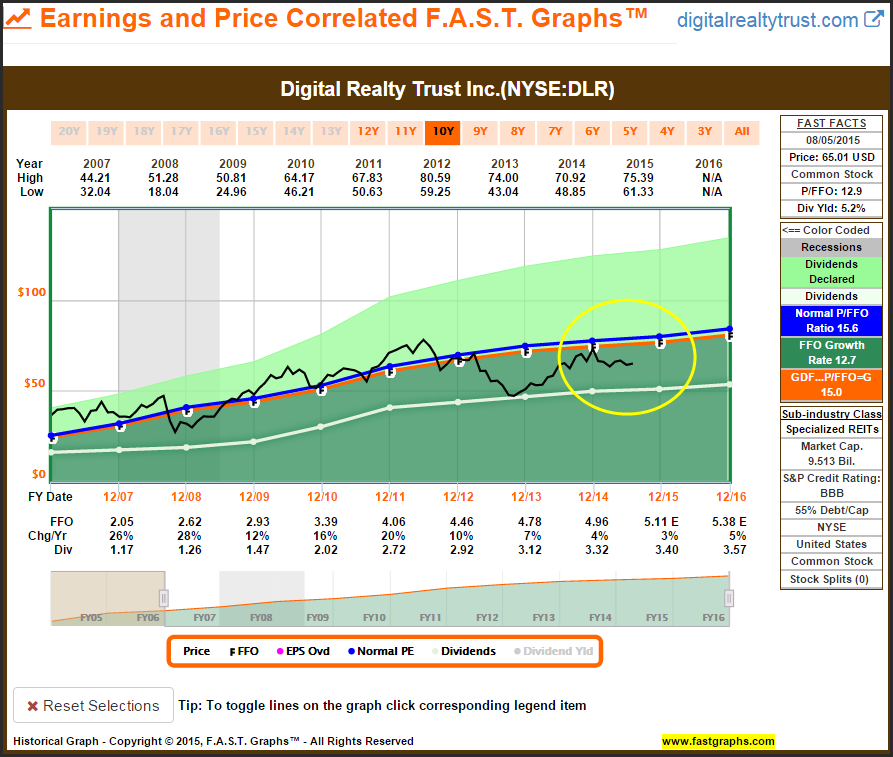

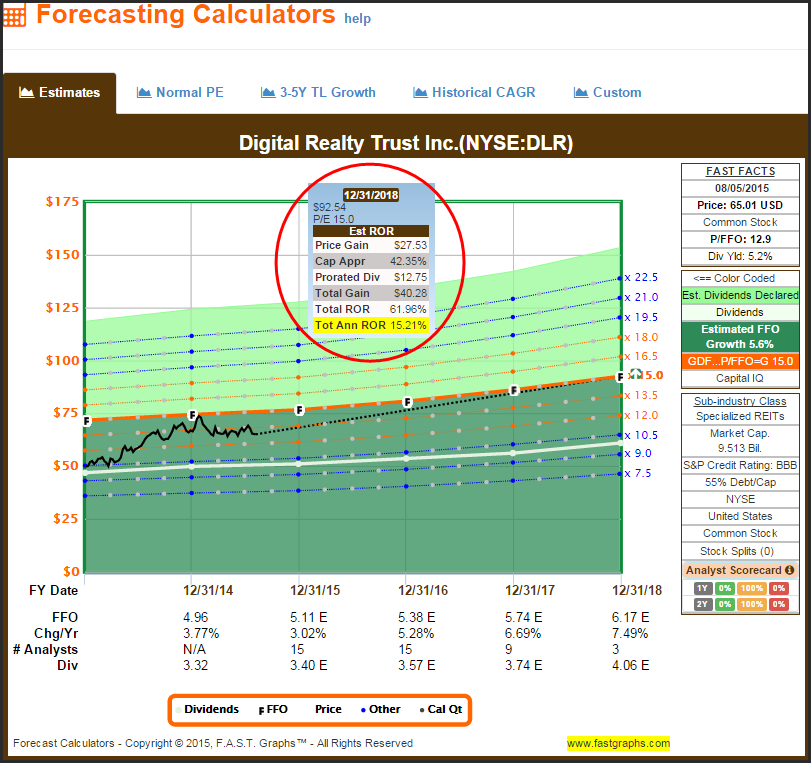

Digital Realty trust Inc. (DLR)

Digital Realty is a specialized REIT that is currently trading at an attractive valuation based on FFO and offers a current dividend yield of 5.2%. Recently there has been a lot of talk about the threat of rising interest rates on REITs. There have also been those who have pointed out that those fears are overblown. Regardless of your position on the effect of interest rates on REITs, I believe that risk is already priced into Digital Realty’s stock.

