Is the United States Insulated from China’s Economic Distress?

The Chinese economic slowdown, following decades of spectacular growth, is more than noticeable now. Also, the world is watching the recent turbulence in Chinese equity markets closely. These developments have triggered many questions. We address the most popular query in our inbox: What are the potential spillovers to the United States from weaker growth in China?

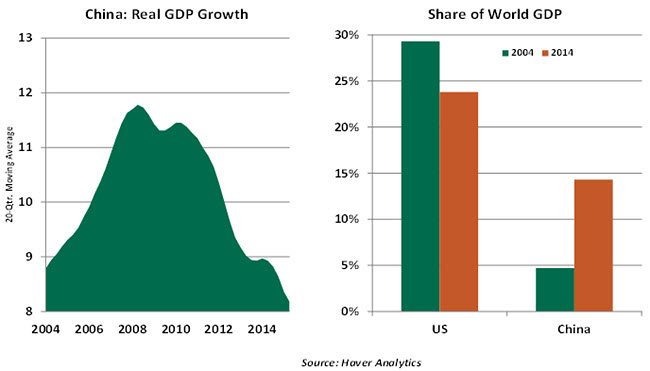

It is widely recognized that underlying economic fundamentals of China are soft and not consistent with the 7.0% increase in real gross domestic product (GDP) reported for the second quarter. China’s stock market performance is not tied to the real economy. Nonetheless, the Chinese authorities have put in place a raft of measures to try to stem the bleeding in the equity market. These confidence-draining events are taking place under unfavorable economic conditions in the world’s second-largest economy.

China’s share in world GDP has increased sharply in a very short time span. China is also one of the world’s largest importers. The size of the Chinese economy and its global trade presence imply that the ripples from an economic slowing will be widespread. But the depth of projected setbacks is undoubtedly varied. In our estimation, the blow to the United States is at the low end of the impact barometer.

Trade and financial linkages between the United States and China are the primary sources through which Chinese headwinds influence business momentum in the United States. China is an important export destination for many U.S. multinationals. Caterpillar, United Technologies and Ford are a few firms that have already cautioned about the negative impact of developments in the country. Essentially, companies exporting to China are likely to experience a decline in profits. At the aggregate level, U.S. corporations earn roughly 20% of their profits from overseas operations. Official data for corporate profits by country are not available; China accounts for about 2.0% of income earned abroad. This is a partial aspect of the China-U.S. linkage.

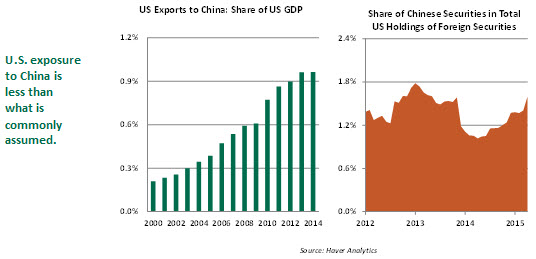

The overall trade relationship between China and United States presents a broader picture of the impact of China’s economic slowdown. China ranks as the second-largest trading partner of the United States, following Canada. This position stems from the fact that U.S. imports from China are roughly four times larger than exports going the other way. Total exports of the United States are 13% of GDP, while exports to China account for only 1.0% of GDP. By this measure, the United States is not likely to experience a large weakening of growth from fewer exports to China.

The second-order effects through China’s trading partners will also affect the size of the hit to U.S. exports. For example, a reduction in exports of copper from Chile and iron ore from Australia to China results in these economies weakening. In turn, the ability of Chile and Australia to import from the United States suffers. Studies indicate that these effects on U.S. exports are small but observable. A modest trimming of headline U.S. GDP is most likely through the trade channel, reflecting the direct and knock-on effects of China’s economic deceleration.

In addition to trade relations, financial exposure of U.S residents to China is another economic linkage that may bear on the economy’s performance. China’s large holding of U.S. Treasury securities is well known. By contrast, U.S. exposure to Chinese financial instruments is not frequently discussed in the financial press.

U.S. residents held almost $10 trillion in foreign bonds and equities in April 2015. Of this, Chinese financial instruments amounted to $159 billion, which is less than 2.0% of total foreign securities that U.S. residents hold. Tight quotas imposed by China allow foreigners to own only a small percentage of Chinese stocks. Therefore, the wealth effect of a large loss from holdings of Chinese financial instruments will not be significant.

Movements of commodity prices related to reduced business momentum in China is a secondary source that can affect the U.S. economy. China is a large consumer of commodities, ranging from energy to metals and a host of other items. One should not be surprised to see commodity prices react bearishly to signs of weakness in China. The S&P Goldman Sachs Metals Price Index has fallen about 26% from a year ago. Part of the decline in energy prices is from expectations of weak demand from China.

Both U.S households and firms stand to benefit from a decline in commodity prices. Also, lower commodity prices will trim import prices and hold back inflation readings, which can complicate the Federal Reserve’s monetary policy strategy somewhat.

Summing up, the United States is not completely insulated from China’s economic woes. But it is also unlikely to buckle from an economic storm in China, provided it is not of historical proportions.

