According to the FT, S&P 500 earnings are on track to decline by about 2.6% year-over-year which is actually about 2% better than what analysts were expecting at the end of June. So this is turning out to be a better earnings season than must expected? Not really. This is just a continuation of the game where consensus expectations are moved lower and lower until companies can, you guessed it, “surprise” to the upside. And its not just for this quarter that growth expectations are taken lower, this happens for growth expectations multiple years out. This game is one experienced investors are fully aware of but it is interesting to see how estimates have been moved lower recently. We can see this change by looking at growth expectations breadth.

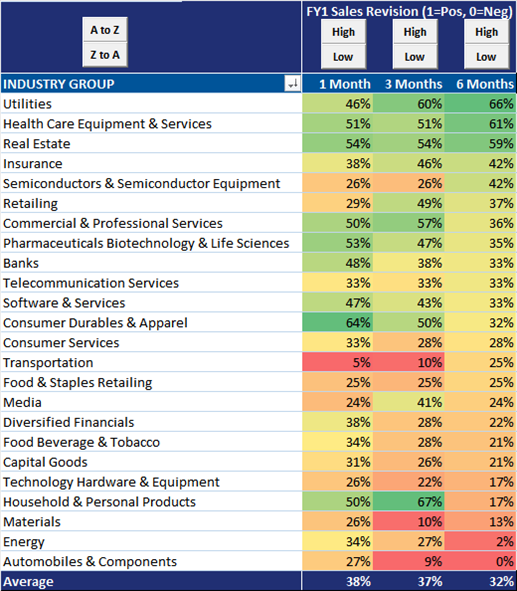

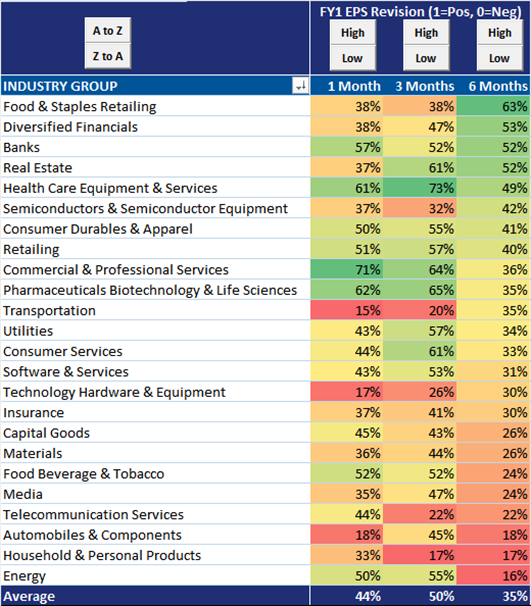

Over two thirds of all US companies have had FY1 sales estimates lowered over the past six months. And more than 60% of all US stocks have had FY1 sales estimates decline over the past one and three months. Similarly, 65% of all US stocks have had its FY1 EPS estimate revised lower over the past six months. And at least half of all stocks have had its FY1 estimate lowered over the past one and three months.