Low valuation, high yield and an estimated earnings growth rate of 5.6% out to fiscal year-end 2018 suggests the opportunity for a total annual rate of return in excess of 15% for Digital Realty. In today’s low interest rate environment, I consider this high-quality high-yield REIT very attractive at current levels.

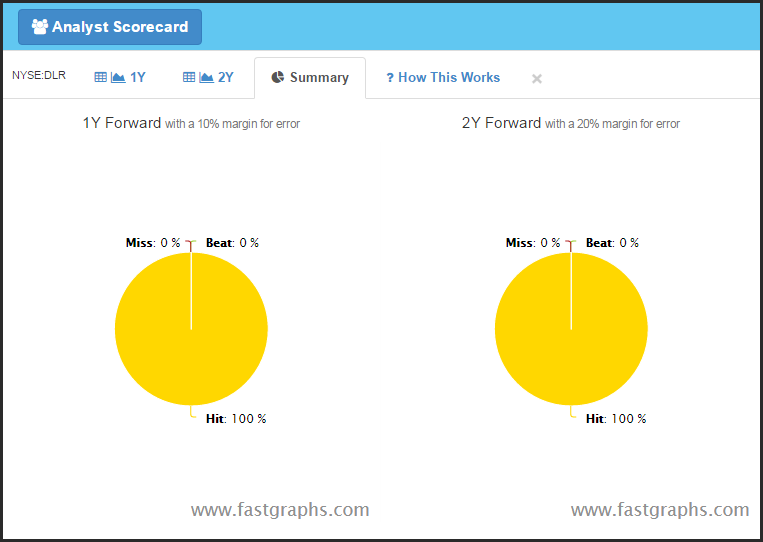

Analysts have been virtually perfect when forecasting Digital Realty’s 1 year and 2 year forward earnings.

