“Life is a series of natural and spontaneous changes. Don’t resist them – that only creates sorrow. Let reality be reality. Let things flow naturally forward in whatever way they like.”

Lao Tzu, 5th-6th Century BC Philosopher, founder of Taoism

Greece is much in the headlines again. As we stated in our Spring 2013 letter, “The European debt crisis will not be over until either: 1) the debt goes away (read: default or substantial inflation) or 2) these governments start producing actual surpluses with which to pay the debt down.” So far, every subsequent deal has failed to produce either of these two scenarios, and so each time news media builds up another weekend summit or referendum, the running joke around here is, “Don’t worry, it will all be resolved this weekend.”

As disturbing as it may be for Europeans, for American investors we believe this circus is largely a sideshow because the prospect of a “Grexit” (Greek exit from the Euro) is not nearly as scary as it was a few years ago. Today, the European Central Bank (ECB) stands ready to print money and buy bonds to keep a “Grexit” from turning into a “Portu/Ital/Irie/Spanexit”. While a “Grexit” would rattle markets and disturb the European financial system, it would also sow the seeds for eventual recovery by freeing Greece from a crushing debt burden and allowing it to devalue its currency and close its perennial trade deficit. What happens to Greece does matter, but considering it no longer appears to be catastrophically important, and because the outcome is near impossible to predict even if one read every single article on the subject, it is best to “let things flow naturally forward in whatever way they like” and concentrate on other matters. There are, after all, other clouds on the horizon.

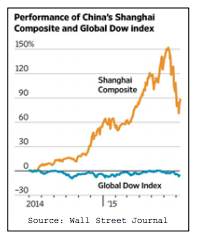

We believe the potentially larger issue is the health of the Chinese economy. The Chinese stock market recently suffered a severe crash, with the Shanghai composite down 30% from its recent highs, wiping away more than $3 trillion in market value. We aren’t worried about the Chinese stock market for its own sake (we own no Chinese equities), but we are worried about what it says about their economy – which is inextricably linked with our own and the rest of the globe’s. No, the collapse of the Chinese stock market doesn’t directly indicate their economy is collapsing, like it might in the U.S.1 ; the Chinese market has more of a casino element than do markets of more capitalistically experienced countries. Rather, what makes us worry about the Chinese economy is the authorities’ response to the crash2 . Consider all of the measures unleashed by the Chinese government in an attempt to stem the declines:

• June 29th (Shanghai Composite 21.7% off high): Regulations are changed to allow pension funds to buy and hold more stock;

• July 1st (Shanghai Composite 21.7% off high): more stock is allowed to be bought with borrowed money on margin (a reversal from a crackdown on margin buying earlier this year); stock exchange transaction fees are reduced 30%;

• July 3rd (Shanghai Composite 28.8% off high): China’s state-owned futures exchange calls up brokers to tell them to not short the market;

• July 4th (market closed): 21 brokers, no doubt encouraged by officials, put $19 billion into a “buy stocks fund”, vowing they will not sell; many brokers stop lending out stock needed to take short positions;

• July 5th (market closed): China’s central bank loans money to brokers so they may in turn make more loans to would-be buyers; IPOs are suspended to restrict the supply of new stocks;

• July 6th (Shanghai Composite 27.1% off high): State-owned banks and China’s sovereign wealth fund pledge they will buy, buy, buy;

• July 7th (Shanghai Composite 28.0% off high): Trading halted in more than 50% of exchange listed stocks (more than 1,300 companies!);

• July 8th (Shanghai Composite 32.3% off high): Company executives, directors and those who own more than a 5% stake are banned from selling stock for six months; China’s securities regulator says it will buy small cap stocks; regulations are changed to allow insurance companies to buy and hold more stock;

• July 9th (Shanghai Composite 28.4% off high): Chinese executives receive directives that they must either: 1) make major shareholders buy more stock, 2) buy back their own stock, 3) make senior employees buy stock or 4) incentivize regular employees to buy stock – records will be kept regarding who buys and how much; regulations are changed to allow banks to buy and hold more stocks; margin requirements are reduced;

• July 10th (Shanghai Composite 25.1% off high): China’s central bank says it will print undisclosed quantities of money and indirectly lend it to those willing to buy stocks.

The Chinese authorities’ recent stock market antics have just demonstrated that they are unwilling to let markets send all-important warning signals, possibly adding to any future calamity. The whole point of having a free market system is that it (usually) produces better outcomes that cannot be achieved by a command economy. Markets provide the invaluable service of signaling when economic plans have gone astray; two of these signals are declining stock prices and defaulting loans. When authorities prevent these signals from being sent, they also prevent the economy from changing course and solving the underlying problems. An unwillingness to endure negative market outcomes often only delays and worsens the inevitable reckoning. Those who seek to command the economy may have some initial success, but ultimately end up like King Canute, issuing commands to the unheeding waves as they continue to wash ashore.

We have just seen how the authorities react to a public market setback: by refusing to let nature take its course. How might they react (or have been reacting?) to setbacks in the much larger and more important banking system? It is very difficult to command that the public stock market not go down (as the authorities are now discovering3 ), but it’s relatively easy to command that the insolvent not default: simply instruct a state-owned enterprise to issue a new loan or buy an unwanted asset at an inflated price. These actions could easily be kept out of the news due to the private nature of bank transactions.

But there are limits to command and control: authorities can successfully command that a business not be allowed to default in the present by giving it more loans, but they cannot command that the business pay everything back if it has no money or way of making it (note the parallels to Greece). It is not hard to understand how continuing to lend money to a failing business in hopes that it turns around often leads to an eventual greater loss.

We worry that the Chinese banking system might be in some variant of the situation described above for the following reasons:

• The Chinese financial system has generated a gargantuan amount of debt. According to the McKinsey Global Institute, the Chinese economy has added $20.8 trillion of new debt since 2007, which represents more than one-third of global growth in debt. Loans made quickly are often loans made poorly, especially when the creditors have just experienced a long period of uninterrupted growth and believe that the authorities can prevent recessions.

• The relative level of total debt to (official) GDP is also quite high at 282%. Supposedly we are all becoming debtors to China, but the comparative U.S. figure is only 269% (Greece clocks in at 317%). Don’t even ask about Japan (ok, it’s 400%).

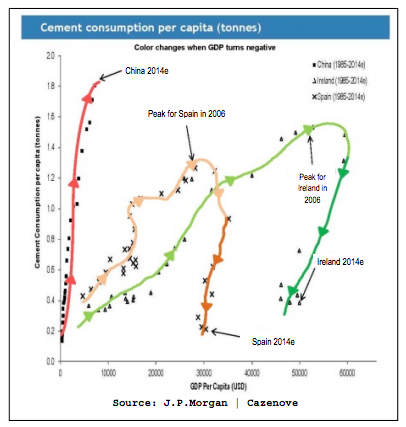

• China is undertaking the greatest building boom in the history of humanity, consuming some 50% of the world’s aluminum, iron ore, and steel while only accounting for 15% of the world’s GDP. And the building boom was state-directed, not market-directed. What usually follows booms?

• There continues to be a severe lack of imagination as to how bad a China contraction could be. A bleak Chinese growth scenario would not be missing the official seven percent GDP growth target by a few points, rather, it would look more like other emerging market recessions: with negative two, negative five, or negative ten percent growth.

In sum, a contracting Chinese economy, potentially driven by a banking crisis, really is something to worry about...especially because those worries are not (yet) widespread. One area where the fear is indeed already widespread is China-linked commodity stocks, many of which are down more than 50% and are starting to look interesting. Trades made with trembling hands often offer the greatest rewards.

Do U.S. stocks seem priced to withstand a weak Chinese economy or are they priced for perfection, and therefore, fragile? We see the following signs of frothiness which would suggest the latter:

• May saw a record $243 billion in U.S. mergers and acquisitions, surpassing the previous records set in May 2007 and January 2000. Each occurred shortly before credit and equity market peaks.

• Deals are not only numerous, but expensive. Acquisition valuations are hitting 20-year highs as indicated by the red line at right.

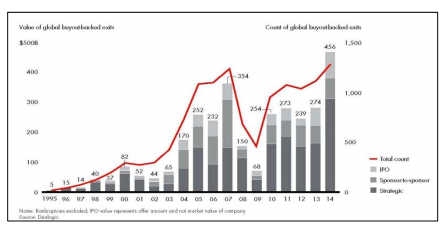

• Private equity used the strong markets to cash out at a record pace; last year the number and value of private-equity-related IPOs and sales to strategic buyers were the greatest of all time, as seen on the next page.

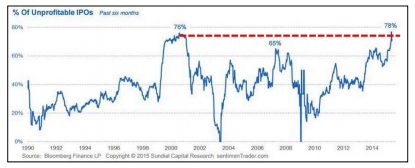

• We recently experienced a six-month period with the highest proportion of unprofitable IPOs ever, just surpassing the previous peak in 2000.

