On virtually every financial website on the planet there is a never-ending daily stream of stock tips and recommendations. Consequently, the investing public is literally flooded with information and advice regarding what stock to buy today or not to buy. Some of what is offered is supported by factual information and logic, but unfortunately, much of what is offered is merely based on the opinion of the author. This presents quite a challenge to the prudent prospective investor seeking sound advice or guidance. The recommendations are presented and it is left up to the individual to act on the advice or not based on the content as written.

In addition to a barrage of information on what stocks to buy, there is also a proliferation of advice alleging to tell the investor what they ought to do. There are pundits who strongly recommend virtually every type of investing philosophy or strategy available. Some are adamant about investing in passive investments such as index mutual funds or ETFs. Others recommend constructing portfolios based on the careful selection of individual stocks. These are just a few of the many “ought to’s” that are often vigorously offered as the one and only choice.

Additionally, there are many pundits attempting to tell the investor that they should be investing in growth stocks, value stocks, dividend growth stocks, large caps, small or mid-caps, and the list goes on. This never-ending litany of information often creates confusion and anxiety as a result of information overload. Therefore, instead of answers, many investors are left with many unanswered questions such as whom to believe, what to believe, or where’s the best place to put their money?

To make matters worse, there is very little or virtually no accountability as to how the recommendations or tips have worked out over the long or short run. To be fair, this last fact is somewhat understandable. As a rather prolific author myself, I understand the challenges that come with the public dissemination of advice and guidance. This is not the same as specifically managing your own portfolio or the actual specific portfolio of someone else.

Financial writers are instead generally speaking to a broad and diverse audience. In my own personal work, I have often presented research candidates that were specifically oriented to different investor types. Some of my past work has presented aggressive growth stocks; some have been oriented towards blue-chip dividend paying stocks and everything in between. To be clear, as it is with most financial writers, each new piece of work is often independent of other pieces of work that were offered previously. In other words, there is rarely any synergy between articles written today versus ones that will be written in the future or the past.

Additionally, in my own personal case, I never offer specific or absolute buy or sell recommendations. Instead, I prefer to present what I believe are interesting research candidates that might serve a certain type of investor’s needs, goals or objectives. However, since I do not know each specific individual’s situation that might be reading my work, I always recommend that each reader conduct their own comprehensive research and due diligence.

Nevertheless, this doesn’t mean that there should be no accountability of an author’s work over time, whether it is mine or any other author’s. This last statement was the inspiration for this series of articles.

My Record as a Financial Writer/Blogger

In part 1 of this two-part series I presented what I consider to be a comprehensive report on the performance of individual research candidates presented in articles I wrote during my first six months as a financial author. In this, part 2, I will complete a review of my first complete year (twelve consecutive months) of presenting research candidates on individual stock selections.

Furthermore, I believe that successful investing implies taking a long-term view when investing in common stocks. By long term, I am referring to investing in and owning a business for a minimum of a normal business cycle of 3-5 years, but preferably longer. Therefore, this series of articles is only reviewing the past performance of my work based on long-term results that spanned at least a normal business cycle. To repeat what I said in part 1, as Ben Graham so eloquently put it, "in the short run the market is a voting machine, but in the long run it's a weighing machine."

Furthermore, as I stated in part 1: To be fair, I will also add that I did not own all of these recommended research candidates, but I did own most of them. Furthermore, these calculations do not include specific times where I sold. In other words, this is not a precise presentation of portfolio performance; instead, it is simply reviewing the record produced by the individual research candidates based on the publication date of articles. Readers of these articles were free to choose to ignore, buy and/or sell any of these offerings based on their own needs or views.

As it specifically relates to this series of articles, it's also important for me to interject that this is not an exercise meant to brag about how smart I have been. As I previously stated, not all of my research candidate recommendations were profitable. I have included the good, the bad and the ugly.

The Many Faces of Performance Reporting

Before I go on and present the record of the articles I wrote my first year as an author, I believe a few comments regarding performance reporting in general are in order. There are those that believe that performance reporting is a straightforward process, in truth it is not. Calculating the numbers from point A to point B for a stock, mutual fund, ETF, individual money manager or any other asset class does not necessarily tell the whole story. There are many other considerations that should be taken into account when evaluating the performance of any investment.

Perhaps the most important consideration is the amount of risk taken to achieve a certain performance. There are times when taking on great risk produces great results, and of course, there are times when taking on great risk produces abysmal results. Therefore, when examining past performance, the prudent investor also evaluates the amount of risk it took to achieve it.

