“Twenty years from now you will be more disappointed by the things that you didn’t do than by the ones you did do, so throw off the bowlines, sail away from safe harbor, catch the trade winds in your sails. Explore, Dream, Discover.”

–Mark Twain

A question came in from an advisor client wanting to know what I think about the record high level of margin debt. Margin debt is clearly a good thing on the way up and it can be hazardous in down markets when margin calls kick in. Forced selling can be a painful reality when a long-term bull market ends. My answer is that while margin debt is at an all time high (indicating excessive speculation), it is currently more supportive to the market than not.

What is interesting, at least to me anyway, is the amount of data available to help us better identify points of inflection. We don’t want to be in front of a tidal wave of forced margin call selling especially when margin debt is excessively high (today such debt is higher than it was in 2000 and 2007). I share a few charts with you below that I believe may help us better ride the wave and avoid its eventual crash.

Additionally, let’s take a look at July month-end market valuations and see what they may be telling about probable forward 10-year returns. Grab a coffee and jump in.

Included in this week’s On My Radar:

- Margin Debt

- Current Valuations

- Trade Signals – Volume Demand is Greater than Volume Supply (New Buy Signal) – 08-5-2015

Margin Debt

Following are a series of charts. The first looks at the total amount of margin debt in billions. Note in the bottom section the amount of margin debt is nearly twice as much as it was in early 2000 and much higher than it was at the prior peak in late 2007. The red line plots the amount of margin debt over time.

What I like about this chart is that it also plots a six-month smoothing line (dotted green line) and shows the performance of the Dow Jones Industrial Average from 1965 to present when the total margin debt is above its six-month smoothing (red line above green line).

