The National Debt Is Over $18 Trillion, Not $13 Trillion

IN THIS ISSUE:

1. CBO’s Latest 2015 Long-Term Budget Outlook

2. Why is Our National Debt Exploding So Rapidly?

3. Intra-Governmental Debt Counts Toward National Debt

4. Is Government Account Series Debt a Federal Liability? Yes!

5. Bottom Line: National Debt is $18+ Trillion, Not $13, Trillion

Overview

In June, the non-partisan Congressional Budget Office (CBO) released its annual “Long-Term Budget Outlook” which concluded yet again that the trajectory of US federal debt is “unsustainable” and will lead to an unprecedented debt crisis in the years ahead.

After running $1+ trillion annual budget deficits in fiscal years 2009-2012, the deficits have come down significantly in the last few years, to $483 billion in FY2014, down from $1.3 trillion in 2011. However, the CBO warns in its latest report that the debt will start to ratchet significantly higher in a few more years if major changes are not made soon.

The CBO estimates that “debt held by the public” will rise to 78% of Gross Domestic Product by 2025 and103% of GDP by 2040 – assuming its long-term assumptions hold true. Several of those assumptions are dubious in my opinion. The CBO admits as much and offers an alternative fiscal scenario which shows the debt rising to over 100% of GDP much sooner.

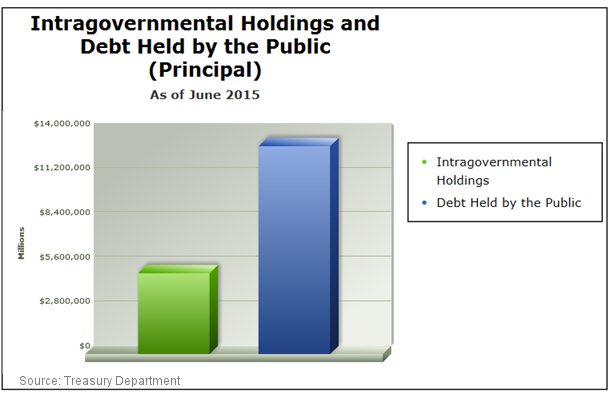

The problem I have always had with the CBO’s debt numbers is that they only consider the debt held by the public, which is currently apprx. $13.1 trillion. The CBO does not include the additional apprx. $5.2 trillion of so-called “intra-governmental debt” which is owed by various governmental agencies including Social Security.

If we add the intra-governmental debt, then our national debt leaps to apprx. $18.3 trillion today, which is actually larger than our GDP of $17.7 trillion at the end of 2014. So our real debt-to-GDP ratio is already above 100%! That’s what we will talk about today. All Americans should understand what follows.

Finally, it is widely agreed that the latest nuclear agreement with Iran is a victory for the Iranians and a dangerous setback for the West, thanks to President Obama. While I don’t have space to address it today, be sure to read the first link in SPECIAL ARTICLES below which points out 16 reasons why this was a very bad deal.

This is just another example that illustrates how our president does not have America’s best interest at heart.

CBO’s Latest 2015 Long-Term Budget Outlook

In its 2015 Long-Term Budget Outlook, the non-partisan Congressional Budget Office warned once again that federal debt is on an unsustainable path. Unless policymakers act soon, the CBO warns that rising debt will jeopardize long-term economic growth, crowd out critical public investments, reduce policymakers’ flexibility to respond to unforeseen events and raise the risk of a fiscal crisis.

The CBO’s Long-Term Budget Outlook includes the following projections, trends and analysis:

- By 2040, federal debt will climb to over 100% of GDP under current law, and could reach 175% of GDP under less optimistic assumptions.

- Rising national debt is the result of a structural imbalance between revenues and spending, fueled primarily by two main drivers: the aging of the population and healthcare cost growth.

- Interest costs on federal debt are projected to grow rapidly: by 2022, they could exceed what the federal government has historically spent on R&D, infrastructure, and education combined, and could exceed them by more than three times by 2050.

- Rising debt will harm our economy and slow the growth of productivity and wages: CBO estimates that it could reduce average real (inflation-adjusted) income per person by as much as $6,000 in 2040.