And since we all know that “past performance is not necessarily indicative of future results” it logically follows that knowing the amount of risk it took to generate a level of past performance is critical. In other words, some investments are suitable for certain investors and others are not, regardless of past performance. Consequently, making an investment decision solely based on past performance can be both misleading and dangerous.

Then there are also considerations that should be given to the makeup of past performance results. How much of it came from capital appreciation versus how much of it came from dividend income is but one example. To the investor that is depending on the income their portfolio produces to live off of, the income component is significantly more important than capital appreciation. For example, a powerful growth stock may have generated significant historical total returns, but no dividends. Consequently, that growth stock might not be suitable for the retired investor needing income.

Of course, I cannot write on the subject of performance measurement without mentioning valuation considerations. There can be times when a given stock produced poor historical total returns simply because the measuring period started at a time of excessive valuation. Therefore, the headwinds of high valuation might have caused poor historical performance even when the company generated strong operating performance at the same time.

The opposite could also be true. Great historical performance could have been a function of extreme undervaluation at the start of the measured timeframe. This could occur even if a given company produced mediocre operating performance. The tailwinds of undervaluation could have easily produced aberrantly high historical results. And it should also be understood that a historical performance result of every valuation metric in between could also be the source of good or bad historical performance. Just knowing the raw numbers is not enough to make an intelligent decision upon.

Then there is the subject of benchmarking. There are many that believe that every portfolio’s performance should be measured against the specific benchmark such as the S&P 500. These people like to argue that if your portfolio didn’t beat an index, it failed you. I completely disagree. My problem with benchmarking against an index is that the index may not be a suitable choice for certain investors, especially retired investors in need of income.

There are many high-quality blue-chip dividend growth stocks that have outperformed the S&P 500 index on both capital appreciation and dividend income. On the other hand, there are many high-quality blue-chip dividend growth stocks that have underperformed the S&P 500 index based on capital appreciation but produced significantly more dividend income. In other words, there are different components of total return or past performance that could make an investment suitable for some investors, but not for others.

As a point of interest, I do believe that every portfolio should be measured against a benchmark. However, I do not believe that the benchmark needs to be an index. Instead, I believe the best benchmarks that certain investors should measure their portfolios against are their own unique goals, objectives and risk tolerances.

To some investors this might be a certain level of income that is growing, to other investors with different goals and objectives it might mean a total rate of return objective that is commensurate with the amount of risk they’re willing to take. I do believe that a portfolio should be managed toward specific goals, but I do not believe those goals are necessarily related to an arbitrarily-selected product or index.

I am only covering a few aspects of the complexity of performance reporting, there are many others too numerous to cover in a single article. However, I hope that what I presented at least enlightens the reader to the reality that performance reporting is not the simple or straightforward process that many would like to lead us to believe. There are many nuances and considerations that must be made when evaluating the historical performance results of any investment.

Research Recommendation Results from My Second Six Months as a Financial Blogger

What follows is a wide-ranging look-back at the second six months of my first year's worth of offerings where I presented fairly valued research candidates for readers to consider. In this, Part 2, I will cover my recommendations through July 2010. In addition to individual companies I covered, I will also cover an example where I wrote about the S&P 500 index as a proxy for the market. Just as I did in Part 1, I will include a few comments on the S&P 500 article that represent the pushback I received because my article was positive about the market.