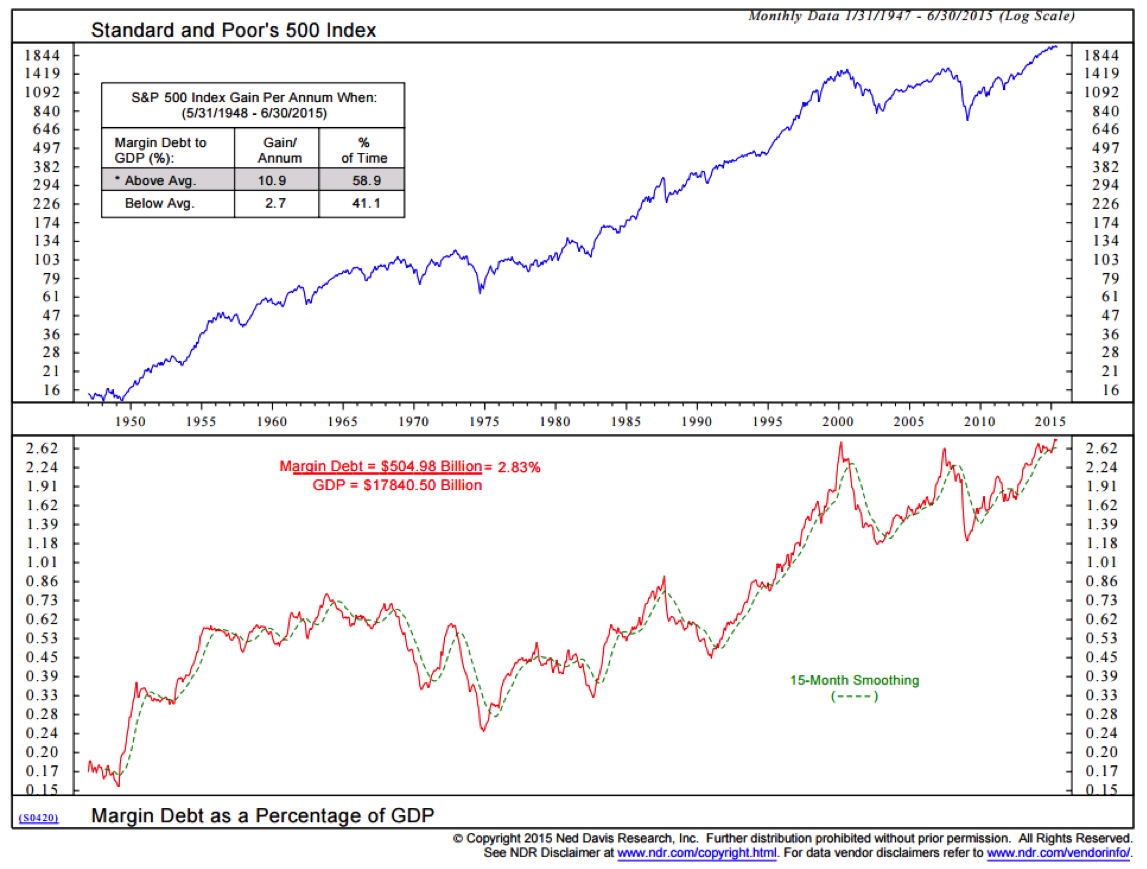

The next chart looks at Margin Debt as a percentage of GDP. Here it is just slightly higher than the peaks in 2000 and 2007. Also plotted is a 15-month smoothing that shows it is better to be in the market when margin debt is above its trend line. This is the case about 58.9% of the time, since 1948.

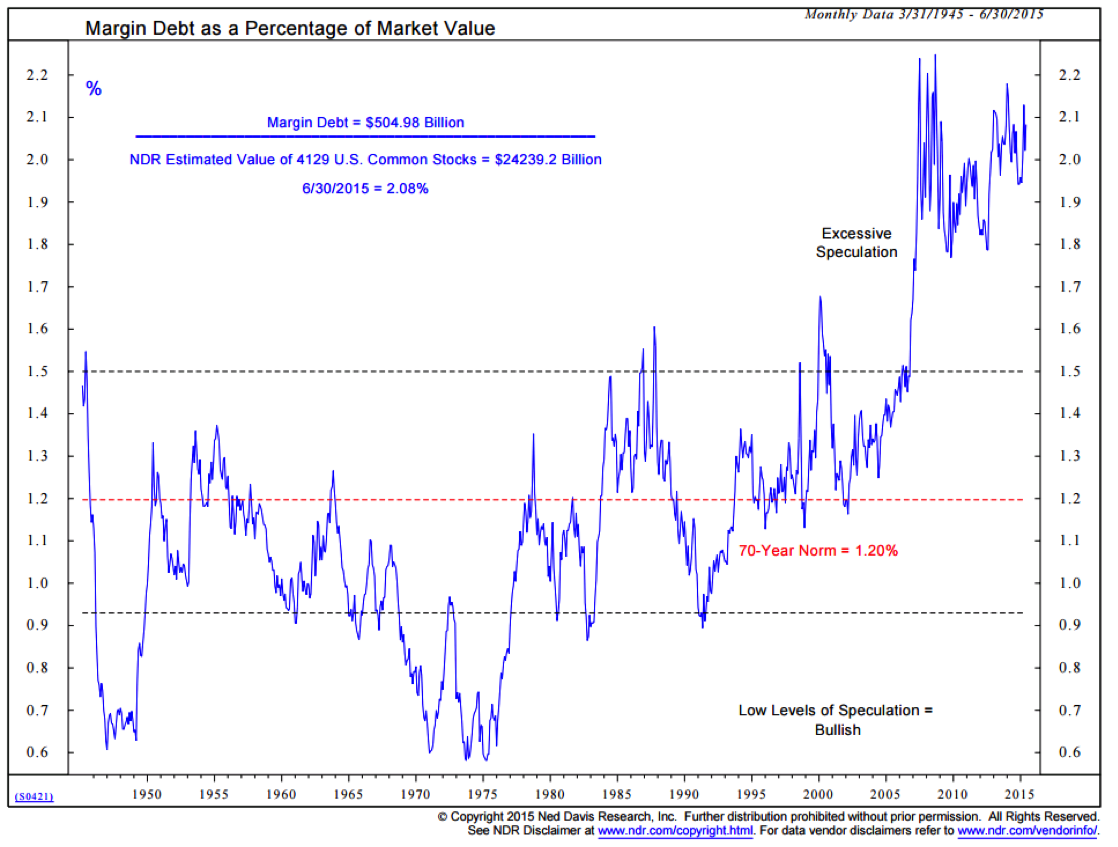

The next chart looks at margin debt as a percentage of market value. Note how low margin debt was in the late 1940s and again after the 1974/75 market crash. Also take a look at the 2000 high and where we are today relative to 2007.

