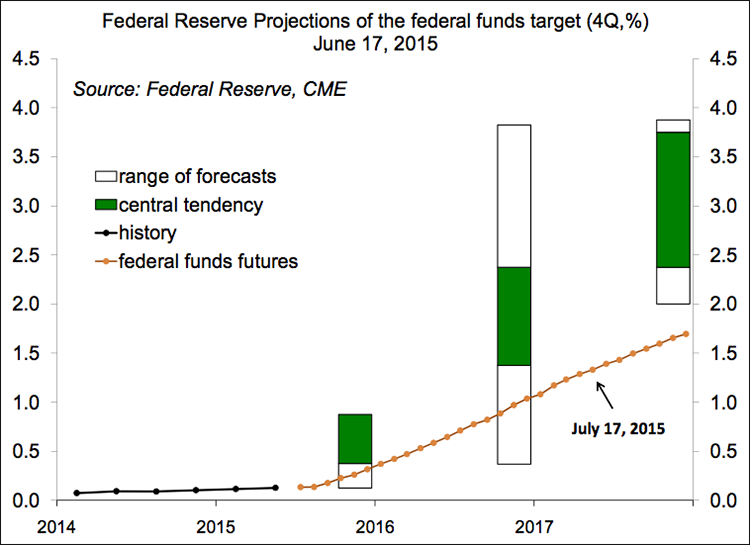

In her monetary policy testimony to Congress, Fed Chair Janet Yellen made it clear that the central bank remains on track to begin raising short-term interest rates later this year. However, she gave herself an out, indicating that Federal Reserve officials’ projections of the federal funds rate are “based on the anticipated path of the economy, not statements of intent to raise rates at any particular time.” Moreover, she continued to imply that people should stop worrying about the timing of the initial move and focus on the projected path over the next couple of years, which she expects to be gradual. None of this has helped ease the market’s anxieties about the Fed’s timing.

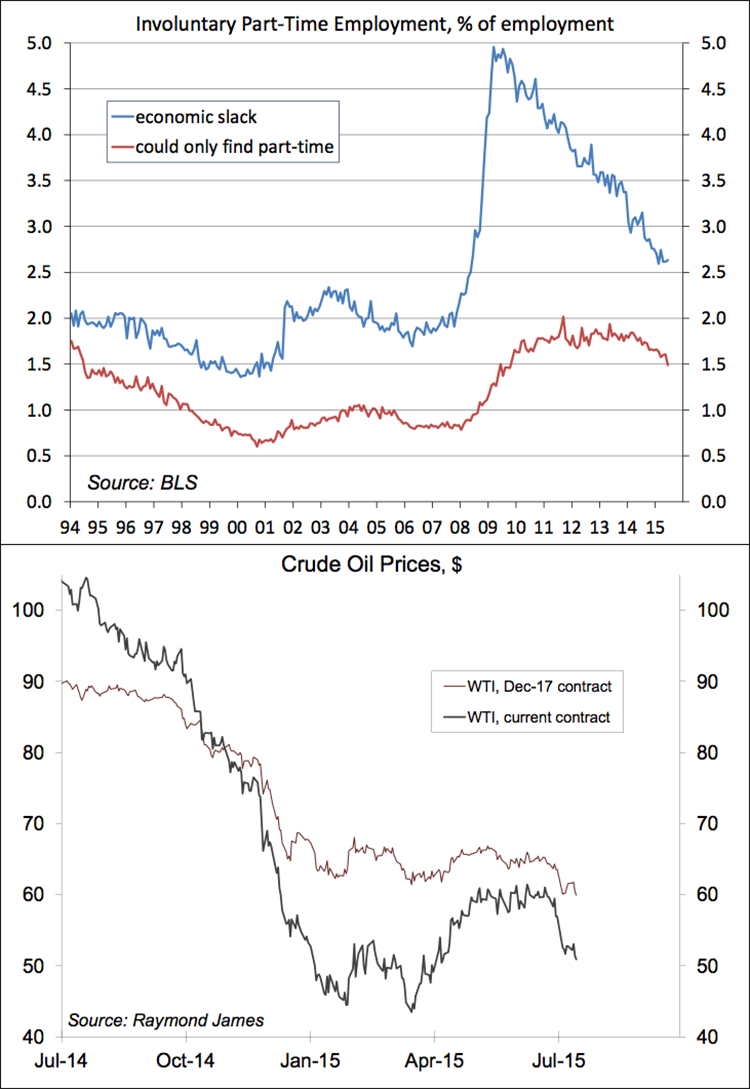

The unemployment rate hit 5.3% in June, but that overstates the improvement in the job market. Fed Chair Yellen has highlighted a number of gauges, including hiring and quit rates. The number of people working involuntarily part-time has been falling, but is still higher than normal. Yellen: “while labor market conditions have improved substantially, they are, in the FOMC's judgment, not yet consistent with maximum employment.”

The inflation outlook is an important factor in the Fed’s decision to begin raising rates. For some time, policymakers have indicated that they need to be“reasonably confident” that inflation will move toward the Fed’s 2% goal. Inflation was pushed lower in the first half of the year due to lower oil prices and a stronger dollar. After falling sharply into the early part of the year, the dollar has been essentially range-bound since mid-March – but that could change. In the short term, exchange rates largely reflect central bank policies. The Fed is considering when to tighten. The ECB has undertaken quantitative easing and Mario Draghi, the central bank’s president, has signaled no intention of curtailing asset purchase plans (which are set to continue to September 2016). The Bank of Canada lowered rates last week for the second time this year. The Fed anticipates that the decline in oil prices will run its course, relieving downward pressure on consumer price inflation in the months ahead. However, crude oil prices have turned down again and longer-term futures contracts (which, granted, aren’t a great predictor of spot prices) point to a sustained period of low oil prices. Low inflation may last longer than the Fed expects.

The federal funds futures reflect a lower rate trajectory than what the Fed was projecting in June. However, the futures reflect some chance that the Fed will have to reverse course and lower rates after the initial increase. That risk is not included in the Fed’s projections. Still, financial markets seem to carry some doubt about the Fed’s willingness to begin raising rates.

Looking ahead, the financial markets are expected to remain sensitive to economic reports, especially those concerning the job market and inflation. On July 31, the Bureau of Labor Statistics will release the Employment Cost Index for 2Q15. The first quarter figure suggested that labor compensation might be picking up, reflecting budding inflation pressures and reduced labor market slack. The 2Q15 figure should suggest otherwise.