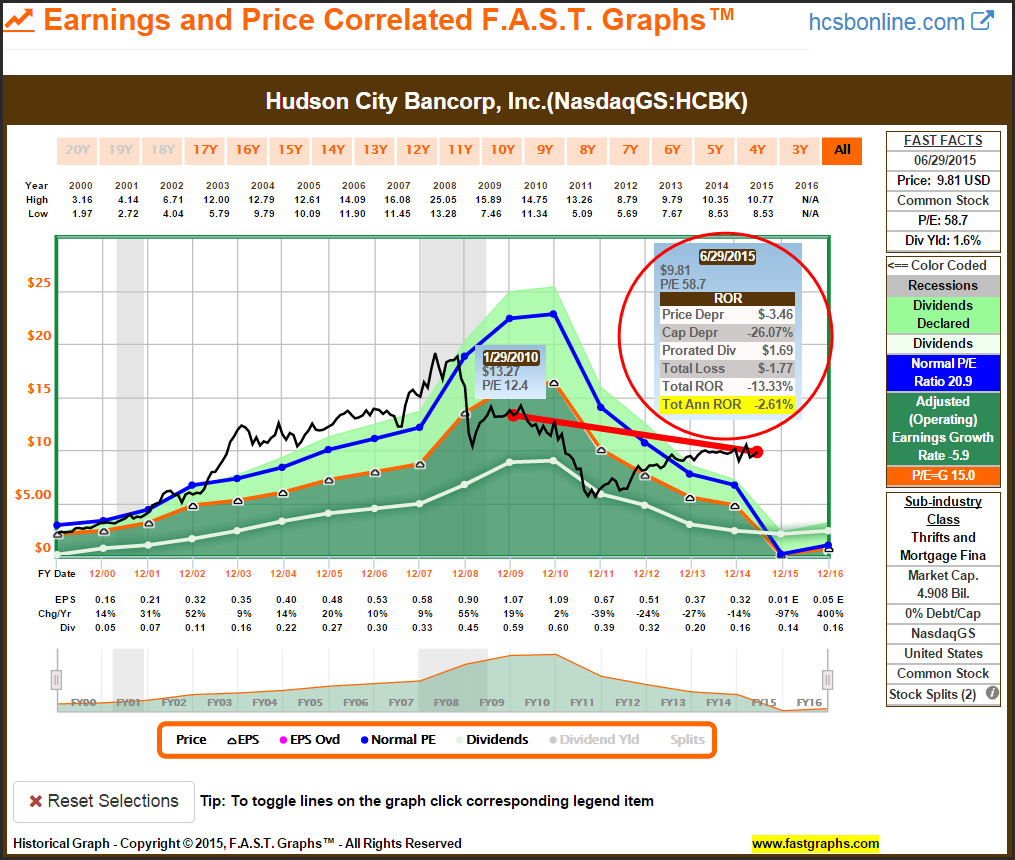

Hudson City Bancorp

On January 14, 2010, I wrote a strong recommendation on Hudson City Bancorp (HCBK). Although this represents another mistake, the long-term losses have been modest. Even though I am not especially proud of this recommendation, I did learn a lot from the experience.

