Introduction

The primary attractions supporting investing in bonds or other fixed income instruments have traditionally been high income and safety. People invest their principal in bonds and receive a stated interest rate (coupon) over the life of the bond and are given the promise of having their principal returned at maturity. Under normal times, bonds would typically pay a higher rate of interest than the dividend rate on stocks. Consequently, bonds have acquired the reputation as low risk and high income instruments.

However, risk is a multifaceted concept. The risk of losing all your money is one of the investor’s greatest fears. Virtually all high-quality bonds eliminate this loss of principal risk. But there are additional risks that bonds do not always protect investors from. Fixed income investments provide little or no inflation protection, especially when interest rates are as low as they are today.

Then, there is liquidity risk. Both stocks and bonds fluctuate in price as a direct consequence of the liquidity they provide investors. The primary determinant of a bond’s price fluctuation is changes in interest rates. When interest rates rise, the prices of existing bonds will fall, and vice versa. In contrast, there are many factors that can cause stock prices to rise or fall. But my primary point is that liquidity risk, when investing in bonds at low rates of interest like we have today, is very high. In the current environment, bonds do not afford much protection against liquidity risk. Stocks may or may not.

The bottom line is that I support investing in bonds when they possess the characteristics of providing higher income than I can get on a dividend stock. In fact, there was a time when I completely avoided investing in stocks altogether, favoring investing only in bonds instead. That time was from 1979 through all of 1985, a period of time when AAA rated corporate bonds were paying double-digit interest rates. When I could get interest rates of 10% to as much as 15% by investing in high-quality bonds, I avoided stocks altogether. It made no sense to me to assume the risk that came from owning stocks when I could get double-digit rates on bonds and be virtually guaranteed to get my principal back.

Unfortunately, today the reverse is true as the rates on high-quality bonds are in many cases lower than the dividend income I can earn on high-quality blue-chip dividend stocks. Therefore, just as I exclusively invested in bonds during 1979-1985, today I am exclusively investing in high-quality blue-chip dividend stocks. However, I consider this a temporary posturing as I would once again enthusiastically utilize bonds when they make economic sense and provide the safety and predictability that they traditionally have.

Rebutting the Rebuttal to My Recent Article

Fellow Seeking Alpha Author Gary Golnik recently authored an article titled “I Can Endure More Bond Duration Than Chuck” in an apparent attempt to retort my recent article titled “How Much Bond Duration Could You Endure?” however, I believe that Gary failed to effectively counter my arguments with his article for the following reasons.

First of all, what Gary failed to point out or recognize, is that 20 years ago when I could have received a 6.82% yield on AAA rated corporate bonds, I would have been delighted to support including them in a retired investor’s well diversified and balanced portfolio. At that time (1996) the dividend yield range on most fairly valued dividend growth stocks was only 1%-3%. Therefore, bonds offered a significant yield advantage.

As a result, the higher yield differential benefit of investing in bonds at that time was worth it. Consequently, I was delighted to support building retirement portfolios balanced between stocks and bonds, especially for retired investors that needed a high level of current income. With interest rates attractive at the time, it was logical to build a balanced portfolio of high-quality bonds laddered across various maturities, coupled with attractively valued dividend growth stocks with lower yields but capital appreciation potential in order to fight inflation.

At that time, a balanced portfolio could easily be designed to be able to adapt to the future when bonds in a rationally designed ladder matured. If capital appreciation was high enough, and the dividend growth stocks were generating enough current income due to growth yield (yield on cost) investors would have the option to reinvest the proceeds in either new bonds or stocks as they chose according to their specific needs and risk tolerances.

Additionally, in 1996 bonds made sense because their yields were high enough to even be considered competitive with the traditional long-term returns of approximately 6%-8% that stocks have historically achieved. Consequently, due to the predictability of their then higher fixed income stream, and the high certainty that your principal would be returned at maturity (at least in nominal terms), it was quite rational to opt for the lower risk qualities available with investing in bonds.

Furthermore, the pricing of previously issued bonds going forward remained strong and healthy because of the continuous downtrend in interest rates that followed. Here I will add that this was not predictable, because forecasting future interest rates never is, but it was an excellent side effect and benefit for owners of bonds previously issued when rates were higher.

Accurately predicting future interest rates remains unpredictable. However, with rates as low as they are today, logic would dictate that the direction of interest rates is more likely to be higher than lower going forward. That would not be a good environment for recent purchasers of bonds. The following historical graph courtesy of FRED (Federal Reserve Bank of St. Louis) of AAA corporate bond yields summarizes the above statements:

The following excerpt from Gary olnik’s article was offered to support his contention that, and I quote: “So while stocks may beat bonds, they don't beat bonds by enough over the next few years to warrant the risk of a portfolio heavy in stocks.” But as I will soon extensively illustrate, Gary left an important return component out of his comparison. Here is what Gary said and his supporting graphic:

“I've finished my thoughts and haven't referred to a single stock!! Egads, what shall I do? The figure below shows the total growth of dividends over the last twenty years (data from Chuck's F.A.S.T. Graphs) for stocks compared to the return available from bonds at various rates. I chose a bunch of stocks at random from Mike Nadel's new DG50 (Southern Co. (SO), Kellogg (K), Realty Income (O), General Electric (GE), Exxon Mobil (XOM), Emerson (EMR), 3M (MMM), Coca-Cola (KO), Clorox (CLX), Hershey (HSY), Deere (DE), PepsiCo (PEP), Lockheed (LMT), Johnson & Johnson (JNJ)) just to illustrate.”

Unfortunately, Gary left out capital appreciation, the most important part of a proper calculation which is the primary reason I don’t like bonds today. To be clear, the above graph compares dividend growth rates only to the interest rate of a bond. Frankly, I don’t see a logical comparison between the two. Gary attributed the results depicted on the dividend growth stocks on the X-axis on his above graph to data he pulled directly from F.A.S.T. Graphs™.

