Much has been made of the fact that defensive sectors, or counter-cyclicals as we prefer to call them, have been leading the market higher. This is very much out of the norm for a bull market, even for a cyclical bull market within a structural bear market, as cyclicals tend to lead equity markets higher while counter-cyclicals help investors play defense when the market breaks lower. However, since the market turmoil in the summer of 2011, growth counter-cyclicals have been a great place for investors to park their capital. Over the past four years, on an equal-weighted, USD basis, the four best performing sectors in the developed market are health care, consumer discretionary, information technology, and consumer staples. What do these four sectors all have in common? They all spend a greater percentage on intangible investments, or knowledge investments, than they do on traditional tangible capital expenditures.

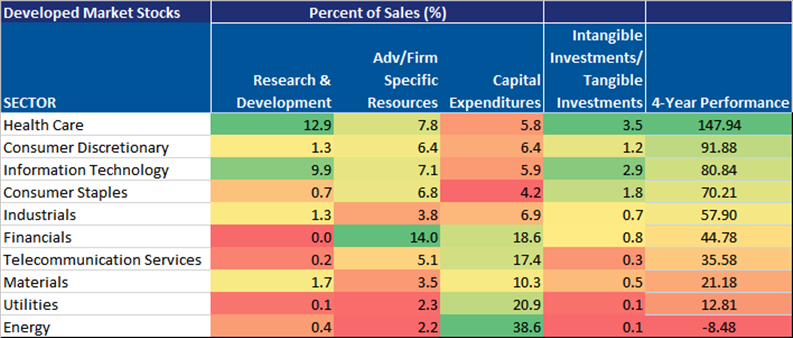

In the table below, we show how much each sector spends on intangible investments as a percentage of sales (R&D and advertising and firm specific resources) and tangible investments as a percentage of sales (capital expenditures) for developed market companies. What we find is that for the four best performing sectors they all invest a greater percentage of their sales in intangible investments than in tangible investments. This gives them a intangible/tangible investment ratio greater than one.

Health care leads the way as this sector spends about 3.5x as much on intangible investments as they do on tangible investments. Information technology is second with a 2.9x ratio, followed by consumer staples (1.8x) and consumer discretionary (1.2x).

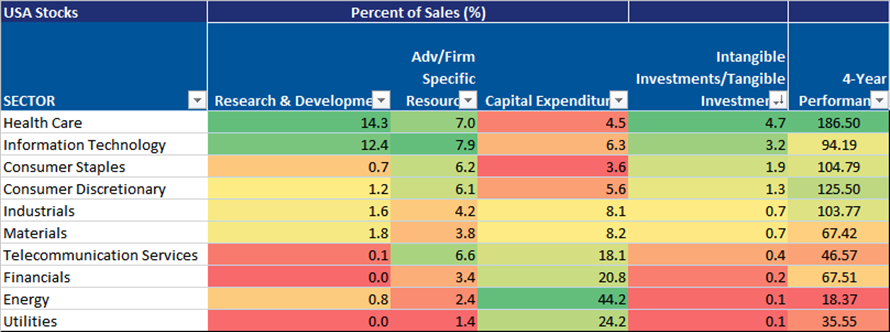

If we look at just US stocks, the 1x ratio threshold holds and it is even clearer that knowledge investments are being valued at a higher premium than tangible investments. In the table below, we are sorting from highest to lowest in the intangible/tangible investment ratio column. This lines up perfectly with the sector breakdowns of our Knowledge Leaders, with highly innovative sectors such as health care and information technology having the best performance while less innovative sectors such as energy and utilities having the worst performance.

So while traditionally it may seem that this has been a defensive-led bull market of late, it is worth considering that we may be in the midst of re-rating of corporate innovative assets. Those companies that are investing more in intangible assets are clearly demanding higher returns than those that are investing more in tangible assets. This is playing out on a broad sector basis as we have shown above but it is also playing out even more clearly if we look at the companies that are truly pushing the innovation curve forward. The most innovative companies, Knowledge Leaders, follow a strategic innovation strategy while Knowledge Followers follow a strategic mimicking strategy. The performance of Knowledge Leaders has outperformed the MSCI World Index by over 5% YTD and by over 141% since 3/31/2000.