When my wife and I became a couple, my finances were a mess. Despite working 25 hours weekly during school and holding two jobs each summer, I barely kept pace with my college tuition. I tried to earn a little spending money by running a beverage service in our dormitory, but the profits sometimes disappeared at the poker table on Saturday evening.

My wife’s accounts were not much better, but she always seemed to have some spare cash. She was kind enough to share a little of it with me when needed, and the microfinance accumulated to a tidy sum. I joke with her that I proposed marriage so that we could form a fiscal union that would provide me with immediate debt relief.

The commingling of finances can be beneficial, but also complicated, to all involved. Each party to the cooperation must exhibit discipline so as not to impose on others. Clear principles should separate what each party can do independently and what each must give over to the collective. And if something goes amiss, a clearly defined resolution process should come into play.

The Greek crisis has illustrated that these three pillars are not fully formed in the eurozone. The desperate negotiations this past weekend in Brussels seemed reminiscent of “Lehman weekend” in 2008. There was a desire to preserve a system amid warnings about the moral hazard of supporting a system member that had gone astray.

The European Union (EU) and the European Central Bank (ECB) worked hard to find a way to hold things together. Wolfgang Schäuble, the German finance minister, pressed for the Greeks to be held accountable and seemed comfortable with the country’s potential exit from the euro. The interplay among parties was, at times, rancorous.

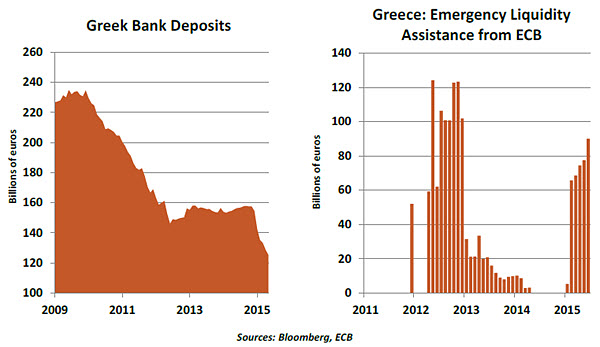

Ultimately, the cash squeeze Greece faced and the fragile state of its banking system forced it to capitulate and pass measures far harsher than the ones rejected by referendum a week earlier. The adoption of reform secured continued support from the ECB and bridge financing from the EU to make upcoming payments. Negotiations on a longer-term solution will begin shortly.

This represents progress, but it is not clear when the Greek economy will return to growth. The country’s weak banks and the impact of tax increases and spending cuts will suppress economic activity in the short term. If the economy continues to contract, it will stress both the budget and the patience of parties to the resolution.

This represents progress, but it is not clear when the Greek economy will return to growth. The country’s weak banks and the impact of tax increases and spending cuts will suppress economic activity in the short term. If the economy continues to contract, it will stress both the budget and the patience of parties to the resolution.

Critics of the eurozone observed at its founding that monetary union would be challenged without other elements of policy coordination. While the Stability and Growth pact was intended to prevent fiscal excesses, its dictates have not been strictly enforced, and Greece was allowed to live well beyond its means. Since government debt in the eurozone is not mutualized, supporting this imbalance has required substantial loans from European institutions to Greece.

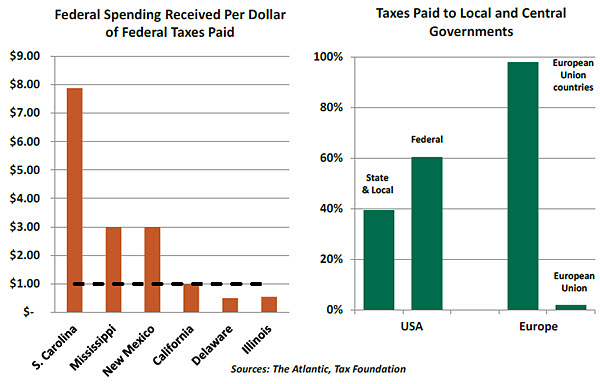

It is not uncommon for states that are part of true economic unions to facilitate subsidies from stronger to weaker partners. The United Kingdom has a formulaic system of transfer payments among its members and administers a number of public programs (including health, education and defense) centrally. Similarly, the United States handles a wide range of policies and programs at the federal level, and tax revenue from some states is redistributed to others.