But most importantly, he leaves out capital appreciation, or in the case of bonds - the lack thereof, and he does not compare apples to apples. So allow me to present the complete picture utilizing the same stocks that Gary referenced in his article. However, I will include the entire dividend record, plus report the capital appreciation thereby reporting the more important total return differential. I have cut and pasted the correlating returns of a 6% bond, which was the highest rate Gary’s rebuttal presented in place of the S&P 500 comparison that is usually on each performance graph.

I think the reader will discover that the advantage of his selected stocks was much greater than Gary indicated. I have placed a highlighted circle around the cumulative total dividend income and around the capital appreciation component, and total income plus capital appreciation for the reader’s quick reference.

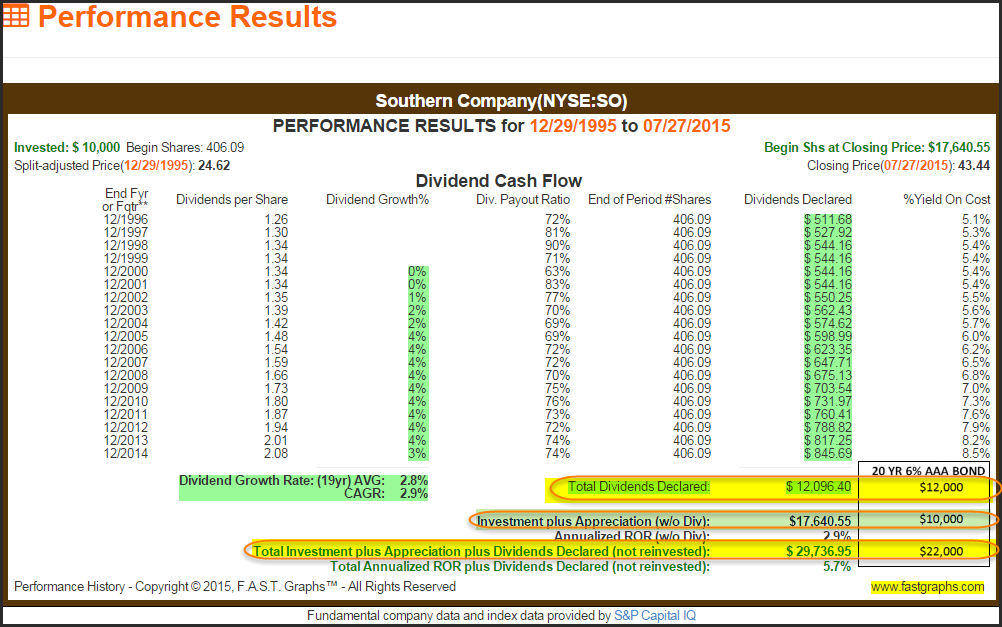

Southern Company

The first and worst performing stock that Gary improperly presented was the low growth, high yield utility stock Southern Company. According to Gary’s graph, it produced less cumulative dividend income than the 6% bond. But once again, he was comparing dividend growth rates with the total income of a bond. The dividend growth rate and the total income it produced are two entirely different things. Consequently, according to the performance report below, Southern Company actually produced approximately the same dividend income as the 6% bond produced cumulative total interest.

However, remember that Gary was comparing apples to oranges by referencing the dividend growth rate which was in fact low as to be expected from a utility, but high enough to produce an equal amount of income. But even with this lowest growth example, Southern Company produced a capital appreciation value in excess of $17,000 while the bond only returned the original $10,000.

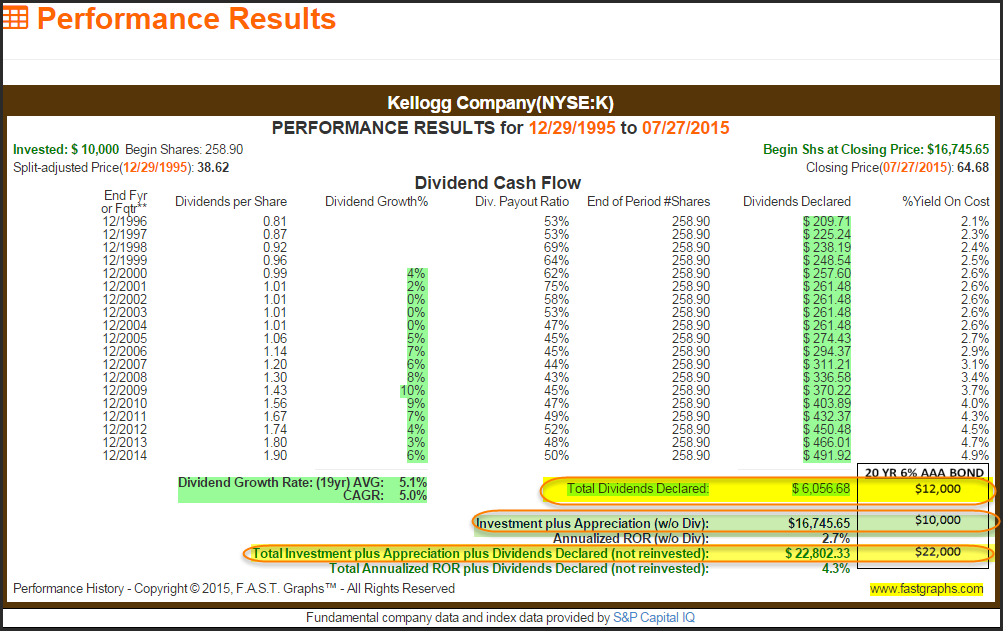

Kellogg Company

The second worst performing stock according to Gary’s graph was Kellogg. But once again, he was referring to the dividend growth rate only, and failed to include total cumulative income or capital appreciation which would be a more exact comparison. Kellogg did in fact produce half as much dividend income as the 6% bond produced interest, so on that front Gary wins. However, Kellogg did return a capital appreciation value of just under $17,000, which brought the stock to a virtual dead heat with a 6% bond regarding a factual comparison of total return.