Significant changes to some combination of spending and tax policies will be required to help get our long-term debt on a sustainable path, and the CBO’s latest report concludes that taking action now to address these trends would provide significant benefits.

As CBO states, “The sooner significant deficit reduction was implemented, the smaller the government’s accumulated debt would be; the smaller the policy changes would need to be to achieve the chosen goal; and the less uncertainty there would be about what policies might be adopted.”

The CBO estimates that federal debt held by the public, which is already at record levels, will climb significantly over the next 25 years. In CBO’s latest projections, debt is expected to climb from 74% of GDP in 2015 to 103% of GDP in 2040 (assuming no changes in current law). But under less optimistic assumptions, CBO projects that debt could soar to a staggering 175% of GDP by 2040.

Debt at 175% of GDP would be unprecedented. Over the past 50 years, debt averaged only 38% of GDP and, as recently as 2007, was as low as 35% of GDP. Since 1790, our debt has never exceeded 100% of GDP, except for a brief time during World War II, after which the debt fell rapidly as a share of GDP.

Absent major reforms, our growing debt will have serious and far-reaching economic consequences. The CBO warns that these levels of debt would:

“…have significant negative consequences for the economy in the long term and would impose significant constraints on future budget policy. The projected amounts of debt would reduce the total amounts of national saving and income in the long term; increase the government’s interest payments, thereby putting more pressure on the rest of the budget; limit lawmakers’ flexibility to respond to unforeseen events; and increase the likelihood of a fiscal crisis.”

Rising debt will slow the growth of the economy by crowding out private and public investment, thereby slowing the growth of productivity and workers’ wages. The CBO estimates that rising debt could reduce average real (inflation-adjusted) income per person by as much as $6,000 in 2040, relative to what it would be if the debt was stabilized at today’s levels. This represents a 7.5% loss in income.

Why is Our National Debt Exploding So Rapidly?

The growth of our debt stems from a fundamental imbalance between spending and revenues. Under current law assumptions, CBO anticipates that federal spending will grow from 20.5% of GDP in 2015 to 25.3% of GDP in 2040. Revenues are also projected to increase during this period, growing from 17.7% of GDP in 2015 to 19.4% in 2040 – but not by nearly enough to match the projected growth of federal spending.

Under less optimistic alternative assumptions, the mismatch between spending and revenues is even more pronounced. CBO projects that spending could soar to 30.4% of GDP in 2040, while revenues grow only slightly and stabilize at 18.1% of GDP.

Much of the growth in total spending will be caused by growing interest costs, which in turn further increases federal debt. Indeed, over the next 25 years, more than half of the growth in federal spending is projected to come from rising interest costs.

Yet those growing costs are avoidable if lawmakers enact policies that put our debt on a sustainable path – not likely, no matter which party rules.

Beyond interest costs, 100% of the growth in non-interest spending (as a percentage of GDP) comes from Social Security and the major healthcare programs, under current law. Healthcare by itself accounts for approximately 70% of this growth. From 2015 to 2040, healthcare spending as a share of the economy is projected to grow by 54%, while Social Security spending is expected to grow by 27%.

There are three primary factors that account for the growth of spending on Social Security and major healthcare programs: aging of the population, the growth of healthcare costs per capita, and the expansion of subsidies provided through the healthcare exchanges created by the Affordable Care Act.

I could go on and on with more statistics on our debt. The bottom line is our debt trajectory is unsustainable and will lead to an unprecedented financial crisis at some point. As noted above, the CBO projections on the national debt include only the debt held by the public. Let’s now turn our attention to why it is so important to also include intra-governmental debt.

Intra-Governmental Debt Counts Toward National Debt

The debt held by the public is apprx. $13.1 trillion, and so-called intra-governmental debt is apprx. $5.2 trillion. The CBO and all other government reporting agencies have long maintained that intra-governmental debt does not count toward the national debt; they maintain that it is “debt we owe ourselves” so it shouldn’t be counted.

To that I say, hogwash!!

