Introduction

No one knows your own personal financial situation better than you do. Every individual possesses their own unique investment goals, objectives, needs and risk tolerances. At first glance this may seem simple and straightforward to the point of stating the obvious. However, I contend that the reality that individuals have different financial situations, goals and objectives is profoundly important as it relates to designing an appropriate retirement investment portfolio. There is no such thing as one-size-fits-all when designing the appropriate retirement investment portfolio, or any type of portfolio for that matter.

I believe that a retirement portfolio should be designed to meet the unique needs and goals of the individual it is built for. To me the first and perhaps most important step is to ascertain a realistic assessment of the investor’s tolerance for risk. This will establish a foundation of what types of assets the investor would be capable of staying the course with. If the investor cannot tolerate the high risk necessary in order to achieve a high rate of return, the odds of a successful long-term outcome are greatly diminished.

Once risk assessment is established, the next logical step when designing a retirement portfolio is to determine the amount of income the investor needs to support them. Just as it was with risk assessment, income goals also need to be realistic and consistent with risk tolerance. After establishing risk tolerance and income needs, it then becomes reasonable to evaluate total return potential. Once again, realism comes into play. Investors need to understand and accept the reality that there is generally a trade-off between rate of return, income and risk.

In today’s market environment, I believe a realistic and reasonably conservative income goal falls somewhere between 2 ½% and 5%. Of course, higher yield is also associated with higher risk. Also, higher yield tends to be achieved at the expense of higher capital appreciation. To clarify and summarize, in order to achieve a higher yield you must simultaneously be willing to accept less growth or capital appreciation potential.

However, that does not necessarily mean that you cannot achieve an acceptable long-term total return at reasonable levels of risk. Instead, it simply means that a greater portion of your return will come from income rather than capital appreciation. I will be illustrating these principles more fully later in the article.

Is Index Investing the Right Choice for Retired Investors?

There are many who argue in favor of investing in index funds or ETF’s over constructing a portfolio of carefully selected individual securities. Their supporting evidence is usually predicated on statements such as the majority of actively-managed accounts do not outperform the S&P 500, or that your portfolio can only be successful if it beats the benchmark, again, usually the S&P 500.

Personally, I find these arguments irrelevant regarding designing a retirement portfolio that specifically meets the needs, goals, objectives and risk tolerances of a specific individual. For starters, as I previously indicated, a properly constructed portfolio is not simply or only about generating the highest total return. Investors are wise to recognize that total return is comprised of the two components income and capital appreciation. The former, income, is usually the most predictable and reliable component. In contrast, the capital appreciation component is harder to predict, and due to its more volatile nature, less reliable.

As to outperforming the index, wouldn’t it be a tragedy to have a portfolio that outperformed the index but did not meet your needs? The corollary to this last point is the fact that an index such as the S&P 500 will not necessarily meet the specific investment needs of every investor. For example, there are many retired investors that require more income than the S&P 500 is capable of generating. Supporters will argue that it doesn’t matter, because you can also harvest profits to supplement your income. But doesn’t that assume that profits will be there? As indicated above, the capital appreciation component is less predictable than the income component.

To conclude this section, retired investors have numerous investment choices at their disposal. In broad terms, investors only have two options - equity or debt. When investing in equities you are positioning yourself as an owner of the asset. Equity ownership comes with no guarantees or assurances that your investments will be successful.

Debt instruments imply loaning your money at interest. With positioning yourself as a loaner, you are assured of getting your money back at some point in the future, at least in nominal dollars, assuming of course the debtor is capable of paying the loan back. Consequently, as a general rule, debt investments are considered safer. On the other hand, debt instruments are typically associated with generating higher levels of income but earning lower total rates of return.

The point is that not all investment options are offered in order to achieve the highest total return. Some are offered to provide a higher level of income and/or significantly lower levels of risk. Therefore, investors are free to pick and choose among all the options that they feel best suit their own needs. Investing is not just about high returns; it’s also about safety and predictability.

Furthermore, within those broad categories are numerous types of securities that can be utilized. As an investor you can choose to selectively invest in individual securities, or you could invest in packaged investments such as ETF’s, mutual funds, partnerships, etc. Regardless of what type of instrument you choose or prefer, I believe they all require an appropriate level of research and due diligence. Just as there are many thousands of individual stocks and/or bonds to choose from, there are also many thousands of packaged products to decide upon. For example, many years ago it was reported that there were actually more stock mutual funds in existence than there were common stocks.

So what is the best option among all the many choices? The only correct answer is that it depends on the preferences of each individual investor to decide what’s best for them. Therefore, my advice is to follow your own hearts and minds and never let anyone talk you into investing in something you’re not personally comfortable with. But most importantly, do your best to choose the options that are best capable of meeting your own needs and risk tolerances. However, in order to accomplish that, you need to understand how the investments work and what they are actually capable of producing.

Performance is Two-Faced

Obviously, all of the available investor choices cannot be adequately covered in a single article. However, I will readily admit that I have a preference for carefully selected individual securities over investing in packaged products. Therefore, the vast majority of my work is oriented towards discussing individual stocks, primarily high-quality dividend growth stocks.

Moreover, consistent with the themes that I’ve already written about in the preceding sections of this article, I offer the following discussion about calculating performance. In my opinion, there are important aspects regarding performance measurement that are often overlooked. Many believe that performance measurement is simply adding up the numbers, I believe it is much more. For example, consideration about how much risk was taken to achieve a given result should also be made. This is what I mean when I often state that measuring performance without simultaneously measuring valuation is a job half done. In other words, I believe it’s more important to understand how and why a given level of performance was created. Additionally, I believe consideration should be given to both components - income and capital appreciation - when assessing performance results.

3 Blue-Chip High-Yield Dividend Growth Stocks: Income and Total Return Performance vs. S&P 500

As I discussed earlier, income is more predictable and reliable than capital appreciation. To illustrate my point more clearly, I offer the following analysis covering three of the most prominent blue-chip dividend growth stocks versus the S&P 500 over numerous timeframes. All three of these companies are Dividend Champions and Aristocrats and all three have calendar fiscal year-ends. This was important in order to provide an apples-to-apples timeframe comparison on each company versus the S&P 500.

At this point I want to be clear that this is a past performance comparison with a focus on cumulative dividend income versus the S&P 500 as one aspect, and total return versus the S&P 500 as the second aspect. Importantly, I arbitrarily picked 4 timeframes utilizing the F.A.S.T. Graphs™ fundamentals analyzer software tool, 20Y, 15Y, 10Y and finally 5Y. Note “Y” equals years, and each timeframe includes the current year we are in and one year of forecast, however, the performance calculations are only calculated up to present time.

Most importantly, valuation considerations were not made as I simply ran each company over the timeframes listed above. What I would like the reader to focus on is that with the exception of only one timeframe on one of these companies, each of these blue-chip dividend growth stocks outperformed the S&P 500 on a total cumulative dividends paid basis. Perhaps even more interesting, is the fact that over the vast majority of the time they also outperformed the S&P 500 on a total return basis. Again, they did not outperform over every timeframe - but they certainly did most of the time. This illustrates that you don’t necessarily have to give up total return for income.