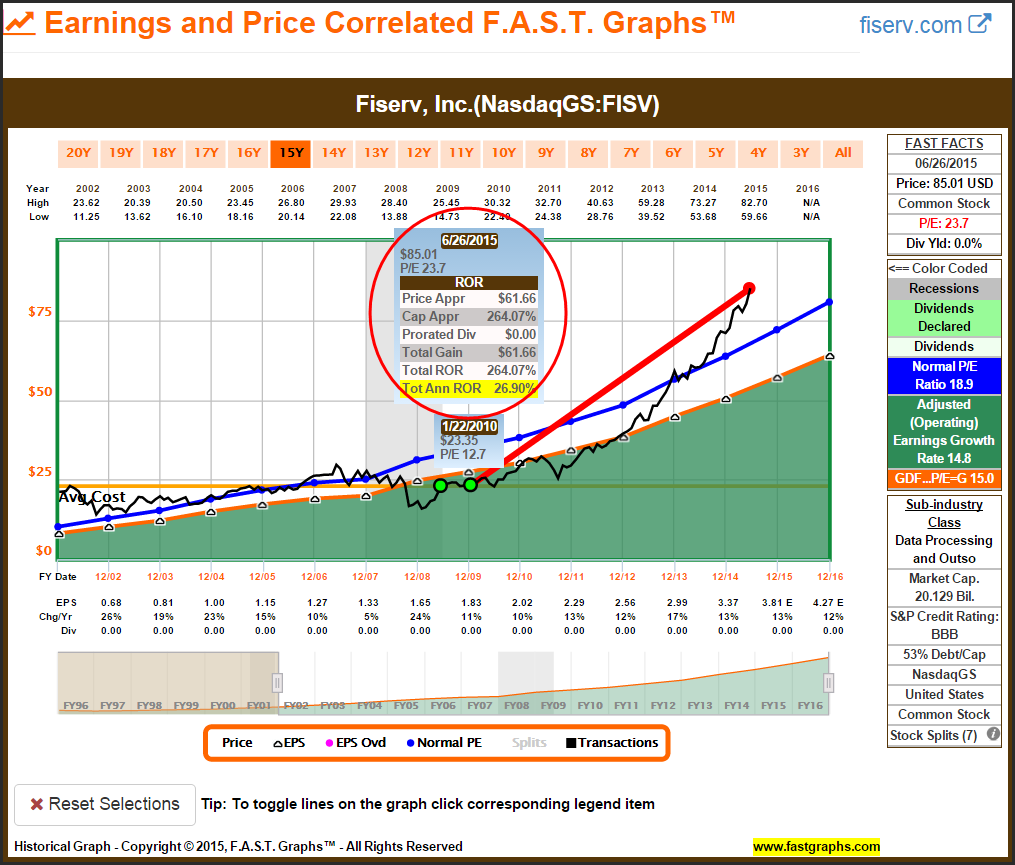

Fiserv (FISV) Article

This was a follow-up to a previous article I wrote on Fiserv in 2009. Valuation remained attractive and the long-term performance has been exceptional. However, current extreme overvaluation contributed greatly. I would be happy if the stock was still trading at a fair value P/E ratio of 15.

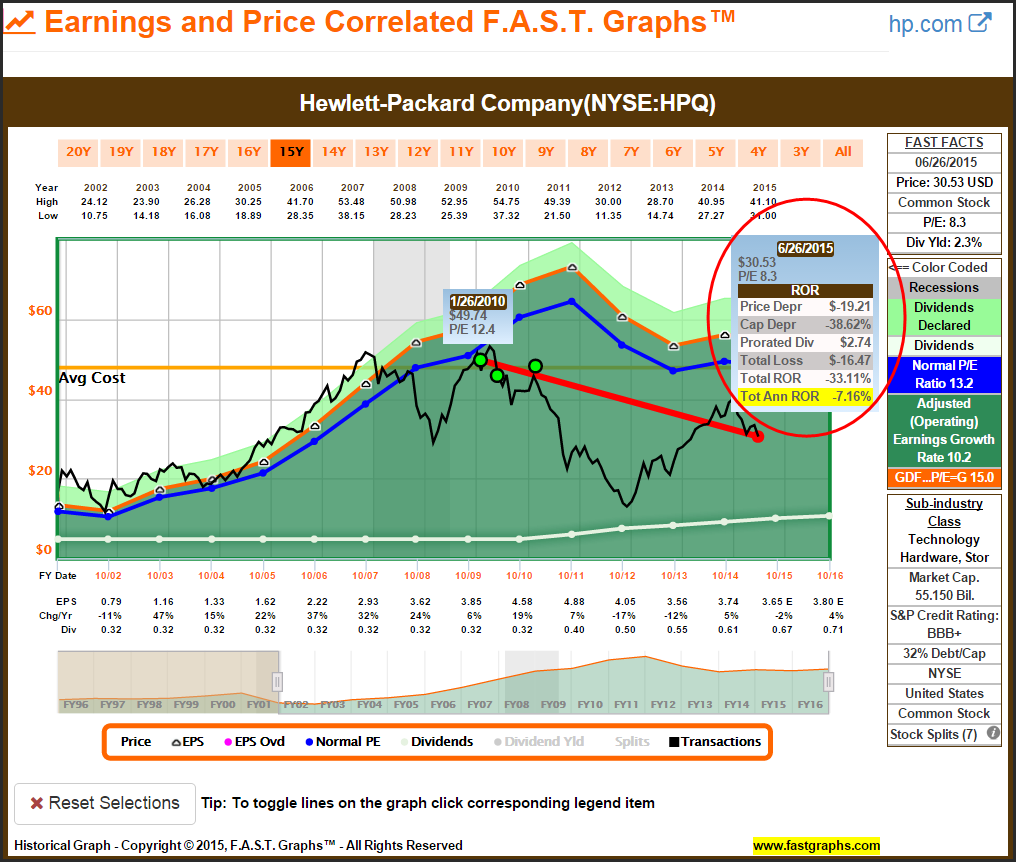

Hewlett-Packard (HPQ) Article

Hewlett-Packard represented another mistake. However, I was long this stock and aggressively added to it in 2011 (not shown on the graph) because I felt that the market had overreacted to temporary earnings weakness. I continue to hold Hewlett-Packard and have a modest profit on the total position.