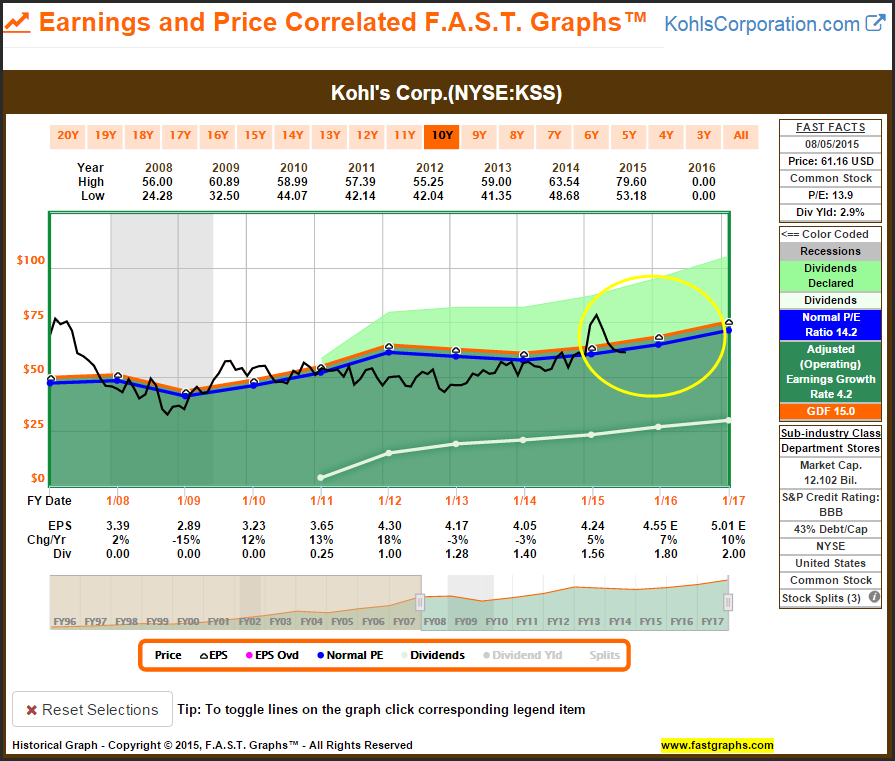

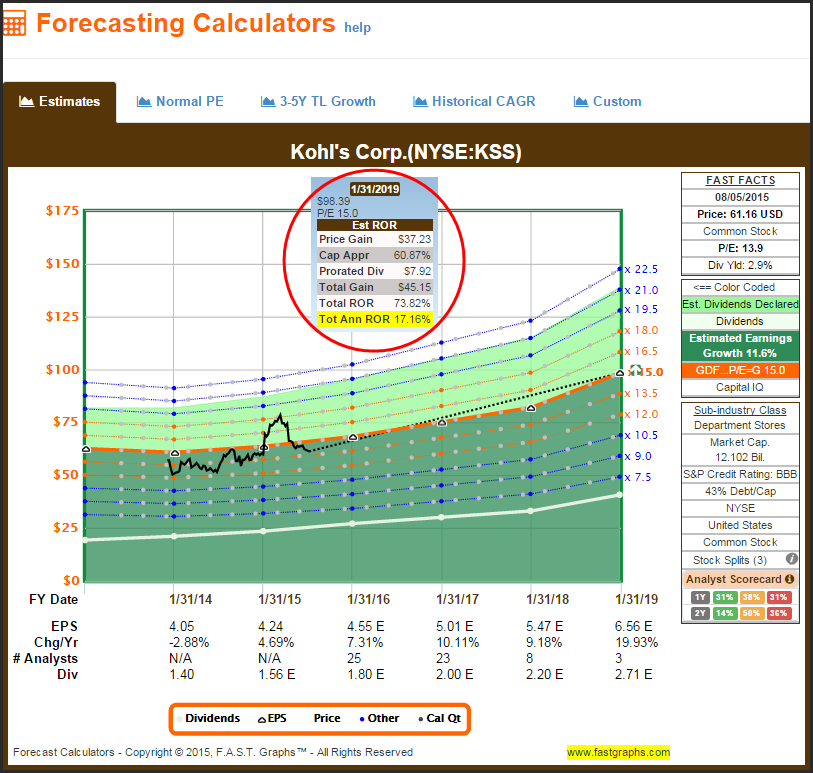

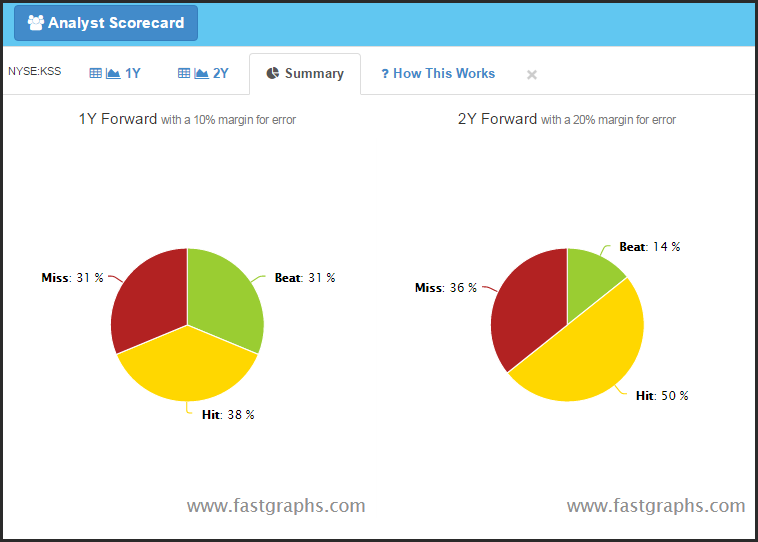

Kohl’s Corp. (KSS)

Although Kohl’s is a relative newcomer to the dividend growth category, it does offer an attractive current yield and a low current valuation. Additionally, this moderately priced retailer has proven to be relatively recession-resistant.

Analysts following Kohl’s are very optimistic regarding earnings growth out to fiscal year-end January 2019. If these analysts are correct and the company only trades at a market-neutral P/E ratio of 15, the total annualized rate of return exceeding 17% per annum is very attractive.

The analysts’ record of forecasting Kohl’s 1 year forward and 2 year forward earnings has been good, but far from perfect.