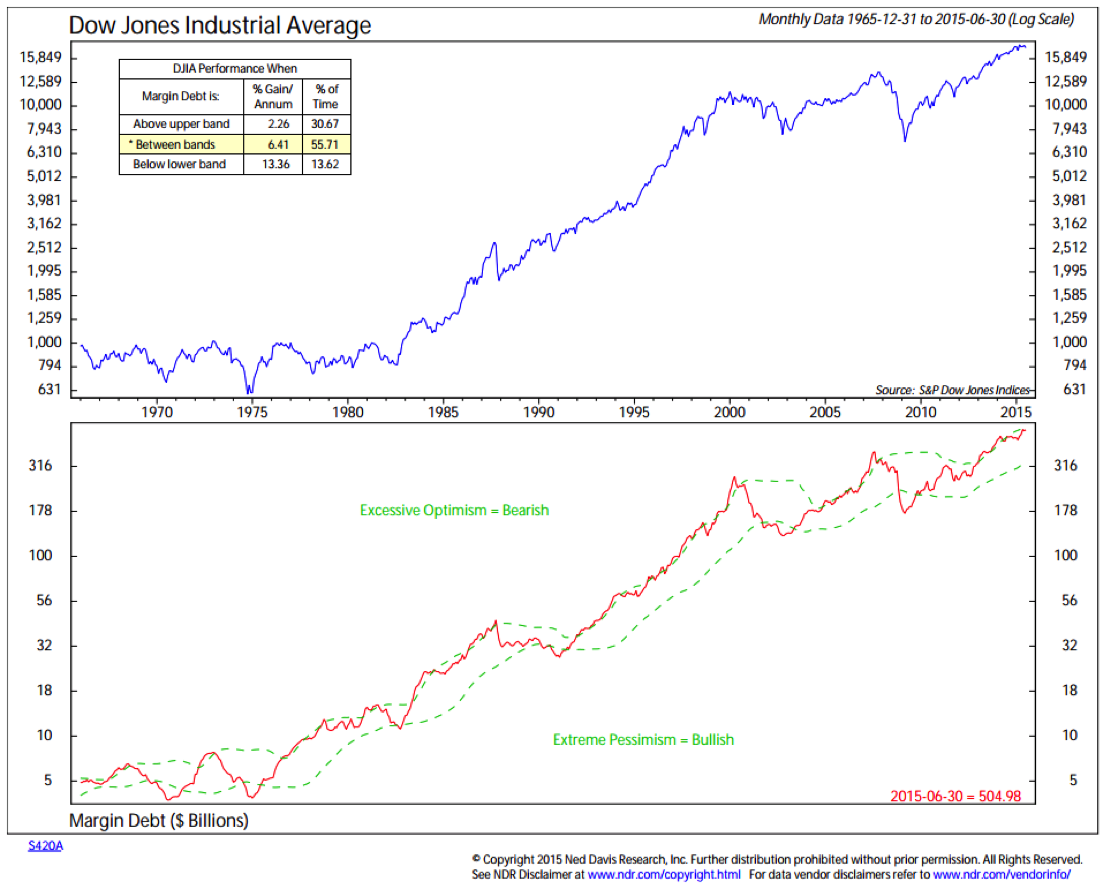

Finally, as it relates to margin debt, I came across this next chart when researching through the NDR site. The bottom section sets two bands: above the upper band (green dotted line) reflects periods of excessive speculation, below the lower band reflects periods of excessive pessimism and between the bands is neutral. The returns for the market is reflected in the upper left had section of the chart. The yellow highlight shows us where we are today and the DJIA’s historical returns when “between bands” (based in this measure).

