Themes from the First Half of 2015 and Questions for the Second Half

by Carl Tannenbaum of Northern Trust,

The past six months have been extraordinarily eventful. And recent events suggest that the balance of 2015 will not lack for excitement. We thought it would be important to take a break from Greece and China to share broad insights from our team on the key goings on.

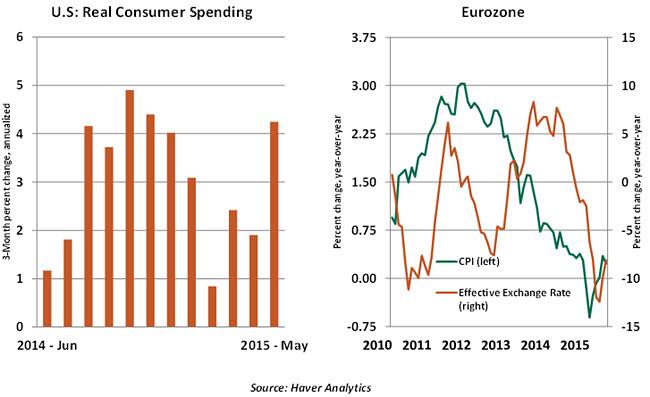

- U.S. consumer spending, on which the world economy relies heavily, showed a strong trend through January 2015. But this changed abruptly, as sales showed a deceleration in each of the following three months. It was a puzzling development because households had accumulated savings from lower gasoline prices and employment conditions were improving. Some held the view that the U.S. consumer was saving the windfall from lower gasoline prices as part of a newfound frugality.

This hypothesis was invalidated as consumers came back with vigor in May to record a 0.6% increase in real outlays. The 3.4% increase over the past year is the best reading for the entire recovery. All three major spending components – durables, non-durables and services – showed noteworthy gains. Auto sales rose at an annual rate of 12% in the second quarter versus a 2.1% dip in the previous quarter. Looking ahead, the fundamentals are supportive of sustained growth in consumer spending during the rest of 2015.

- The European Central Bank’s (ECB) quantitative easing (QE) program began in March with a plan to buy around €60 billion in public and private assets every month. Early returns suggest that the effort is succeeding.

There is considerably less worry that the eurozone will slide into sustained deflation, although inflation remains well below the target. There are also tentative signs that the program may be boosting the provision of credit. Lending to households saw an annual increase in May for the first time in two years. Yet the overall provision of credit to nonfinancial corporations is still negative, thanks to a still-declining trend in credit of over five years. And credit of less than a year is accelerating at its fastest pace in three years, while one- to five-year credit finally turned positive, a first in six years.In the eurozone, QE clearly has affected exchange rates and equity values. On a broad trade-weighted basis, the euro fell about 10% year-over-year in the second quarter; it lost almost 20% against the U.S. dollar. It also contributed to a strong showing for eurozone shares, a performance that the deepening Greek debt crisis rudely interrupted.

These successes have some suggesting that the ECB might curtail its bond purchases before its scheduled conclusion in September 2016. But to ensure a lasting impact, we expect ECB President Mario Draghi to see the program through to its conclusion.

In the eurozone, QE clearly has affected exchange rates and equity values. On a broad trade-weighted basis, the euro fell about 10% year-over-year in the second quarter; it lost almost 20% against the U.S. dollar. It also contributed to a strong showing for eurozone shares, a performance that the deepening Greek debt crisis rudely interrupted.

In the eurozone, QE clearly has affected exchange rates and equity values. On a broad trade-weighted basis, the euro fell about 10% year-over-year in the second quarter; it lost almost 20% against the U.S. dollar. It also contributed to a strong showing for eurozone shares, a performance that the deepening Greek debt crisis rudely interrupted.

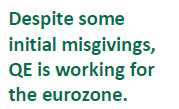

- Oil prices fell precipitously during the second half of 2014. That prompted a similarly precipitous decline in the number of American rigs actively producing petroleum. The rapid retreat of the U.S. energy sector was among the factors depressing economic growth in the first half of 2015.

Since January, however, oil prices have quietly risen by around 30%. A recovery in equipment spending within the energy sector logically could be expected but seems unlikely. U.S. producers have sustained output growth profitably even with fewer wells operating. Costs in the sector have been cut sharply, and production has focused on the most-fertile fields.

The increase in output also likely will cap oil prices during the balance of the year. This should solidify the “energy dividend” for consumers, which should aid economic growth in most developed countries.

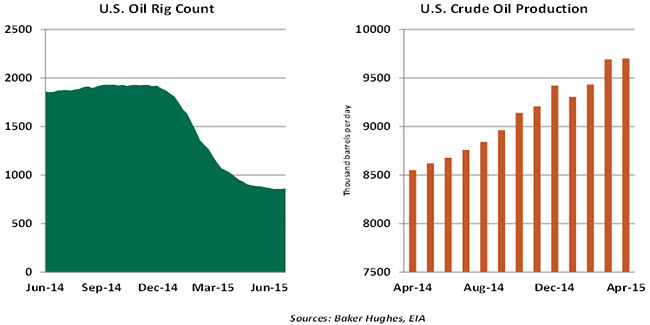

- The U.K. has had a solid and surprising six months. Data releases so far in 2015 have been mainly positive, with unemployment falling, real wages accelerating, consumer confidence rising and purchasing managers’ indexes posting strong figures. The election result was the major surprise and gave the Conservative Party an unexpected but slim majority. Support for the Liberal Democrats collapsed, and the Scottish National Party (SNP) gained nearly all the seats in Scotland at the expense of the Labour Party.