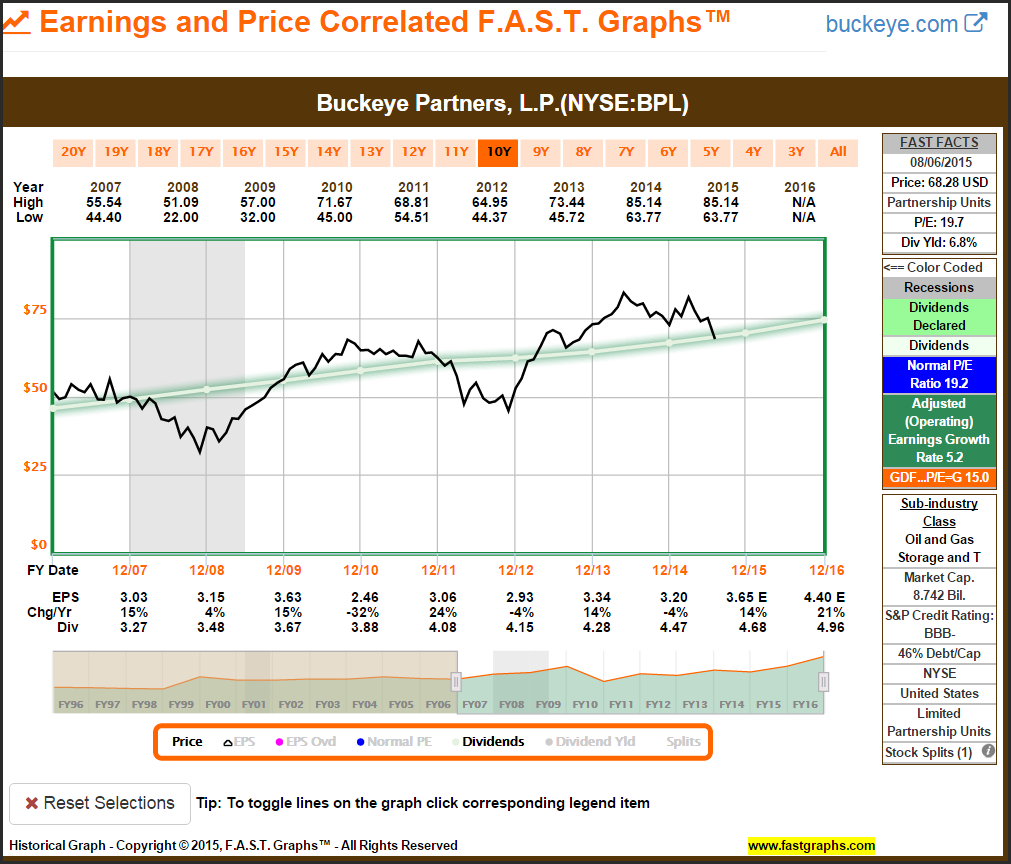

Buckeye Partners, LP (BPL)

Buckeye Partners is a midstream MLP that I consider attractive based on its current high dividend yield of 6.8%. Since the attraction to midstream MLPs is primarily for their high yield, I like to assess fair valuation based on price in relation to their dividend. As the graph below depicts, there is a high correlation between Buckeye Partners’ price and its dividend since 2007. This relationship clearly reveals periods of fair value, overvalue and undervalue. On this basis, I currently consider Buckeye Partners fairly valued. Since I prefer valuing MLPs based on dividends, I did not include a forecasting calculator or analyst scorecard on this research candidate.