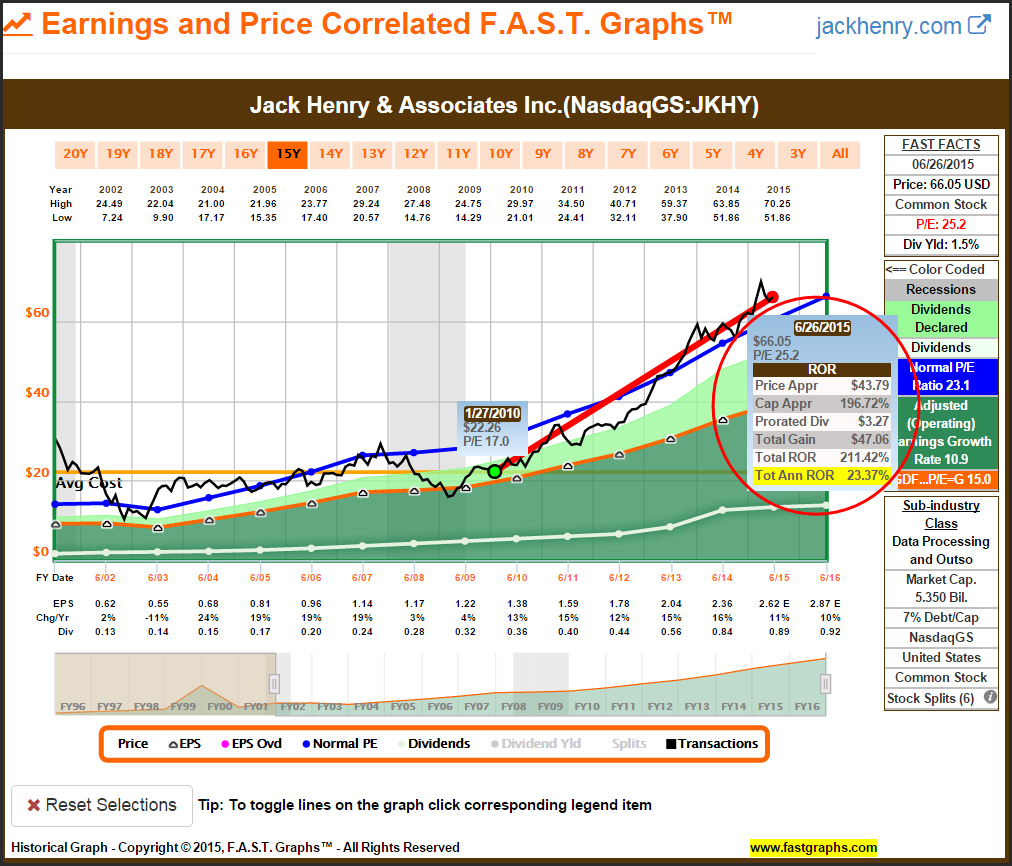

Jack Henry (JKHY) Article

Jack Henry was offered as a high growth dividend growth stock with a modest yield. Performance has been exceptional, but valuation is currently higher than I am comfortable with.

PepsiCo Article

On February 3, 2010, I saw an opportunity to invest in the blue-chip Dividend Champion/Aristocrat PepsiCo (PEP). The opportunity to find a blue-chip dividend growth stock at such an attractive valuation was a rarity that I was happy to see.

To get a free more detailed perspective on the advantage of investing in a blue-chip like PepsiCo at sound valuation follow this direct link to a video on my site mistervaluation.com and watch and listen to me analyze PepsiCo out loud via the FAST Graphs fundamentals analyzer software tool.