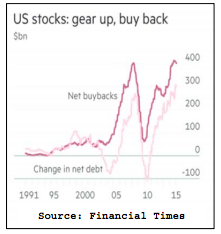

• Corporations are issuing debt at a record pace in order to buy back stock. Historically managers have not proven to be the best market-timers. They bought back gobs of stock in 2007 and very little in 2009 when the same stocks were half the price. Today, it is very much in vogue for corporate managers to fancy themselves “great capital allocators”, wisely buying back their “undervalued” stock. A market correction might subsequently prove them to rather have been “great capital alligators”...chomping away at capital and reducing shareholder returns.

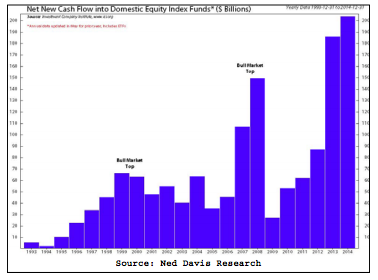

• Money is gushing into equity index funds. Previous peak inflows occurred around the 2000 and 2007 stock market tops. Mutual funds hold very little cash (3% of fund assets – an all-time low) as they struggle to keep up.

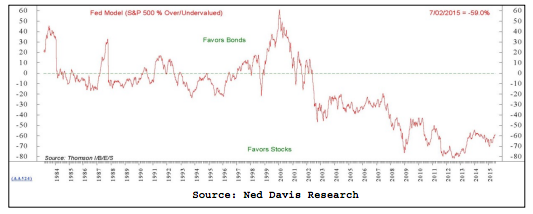

With conditions increasingly frothy and stock market valuation well above historical averages, we have incorporated some defensive positioning in portfolios, with cash levels generally running 20% to 30% this year. Why not more? Well, there is another side to the stock market story...one that we have been too slow to sufficiently appreciate...and that is the relentless pressure on stocks from low interest rates...a relentless upward pressure. To put the dilemma succinctly, stocks look expensive relative to the stocks of yesterday, but they look cheap relative to the bonds of today. We have shown a number of charts bearish for stocks. Here is a bullish one, the “Fed Model”, which compares the yield on 10-year Treasuries to the forward earnings yield of the S&P 500. It suggests stocks are significantly undervalued...and have been so for years.

If rates remain low, they will continue to pressure stock prices to be expensive, but deservedly so. Comparing stocks to previous valuations isn’t very worthwhile if the conditions that prevailed previously don’t return. The old paradigm was that interest rates couldn’t stay low for extended periods...previous conditions (i.e. higher rates) would return, because the hands of central bankers would be forced by inflation. This seems to be less and less the case. With commodity prices from oil, to metals, to agricultural grains still plummeting, the signs of incipient inflation seem absent. Any financial turmoil in Europe or China would engender forces further depressing inflation. Just recently, before a single rate hike, the IMF warned the Fed against raising rates in 2015. Our thematically astute neighbors across the street (PIMCO) have embraced the view that, even in the event of a few Fed hikes, rates are likely to remain historically low for an extended period.

Discerning readers will respond, “They can’t keep rates low by printing money forever!” and we might agree...but it would appear they can continue long enough that it could seem like forever. Ten years? Twenty years? As noted in previous letters, we are in unchartered monetary territory. The blunt truth of the matter is that money printing can patch over pretty much every economic problem except two: inflation and its even darker cousin, a loss of faith in paper money4 . We expect authorities to use this tool until one of these evil spirits emerges...but at the moment, they are nowhere in sight.

Despite the real estate devoted to macro concerns in this letter, we spend the great majority of our time picking stocks. We recently initiated and then sold a position in Deere & Co. in a much shorter time period than is typical. While we rarely like to take short-term gains, in this case we felt the stock price had gotten in front of itself, especially given what may prove to be an extremely tough agricultural cycle. While we have a long established investment process to which we continue to adhere, in this specific case our research indicated a sale was prudent and, taking the advice of Lao Tzo, we decided resistance would only create sorrow. We seek to reestablish the position at a lower price if concerns of a more extended downturn become expected and priced in.

It is with these concerns in mind that we try to navigate today’s turbulent economic waters. We seek to be aware of the risks, without being paralyzed by them.

We thank our investors for maintaining an even keel during the recent turmoil.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Even U.S. stock market crashes are not always related to the real economy.

2 After all, in aggregate the Chinese market is still up substantially on the year.

3 The measures seem to have worked for now as the Shanghai Index found a (temporary) bottom on July 8th.

4 The potential (even if small) for these two issues is part of the reason why we continue to maintain a gold miner position, though miners are looking better and better as operating businesses as well.

© Knightsbridge Asset Management, LLC