|

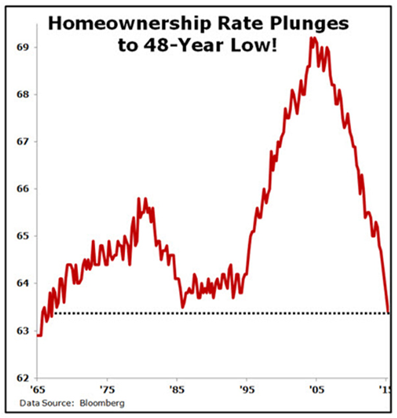

IN THIS ISSUE: 1. US Homeownership Rate Falls to Lowest Since 1967 2. More Millennials Living With Their Parents Than Ever 3. Rising Household Formation is Driving Rents Higher 4. Rental Problem Not Likely to Go Away Anytime Soon 5. The “American Dream” of Home Ownership is Fading Overview The government’s Census Bureau reported last week that the US homeownership rate fell to the lowest level in the last 48 years. It is indeed a sad awakening that the level of home ownership is now the lowest since 1967. Along this same line, the Census Bureau found that more Millennials (18 to 34 year-olds) are living with their parents today than at the worst point in the Great Recession. This is despite the fact that the economy and labor market conditions have improved in recent years. The issue is not that we aren’t forming more households. We are. The problem is that fewer and fewer households can afford to buy a house – despite record low interest rates – and more and more are renting rather than buying, whether by choice or by necessity. The fact that more and more Americans are choosing to rent their homes and apartments has resulted in rents going through the roof. It’s supply and demand, of course. But the fact that Americans are spending more and more on rent means that they have less and less to spend on buying other goods and services to spur the economy. The bottom line is that the American Dream of owning your own home is fading fast. This fact is affecting younger Americans the hardest. Way too many have given up the dream of owning their own home, as a recent Gallup poll has found. Today, we’ll look at this disturbing trend and try to discern why it is happening. US Homeownership Rate Falls to Lowest Since 1967 The nation’s homeownership rate continued its decline in the second quarter, dropping to a 48-year low, the Census Bureau reported last week. The homeownership rate slid to 63.4%, down from 63.7% in the first quarter and 64.7% in the second quarter of last year. The homeownership rate peaked in 2004 at 69.2% and has been down ever since. The last time homeownership was this low was in the first quarter of 1967, when the rate was 63.3%. Yet it’s not like tens of millions of Americans are living in the streets. Instead, they’re becoming renters – either by choice or necessity. Some of that stems from tighter mortgage standards. While they’ve eased ever so slightly in the past few years, they’re nowhere near as easy as they were in the early 2000s. Today, getting a mortgage or home equity loan involves multiple credit checks over a period of weeks, onerous income and asset verification headaches, higher credit scores and lower total debt-to-income ratios. That’s true even for well-qualified borrowers, not just those with credit blemishes.

Lackluster income growth is another problem, as is the fact that many younger potential buyers have insufficient down payment funds and meager savings. Many of them are burdened with high student debt loads and are under-employed based on their education levels. That means first-time home buyers are fewer and farther between. Then there’s the lingering psychological damage of the housing bust, and the desire for more mobility among the typical first-time buyer demographic. Renting keeps them from being tied down – a desirable situation given the fact “jobs for life” are a distant memory these days. More Millennials Living With Their Parents Than Ever Young adults are living with their parents at greater rates than during the lowest point of the Great Recession, even in the face of improved job prospects as the economy recovers. The living arrangements of young adults seem to have come unhinged from labor market conditions, as they are becoming less likely to live on their own as the economy improves from the financial crisis. Five years into the economic recovery, full-time employment is up and wages are starting to rebound. But despite these improvements in the labor market, more Millennials are living with their parents than they were during the worst period of the recession, according to a new Pew Research report last week based on the latest Census Bureau data. In fact, the nation’s 18 to 34 year-olds are less likely to be living independently of their families and establishing their own households today than they were in the depths of the financial crisis. In 2007, apprx.71% of this demographic lived independently of their parents; but the Census Bureau found that only 67% are living on their own as of the end of April of this year. Meanwhile, the national unemployment rate for adults ages 18 to 34 declined to 7.7% in the first third of 2015, a significant recovery from the 12.4% who were unemployed in 2010. Other standard benchmarks also demonstrate that nationally the young adult labor market has strengthened. In spite of these positive economic trends and the growth in the 18 to 34 year-old population, there has been no uptick in the number of young adults establishing their own households. In fact, the number of young adults heading their own households is no higher in 2015 (25 million) than it was before the recession began in 2007 (25.2 million). This may have important consequences for the nation’s housing market recovery, as the growing young adult population has not fueled demand for housing units and the furnishings, telecom and cable installations and other ancillary purchases that accompany newly formed households. Rising Household Formation is Driving Rents Higher Despite more young adults living with their parents, the number of US households was up by almost 1.5 million in the first quarter of 2015 from a year earlier – the second consecutive quarter of relatively strong growth, following years of only tepid gains. But the net increase was entirely due to renters, since the number of owner-occupied households fell slightly. Much of the problem is attributable to simple supply and demand. The job market has improved and more people are entering the labor pool in force, boosting household formation. But in a structural shift for the real estate market, new households are much more likely to be renters than buyers.