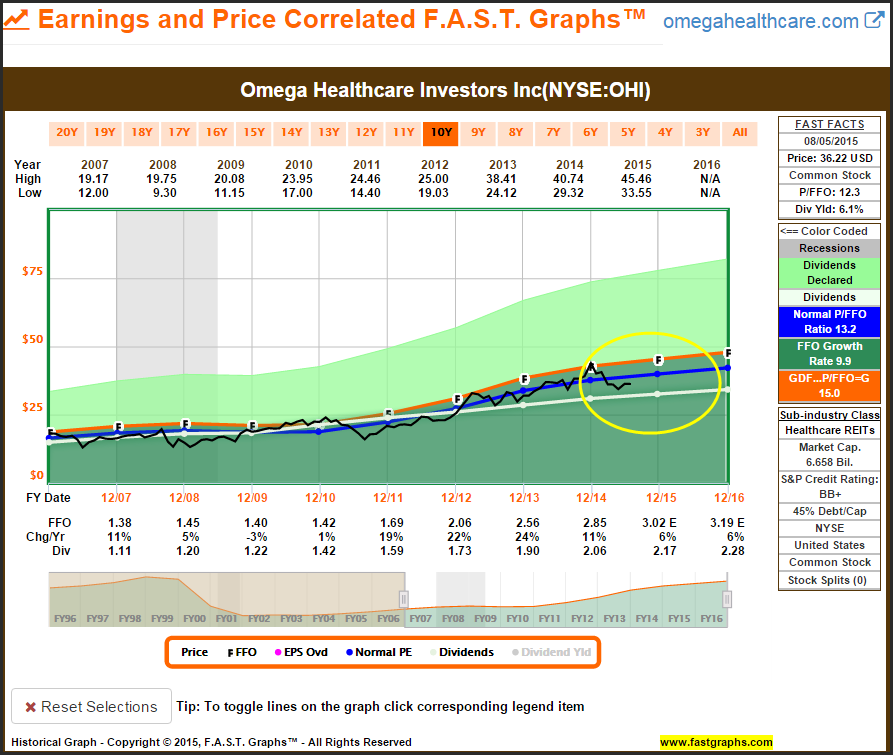

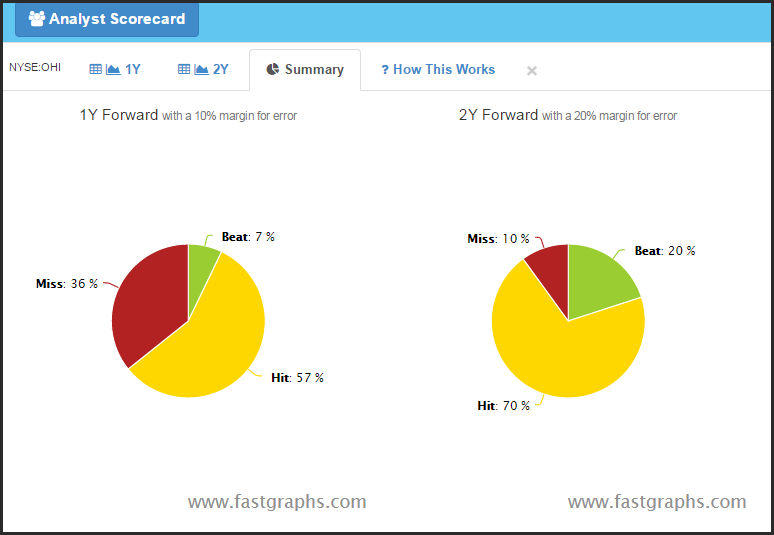

Omega Healthcare Investors Inc. (OHI)

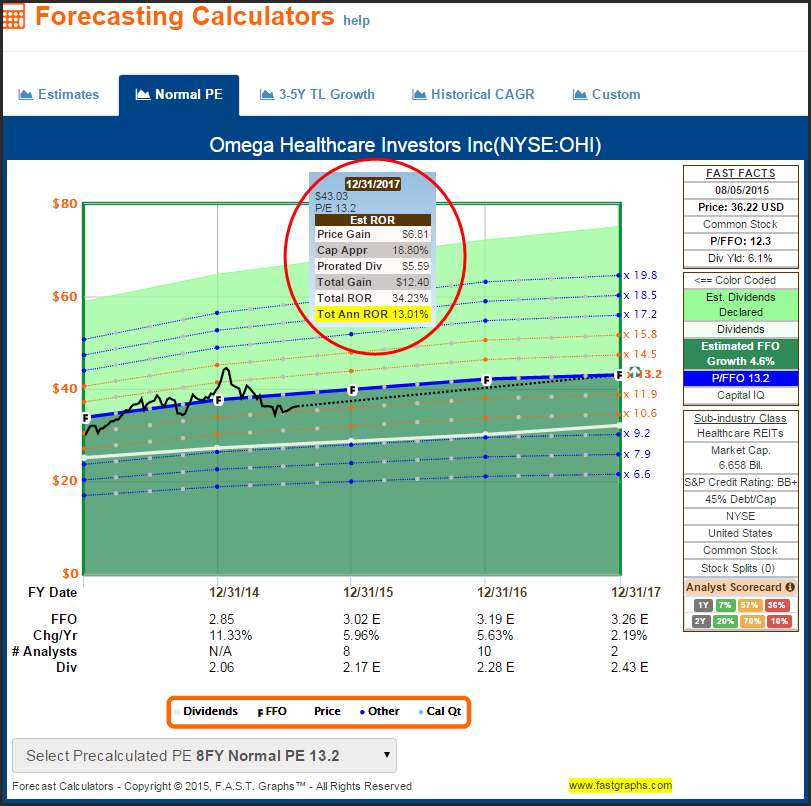

Omega Healthcare is attractively valued at a P/FFO of 12.3 and a dividend yield of 6.1%. I believe that demographics support strong future business prospects for Omega Healthcare going forward.