In sum, the high level of margin debt is concerning but not yet a problem. Let’s keep a watch for a change in trend.

Valuations

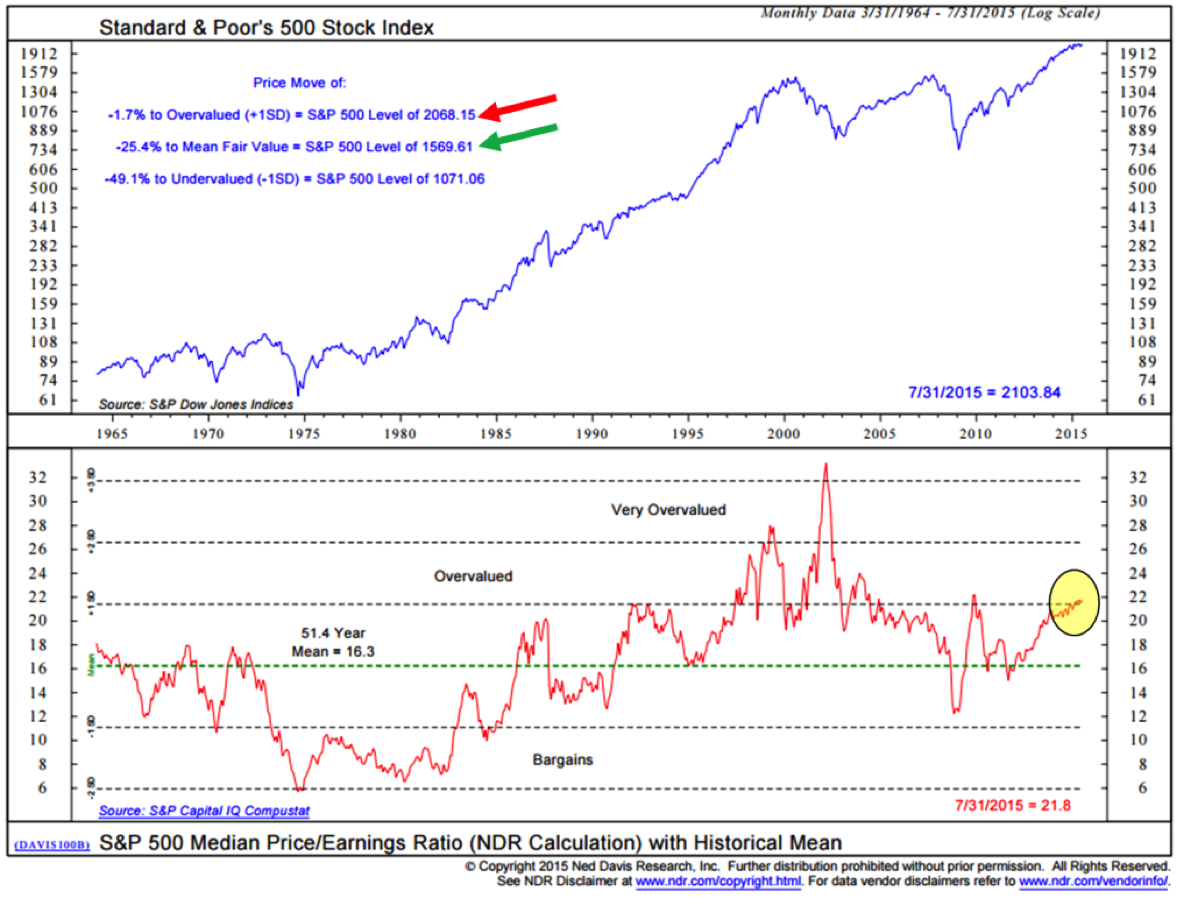

The market has been treading water and perhaps a good part of that struggle is the current level of high valuation. So let’s take a look at a few different valuation measures and start with my favorite (Median PE). Valuation can tell us a great deal about what 10-year forward returns might be. Buy low, sell high as they say.

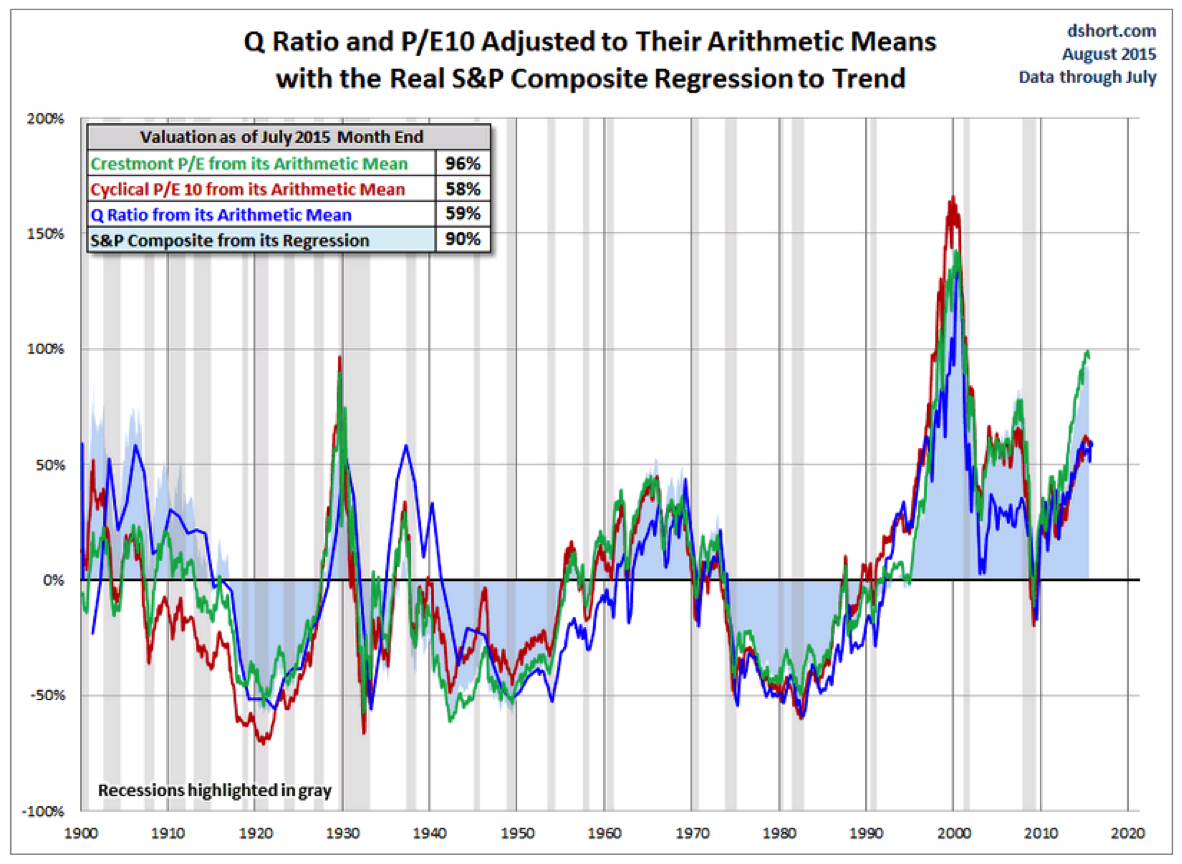

The yellow circle highlights the July 31, 2015 PE of 21.8 putting the market (by this form of PE measurement) at an “Overvalued” level. The green arrow shows the market to be fairly valued at 1569.61 based on a 51.4 year mean. A reasonably good guess in my view.

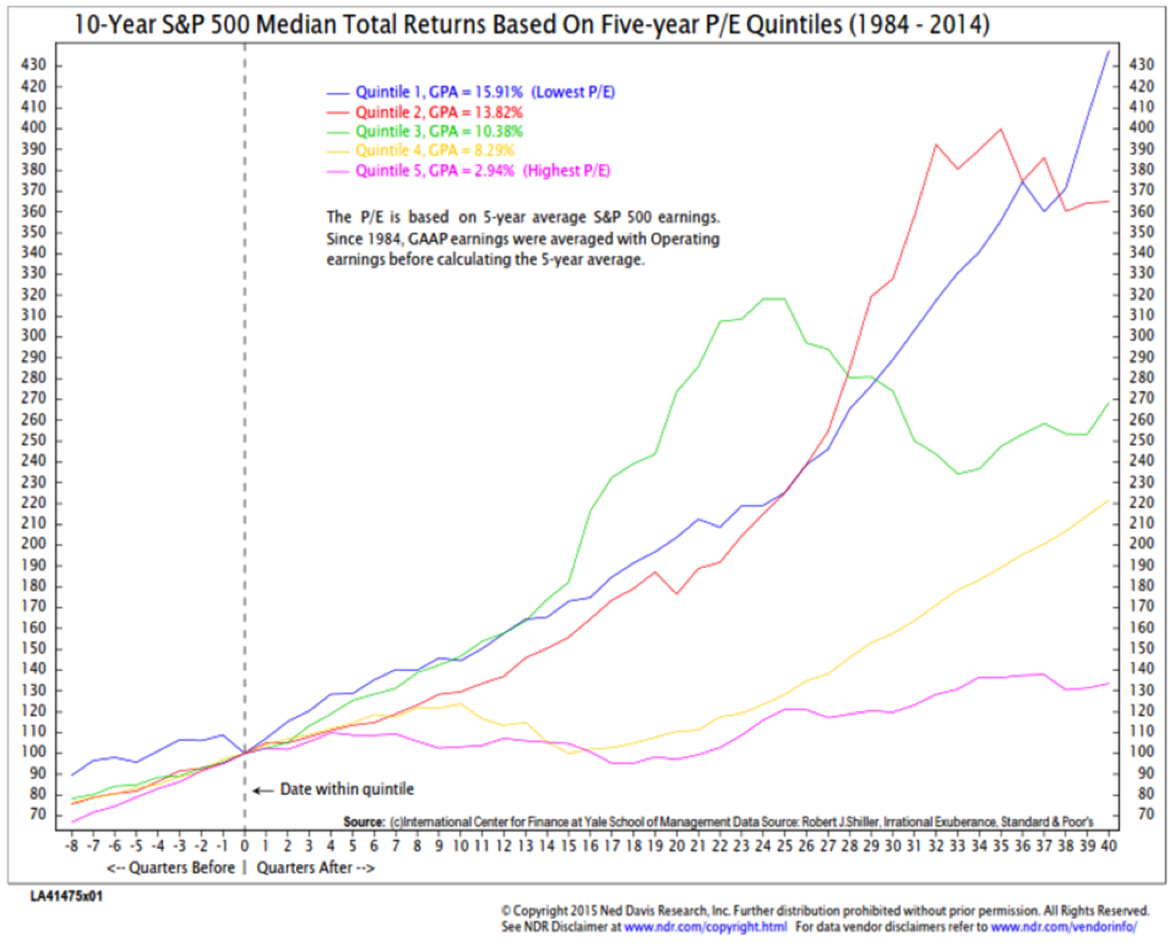

As we’ve shown before, the forward returns are not so good when the market is in an overvalued state. At a median PE of 21.8, the current reading is in the 5thquintile or highest 20% of recorded month-end market median PE valuations. Here is a plot of returns, 1984 through 2014, based on whether PE was low (Quintile 1) or high (Quintile 5) and what happened over the subsequent 10 years.

Clearly it is better to buy when valuations are low (Quintiles 1, 2 and 3). We want to be very careful (and hedge) when in Quintile 5. Note the light purple line in the chart above. We are in Quintile 5 today. This measure is projecting a 10-year forward return of just 2.94%.