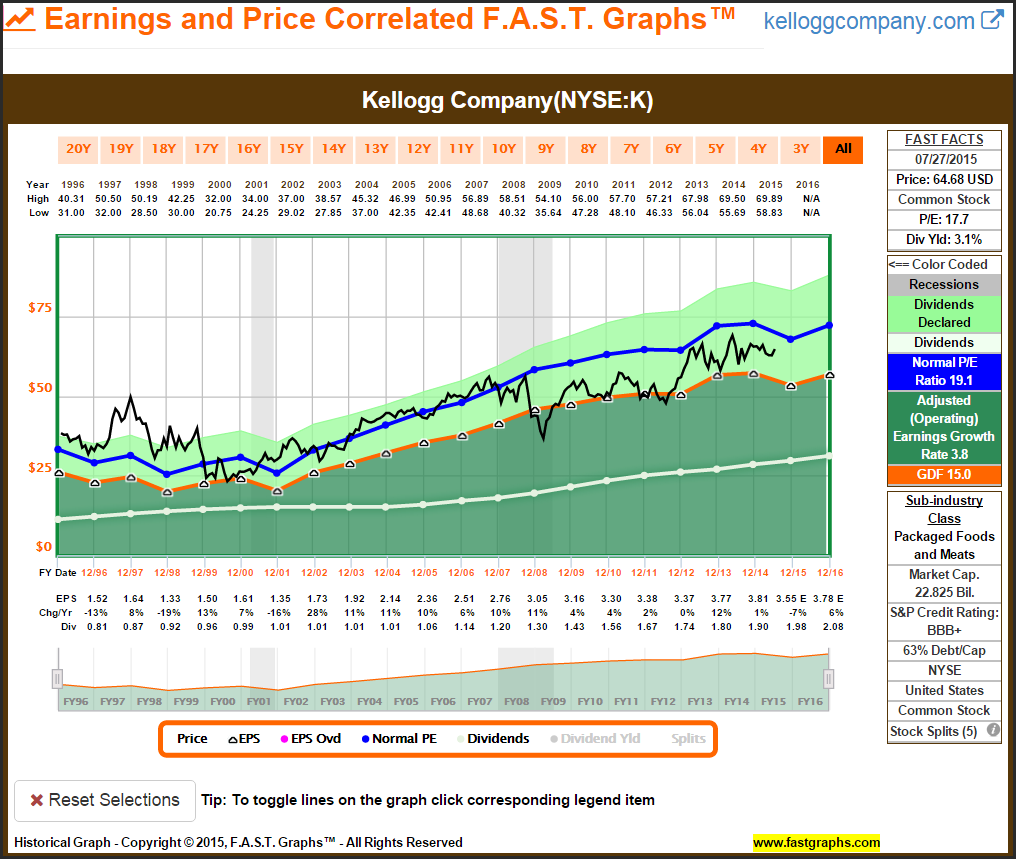

However, something else that Gary failed to take into consideration was the fact that Kellogg was overvalued in 1996, and therefore, a rational valuation oriented investor like yours truly would not have invested in it at that time. I am only against bonds when they don’t make rational economic sense, but likewise, I am also against investing in dividend growth stocks when they don’t make rational economic sense.

At the beginning of 1996 that was clearly the case with Kellogg as the following earnings and price correlated F.A.S.T. Graphs™ reveals. However, I will concede that Kellogg’s P/E ratio of 22.3 at the beginning of 1996 may not have deterred all dividend growth oriented investors.

Realty Income Corporation

The third worst performing stock suggested by Gary’s graph was Realty Income Corporation, the high-quality REIT known as the monthly income company. I felt that this example was especially misleading because simply referencing its dividend growth rate of just less than 4% ignored the significant total income advantage it generated over the bond and the capital appreciation value.

Realty Income Corporation generated more than twice as much cumulative total dividend income than the 6% bond, and additionally returned almost $42,000 of capital versus the $10,000 return of principal for the bond. I chalk this one up as a great win for the dividend stocks.

Additionally, it is interesting to note that Realty Income Corporation actually offered a higher current dividend yield than 6% at the beginning of 1996 (see orange highlight on above graph). There was arguably more risk here, but Realty Income Corporation even offered a yield advantage over the 6% bond. But my main point is that Gary’s graph greatly understates the value of investing in Realty Income Corporation in 1996, which by the way was also attractively valued at that time.