Intra-governmental debt is a term used to define the flow of money between the federal government and specific government agencies, the largest being the Social Security Administration. There should be no mistaking this: The federal government has spent (consumed in advance) the difference in Social Security inputs (premiums) vs. outputs (benefits).

Essentially it works like this. The federal government claims all of the Social Security premiums as income and pays out benefits to the recipients. According to the CBO, the government has borrowed and spent the Social Security surplus of $2.15 trillion from 1986 to 2007 as the Baby Boomers have been working and paying in for their eventual retirement.

Applying this surplus as an offset to the annual deficit, it’s reduced the real shortage between federal receipts and spending. Of course, this money robbed from Social Security will have to be paid back at some point, or benefits will have to be cut. But that’s a topic for another time.

Absent the looting of the Social Security surplus, the government would have had to sell $2.15 trillion more in Government Account Series securities (GAS) – Treasury bonds, bills, and notes – from 1986 to 2007 to obtain the necessary funds for that same amount of spending. The only difference is the counterparties– in this case, the government is BOTH.

Is Government Account Series Debt a Federal Liability? Yes!

To say that Government Account Series securities are simply a debt among domestic government agencies that should thus be ignored is naïve. In every case, GAS is a debt that the federal government owes a specific government agency, and that agency then owes its beneficiaries.

It can even be worse than that. For a moment, let’s accept the claim that a benefit due is no different than a bond redeemable. Yes, if we accept that the government is implicitly or explicitly guaranteeing benefits (not just the nominal amount of GAS securities outstanding), then future federal liabilities grow substantially.

According to the respected Peter G. Peterson Foundation, the difference in current and future benefits versus related revenues is $6.6 trillion for Social security and $36.3 trillion for Medicare. To be fair, critics argue that eligibility ages could be raised in the future, benefits cut or payroll taxes raised. But who amongst our incumbent re-elect political system is willing to vote on such measures short of a crisis? Almost no one!

A growing problem: Baby Boomers are beginning to retire. Add in early retirements due to the weak economy, and Social Security beneficiaries climbed by nearly 20% from 2008 to 2009. Revenues (taxes in) have steadily dropped. The CBO is now forecasting a small annual Social Security deficit through 2012. With no surprises, 2017 is the year where benefits and revenues begin to “structurally” separate for the worse. This is a real problem, but a discussion for another time.

Remember, Social Security is just one form of GAS. Veterans, the disabled, military and civilian pensions and retiree health benefits, etc. are all covered by various government agencies that hold GAS securities.Unmistakably, this is part of the public debt; the debt that the federal government is responsible for paying back with tax dollars.

The Treasury itself says so on its website, “The Treasury securities issued to the public and to the Government Trust Funds (Intragovernmental Holdings) then become part of the total debt.” Thus, even the government admits it!

Bottom Line: Government Debt is $18+ Trillion, Not $13 Trillion

For those who attempt to understate the debt problem in the United States, one must embrace the notion that it’s easier to reduce a benefit due than repay monies due on a bond. And there's a degree of truth in this.

For instance, as citizens, we are ultimately subject to the rules the government makes. Foreign creditors, however, may not be so accommodating. Perhaps it will be easier to break a promise over a bond. But still, the intra-governmental debt is held in GAS securities, so this is more untouchable than a benefit.

At the end of the day, intra-government debt among federal agencies is no different than the debt held by the public. These Treasury bonds, notes and bills mature just like debt held by the public and must be repurchased periodically.

The notion that these debt securities should not be counted toward the national debt is simply ridiculous. The idea that these $5+ trillion in federal obligations should not be counted toward the national debt is simply a government smoke-screen to hide the true magnitude of federal debt from us.

Of course intra-governmental debt should be counted in any measurement of our national debt! The national debt is $18.3 trillion, not $13 trillion. And the debt crisis the CBO warns of will come much sooner than 2040. To think that it won’t come before then is wildly optimistic in my opinion.

I rest my case (that I’ve made for over 30 years), yet again. Federal deficit spending is out of control and rises EVERY YEAR, under both parties. If we include both debt held by the public and intra-governmental debt, as we certainly should, the national debt at $18.3 trillion is already above 100% of GDP. This party will end very badly at some point.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.