With a majority comes political stability, allaying fears of protracted coalition talks. However, it also brings risk in the form of an in-out EU referendum, the date of which is yet to be set. Over the coming months, we can expect U.K. Prime Minister David Cameron to hold talks with European leaders on negotiating a new deal for the United Kingdom’s place in the union. At home, the SNP’s rise will present challenges should it demand further devolution of power to Edinburgh. Economically, fiscal consolidation will continue, with spending cuts outlined in the July budget expected to reduce the deficit to 3.2% of gross domestic product (GDP) this year. The United Kingdom is expected to be one of the strongest G7 economies in 2015.

- The Trans-Pacific Partnership (TPP) has been a main focus of President Obama’s second term. The 12-nation trade agreement has struggled for years, as Democrats in Congress are wary of negative implications – primarily job displacement in export industries. The pact has been criticized for its lack of transparency and its handling of standards covering health, the environment, labor and intellectual property protection.

Tensions rose in June as prospects of the TPP’s ratification dwindled due to political gridlock. However, Congress recently granted President Obama Trade Promotion Authority (TPA). This motion, which nullifies Congress’ right to amend trade agreements, provided the president greater negotiating capabilities, significantly increasing the probability of a successful TPP. A formal agreement is expected following the Canadian general election in October.

The TPP remains a polarizing topic, especially as 2016 presidential election campaigns are underway. Critics claim the removal of tariffs will increase income inequality. But, the Petersen Institute of International Economics estimates the United States will gain $78 billion annually and increase GDP by 0.4% by 2025 through the TPP.

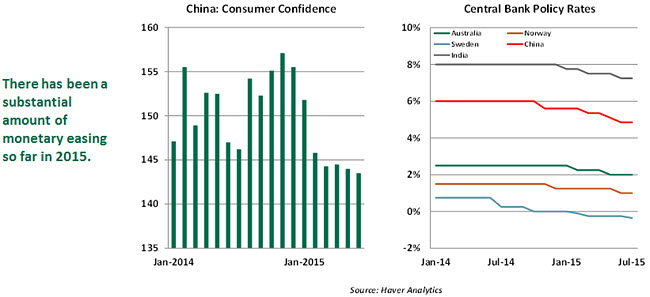

- It must be hard being a government official in China these days. Little is going right in the economy, and consumer confidence has sustained a blow as retail investors absorb the worst of the equity market correction. Beijing tried responding to the market correction with its usual rhetoric, backed by a significant injection of liquidity and increased intervention. This finally seems to have taken hold, with the Shanghai index rallying after declining 30% from its peak in less than a month. But many shares remain closed for trading.

The equity correction and the government’s response put China’s long-term economic plans at risk. The loss of value and tenuous market psychology represent speed bumps in the effort to promote more internal consumption. And the effort to gradually liberalize markets to a point where they operate without needing official intervention has clearly taken a backward step. Massive stimulus aimed at forestalling the impact of the Global Financial Crisis accompanied the last market crash in 2008. This time around, more government stimulus may be needed to achieve the “around 7%” growth target the government has set for itself.

- With very few exceptions, monetary policy has been incredibly loose this year. Worldwide, central banks have eased rates more than 50 times thus far in 2015, with China’s cuts two weeks ago being the latest. With very few exceptions, the motivation for these movements seems to have shifted from engaging in currency competition to recognition that tepid global growth and low oil prices have taken a toll.

With price stability part of most central bank mandates, the downward force of energy and commodity prices on inflation led monetary officials to respond to lackluster consumer price index readings with monetary loosening. This raises questions about whether an individual central bank, especially one in a moderately sized country, can affect prices that are influenced by global forces.

The bias of some global central banks toward loosening could end abruptly when the U. S. Federal Reserve starts raising rates. The shift will be especially pronounced in emerging markets, which rely on capital inflows and will need to maintain attractive interest rates to lure investors and prop up their currencies.

- Protests, strikes and insurgencies around the world are showing alarming vigor. The victory of Syriza in Greece is the foremost example, but there are many others. Parisian taxi drivers brought the city to a near-standstill in an effort to put Uber out of business. A work slowdown crippled the port of Long Beach, Calif., for a number of weeks, deeply disrupting trade. Islamists continue their march through the Middle East, and Russia continues to threaten former Soviet satellites. The post-crisis world seems to be far less-secure. The disappointing and uneven pace of the global recovery has created struggles for communities around the world. Those enduring poor fortune can begin to question whether the system is working for them and come to see the forces of change as enemies. Leveraged governments appear to have neither the appetite nor the funds to respond aggressively to domestic or international threats.

Restoring economic growth after the global financial crisis has been hard work. But the recovery has exacerbated the gap between the “haves” and the “have-nots.” Unless this gap begins to close, the politics surrounding economics will continue to get more complicated and potentially more dangerous.

The post-crisis world seems to be far less-secure. The disappointing and uneven pace of the global recovery has created struggles for communities around the world. Those enduring poor fortune can begin to question whether the system is working for them and come to see the forces of change as enemies. Leveraged governments appear to have neither the appetite nor the funds to respond aggressively to domestic or international threats.

The post-crisis world seems to be far less-secure. The disappointing and uneven pace of the global recovery has created struggles for communities around the world. Those enduring poor fortune can begin to question whether the system is working for them and come to see the forces of change as enemies. Leveraged governments appear to have neither the appetite nor the funds to respond aggressively to domestic or international threats. (C) Northern Trust