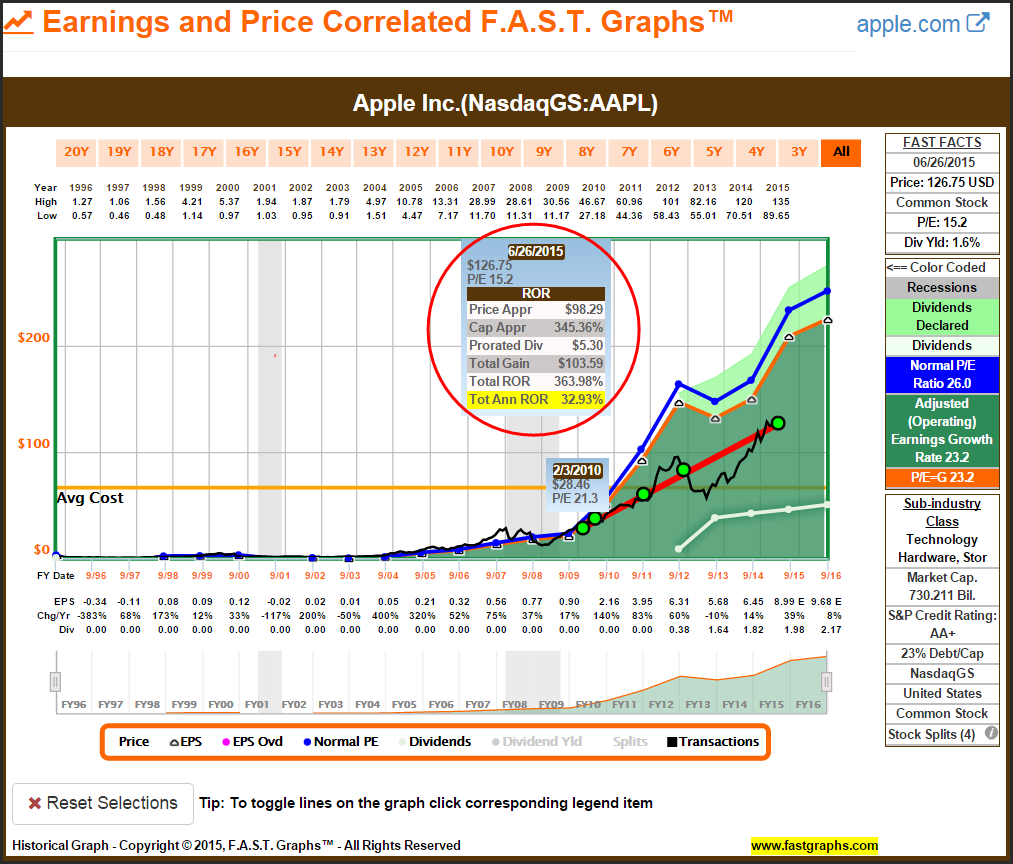

Apple (AAPL) Article

As indicated by the green dots on the graph, I published several articles on Apple and each produced attractive returns thanks to growth and valuation. I am long Apple, and continue to recommend it even today.