If analysts are correct with their forecasts and Omega Healthcare trades at its normal P/FFO of 13.2, shareholders could receive a total annual rate of return in excess of 13%. Thanks to its high yield and historical record of dividend growth, dividends would provide almost half of that total expected rate of return.

Analysts’ record of forecasting forward earnings 2 years out for Omega have been very high. However, when forecasting 1 year forward, the analysts’ record has not been as good.

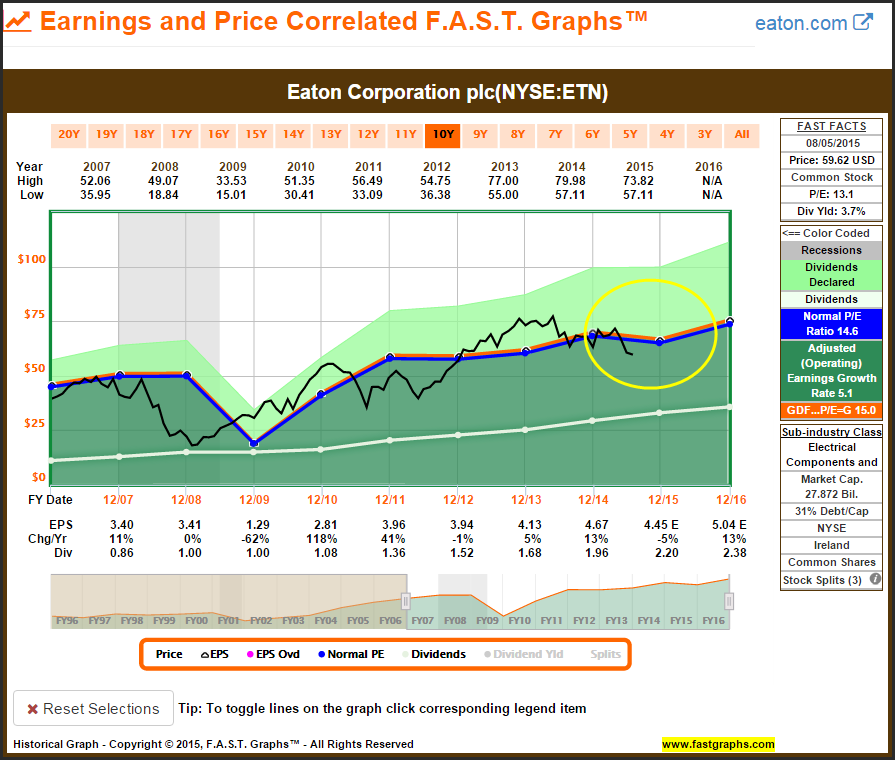

Eaton Corporation plc (ETN)

Although Eaton Corporation is only a Dividend Challenger that has increased its dividend for 6 consecutive years, this can give a false impression of its dividend record. Since 1997 the company has never cut their dividend, but did freeze it for the period 1999 to 2001, and again in 2009. Notwithstanding those dividend freezes, the company’s average dividend growth rate and compound average dividend growth rate have both exceeded 9% since 1997.