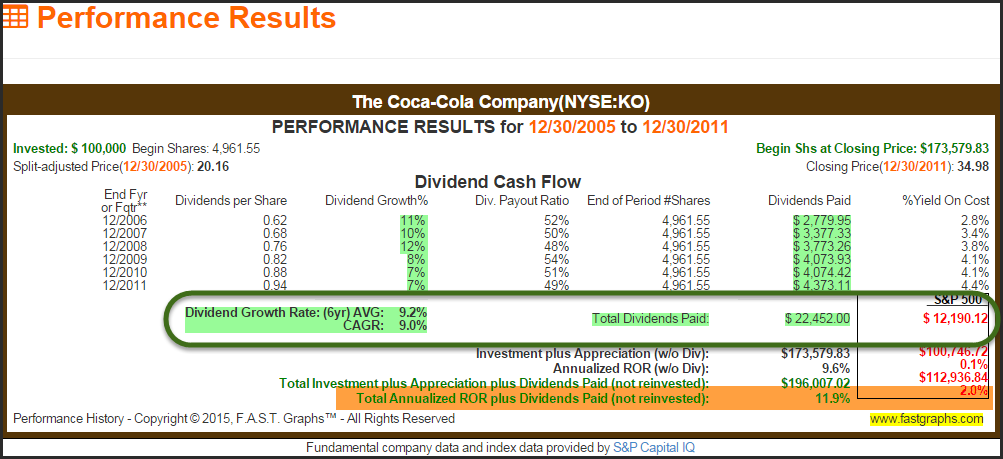

On each performance report I have placed the dark green circle around the total dividends paid calculation versus the S&P 500, and an orange highlight on the total annualized rate of return calculation versus the S&P 500. Also, for dramatic effect I have ran each performance result based on a $100,000 initial investment. Although I do not necessarily recommend investing that much in a single company, it makes the comparison versus the S&P 500 more relevant considering that it is a basket of 500 companies.

As a bonus, I have prepared a free analyze-out-loud video on my website MisterValuation that provides a more in-depth and detailed analysis on Coca-Cola in order to illustrate the importance and effects of valuation. As you will soon see, I specifically chose that company because it is the only one that did not produce higher total cumulative dividend income over all timeframes versus the S&P 500. However, as I suggested above, measuring performance without simultaneously measuring valuation is a job half done. If you watch the video you will discover that it took extreme overvaluation to keep Coca-Cola from generating more dividend income than the S&P 500 overall timeframes.