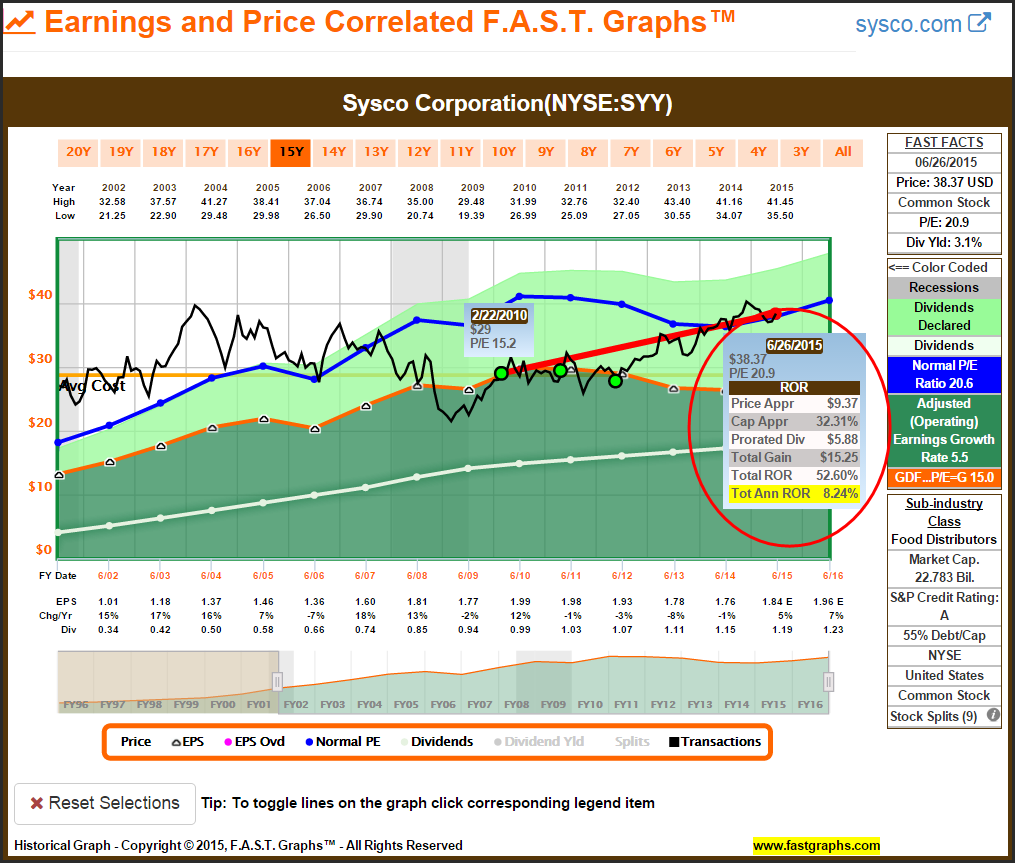

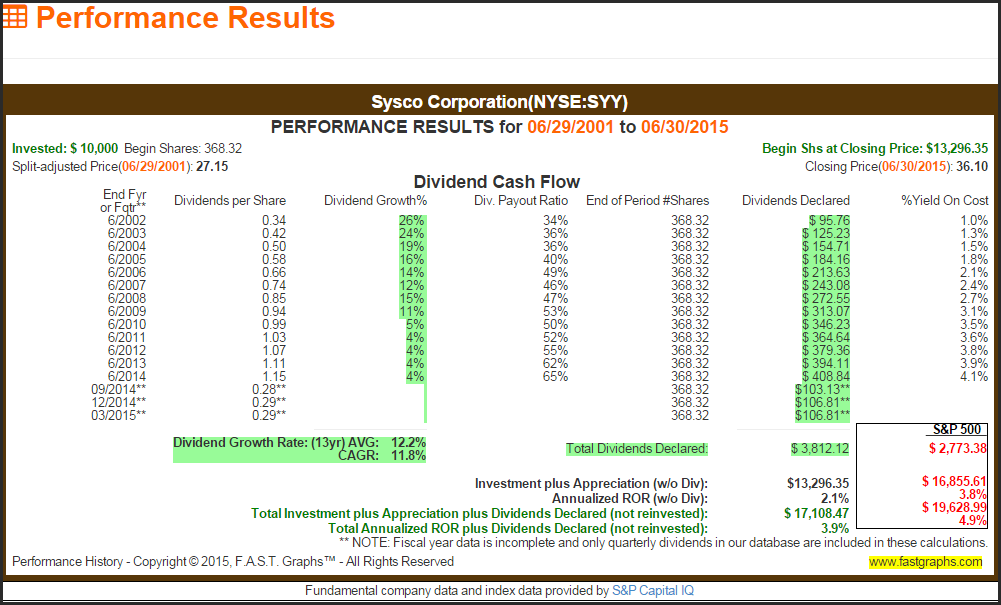

Sysco (SYY) Article

Sysco was offered as an opportunity to invest in a blue-chip dividend growth stock that historically commanded a premium valuation. As time unfolded, the company has moved back towards its historical premium valuation and its dividend has increased each year. Earnings, however, have been a disappointment.

The following performance on Sysco associated with the above graph illustrates one of the nuances of performance calculations discussed above. Although capital appreciation for Sysco modestly underperformed the S&P 500, this blue-chip dividend growth stock produced significantly more dividend income than the index. For the retired investor in need of dividend income, Sysco’s performance was better than the index. This is especially true when you consider that the S&P 500 index froze their dividend in 2007 and cut their dividend by 20% in 2008. Sysco’s shareholders saw their dividend income increase over the same timeframe.

Kohl’s (KSS) Article

Although Kohl’s did not produce the earnings growth I anticipated, the initiation of a dividend in 2011 contributed to positive results. Today the company appears attractive with an above-market current dividend yield and attractive valuation.

Best Buy Article

Best Buy (BBY) was a disappointment even though earnings continued to grow over the next year and a half after I wrote the article. This is a classic example representing the importance of continuous monitoring and due diligence. Best Buy was sold in 2012.