Individual states in the United States do borrow to fund expenditures they are responsible for, but at a much lower level than is the case in Europe. American law does not presently allow states to declare bankruptcy; should local difficulty prove intractable, the federal government would almost certainly step in with support.

Converting loans to subsidies would be very helpful for Greece, but this is not allowed by the Maastricht Treaty that founded the euro. The International Monetary Fund (IMF) will not participate in a new aid package without such concessions, so there is a bit of a Catch-22 awaiting those tasked with finding a long-term solution.

Mario Draghi, ECB president, observed this week that Europe is an imperfect union. Flaws and gaps in treaties must be filled by trust among members. Having failed to follow the dictates of past bailout programs, the Greeks lost the trust of their eurozone partners and will now be subject to very close fiscal oversight.

Mario Draghi, ECB president, observed this week that Europe is an imperfect union. Flaws and gaps in treaties must be filled by trust among members. Having failed to follow the dictates of past bailout programs, the Greeks lost the trust of their eurozone partners and will now be subject to very close fiscal oversight.

Perhaps this is a backdoor form of fiscal consolidation, which can serve as a model for other countries that reach a critical point. There is a broad community of countries with high levels of debt and slow economic growth, although none to the extent of Greece. But sovereign nations are understandably reluctant to give their budgets over to foreign bureaucrats, and if external prescriptions fail, the potential for local unrest is very high.

If the programs are successful, though, they could end up adding strength to the union. Shortly after we were married, my wife faced the challenge of paying off her student loans. I prescribed austerity measures (no more restaurants), which were initially unpopular. But the beneficial effect of long-term solvency stabilized our relationship. Here’s hoping that Europe achieves the same outcome.

Seeking Respect for the RMB

China’s economy has grown immensely over the last generation; real gross domestic product (GDP) has doubled five times in the last 30 years. But even though China is undeniably a burgeoning power, it worries periodically about not getting the respect it feels it deserves. Whether this is due to actual disrespect or official paranoia is up for debate, but Beijing’s push to establish itself as a financial force is undeniable.

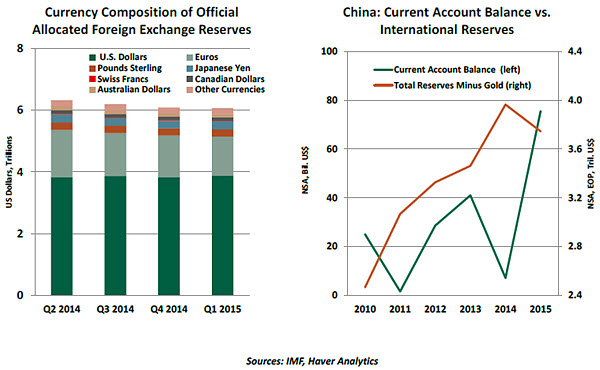

In the past year, officials have launched numerous measures aimed at challenging the dominance of U.S.- and European-led institutions and establishing itself as a presence on the world’s stage. Another key element of this “respect campaign” would be having the Chinese renminbi (RMB) included as a reserve currency in the IMF’s Special Drawing Rights (SDR) basket. The basket, which currently includes the U. S. dollar, Japanese yen, British pound sterling and the euro, could be expanded later this year.

It is important to note that being a reserve currency for SDR purposes is not the same as being a reserve currency as far as the market is concerned. SDRs are essentially vouchers that can theoretically be exchanged for actual currencies. Even if the RMB is deemed “freely useable” and gains admission to the basket (and this is far from certain), it does not mean much in practice unless a market for SDRs crops up (nearly inconceivable).

What does the rising profile of the RMB mean for the U.S. dollar? The succinct answer is: not much in the short term. The United States boasts superior financial depth, and the dollar is the dominant currency for invoicing, foreign currency debt, official reserves and currency pegs. It also holds the distinction of serving as the basis for trading in petroleum.

The true test of a currency aspiring to greater international status is adoption by markets. For that to happen, a number of benchmarks must be met. The host country should have deep and open capital markets, and the currency should be widely used in trade and investment. The RMB is already the second most-used currency in trade finance, thanks in part to Chinese companies offering discounts when transactions are settled in RMB.