FY1 Sales Revisions Breadth For US Stocks By Industry

FY1 EPS Revisions Breadth For US Stocks By Industry

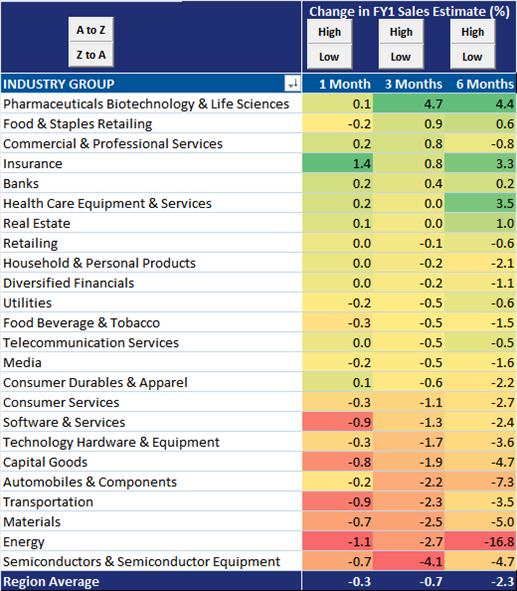

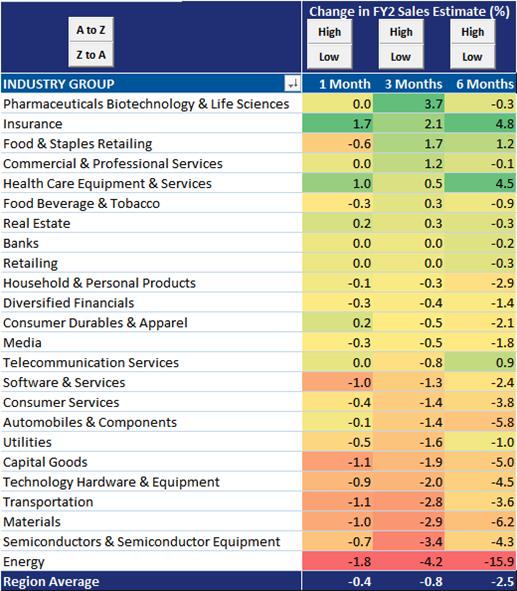

On average, FY1 sales estimates have fallen by -0.7% over the past three months and -2.3% over the past six months. For FY2 sales estimates, on average, it has fallen by -0.8% over the past three months and -2.5% over the past six months.

Change In FY1 Sales Estimates For US Stocks By Industry

Change In FY2 Sales Estimates For US Stocks By Industry

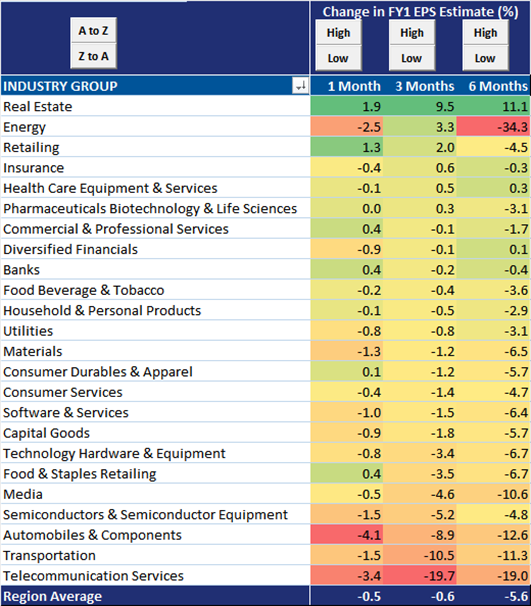

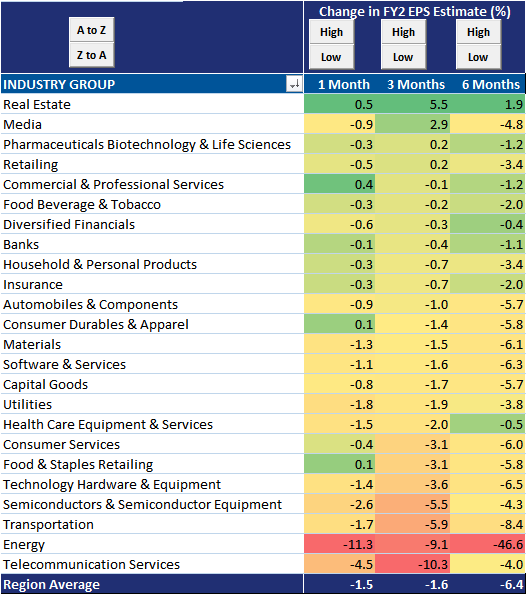

EPS estimates, as usually, have been hit harder. 18 out of the 24 industries have seen declines over the past three months for FY1 to the tune on average of -0.6%. 20 out of the 24 industries have seen declines over the past three months for FY2 by an average of -1.6%. The decline over the past six months for FY1 EPS estimates is 5.6% while the decline over the past six months for FY2 EPS is even greater at -6.4%.

Change In FY1 EPS Estimates For US Stocks By Industry

Change In FY2 EPS Estimates For US Stocks By Industry

What would really be surprising for investors is when these companies start to beat growth expectations that have been steadily revised HIGHER. But most likely companies will continue to under-promise to (barely) over-deliver.