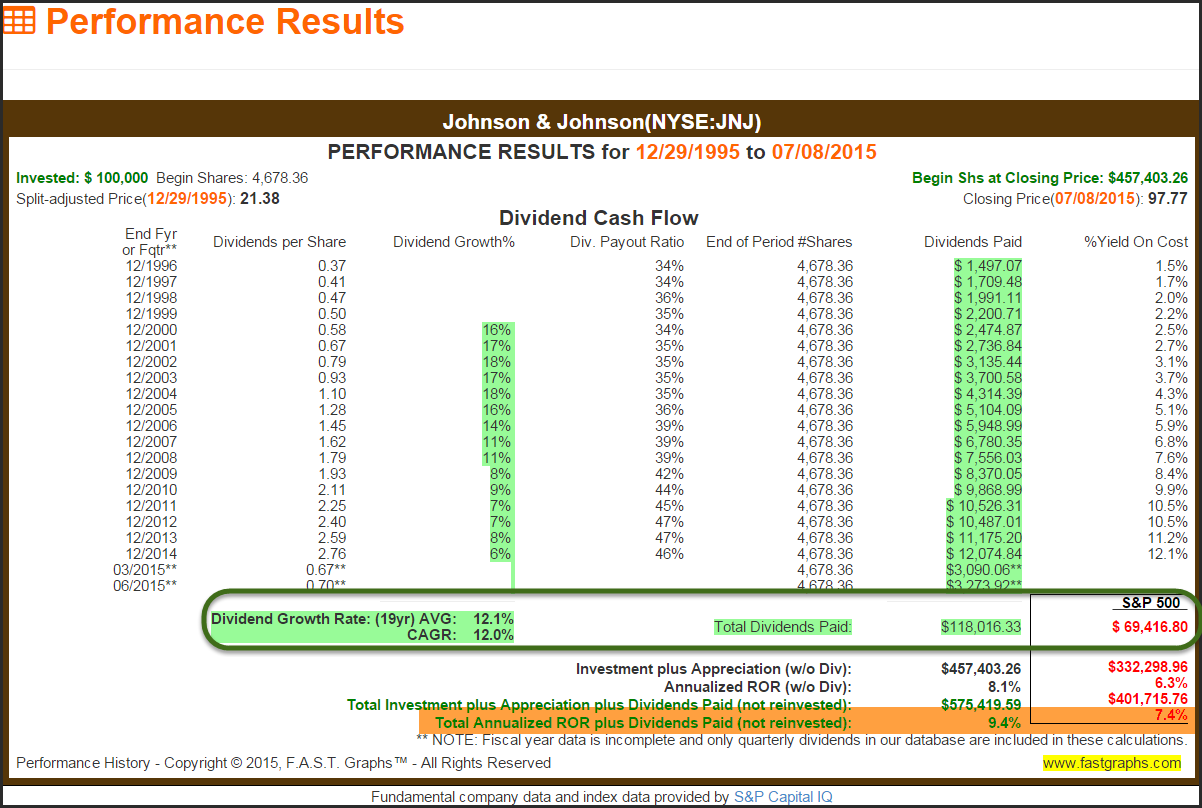

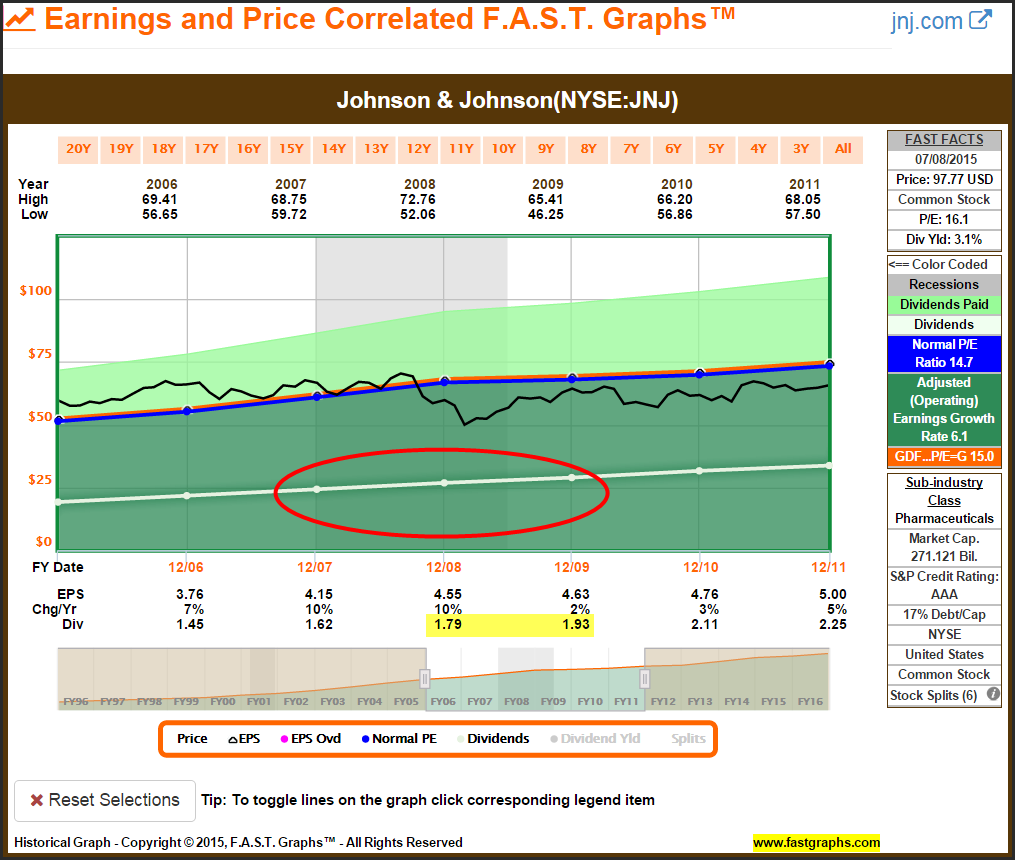

Johnson & Johnson Performance

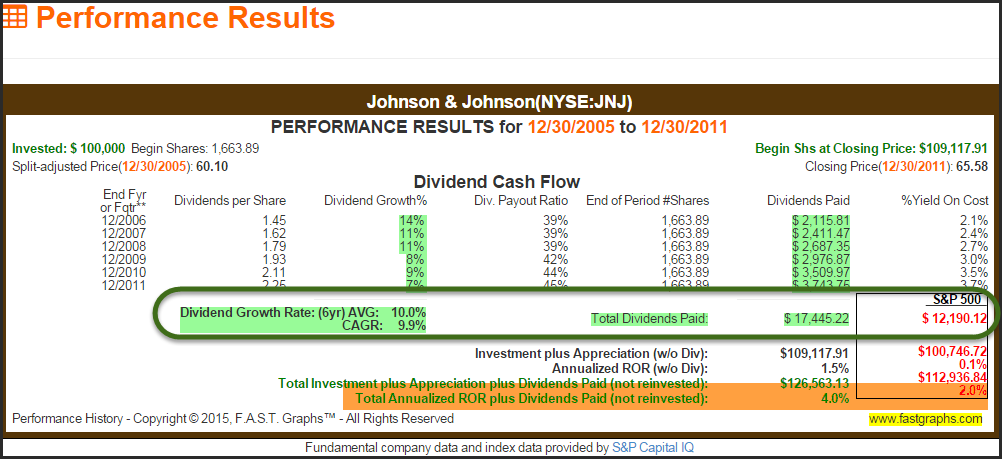

Going back to the beginning of 1996 Johnson & Johnson (JNJ), perhaps the most popular dividend growth stock of all, outperformed the S&P 500 on both counts - income and capital appreciation. However, the real story is found in the significant dividend income advantage it had over the index.

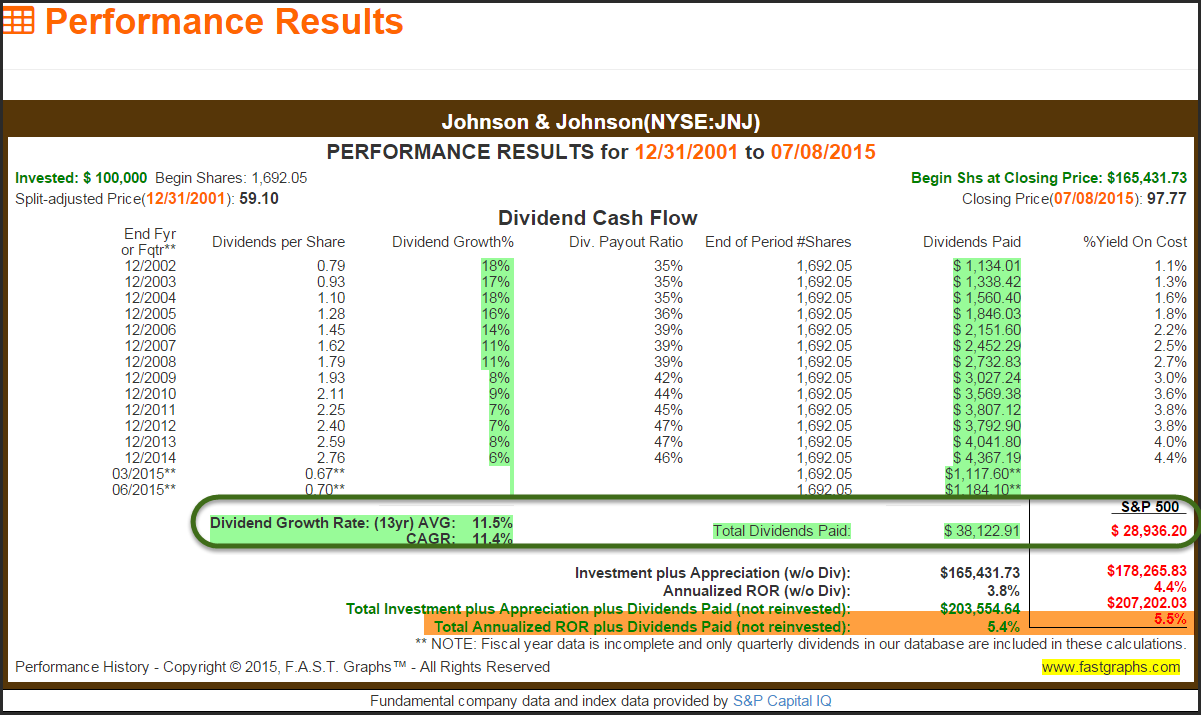

For the timeframe beginning in 2002, overvaluation headwinds caused Johnson & Johnson to underperform the S&P 500 on a total return basis, but only ever so slightly. Nevertheless, total cumulative dividends paid significantly outperformed the S&P 500.