The Chinese have also made progress in opening their capital account with measures such as the Shanghai-Hong Kong Stock Connect, the Qualified Foreign Institutional Investor program and the opening of domestic bond markets. But the process is heavily regulated and incomplete. And in comparison with other large markets, China’s is still effectively closed. Further, its current account surplus and massive holdings of international reserves will make it difficult for other countries to accumulate RMB assets in significant quantities.

The Chinese have also made progress in opening their capital account with measures such as the Shanghai-Hong Kong Stock Connect, the Qualified Foreign Institutional Investor program and the opening of domestic bond markets. But the process is heavily regulated and incomplete. And in comparison with other large markets, China’s is still effectively closed. Further, its current account surplus and massive holdings of international reserves will make it difficult for other countries to accumulate RMB assets in significant quantities.

Perhaps the biggest obstacle to widespread adoption of the RMB is a lack of confidence in the macroeconomic, political and policy environment in China. Beijing has asserted a commitment to liberalize markets, but its heavy-handed approach to the recent equity market correction ceded a lot of accumulated international goodwill on this front.

Governments intervene in markets with some regularity, but the recent Chinese response has been striking in its scope and disregard for international norms. Can investors trust the resolve of Chinese policymakers? Can China trust its economic project enough not to meddle in the face of domestic and/or international volatility? The RMB will never become a true reserve currency until it is allowed to float freely, without being managed by an invisible hand.

The one guarantee in life is that change can and will happen. The British pound yielded to the U.S. dollar in the first half of the last century, and a shift is possible this century. However, the prospects of a near-term shift to the RMB are remote. Hang on to your greenbacks, at least for now.

The Economic Opening of Iran

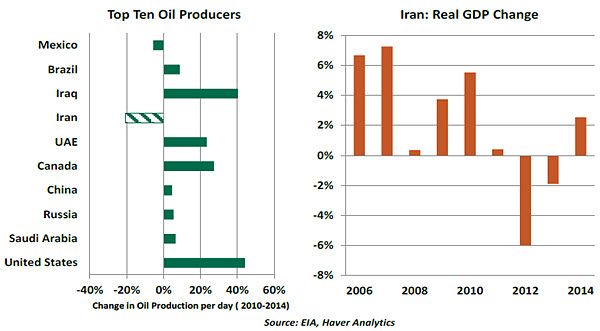

The nuclear deal signed by Iran and six world powers (United States, France, Russia, China, United Kingdom and Germany), when implemented, should have significant and positive economic implications.  Broadly speaking, the impact can be summarized in terms of energy and non-energy aspects. Iran is one of the top 10 oil producers in the world, but sanctions have restricted its production and sale of petroleum. If and when these are lifted, optimists expect oil production to increase by around 800,000 barrels a day.

Broadly speaking, the impact can be summarized in terms of energy and non-energy aspects. Iran is one of the top 10 oil producers in the world, but sanctions have restricted its production and sale of petroleum. If and when these are lifted, optimists expect oil production to increase by around 800,000 barrels a day.

Obsolete technology and a lack of investment will prevent an immediate and rapid increase in oil production. But they do represent an opportunity for foreign firms to sell equipment and advice to Iran. The big players in the industry have been intensifying their calling on Iran, hoping to take advantage of what one analyst called a “candy store” for developers.

While some think this gush of new oil will result in lower prices, the future trajectory of oil prices and production is more complex. Much will depend on the strategic actions of other producers, and the full lifting of sanctions is conditional on the numerous verifications laid out in the agreement. Crude prices were only slightly lower on the week.

Despite a severe slowing of business conditions after sanctions were imposed, Iran’s economy remains among the top 30 in the world. There are about 81 million consumers in Iran with a thirst for consumer products hitherto not freely available. Iran has significant industrial strength and is a leading producer of steel, cement and automobiles. The country has a substantial endowment of hydrocarbons, minerals and human capital. The possibility of selling into Iran or sourcing from Iran represents an important opportunity.

The agreement between Iran and the United States could open promising trade vistas for many parties. While nuclear and strategic issues will be at the center of the negotiations, deeper economic ties might also help keep the peace.

(c) Northern Trust