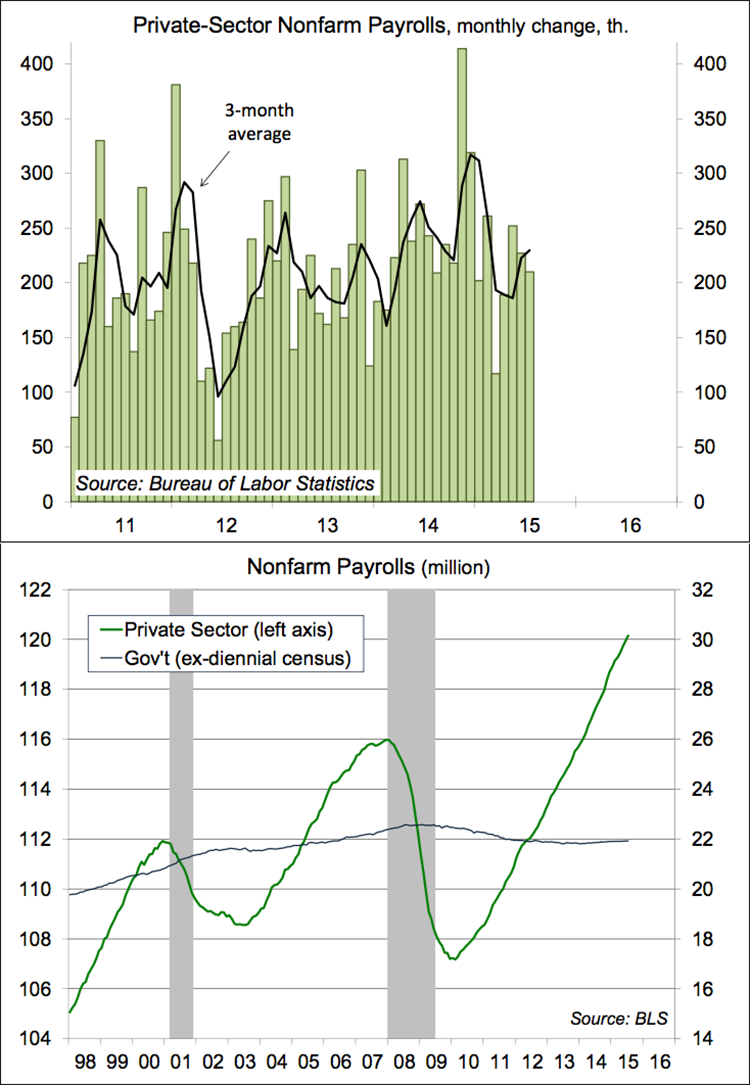

Job growth remained strong in July. The average monthly gain for May, June, and July was 235,000, or 2.82 million at an annual rate. To remain in line with population growth, we need to add about 1.4 million jobs per year. Slack in the job market is being reduced, but a considerable amount remains. How much? The Fed has to consider the pace and plan ahead.

Nonfarm payrolls rose roughly in line with expectations in July, accounting for a small upward revision to the two previous months. There is a fair amount of statistical noise in the monthly payroll figure (a 90% confidence interval is ±105,000). Figures are often revised. In February, the Bureau of Labor Statistics added the three-month average increases in total payrolls and private-sector payrolls to the highlighted tables at the beginning of the report. These aren’t difficult calculations. Rather, the BLS sought to emphasize the recent trend. The three-month average is less volatile than the individual months (noise in one month often washes out in subsequent data).

The three-month averages really haven’t caught on among financial market participants. We still see oversized reactions to surprises in the monthly numbers. That wasn’t the case in July, as the headline figure was close to the median forecast.

The Federal Reserve has two goals: price stability (interpreted as a 2% annual rate in the PCE Price Index) and maximum sustainable employment. Traditionally, the employment goal is taken as a target unemployment rate. However, the unemployment rate has been distorted by the decline in labor force participation. The employment/population ratio is seen as a better measure of labor utilization, but here’s the puzzle. While growth in nonfarm payrolls has been strong, the employment/population ratio has barely budged over the last year (in fact, unchanged over the last six months).

We lost almost 8.7 million private-sector jobs during the downturn and have added more than 12.8 million jobs in the recovery. That leaves payrolls up by 4.2 million versus the pre-recession peak. However, we ought to have added about 9.8 million if not for the recession. That leaves us over 5 million jobs behind (these calculations are rough, the shortfall may be a lot less than that). At the current pace of job growth, much of that slack will be taken up over the next couple of years.

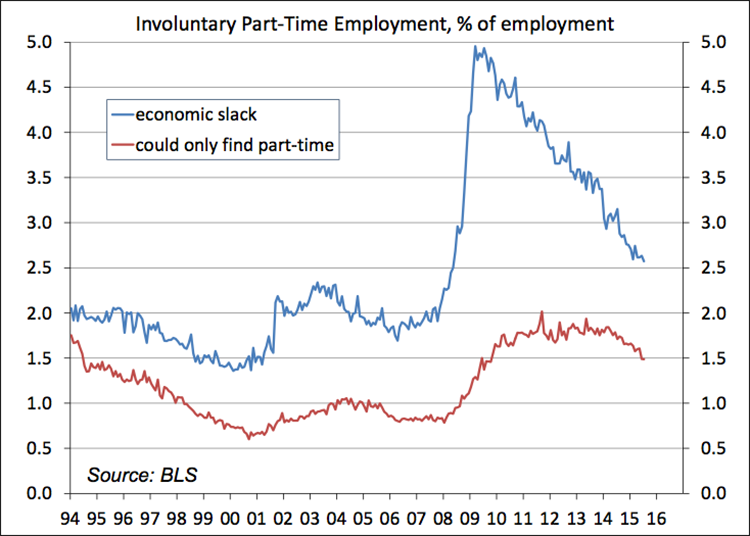

The percentage of involuntary part-time workers is trending lower. Most of the decline reflects improving economic conditions. Some firms have restricted hours as a strategy to limit labor costs or to avoid an impact from the Affordable Care Act. However, the ACA was supposed to be an issue only for firms with around 50 employees. The fear was likely worse than the reality. With the law in place, the percentage working part-time because that was the only thing offered has declined.

The data suggest a path of further reduction in labor market slack, with normal job conditions likely to be reached in 2017. That’s consistent with a very gradual Fed rate hike path.