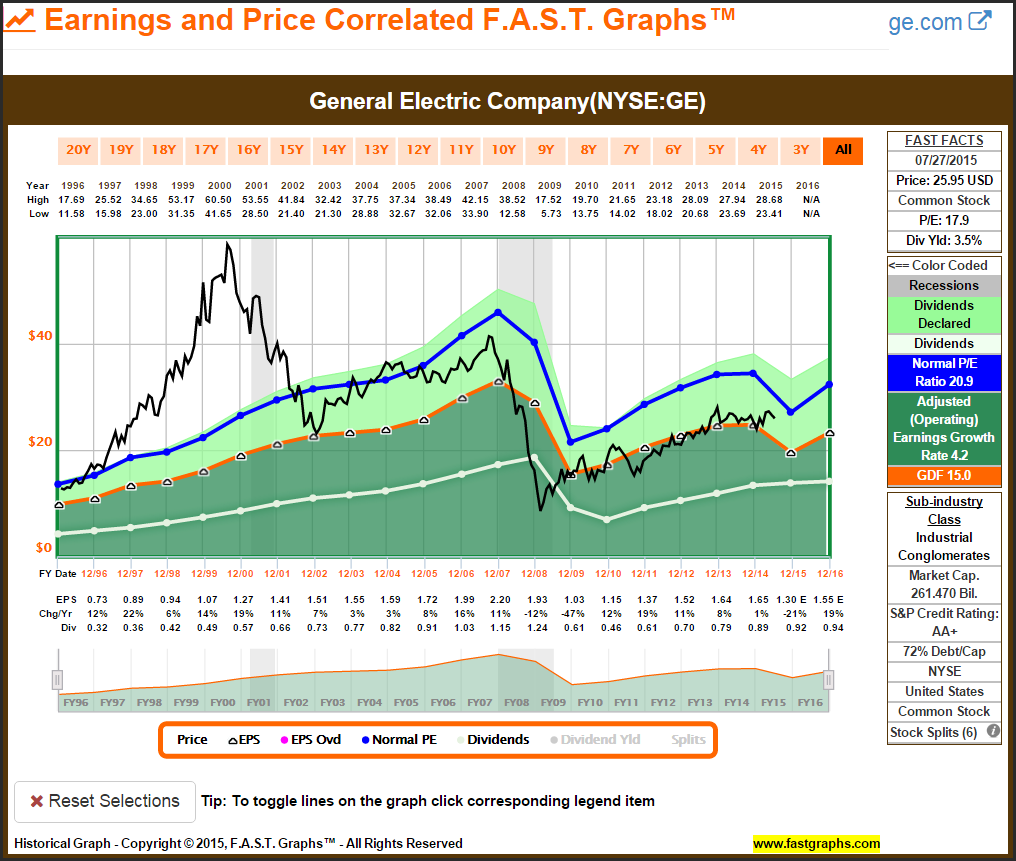

General Electric Company

As it turns out, General Electric was a rather interesting company for Gary to highlight for several reasons. First of all, it became insanely overvalued coming into the irrational exuberant timeframe 1996-2000, which led to what can only be called a catastrophic fall from grace by the end of 2002. Then with the Great Recession came another catastrophic drop in price, and making matters worse, a 51% dividend cut in 2009 followed by another 25% cut in 2010.

Yet, in spite of all that calamity, long-term shareholder owners of General Electric would have received just under $11,000 of total cumulative dividend income compared to $12,000 of interest income from the 6% bond, and ironically notwithstanding all the volatility in between, just over $21,000 of capital appreciation value.

As an interesting aside, in reality I personally would not have held General Electric over the following 20 years, because in truth and fact, I did own it in 1996 but sold it in 1999 due to excessive overvaluation. I only mention this because it speaks to risk control that comes when prudent investors pay attention to sound valuation.

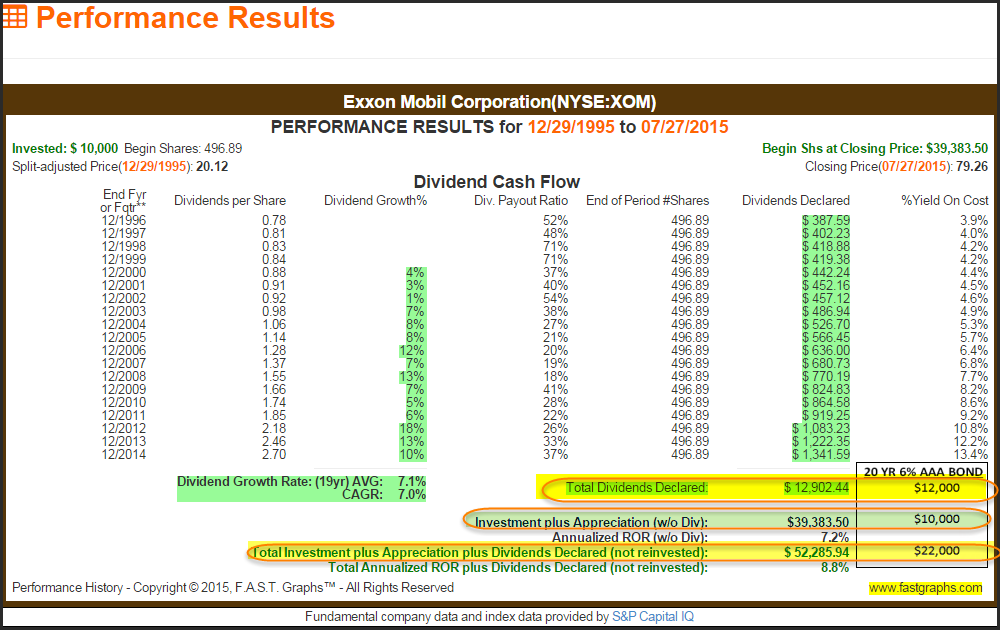

Exxon Mobil Corporation

Due to the problems the oil sector is now experiencing, energy stocks like Exxon are clearly currently under great stress. Nevertheless, I find it interesting that Exxon, thanks to its long and consistent history of raising its dividend, generated a slight total dividend income advantage over the 6% bond. But more importantly, even when measured in the backdrop of the current or recent poor performance of energy stocks, the fact that it almost quadrupled the original $10,000 investment is worth noting.

Emerson Electric Co.

Emerson Electric did as Gary indicated; generate an interesting dividend growth rate which placed in the middle of Gary’s graph. However, in spite of that fact, Emerson Electric underperformed the 6% bond based on total dividends, but did return just over $28,000 of capital value. In other words, 2.8 times the ending value of $10,000 returned by the bond.

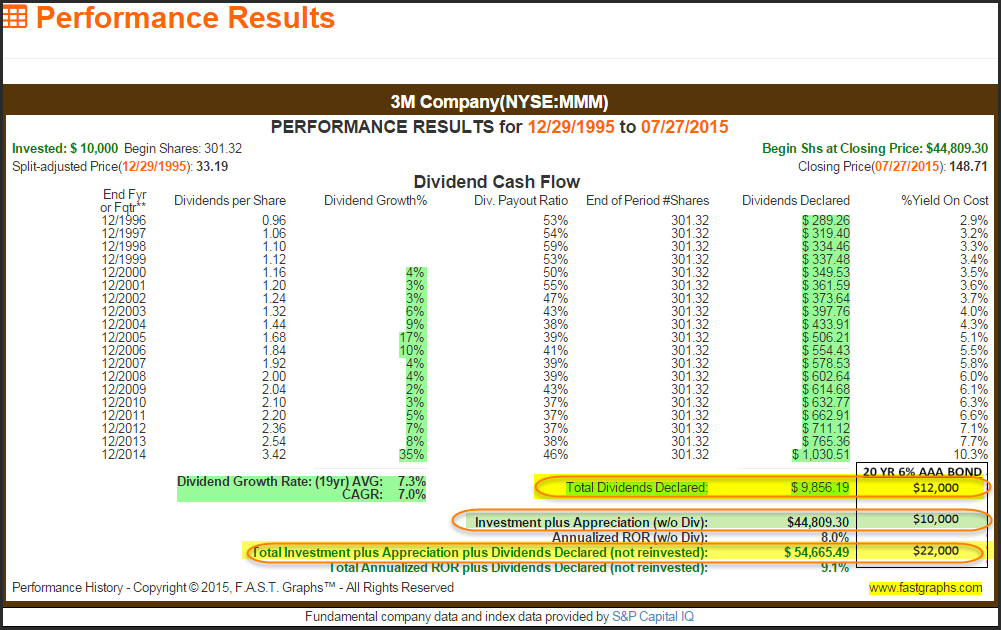

3M Company

As we continue up the staircase of Gary’s graph, we come to 3M. This company did produce less total dividend income than the 6% bond produced interest, but it did provide just under $45,000 of capital value providing a solid hedge against inflation.