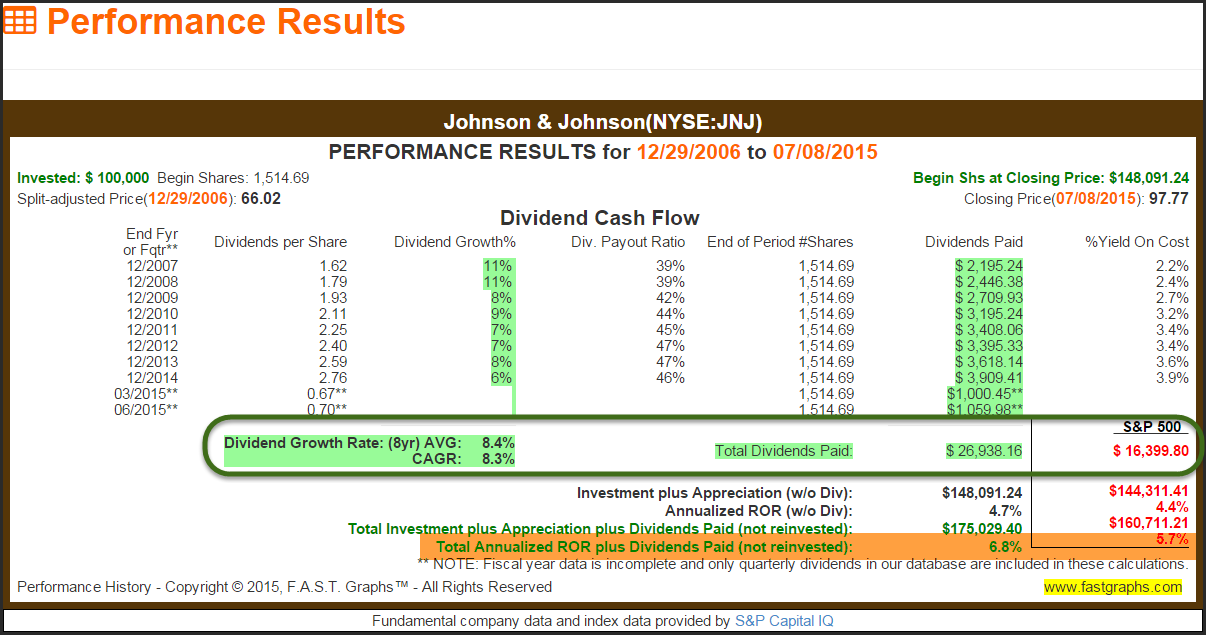

For the timeframe beginning in 2007, Johnson & Johnson slightly outperformed the S&P 500 on capital appreciation thanks to more reasonable valuation. However, significantly greater total cumulative dividends paid produced total return outperformance versus the S&P 500. This clearly illustrates the power and importance of dividends.

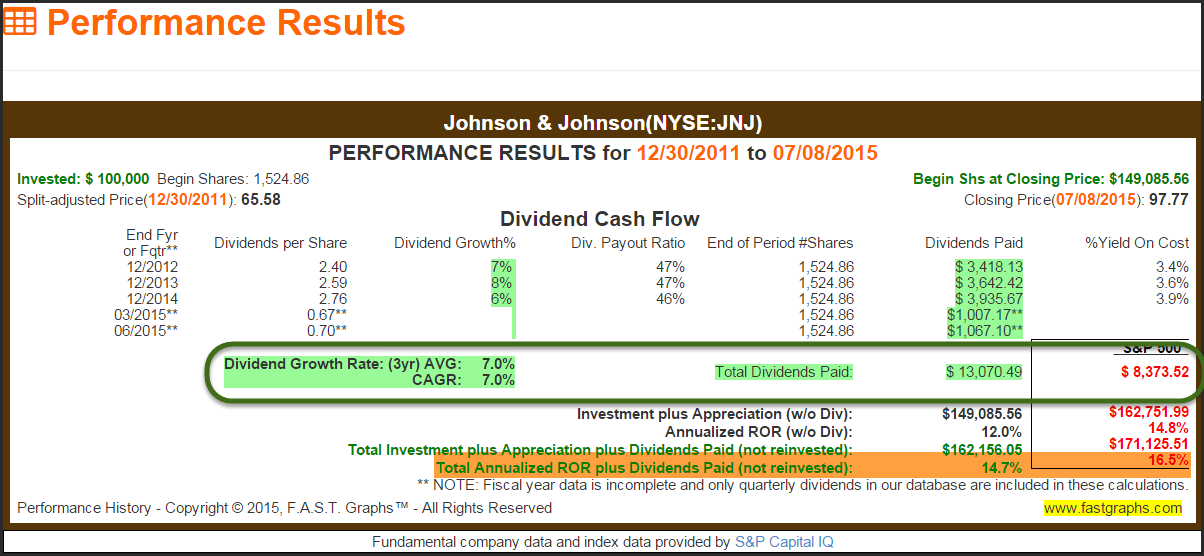

For the timeframe beginning in 2012, Johnson & Johnson underperformed the S&P 500 on a capital appreciation basis. However, double-digit capital appreciation in excess of 12% was more than acceptable considering how much more dividend income it paid versus the S&P 500.

