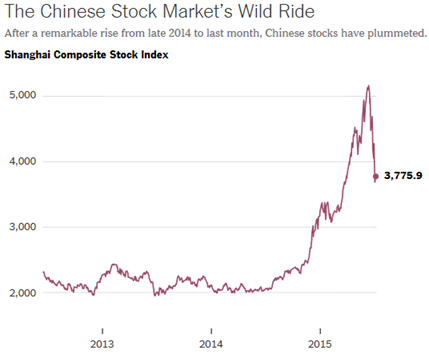

|

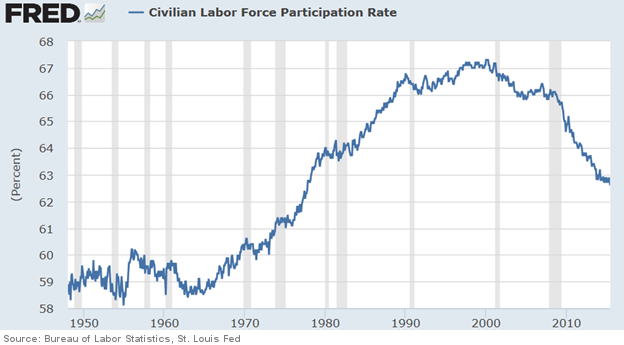

FORECASTS & TRENDS E-LETTER IN THIS ISSUE: 1. Another Ho-Hum, Disappointing Jobs Report For June 2. June Consumer Confidence Was Up More Than Expected 3. Gallup Job Creation Index at Record High May/June 4. China’s Stock Markets Imploded Over the Last Month Overview While the mainstream media has been obsessed with Greece over the last month or so, there has been scant attention paid to the fact that China’s high-flying stock markets unexpectedly have plummeted in June and were down around 30% through the end of last week. China’s exploding economy in recent years has made it the hotspot for global investors. Mutual fund families and ETFs have rushed to add exposure to the Chinese markets. China’s two major stock exchanges have seen their share indexes surge over 100% in the last year, drawing ever more investors to jump in. This includes many middle class Chinese who have never invested in anything before (many of whom have borrowed money to invest). Yet as noted above, in the last month, share prices on China’s stock exchanges have plummeted by around 30% as of the end of last week, to the surprise of just about everyone. The decline continued overnight (Tuesday). Many investors don’t even know it yet since they have not seen their June account statements. With the world’s attention focused on Greece over the last couple of weeks, the China story has not made its way onto the media’s radars for the most part. For that reason, I will focus on the latest disturbing developments in the China story today. But before we get to the troubling news on China, let’s take a look at a few of the latest US economic reports – including the June unemployment report, the big jump in consumer confidence last month and the Gallup Job Creation Index which is at a new record high. Another Ho-Hum, Disappointing Jobs Report For June The Bureau of Labor Statistics (BLS) reported last Thursday that the headline unemployment rate unexpectedly dipped to 5.3% in June from 5.5% in May. That’s the lowest level since April 2008. Employers added 223,000 jobs in June. While economists were forecasting an addition of around 230,000 jobs, the latest figure does continue the recent trend of above 200,000 average monthly growth in new jobs. The reason that the unemployment rate fell more than expected was the fact that the Labor Force Participation Rate unexpectedly fell to 62.6%, the lowest level since 1977. The Labor Force Participation Rate counts those who are working and those who are actively looking for work. That number dropped by 0.3% in June. That is why the unemployment rate fell more than expected to 5.3% last month.