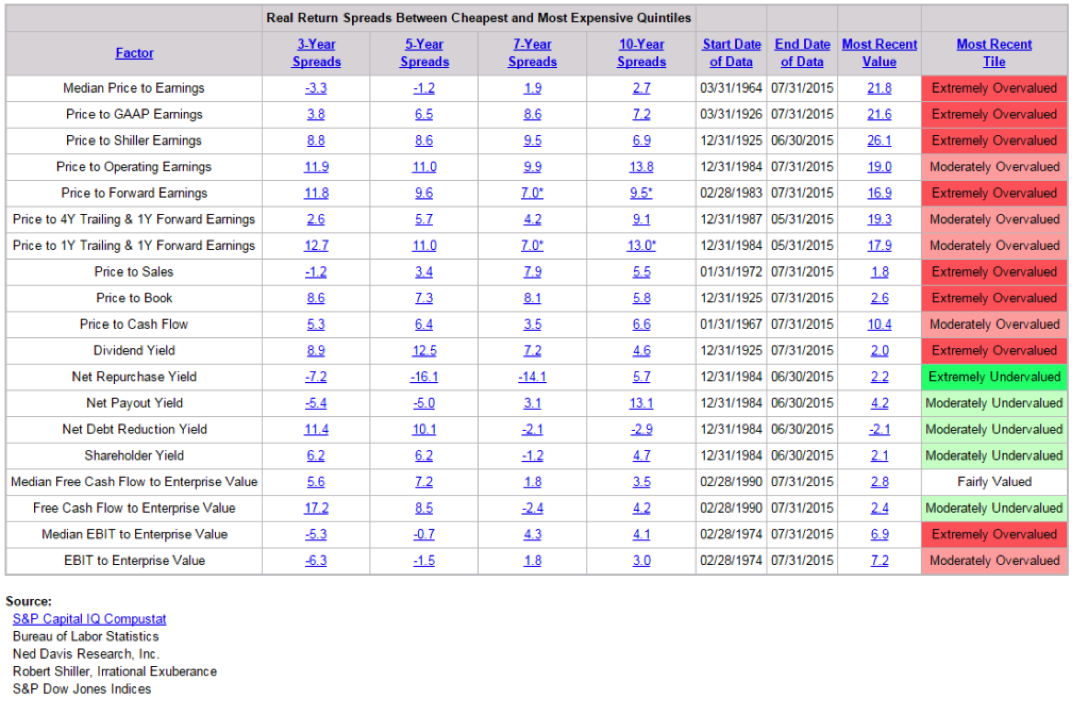

Next is a summary of several popular valuations measures.

On their own, high valuations can grow to become move overvalued. Valuations are a very poor timing tool. However, they are a very good risk level tool and can help us identify periods in time where we should become more conservative. That is why I favor risk management (hedging processes) and other diversifiers when risk is high (like today).

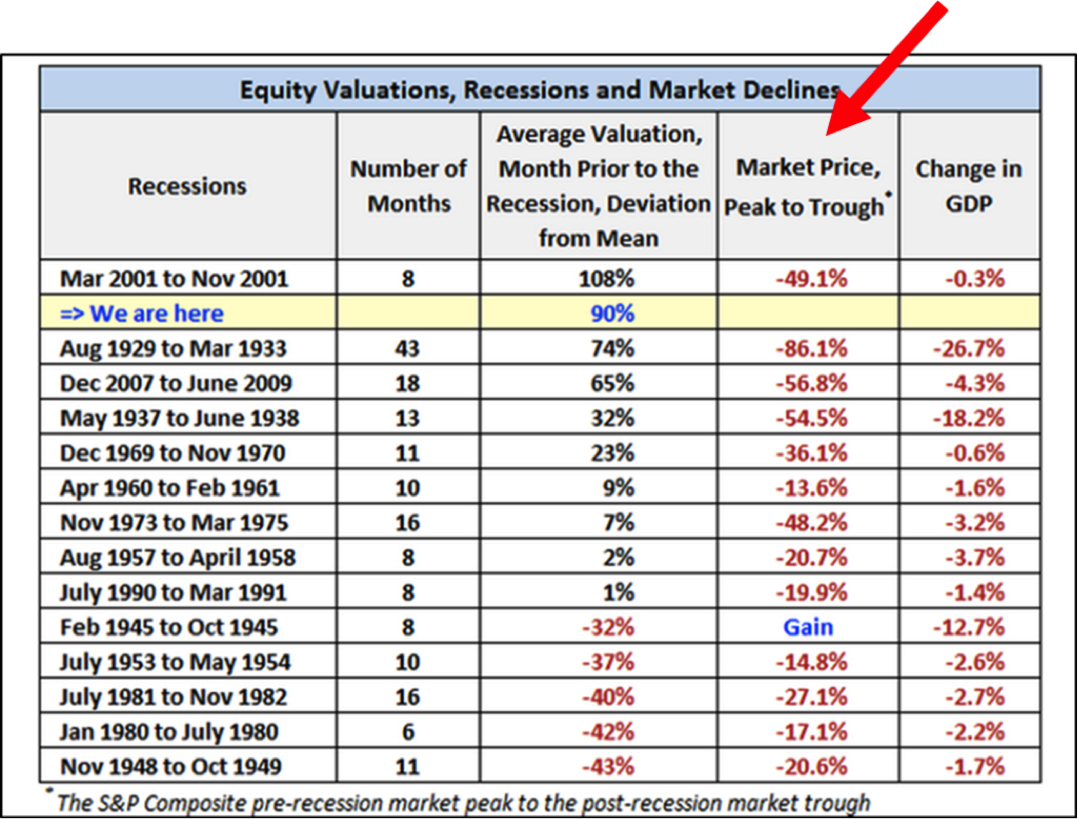

The next chart (red arrow) shows us that the worst market declines have come during recessions and warn us to be most concerned when our beginning point is high. The yellow highlight reflects today’s current overvalued state based on the above data courtesy of Doug Short.

Put your glasses on for this next chart or simply note that the majority of various other valuation indicators are red (extremely overvalued or moderately overvalued). “Warning Will, Warning Will” – I picture that robot from one of my favorite childhood shows, Lost in Space.

The good news is that, while we remain patient for better value, we investors have tools available that allow us to participate and protect (hedge) and broader strategies that enable us to build stronger and more broadly diversified portfolios. Such strategies are called tactical and alternative strategies.

“This is the one thing I can never understand. To refer to a personal taste of mine, I’m going to buy hamburgers the rest of my life. When hamburgers go down in price, we sing the “Hallelujah Chorus” in the Buffett household.

When hamburgers go up, we weep. For most people, it’s the same way with everything in life they will be buying–except stocks. When stocks go down and you can get more for your money, people don’t like them anymore.” Warren Buffett

Like Buffett, we’ll sing the “hallelujah chorus” when the hamburgers go down in price. Right now we should probably weep.

Keep one eye on the trend indicators (Trade Signals) and keep the other on the lookout for a turn down in margin debt.

Trade Signals – Volume Demand is Greater than Volume Supply (New Buy Signal) – 08-5-2015

More buyers than sellers drives price higher. One of the charts I post each week measures volume demand vs. volume supply. The buy and sell signals are posted below. A new buy signal was triggered on July 30, 2015. This, along with favorable trend and sentiment measures, causes me to lean bullish.

Included in this week’s Trade Signals:

- Cyclical Equity Market Trend: The Primary Trend Remains Bullish for Stocks

- Volume Demand is Greater than Volume Supply: Buy Signal for Stocks

- Weekly Investor Sentiment Indicator:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for stocks)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for stocks)

- Don’t Fight the Tape or the Fed: Modestly Bearish – Watch Out for Minus Two

- U.S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Currently signaling No U.S. Recession

- The Zweig Bond Model: The Cyclical Trend for Bonds is Bullish

Click here for the link to all of the charts.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group