The problem is, all those forces noted above are driving rents much higher. With homeownership out of reach of many people, the cost of renting is rising much faster than inflation, forcing even more low and middle income Americans to pay a larger share of their income for housing. Nationwide, US government data shows tame overall inflation, with the notable exception of rent. MPF Research, which tracks occupancy and rental rates, found second-quarter rents rose 5.2% from a year earlier nationwide, a 15-year high. Oakland, CA led the way with an 11.8% increase in rent. The strongest rent growth is in the West, but prices also are rising in mid-tier cities across the US.

Economists and mortgage lenders generally consider a household to be “cost-burdened” when it is paying 30% or more of its income for rent. And as we can see above, the national average is now at 30% of average household income. Younger Americans also are taking an even bigger hit. From 2003 to 2013, the share of renters aged 25 to 34 who are considered cost-burdened increased from 40% to 46%, according to a recent report by Harvard University’s Joint Center for Housing Studies. So, we now have yet another housing affordability crisis on our hands. Rental Problem Not Likely to Go Away Anytime Soon Many people now living in rentals were once home owners. Millions lost their homes to foreclosure during the Great Recession and now have such damaged credit reports that they find it nearly impossible to qualify for a mortgage. Others are trapped because lenders have significantly tightened credit standards after the lending abuses of the boom era.

While home foreclosures fell to the lowest level since 2006 last year, millions of Americans lost their homes in the Great Recession. The numbers in the chart above include foreclosure filings, default notices, scheduled auctions and bank repossessions. While the federal government has created programs to encourage lenders to offer mortgages requiring only a small down payment, the results have been disappointing – to the point that the government won’t even say how many people have taken advantage of them. President Obama’s mortgage modification program has been a bust (see first link below). The nation’s changing demographics are also causing a major shift in housing trends. For instance, a majority of new households expected to be formed in coming years will consist of people with a minority background. Historically such Americans have had lower incomes and fewer assets and were less able to buy homes, according to the Urban Institute. At the same time, millions of young adults who normally would be first-time home buyers are still struggling to find decent jobs; many are also putting off marriage and having children, a trigger for home buying. As noted above, they are also more likely than previous generations to be saddled with heavy student loan debt that hurts their ability to save for a down payment or qualify for a mortgage. But it is not just younger people who are having trouble owning a home. According to the Harvard report noted above, the home ownership rate dropped the fastest for people in their late 30s to early 50s. These people are in their prime home-buying years. The “American Dream” of Home Ownership is Fading The so-called American Dream is a national belief in a set of ideals in which freedom includes the opportunity for prosperity and success achieved through hard work in a society with few barriers. Within that dream is the desire for homeownership. But that dream is fading for too many. A Gallup poll taken earlier this year found, unfortunately, that more and more Americans have given up on the dream of owning their own home. Only 7% of Americans polled think they will buy a home in the next year; only 36% think they will buy a home in the next five years – although both figures are not far off of where they were two years ago. But the numbers further out are startling. Among those asked if they think they will buy a home in the next10 years, the number drops from 22% in 2013 to only 15% this year. Of those who were asked if they don’t expect to buy a home within the foreseeable future, the number jumps from 31% to 41%. Put differently, over four in 10 Americans have given up on owning a home!

In Gallup’s own words: It has been a closely held belief for many in the U.S. that owning a home is a key to eventual personal prosperity. But the Great Recession of 2007-2009 may have changed Americans’ ability to act on that belief, given that the housing market has yet to return to pre-recession levels of ownership or home values. It is possible that homeownership will return to previous levels in the years ahead if the economy continues to improve; it is also possible that a ‘new normal’ is occurring in this country, wherein Americans won't be buying a house for the foreseeable future. For a younger generation that is struggling with student debt, renting a home may be an increasingly safe option. Whatever the reasons, non-homeowners’ expectations for buying a home in the near future appear to be waning, and the percentage who say they own their own home is the lowest in nearly 15 years. The trend toward renting versus owning is troubling, and the homeownership rate now stands at the lowest level in 48 years, according to the Census Bureau. Even worse, if this trend continues, the homeownership rate will be at the lowest level ever recorded sometime next year. We have become a “Renter Nation.” Finally, with interest rates at historic lows and mortgage rates below 4% in many places, this should be the home buying opportunity of a lifetime. Sadly, too many Americans are deciding to rent – either by choice or necessity. I’ll leave this discussion on homeownership versus renting there for now. Finally, if you want to read my analysis of last week’s GDP report and the multi-year revisions, go to my BLOG from last Thursday afternoon. Wishing summer wasn’t going so fast, Gary D. Halbert |

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |