Federal Reserve Chair Janet Yellen will give her semiannual monetary policy testimony to Congress this week. In the past, this has been an important event for the financial markets. However, Fed communication is a lot more open these days. For example, we have the forecasts of senior Fed officials and the minutes of the June policy meeting in hand. However, there is still scope for financial market participants to learn a bit more.

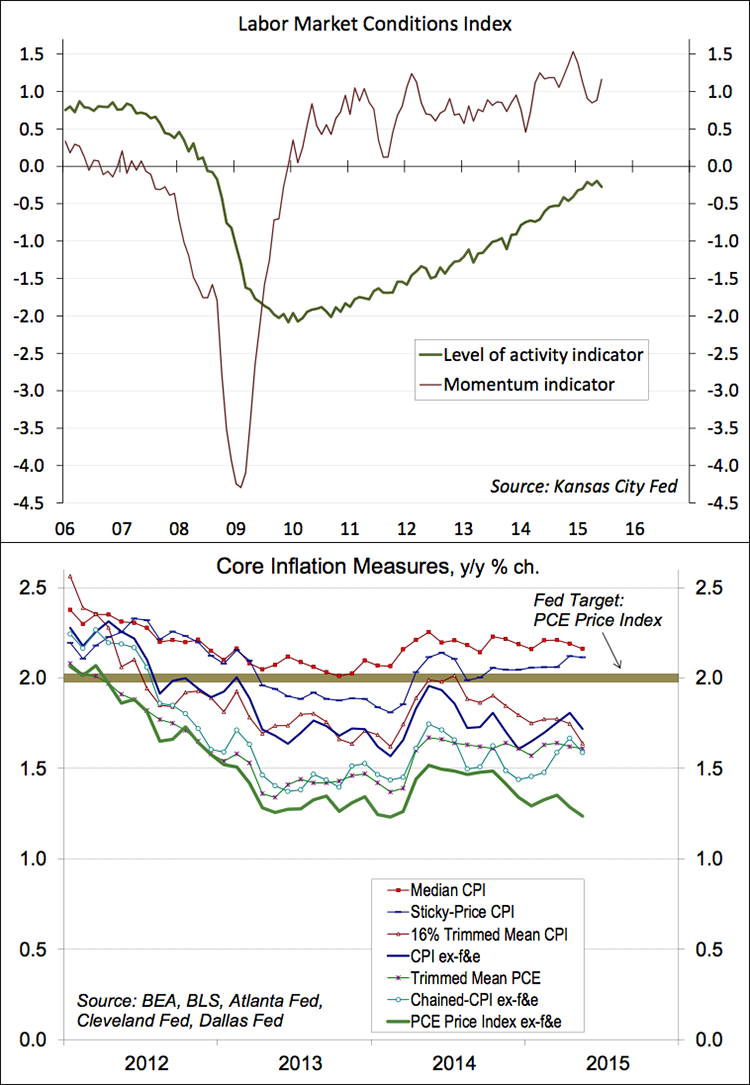

Over the last several months, Fed officials have made it clear that monetary policy decisions will depend critically on job market conditions and the inflation outlook. Job growth has remained strong. The unemployment rate has continued to decline and is now near levels that were once considered to be consistent with “full employment.” However, that figure presents a false image due to shifts in labor force participation. Some of that is demographics, the aging of the population. The Kansas City Fed’s Labor Market Conditions Index indicates that slack is being taken up, but considerable slack remains.

There are many measures of “core” inflation. One can exclude food and energy. It’s not that these don’t matter. Rather, monthly changes in food and energy are often volatile and we are interested in the underlying trend. Trimmed measures exclude the highest and lowest price changes. The Atlanta Fed’s sticky price index looks at prices of goods and services that change only gradually. Of these measures, the one the Fed focuses on (the PCE Price Index ex-f&e) is trending at the lowest level (that doesn’t mean that the Fed is wrong).

More importantly, the Fed isn’t worried about past inflation; the focus is on future inflation. The drop in energy prices and the strong dollar have put downward pressure on inflation over the last year, but as they stabilize, their impact on inflation will fade. In domestic production, there are no signs of the type of bottleneck pressures that would push prices higher. The labor market is the widest channel for inflation pressure. There are some signs that wage growth has picked up, but the pace has remained relatively lackluster. Average hourly earnings were reported to be flat in June, up just 2.0% from year ago.

Still, the Fed has to base policy on where the economy is expected to be many months down the road. Simply eyeballing the LMCI graph, it looks as if the labor market is on track to achieve some sense of normality in late 2016. The Fed is not going to wait until we get there to begin policy normalization. The best analogy is that while there is no pressing need for the Fed to hit the brakes, it does need to begin taking the foot off the accelerator in the not too distant future.

Yellen ended her July 10 speech on the economy by bringing up the issue of productivity growth, the most important factor in the long-term economic outlook. However, it’s unclear why output per worker has slowed in recent years. A long-lasting low trend in productivity would have important implications for the standard of living, but also for wage growth (slower), interest rates (lower), and the federal budget deficit (wider).