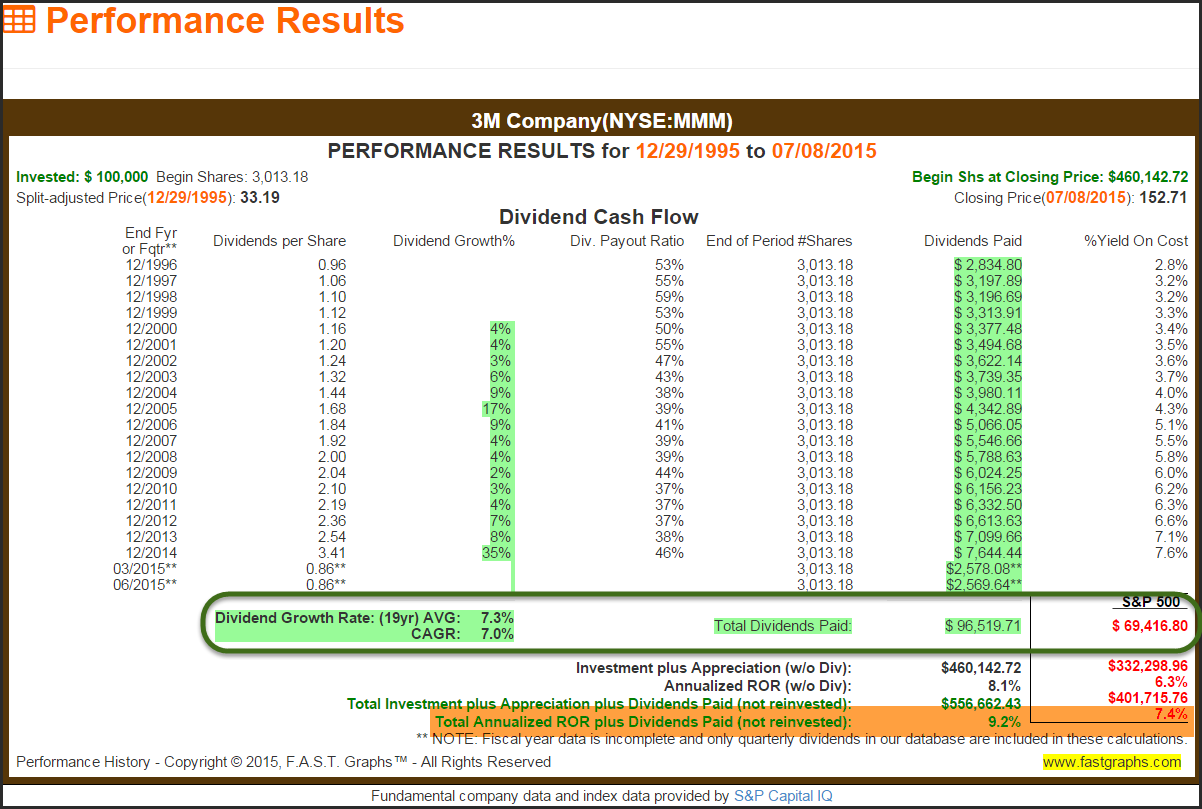

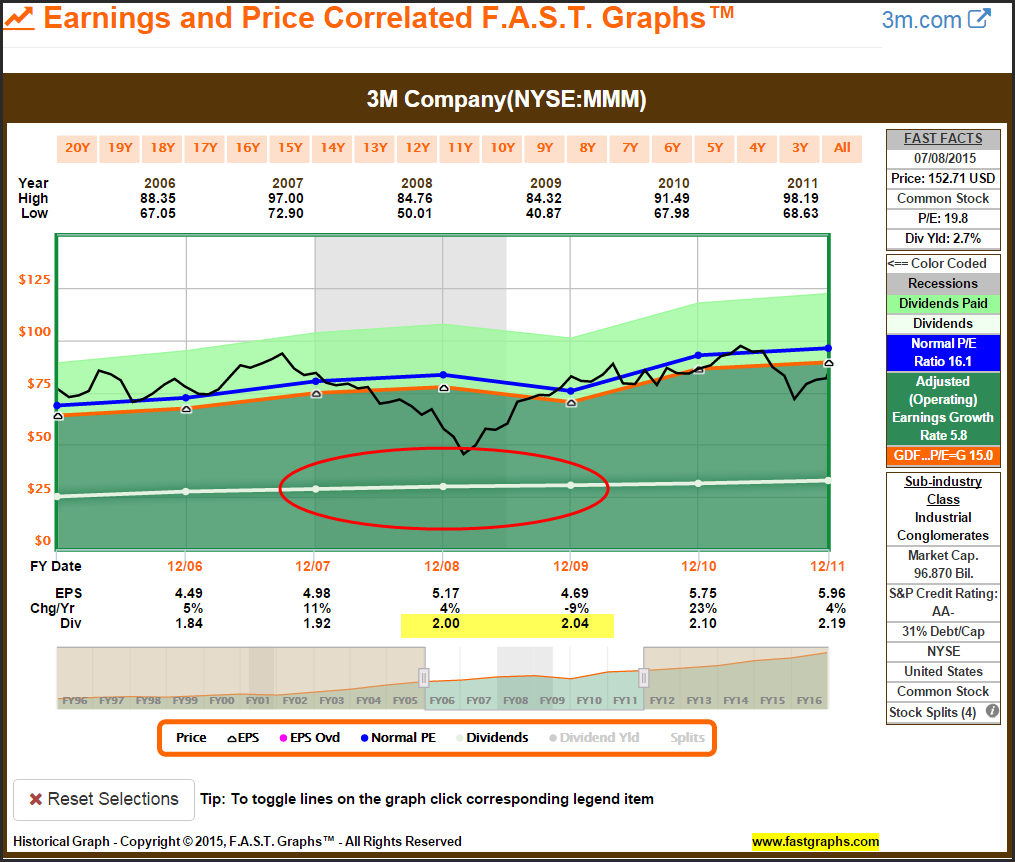

3M Company Performance

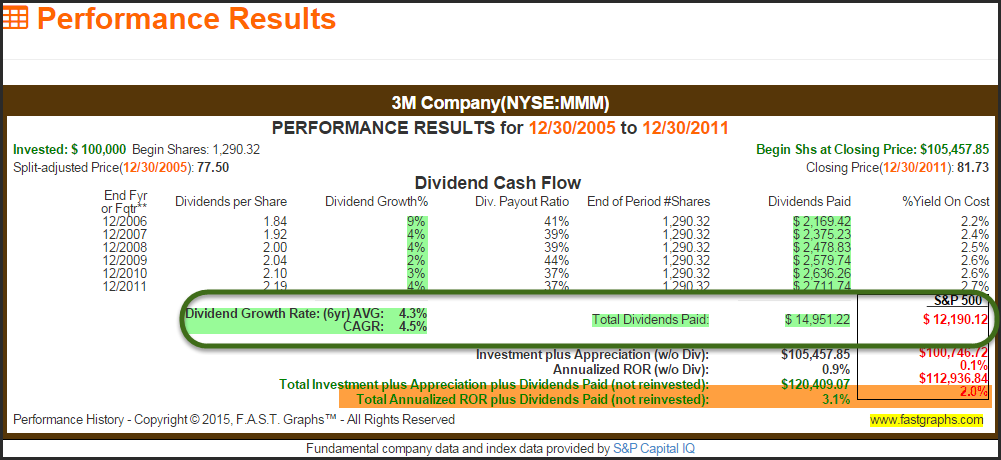

Over the long term since the beginning of 1996, 3M (MMM) outperformed the S&P 500 on both counts -capital appreciation and dividend income. However, for the retired investor needing income, the dividend advantage is the real story over this long timeframe.

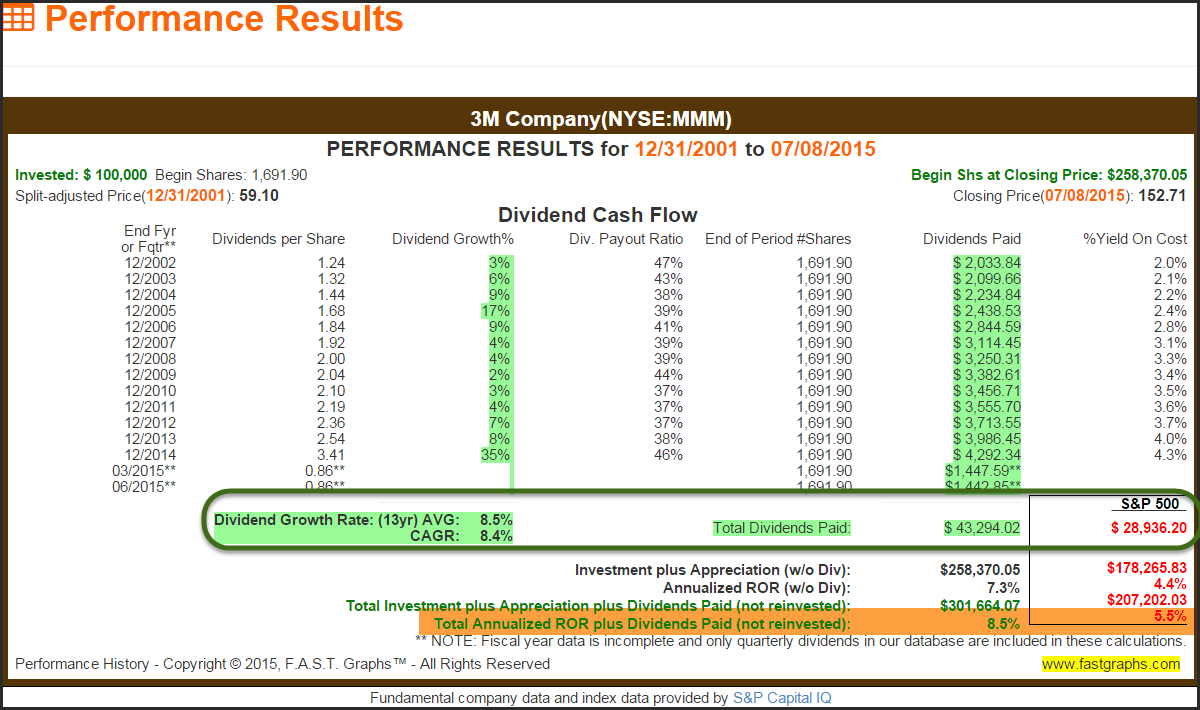

Since the beginning of 2002, 3M once again outperformed the S&P 500 on both counts - capital appreciation and dividend income. As I previously stated, you don’t necessarily have to give up total return in order to achieve greater dividend income.

