According to this CNBC article, “twenty percent of the S&P 500 have reduced their share count by 4% year-over-year in each of the last five five quarters” with the trend continuing in the second quarter. There are plenty of large buyback programs being undertaken by large-cap companies such as Intel and McDonalds and in that CNBC article they also mention Apple as a company joining the “buy back monsters” such as IBM and Exxon Mobile. However, for the market as a whole, is this time really all that different?

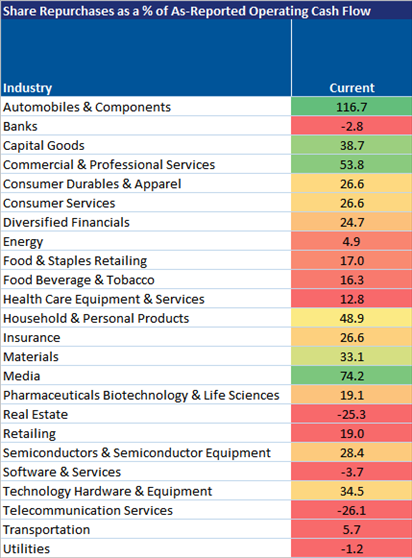

If we break out the data by industry group, 2014 certainly was a big year for share buybacks. However, 2007 was a bigger anomaly compared to the trends of the last decade. In the table below, we show share repurchases as a percent of operating cash flow for each industry group, using equally weighted company data. The table is conditionally formatted by row.

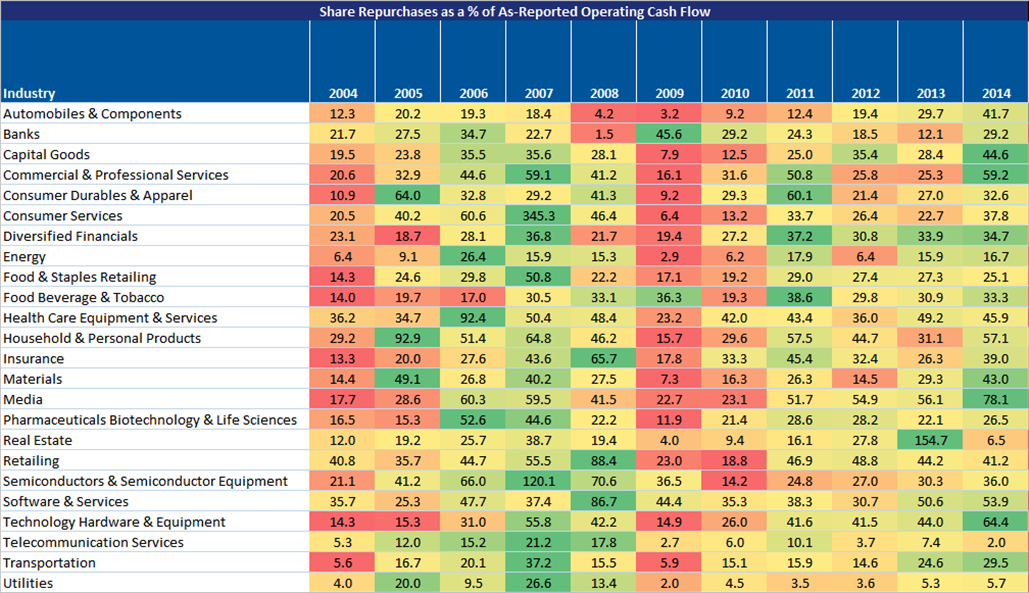

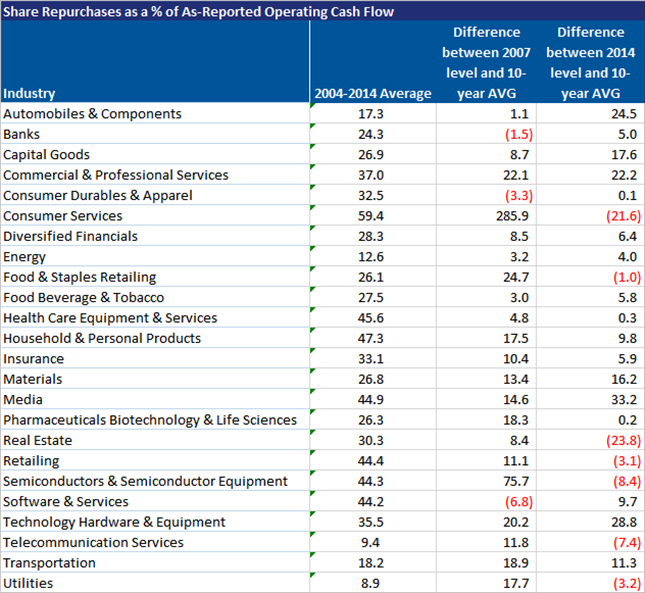

Over the past decade, share buybacks have been a consistent characteristic of the US stock market. The 10-year average, from 2004-2014, of share repurchases as a % of OCF for an industry ranges from 8.9%-59.4%. Half of the industries have a 10-year average of spending at least 30% of their OCF on share repurchases.

In 2007, companies were buying back stock using a much larger percentage of their operating cash flow than they did in 2014. For example, 14 industries bought back at least 10% more than their 10-year average percentage of OCF. In 2007, only 7 industries bought back more than 10% of their 10-year average rate. Similarly, only three industries in 2007 bought back less than their 10-year average rate while in 2014 seven industries bought back less than their 10-year rate. Overall, more companies in 2014 were buying back an “average” amount of shares than than in 2007.

2015 may end surprassing the buy back frenzy of 2007. However, as of now, current levels in 2015 are well below 2007 and 2014 levels.