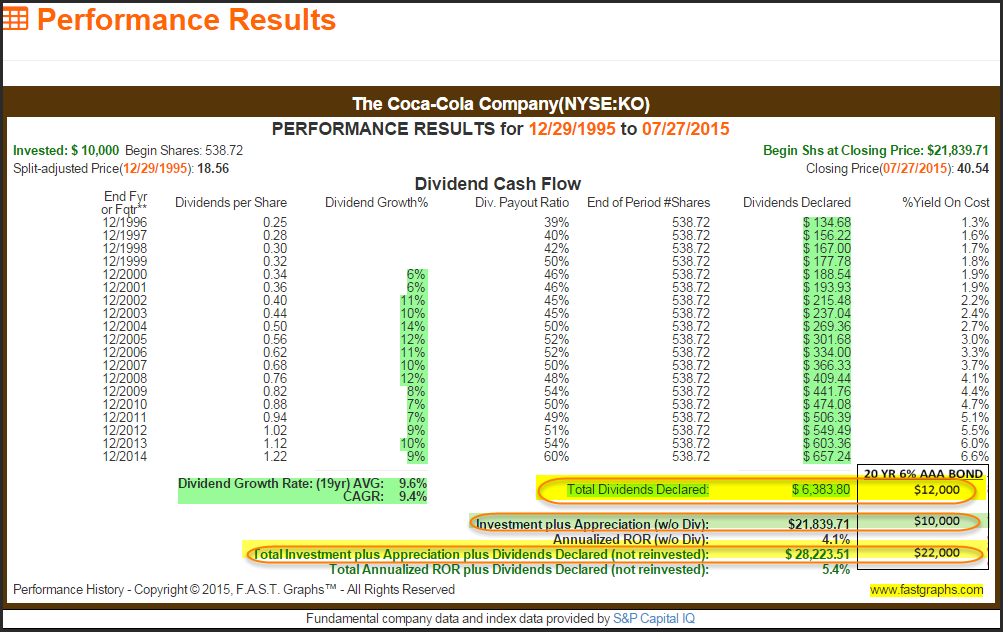

The Coca-Cola Company

Coca-Cola produced approximately half the dividend income as compared to the interest the 6% bond would have generated. However, it did produce just under $22,000 of capital value. I would agree with Gary that this example did not beat bonds by enough to justify the risk. However, I would argue that prudent valuation oriented dividend growth investors should not have invested in Coca-Cola at the beginning of 1996. Valuation was too high, and the dividend yield to low.

Personally, I would have definitely chose 6% bonds over Coca-Cola in 1996 because its dividend yield at that time was only 1%, and it was significantly overvalued. I am not against bonds, especially when they make economic sense. I am not generally against stocks, but I am against them when they don’t make economic sense.

The Clorox Company

I found the Clorox example that Gary selected especially interesting. First of all, Clorox was very attractively valued at the beginning of 1996 and offered a dividend yield of close to 3%. Over time, the company’s dividend yield eventually caught up to the 6% bond, resulting in total dividend income that was significantly higher than the cumulative total interest on the bond. And as Gary alluded to in his graph, its dividend growth rate was also high at approximately 10% per annum.

However, the most interesting aspect of this example was the capital appreciation value that came in at over $67,000, or more than 6 ½ times what the bond returned. In other words, when a great dividend growth stock can be purchased at a sound valuation and an attractive dividend yield, the long-term rewards can be quite satisfying.

The Hershey Company

I have long admired the Hershey Company, but alas I’ve never been comfortable paying the premium valuation that this company has consistently commanded. The following performance report would support that my decision to avoid Hershey has been a mistake. However, since both this article and Gary’s are focused on risk, Hershey’s chronic overvaluation has been a risk that I have been unwilling to take.

Had I been willing to take the risk, since 1996, I would have received just slightly less total cumulative income than I would have received interest on the 6% bond, and my capital appreciation would have been more than fivefold what the bond returned.

Deere and Company

Deere & Company represents another example of a dividend growth stock that was fairly valued and available at a moderately high yield at the beginning of 1996. Consequently, it would have produced cumulative dividend income that was only slightly less than the 6% bond. However, the original $10,000 investment would have grown to over $62,000. I think that’s a clear advantage to stocks.

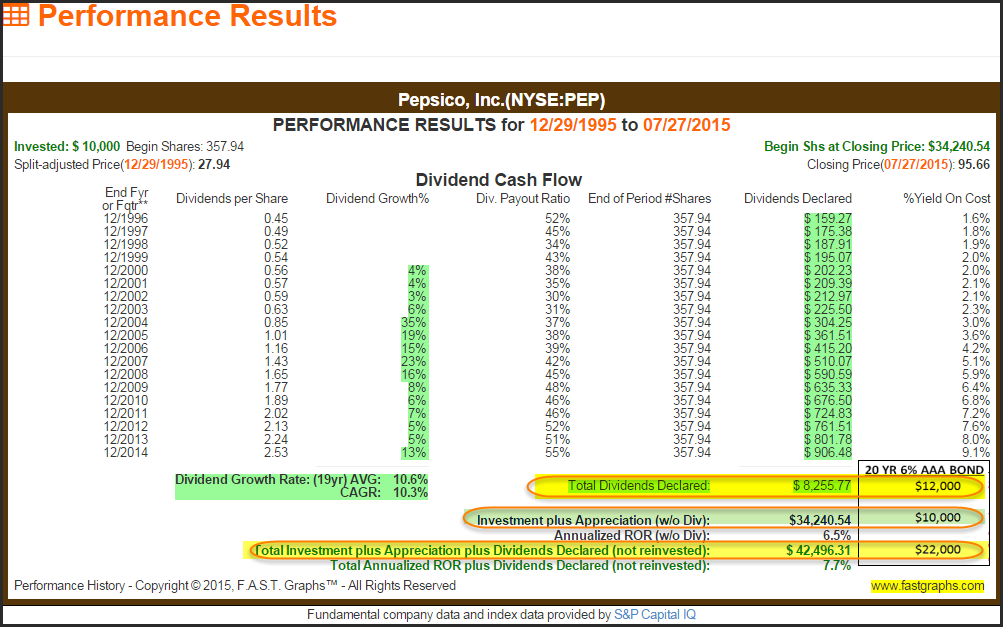

PepsiCo, Inc.