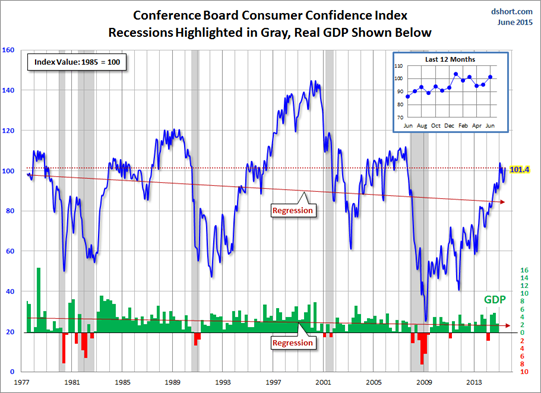

Making matters worse, the BLS made downward revisions in the number of new jobs created in April and May, reflecting a slower rebound from the weakness in the 1Q than previously thought. The jobs gain for April was revised lower to 187,000 from the last estimate of 221,000. The new jobs number for May was also revised down to 254,000 from 280,000 initially reported. So net total employment gains in April and May were 60,000 lower than the BLS previously reported. Currently 8.3 million Americans are unemployed. The number of long-term unemployed (those jobless for 27 weeks or more) declined by 381,000 to 2.1 million in June. These individuals accounted for 25.8% of the unemployed. Over the past 12 months, the number of long-term unemployed has declined by 955,000. This number is improving but very slowly. A long-standing concern has also been the large number of people who are working part-time, not by choice but because they have no better option. The U-6 unemployment rate, which measures under-employment, came in at 10.5% in June versus 10.8% in May and down from 11% a year earlier. That’s a modest improvement but still not good. Hourly wages in June were unchanged from last month at $24.95. As a result, the 12-month wage growth rate moved lower to 2.0%, down from 2.3% in May. Despite the flat wages in June, most economists remain optimistic that wages will show improvement in the third and fourth quarters of this year. So while the media hailed the June jobs report as a success, it was at best ho-hum considering the internals and the downward revisions to April and May. June Consumer Confidence Up More Than Expected Last Tuesday, the Conference Board reported that its Consumer Confidence Index rose sharply last month. The Index jumped to 101.4, up from 94.6 in May and above the consensus of 97.3.

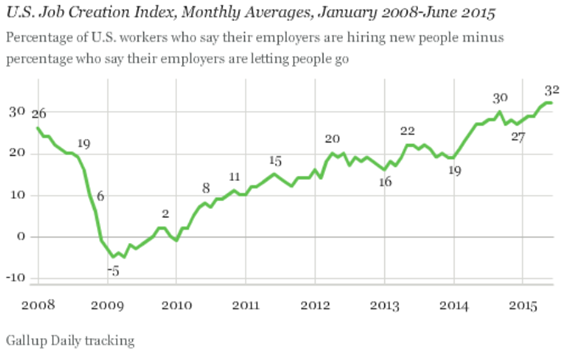

“Over the past two months, consumers have grown more confident about the current state of business and employment conditions,” said Lynn Franco, director of economic indicators at the Conference Board. “Overall, consumers are in considerably better spirits and their renewed optimism could lead to a greater willingness to spend in the near-term.” The University of Michigan’s Consumer Sentiment Index saw a similar jump in June, rising to 96.1 from 90.7 in May. The June reading marked a five-month high. Economists welcomed the improved mood of consumers with most predicting an increase in household spending just ahead. Automakers should be one beneficiary. With borrowing costs expected to increase, 13% of consumers have plans to buy a car in the next six months, the highest reading since January. In June, 60.6% of consumers said they think interest rates will go higher in the next year, just slightly below the 12-month high of 60.9% in May. Consumers in June also had a much better view about the current labor situation. Consumer perceptions of the labor markets are seen as an indicator of the trend in unemployment. The confidence survey found that 21.4% of consumers thought jobs were “plentiful” in June, compared with 20.6% who thought that in May. Another 25.7% described jobs as “hard to get,” down from 27.2% saying that last month. This metric is improving, but slowly. Gallup Job Creation Index at Record High May/June Gallup’s U.S. Job Creation Index remained high in June at +32. The Index score is the difference between the percentage of workers who say their employer is hiring people and expanding its workforce compared to those saying their employer is letting workers go and reducing its workforce. In June, 43% said their employer was hiring versus only 11% who said their employer was letting workers go – hence the reading of +32 which is a record high.

Gallup began tracking job creation in January 2008 as the Great Recession began taking hold in the US economy. Gallup’s latest Job Creation Index was based on interviews with 16,572 full- and part-time workers in the US, conducted June 1-30. The strong reading in the Gallup Job Creation Index and the jump in consumer confidence in June bolstered the chances for the economy rebounding in the second half of the year. By how much remains to be seen. The Commerce Department’s advance estimate of 2Q GDP will be released on July 30. China’s Stock Markets Imploded Over the Last Month China’s exploding economy in recent years has made it the hotspot for global investors. Mutual fund families and ETFs have rushed to add exposure to the Chinese markets. China’s two major stock exchanges have seen their share indexes surge over 100% in the last year, drawing ever more investors to jump in – including many middle class Chinese who have never invested in anything before. Yet in the last month or so, share prices on China’s stock exchanges have plummeted by around 30%as of the end of last week, to the surprise of just about everyone. Many investors don’t even know it yet since they have not seen their June account statements.