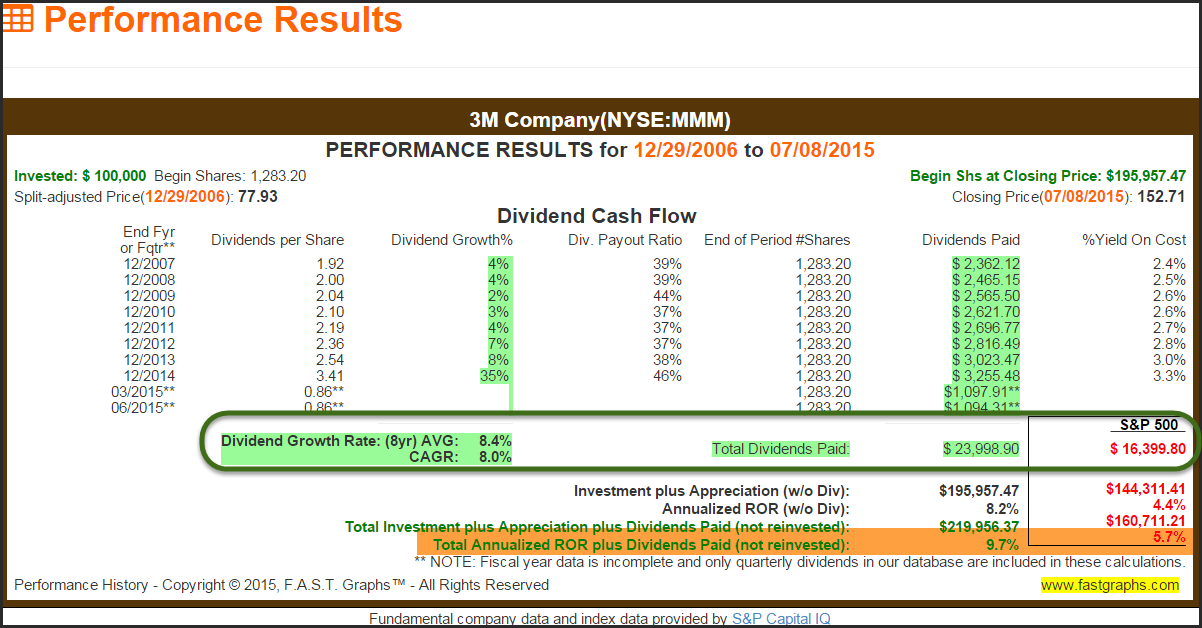

Since the beginning of 2007, 3M once again outperforms the S&P 500 on both counts – capital appreciation and dividend income.

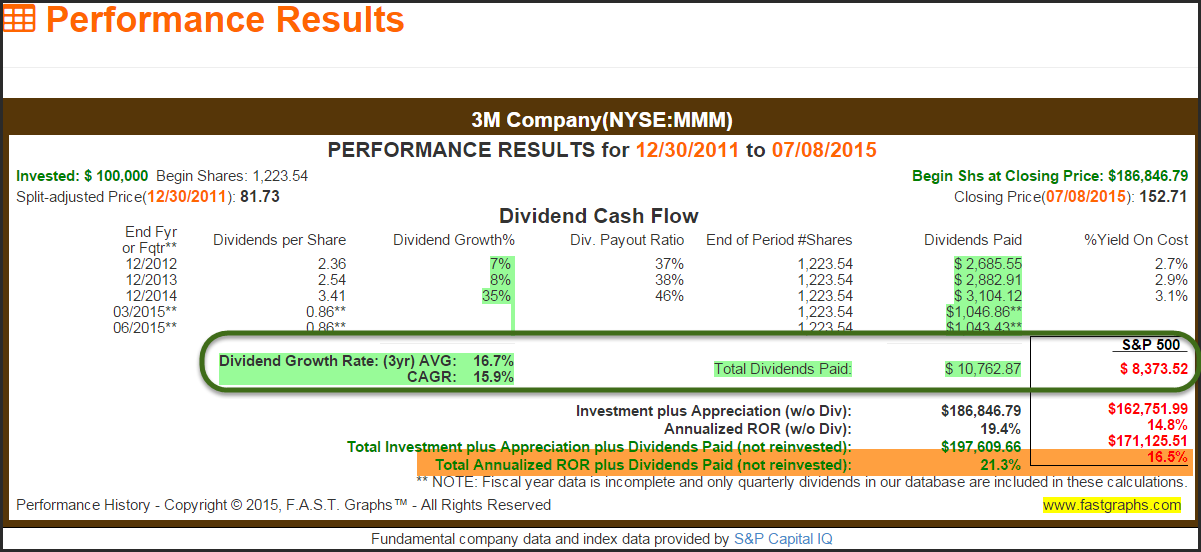

To complete its sweep of outperformance versus the S&P 500, 3M outperformed on both counts - capital appreciation and dividend income since the beginning of 2012. Perhaps the most interesting aspect of this outperformance is the consideration that this was one of the best performance records of the S&P 500 in history.

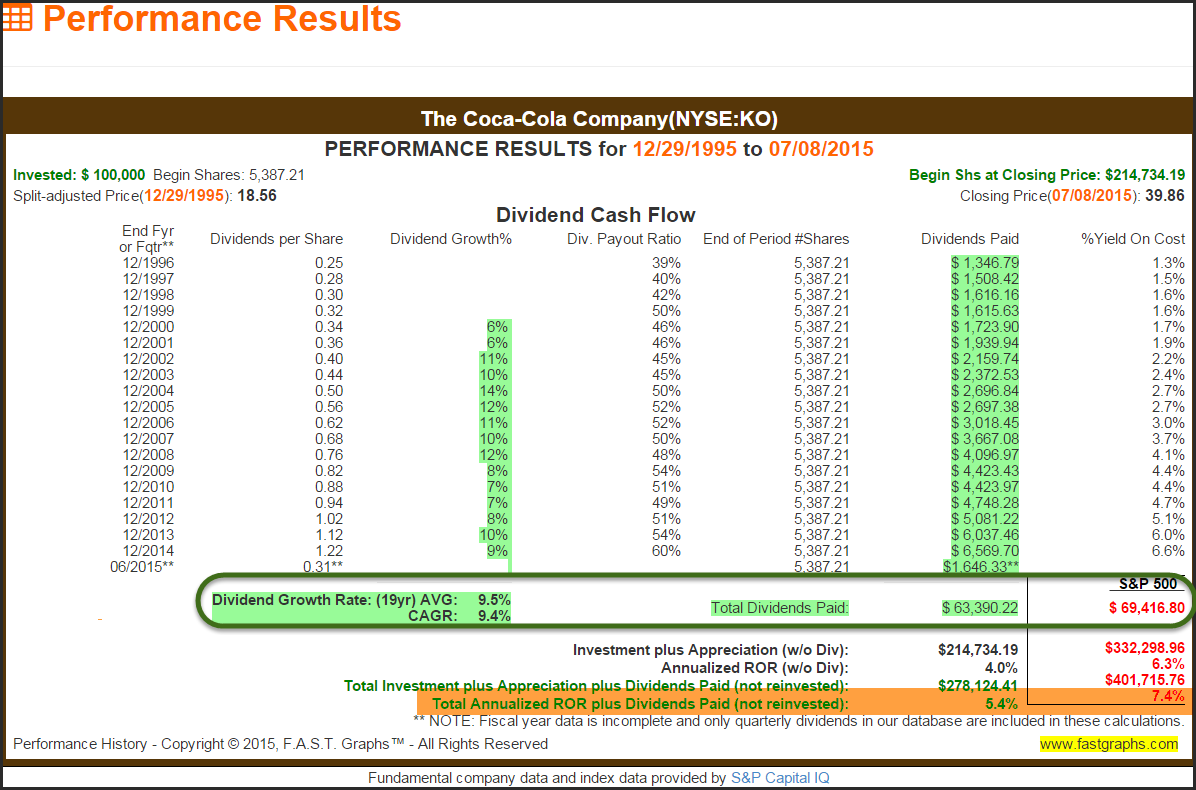

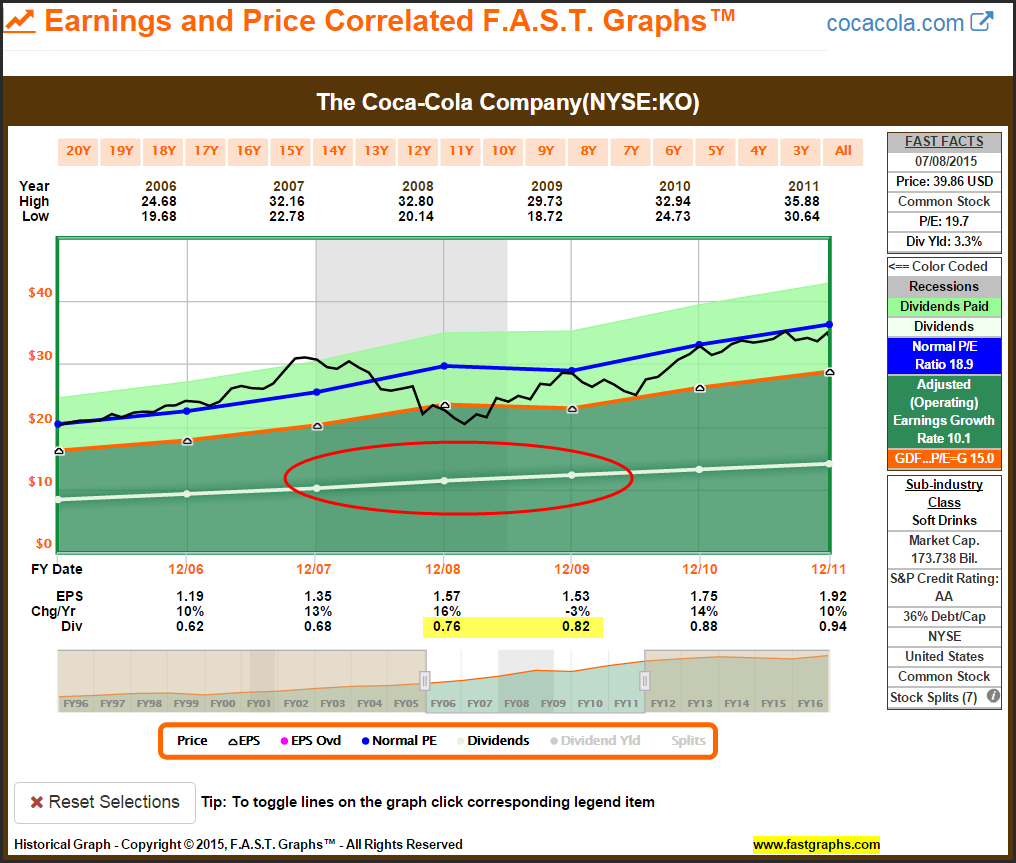

Coca-Cola Company Performance

At the beginning of 1997 Coca-Cola (KO) was trading at an excessively high P/E ratio of over 30. As a result of such high valuation, this blue-chip Dividend Aristocrat underperformed the S&P 500 on both counts - capital appreciation and dividend income. What is interesting about this particular timeframe is that it represents only one of two timeframes since the beginning of 1997 where Coca-Cola underperformed the index. The other timeframe was since the beginning of 1998. However, in every other single timeframe since, Coca-Cola significantly outperformed the S&P 500 on the basis of total cumulative dividends paid.

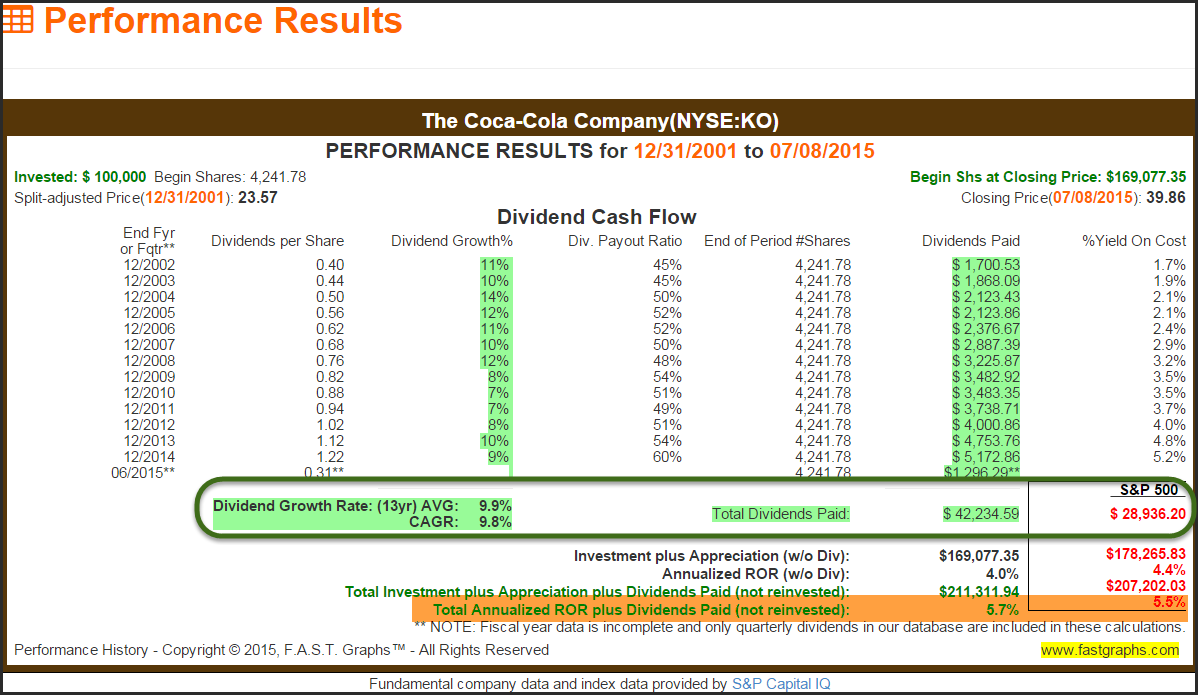

Since the beginning of 2002 Coca-Cola dramatically outperformed the S&P 500 on the basis of total cumulative dividends paid, but modestly underperformed on the basis of capital appreciation. However, thanks to its great dividend advantage, it modestly outperformed the S&P 500 on a total return basis.