In the same vein as Coca-Cola, and similar to Hershey, PepsiCo is a dividend growth stock that I have long been interested in owning. However, excessive overvaluation in 1996 coupled with a low dividend yield in 1996 was a deterrent. Nevertheless, even this overvalued low yielding dividend growth stock since 1996 produced an attractive level of total dividend income, albeit less than that 6% bond. And in spite of the overvaluation headwinds, it would have produced more than three times my original investment thanks to the inflation fighting capabilities of capital appreciation.

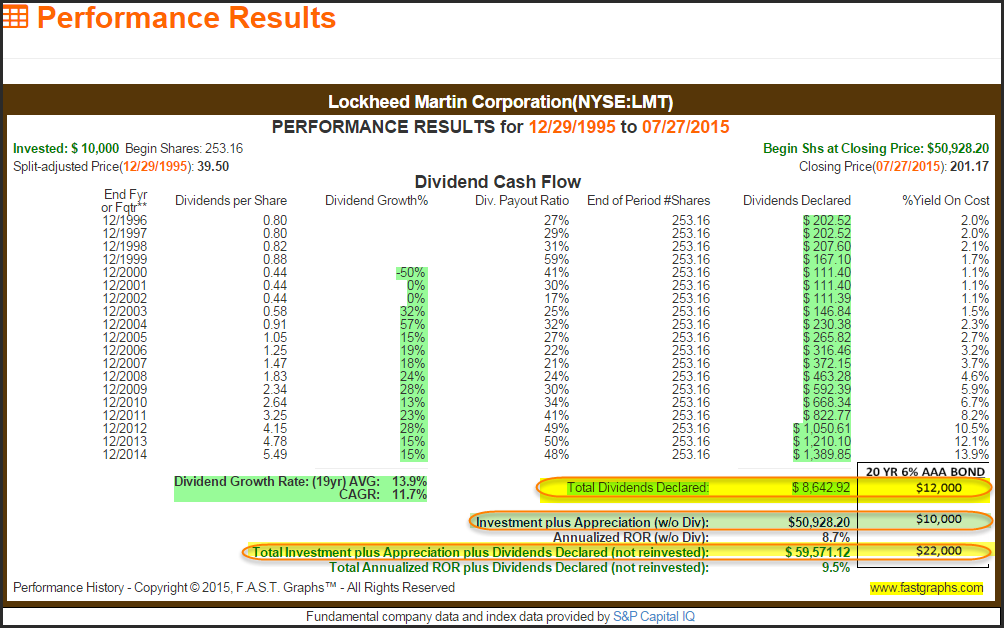

Lockheed Martin Corporation

This was another dividend growth stock that was fairly valued in 1996 but still underperformed the 6% bond in total income. However, capital appreciation that was more than fivefold the bond supports the benefit of investing in stocks over bonds regarding the opportunity of fighting inflation.

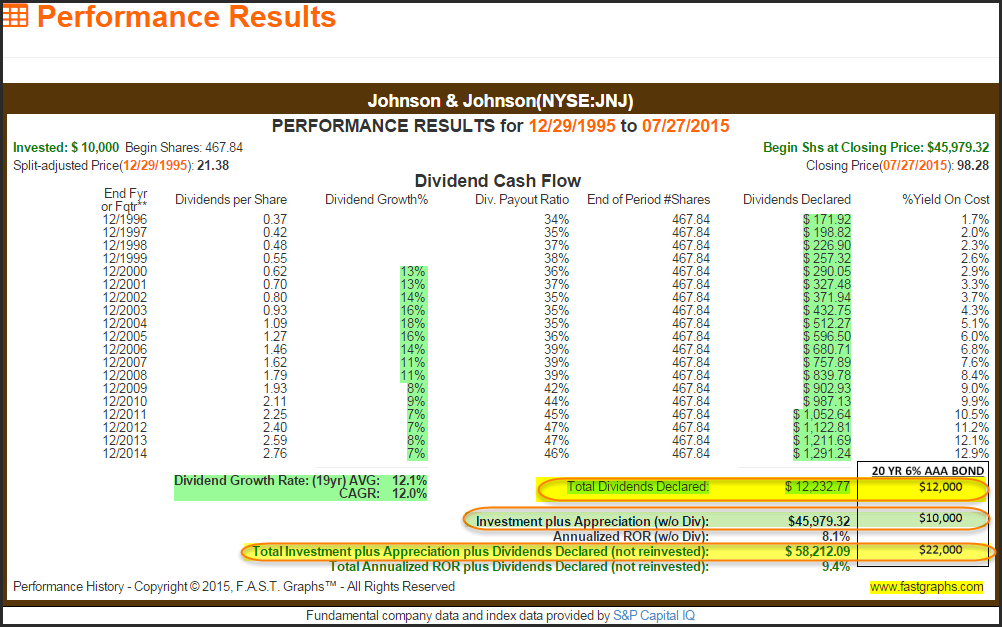

Johnson & Johnson

Gary’s final example on his graph was what many consider the “king” of all dividend growth stocks Johnson & Johnson. As Gary’s graph indicated, Johnson & Johnson did have the highest dividend growth rate, but this was somewhat mitigated by high valuation in 1996. Nevertheless, this AAA rated blue-chip outperformed the 6% bond on total income, and generated over $46,000 of inflation fighting capital appreciation.