The Communist government of China has reacted to the stock market plunge with some extraordinary intervention to try and halt the decline, but it remains to be seen if those measures will be successful. With the world’s attention focused on Greece over the last couple of weeks, the China story has not made its way onto the media’s radars for the most part. For that reason, I will focus on the latest troubling developments in China today. I looked to Dr. Minxin Pei (PhD) who is a recognized expert on China. He wrote an excellent analysis on the latest developments in China in FORTUNE magazine online on Monday, which has the best and most understandable explanation I have seen. I have reprinted it for you below. China’s Big, Misguided Stock Market GambleBeijing should be building social safety nets and recapitalizing The rout in China’s frothy stock markets since mid-June has been painful, to say the least. Between its peak on June 12 and July 2, the Shanghai Composite Index, which includes China’s largest companies, dropped 28%, wiping out $2.4 trillion in paper wealth. In real market economies, stock crashes of such magnitude may cause heartburn but unlikely precipitate frenzied government efforts to prop up equity prices. But China is, as we know, not exactly a market economy and has a government that acts differently. In response to the latest crash, instead of allowing market forces to self-correct, Beijing is rolling out aggressive measures to keep the bubble from popping completely. Over the weekend, the People’s Bank of China announced a plan to inject funds into a state-owned entity that lends to brokerage firms. The country’s 21 brokerage firms also pledged 120 billion yuanto invest in stocks when the Shanghai Composite Index is below 4,500 (it closed at 3687 on July 2). Besides financing the bubble with new money, the Chinese government has suspended IPOs, cut trading fees, and relaxed requirements on margin loans (for example, Chinese retail investors can now use their apartments as collateral). We can excuse Chinese leaders for fearing that a rapid collapse of the leverage-fueled bubble would set off secondary financial implosions in the country’s financial sector. Margin loans are estimated to total 4 trillion yuan, half of which is supplied by the shadow banking system, and they are the source of 18% of the country’s total credit, making them an integral part of the financial system. Beijing worries that a market crash could create, through the shadow banking system, financial contagion that, in turn, will accelerate the bursting of another much bigger bubble: Chinese real estate. There are, however, two less charitable explanations for China’s latest moves. First, Chinese leaders tend to view economic issues from a purely political perspective. Unsurprisingly, the performance of the stock market has been made a barometer of the popularity of the current regime. The head of [the] China Security Regulatory Commission not too long ago called the soaring market “a reform bull market,” suggesting that investors were giving a vote of confidence in the leadership’s promised reform programs. A plunging market would imply a loss of confidence and falling popularity of the current leadership—an intolerable prospect. Second, those who have watched how China deals with bubbles know that its leaders have little faith in market forces but excessive confidence in their ability to sustain bubbles. We can see this mindset at work in China’s management of two recent bubbles: the real estate market and local government debt. In addressing the real estate market bubble, Beijing has opted to keep insolvent developers alive by forcing their lenders to roll over the loans. Consequently, the glut of unsold inventory hangs over the real estate sector. Because there is such an excess in the supply of housing, it is unlikely that those zombie real estate developers will return to life and pay their creditors in full. Beijing has used a similar recipe for shoring up its debt-laden local governments. After the bond market rejected Beijing’s plan to float the debt issued by local governments earlier this year, Chinese leaders simply ordered state-owned banks to buy such debt, adding assets of dubious quality to their balance sheet. Fortunately for Chinese leaders, they have not paid a heavy penalty for supporting these bubbles. At least not yet. It is also likely that, in deciding to intervene in a crashing stock market, Beijing believes that it can again get away with market-defying policies. We do not know whether Beijing’s big stock market gamble will pay off, but its odds are not encouraging. Even after its recent plunge, Chinese stock prices are overvalued. The price-earnings (P/E) ratio of the Shanghai Composite Index is 23, compared with 12 for the Hong Kong’s Hang Shen Index, on which many of the same Chinese firms are listed. The Shenzhen Composite Index, which has lost a third of its value, has an average P/E ratio of 50. (However, a hefty portion of the reported earnings of Chinese firms is “investment income,” paper gains from their overvalued stock portfolios.) Efforts to support the market at high valuations are expensive and unlikely sustainable. Beijing is trying to save the stock market bubble while three other bubbles have yet to deflate: real estate, local government debt, and manufacturing overcapacity. It’s possible that these bubbles will feed into each other, amplifying distortions and raising the final bill to clean up the mess. The opportunity costs for Beijing’s intervention are very high. Right now, Beijing should be building social safety nets and recapitalizing its banks, not betting the house on a stock market bubble. In closing, there is a lot more to worry about with China than with Greece. US bank exposure to Greece is minimal versus China – a reported $2 billion versus $20 billion, respectively. For that reason and others, we need to keep an eye on China. I will keep you posted in the weeks to come… Interesting times! Best regards, Gary D. Halbert |

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |