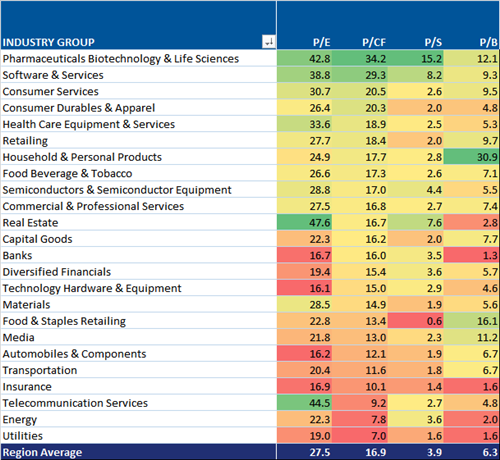

The average price to cash flow multiple for a US equity is currently 16.9x. However, as is always the case in a diversified market, the range of valuation multiples varies quite a bit if we break out companies by industry group. The cheapest industry group is utilities currently trading at 7x cash flow. Only two other industries, energy and telecom, are trading below 10x cash flow. On the other end of the spectrum, four companies are trading above 20x cash flow and one, pharma, biotech and life sciences, are trading above 30x.

As-Reported Valuations By Industry Group

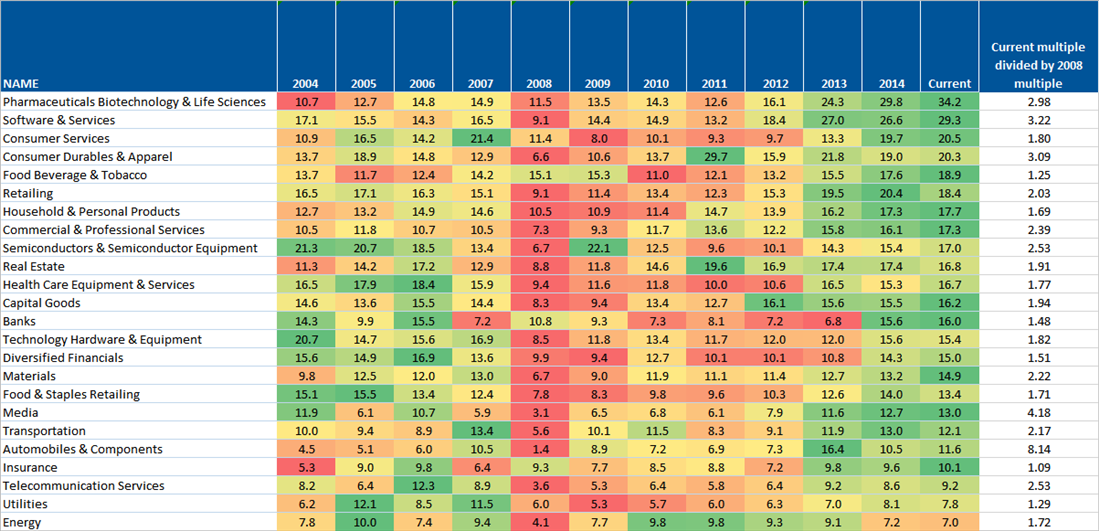

It is interesting to see just how far multiples have expanded since the financial crisis. Since 2008, price to cash flow multiples are at least 25% higher (food beverage and tobacco actually didn’t make a valuation low until 2010) and is has many as 8x higher in the case of automobile and components. On average, valuation multiples have increased by 135% since 2008. 11 out of the 24 industries have seen multiples expand by at least 100% since 2008 and four industries have seen multiples expand by at least 200%.

Price to Cash Flow Valuations By Year and By Industry Group

Lastly, it is worth remembering that when an entire industry gets below 10x cash flow (5x cash flow for less growth oriented industries like telecom and utilities) it tends to be a screaming buy. In 2008, only four out of the 24 industries never reached 10x cash flow and eventually two of those industries, consumer services and banks, broke below 10x cash flow in 2009.