A Summary of My Rebuttal to Gary’s Rebuttal Thus Far

Although I apologize to the reader for the lengthy rebuttal to what represented the conclusion of Gary’s article, I did so because as the old adage goes “the devil’s in the details.” First of all, Gary utilized bond rates in his closing argument that simply are not available today. Furthermore, his graphic presented the argument that stocks did not provide enough of an advantage over bonds to justify the risk.

However, his graph compared dividend growth rates, not dividend income generation or capital appreciation, to the income from high interest paying bonds that are actually not currently available. But most to the point, comparing the dividend growth rates of stocks offers no relation or relative merit to the interest rate available on the bond.

The dividend growth rates of stocks are simply not relevant to his argument. The only thing that would have been relevant is a side-by-side comparison of the total returns generated by each, which is what I presented. So sorry, Gary, I believe you meant well, but I did not find your concluding argument relative or even germane to the subject.

I Have an Investment Proposition for You

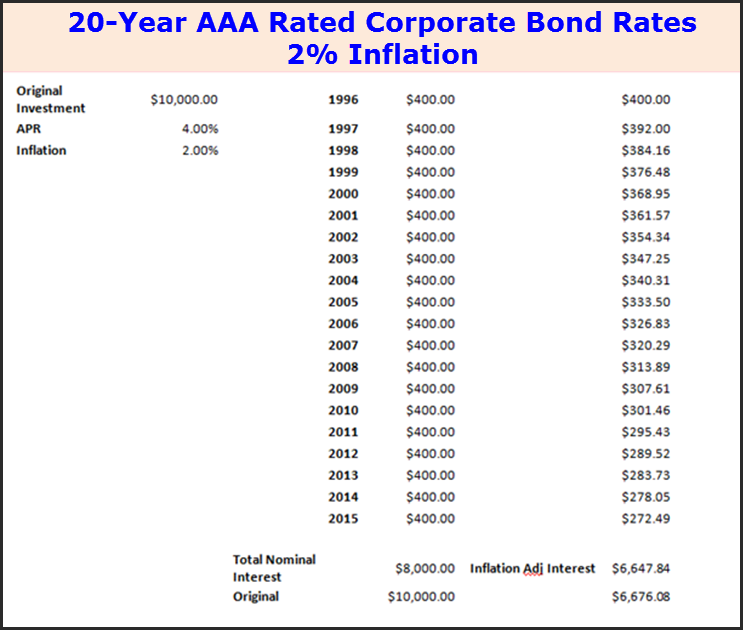

If I was an investment salesman, although I am not, and came to you with the following proposition, would you be interested? The proposition is as follows: I would like to offer you a 20-year investment that will start out paying you 4% per annum, however, the yield will drop or decrease by 2% every year thereafter until maturity. Additionally, I will virtually guarantee that I will return approximately 67% of your original principal invested after the 20 years have passed. How many thousands of dollars would you like to invest with me today?

I doubt that many of you would take me up on that proposition. However, the odds are extremely high that that is exactly what you would be doing if you invested in an AAA rated corporate bond today. The 20-year AAA rated corporate bond currently yields 3.8%. In the following presentation, I rounded that up to 4%. Therefore, I provided a mild advantage to the bond.

Then I assumed an inflation rate of 2%, which is significantly less than the rate of inflation over the last couple of decades. Once again, I provided a mild advantage to the bond. In my original article, I suggested on several occasions that bonds were simple. I did receive comments challenging that statement; however, I stand on my position. The reason I state that bonds are simple is straightforward. You buy a bond at a specific amount (face value), it will then pay a specific rate of interest over the specified time if held to maturity. Bond investing cannot really get any simpler than that.

However, because of inflation, bonds are not as low risk as Gary suggests. I am not saying that bonds are riskier than stocks; I concede that the opposite is true. On the other hand, the alleged lower risk of bonds only applies to the predictability of receiving a fixed amount of interest each year, and a high probability of having your original investment returned. Because by definition, bonds are fixed income instruments, they have no inflation fighting capacity at all. In contrast, it cannot be said that stocks will absolutely fight inflation, but they at least provide the potential to.

Additionally, the only time that bond investing can get complicated, is if you decide to sell the bond prior to it maturing. This simply provides liquidity risk or benefit depending on what interest rates have done since you originally purchased your bond. As I did in my original article, and for those that would like to learn more about the relationship between bond prices and interest rates here is a link to a Wells Fargo educational piece that summarizes things nicely. If you have any confusion about how this all works, I believe the Wells Fargo investing basics explanation will clear things up.

This brings me to a further rebuttal of what Gary presented in his article. In the article he states, and I quote:

“Bonds

Much has been made about the declining value of bonds in a rising interest rate environment. Bond pricing is simple to calculate in Excel, but is a bit hard to wrap your head around. The figure below lets me understand the basic concepts a bit more easily. I plotted the cost (or value) of a $10,000 face value 10-year bond with a 5% coupon, with various market rates (4, 5, and 6 percent).

The first thing to note is that all of the different rate curves collapse to $10,000 at the end (you get your face value back). From a price point of view, bonds get cheaper as rates increase. The current rate environment gives about 4% yield for a high-rated corporate bond and rates are likely to go up. The blue curve shows what happens if they increase steadily to 6% over ten years.”

My problem with the above quote and graphic is that Gary explicitly states that: “high-grade corporate bonds under the current rate environment gives a 4% yield.” However, he creates a graph of a $10,000 face value 10-year bond paying 5%. The problem is, no such high-grade corporate 10-year bond exists.

But what I really don’t understand is how a lower yielding 4% bond rate starts out at $10,800. I guess he is suggesting that the 4% rate would be at a premium at that time to the nonexistent 5% bond that he presented. I also have a problem with the assumption that rates gradually rise to 6%. What happens if interest rates rise much quicker than that? Bond prices can fall sharply if rates rise quickly.

Gary then follows the above up with two graphs with stock and bond calculations at various rates. Once again, the problem is he uses 10-year bond rates of 4%, 5% and 6%. Unfortunately, no high quality 10-year bonds offering those rates exist today. If they did, I would better accept his argument, but since they don’t, I don’t.

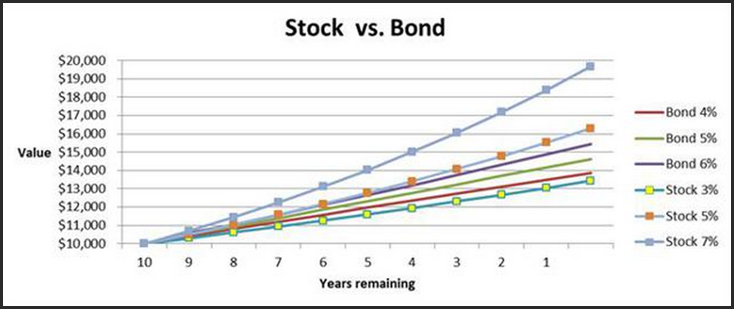

“Stocks versus Bonds

The next figure shows the value of $10,000 invested with ten-year bond rates at 4%, 5%, and 6%. It also shows the total value of $10,000 worth of DGI stock invested in a 3% dividend yielding company, which grows its dividend and its stock price at 3%, 5%, and 7% rates. These correspond to a range of total dividend growth of factors of 1.8 to 3.9, and growth rates of dividend of 6%, 10%, and 14%. Neither of the investments are reinvested.”

Gary’s accompanying graph:

Once again, the biggest problem I have with the above graph is that high-quality 10-year bonds that are paying 4%, 5%, or 6% are not available today. The best rate that I see on a 10-year corporate bond of any quality is an A rated corporate which only offers a yield of 3.52%. As I will discuss later, if I could in fact find quality bonds of reasonable maturities with yields of at least 5%, but preferably higher, I might to an extent buy into Gary’s argument.

But unfortunately for Gary and the rest of us, rates like that are simply not available today. Consequently, bonds do not offer any protection against inflation risk, and that is a real risk. Moreover, even when yields were much higher, they still didn’t fight inflation, but they at least generated a high enough level of current income that they made sense to include in a balanced portfolio of stocks and bonds. I am not anti-bonds, but I am anti-bonds when rates are as low as they are today as evidenced by the following table courtesy of ValuBond:

Additionally, Gary attempts to support his argument by presenting his views of a Monte Carlo simulation by Wade Pfau and the glide path. However, I believe that Gary dramatically oversimplifies what Wade Pfau’s work was really about. For example, Gary offers what I interpret as a moderately cynical statement about investors and stock picking. However, the Monte Carlo simulations that Wade Pfau and others developed focus significantly on stock valuations as the following excerpt indicates:

“This study explores the interaction of two research threads relating to asset allocation in retirement: whether the optimal equity glide path should rise or fall throughout retirement (and at what pace those changes should occur), and/or whether retirement asset allocation should move up and down dynamically in response to stock market valuation extremes.”

Additionally, and perhaps even ironically, Wade Pfau and Associates indicated that glide paths performed better with stocks and treasury bills and not bonds, as the following two excerpts from the Journal of Financial Planning, with bold emphasis added by me:

“It is notable that in these high-valuation environments glide paths and dynamic valuation-based allocations tend to perform better with stocks and Treasury bills (or similar cash substitutes) and not bonds. The potential bond volatility with interest rate risk can be dangerous and possibly lead to lower SAFEMAX outcomes when equity valuations are already so elevated (even if the bonds still have better long-term returns).”

“This suggests that financial planners guiding clients on retirement income in today’s environment should focus on managing interest rate risk, even at the cost of lower bond portfolio returns. It is not necessarily fatal to a retirement plan to hold high allocations of short-term bonds in the face of low interest rates, because its primary purpose is to defend against equity declines and be available to reinvest for better equity returns, not to be a return driver itself.”

Now, I will admit that the link to the above article allegedly supports the general idea of including fixed income in all portfolios. Nevertheless, my main point is that there is much more to the glide path scenario than Gary would like us to believe with his glide path graph. The reader is free to review the entire article, as I have, to gain a deeper insight into what I’m discussing.

“Wade Pfau and the Glide Path

Dr. Pfau has done a lot of Monte Carlo simulations of various retirement outcomes (oh, goody, Monte Carlos; my engineer brain starts to get excited). Seriously, it's a good and valid tool. He looked at various ratios of stocks and bonds in an investment portfolio (and look, please, cash is just a very low return bond as far as this analysis is concerned). I know I can pick stocks better than averages (oh wait, most investors can't). Trust me, all of these arguments are minor details in the overall analysis. What he showed is that the best chance of having your money last through retirement is to follow a "glide path" (see the figure below, my interpretation of the concept). And yes it's a V rather than a U because I didn't bother to make the allocation nonlinear.”

Summary and Conclusion

I want it to be crystal clear that in the general sense I am not anti-bonds. When and if bonds make economic sense, as they have in the past, I would be enthusiastic about including them in retirement portfolios, as I have been in the past. However, I do not believe that bonds make economic sense at today’s low level of interest rates. The yields they offer are simply not high enough to overcome the inflation risk (and tax risk if in taxable accounts) that is highly certain to destroy their true future purchasing power.

Yes, it is possible that stocks might also do poorly. But in my opinion the reality in the current interest rate environment is that I can find fairly valued, high quality dividend growth stocks that offer higher current yields than I can find on high-quality bonds, and they at least provide the potential to fight inflation. I would rather take the risk that I may or may not beat inflation with a temporary overweight in stocks, over the risk of being virtually guaranteed that I won’t.

But my bottom-line point is that retired investors should not buy bonds until they once again provide the traditional yield advantage over stocks that they have in the past. When that happens, and I believe that it will, but I don’t know when, bonds will once again become a viable investment alternative.

But until that happens, I don’t believe it makes sense to invest in low yielding bonds unless you keep your maturities ridiculously short. Unfortunately, if you do that, there is no return of any kind available at all. If you cannot stomach temporarily having all your money in dividend stocks, then put it in cash, not bonds.

Disclosure: Long GE,EMR,KO,CLX,DE,PEP,JNJ at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.