A Higher Fed Policy Rate Should be in Place Soon

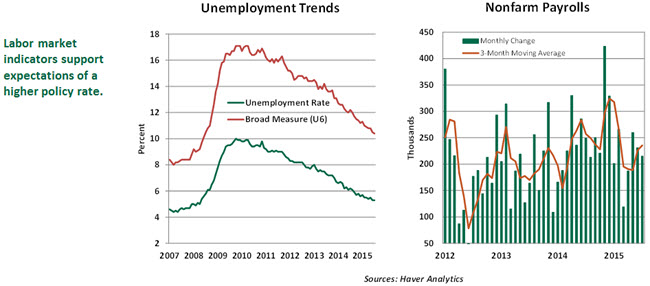

Headlines and details of the July employment report give little reason for the Fed to change its current view about labor market conditions.

The unemployment rate held steady at 5.3% in July, while the broad measure declined one notch to 10.4%. The participation rate – the share of the working-age population that is employed or looking for a job – was unchanged at 62.6% after recording a three-tenths drop in June. Even if more workers re-enter the labor force, the participation rate is likely to remain flat as baby boomers retire.

The decline in the broad measure of unemployment reflects a drop in the number of persons working part-time for economic reasons but who would prefer full-time jobs. The median duration of unemployment was unchanged at 11.3 weeks.

Non-farm payroll employment increased 215,000 in July, and upward revisions added 14,000 new jobs to prior estimates of payroll employment during the May-June period. The indicator’s 3-month moving average of 235,000 represents a firm hiring pace in the economy.

In the goods sector, employment rose 17,000, with construction and factory jobs both recording gains. Hiring in the service sector moved up 198,000, reflecting increases in government (+5,000) and private-sector employment. Health care, retail, finance, and business and professional services led with noticeable gains in employment. Oil industry-related hiring fell 5,000, marking a steady decline since the recent peak in December 2014.

The payroll diffusion index (measures percentage of industries increasing employment) also showed signs of strength, rising to 64.4% from 60.6% in June. The average workweek was longer in July (34.6 hours versus 34.5 hours in June), boding well for income and consumer spending but casting a shadow on the economy’s productivity. Average hourly earnings increased 2.1% from a year ago, a marginal improvement from June’s 2.0% gain.

Market expectations for a September increase in the policy rate have risen as of this writing. The disappointingly low gain in the Employment Cost Index during the second quarter led some to suggest a postponement of tighter monetary policy. However, the weakness was caused by volatile incentive compensation components of the index, which the Fed is likely to look through. Chair Janet Yellen has noted that while wage acceleration would certainly raise the level of Fed’s confidence, it is not a precondition for a rate hike. Fed rhetoric, particularly Atlanta Federal Reserve President Dennis Lockhart’s remarks earlier in the week, also suggests a September tightening of monetary policy.

Barring major downside surprises in U.S. economic reports between now and the September 16-17 Federal Open Market Committee meeting, a higher policy rate at that gathering is strongly likely.

Continued Low Inflation in the Eurozone

The European Central Bank (ECB) announced its new quantitative easing (QE) program in January, with the explicit goal of fulfilling its price stability mandate. The monthly purchase of €60 billion in sovereign, agency and private sector bonds aims to “address the risks of a too prolonged period of low inflation” when policy interest rates are at their lower bound. So how is it going?

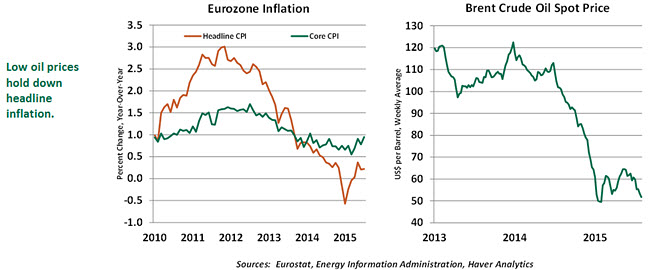

At the time of the announcement, the annual rate of inflation had dipped into negative territory for the first time in five years. The QE program kicked off in early March; since April, the slide into deflation has reversed but annual headline inflation is barely in positive territory. The global price of oil makes a significant contribution to the headline rate and is the primary reason inflation is still so low.

Core inflation (which strips out the price of energy, food, alcohol and tobacco) has remained in positive territory and now appears to be developing more upward momentum. However, the ECB targets headline inflation of “below, but close to, 2.0%.” The central bank focuses more on inflation expectations and on wages than on the core inflation measure.

On the plus side, QE seems to be helping end the prolonged credit crunch across the eurozone. Despite low energy prices, headline inflation readings should start to pick up as business momentum develops in the second half of this year and the slack in the economy eases.

In his comments after the ECB’s July 16 policy meeting, President Mario Draghi was notably dovish. With headline inflation still well below target, that stance is unlikely to change at the next meeting on September 3. Indeed, with global energy prices still weak and the broader eurozone economic recovery still tenuous, monetary tightening is off the table for a long time.

(c) Northern Trust