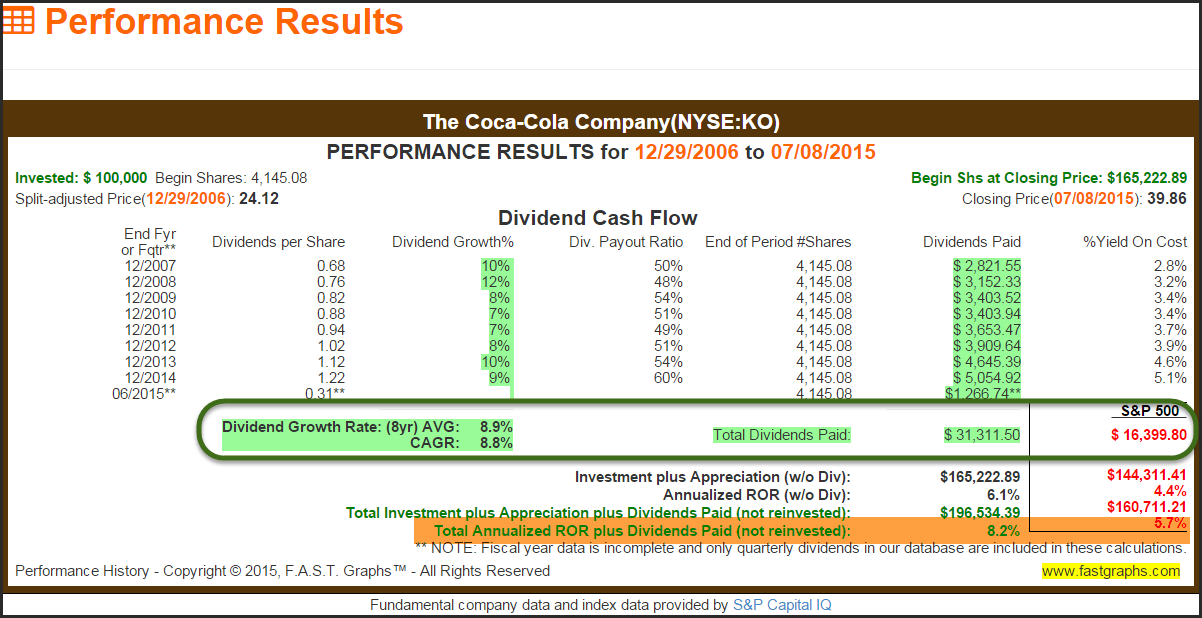

Since the beginning of 2007, Coca-Cola outperformed the S&P 500 on both counts - total dividends paid and capital appreciation. However, it should be noted that this was a time when the company could have been purchased when its price was aligned with its historical normal P/E ratio.

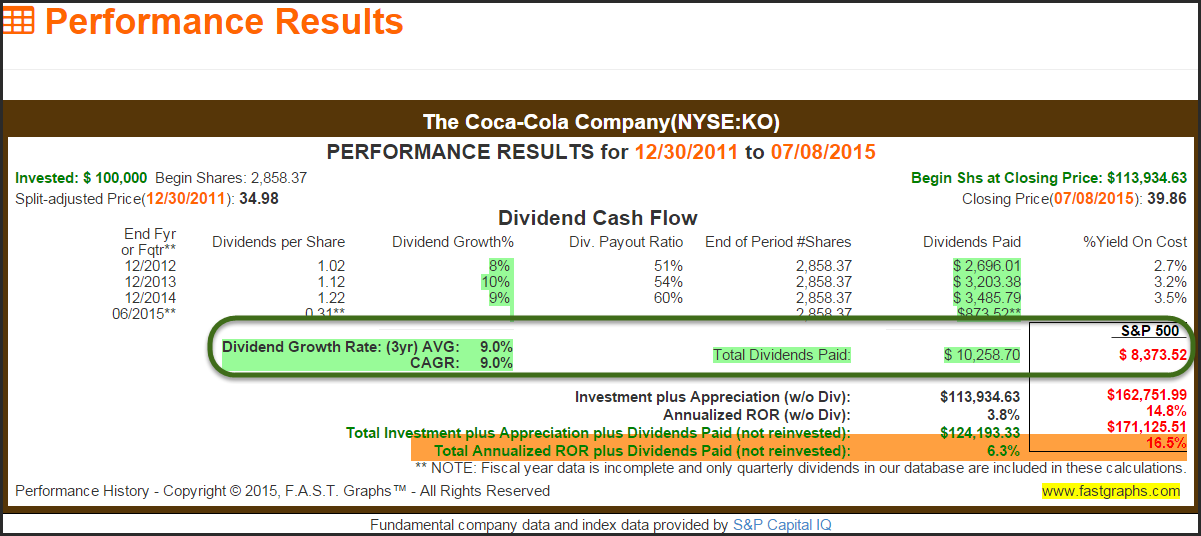

Since the beginning of 2012, Coca-Cola dramatically underperformed the S&P 500 on a capital appreciation basis. However, for the retired investor in need of income, it outperformed the S&P 500 on a total dividends paid basis. Although the capital appreciation component would be considered disappointing over this timeframe, the dividends paid represented spendable income without the need to harvest shares.

Battle Tested Through the Great Recession One of the Worst Economic Periods in Our History

One of the most important attributes that a retired investor needs is a consistent level of income. Additionally, it’s even better if the income increases each year. One of the great advantages of investing in blue-chip dividend growth stocks such as Dividend Champions or Aristocrats is a consistent and increasing dividend. This represents a significant advantage over investing in an index such as the S&P 500.

The following graphic presentation reviews each of the three featured Dividend Champions in this article during a period just before and just after the Great Recession. This was one of the most trying economic periods in our history. The three blue chips increased their dividends prior to, during and after the Great Recession. In contrast, the S&P 500 cut their dividend.

I have circled the Great Recession period on each of the earnings and price correlated graphs and highlighted the dividend record of each during the Great Recession. I have also included similar graphs on the S&P 500. I will let each of the following graphics speak for themselves.

Summary and Conclusions

When designing your retirement portfolios it’s important to focus your attention on building a portfolio that will meet realistic goals and objectives. Obtaining the highest possible total return is not always the proper approach. If income is your objective, it makes more sense, to me at least, to focus on the dividend potential that your equity portfolio is capable of achieving. Dividends are more predictable, and I contend, reliable than attempting to guess where stock price might go.

Moreover, if you invest in high-quality dividend growth stocks when valuations are sound, you do not necessarily have to give up capital appreciation or an attractive total return. A carefully selected portfolio of high-quality dividend growth stocks is a proven strategy for generating a consistent, reliable, and best of all, growing income stream. Additionally, you may not always earn a higher total return than investing in an index, but your odds of generating a greater dividend income stream are greatly in your favor.

Disclosure: Long KO, JNJ at the time of writing.

The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.