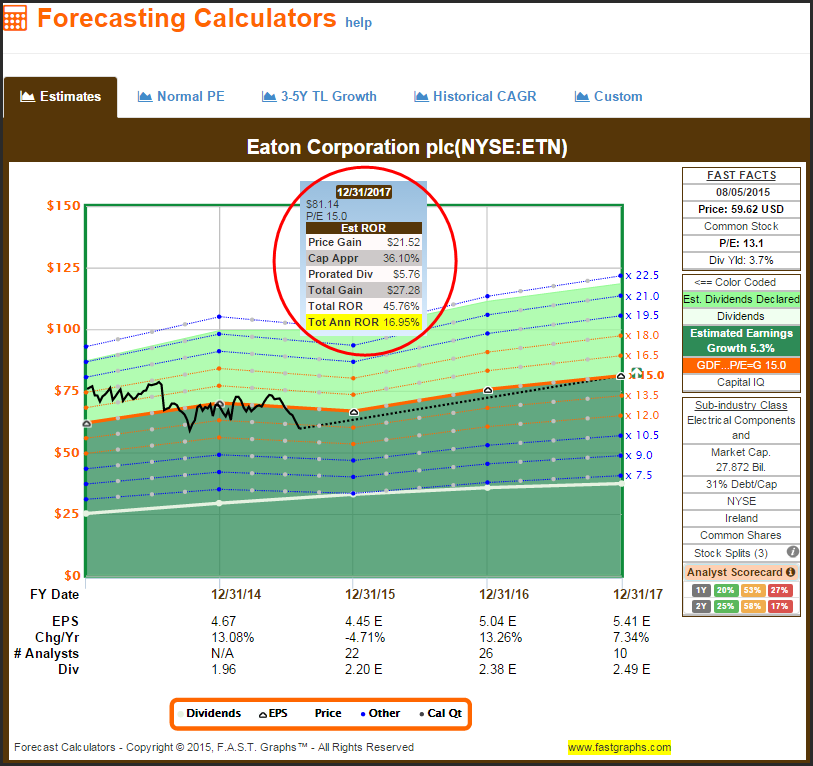

If analysts are correct with their forecasts out to fiscal year-end 2017, investors purchasing Eaton today have the potential to receive a total annual return of almost 17%. Therefore, I consider Irish-based Eaton Corporation an attractive dividend growth stock with a current yield of 3.7% and a low debt-to-capital ratio of only 31%.

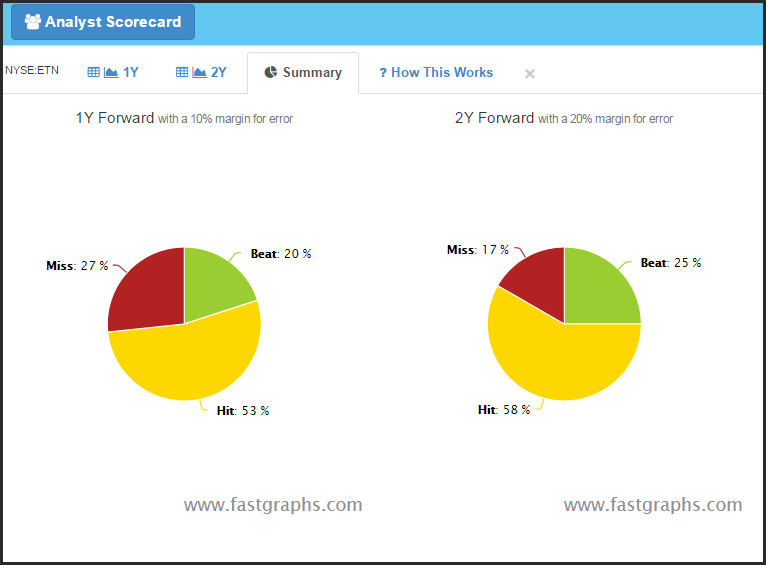

Analysts have been accurate with their forecasts on Eaton Corporation approximately 75% of the time for both 1 year and 2 year forward forecasts.

Summary and Conclusions

I readily acknowledge that it is currently very difficult to find good value in today’s extended stock market as I illustrated with the S&P 500 graph in part 1 of this 2-part series. However, I also acknowledge that it is virtually impossible to time the market. Therefore, I have long favored basing investment decisions on a carefully researched assessment of sound fundamental value. Stock prices can, and often do, fall from fair valuation levels. On the other hand, as long as fundamentals stay intact they will eventually, and I believe inevitably, recover.

For the retired investor utilizing high-quality dividend growth stocks in their portfolios, the dividend record is less volatile, more reliable and predictable. Consequently, for the investor in need of income, time in the market becomes significantly more important and relevant than attempting to time the market. Stock price volatility is a reality of the market, and as such, unavoidable. However, it can be rationally dealt with when the investor focuses on dividends and fundamentals.

The 20 research candidates presented in this two-part series are companies that I believe are attractive today. That is not to say that they will all immediately do well price-action-wise in the short run. However, I do believe that the vast majority will produce a reliable growing income stream into the foreseeable future. Therefore, over the longer run, I think a portfolio comprised of these 20 research candidates should provide the above-average and growing income stream that many retired investors are looking for. Finally, if any or all of them are utilized, I strongly suggest continuous due diligence and monitoring with a primary focus on fundamentals and the dividends.

Disclosure: Long EMR,PEP,T,SCG,KSS,OHI,ETN at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.