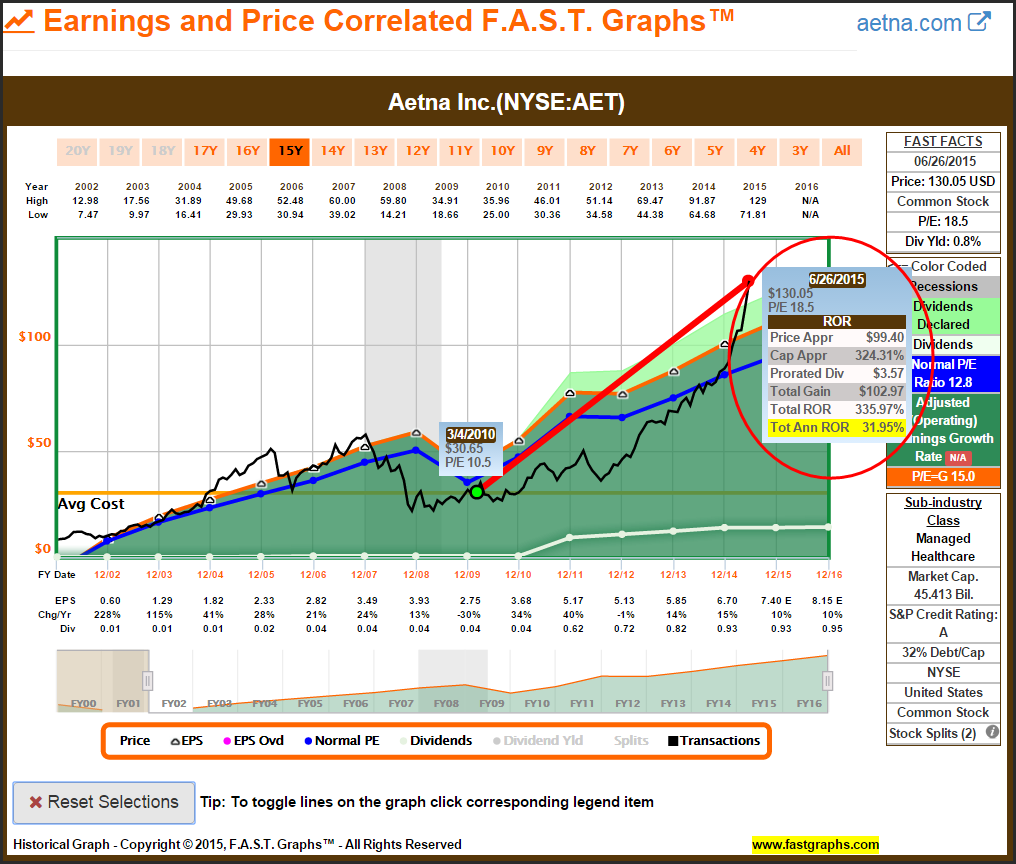

Aetna (AET), United Healthcare (UNH) Article

In March 2005 I presented an article that covered the two primary managed care companies Aetna and United Healthcare. Healthcare reforms created significant undervaluation opportunities for both companies. At the time these were pure growth stocks, today they are dividend growth stocks. However, I consider them both overvalued at this time.

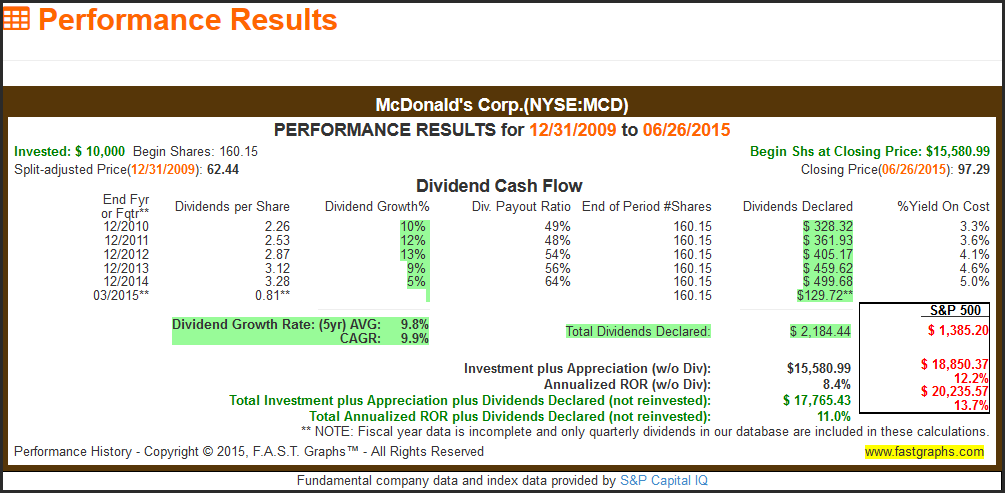

McDonald’s (MCD) Article

McDonald’s was offered as a dividend growth stock with a strong historical record of earnings and dividend growth. Based on past growth, the company was fairly valued at the time. However, earnings growth since the article was published has been disappointing. Nevertheless, as we will soon see, McDonald’s performance, based on dividend income, was attractive as compared to the S&P 500.

The following performance report is produced over approximately the same timeframe since the article was published. Although McDonald’s underperformed the S&P 500 based on capital appreciation due to weaker-than-expected earnings growth, total cumulative dividend income significantly exceeded the S&P 500.

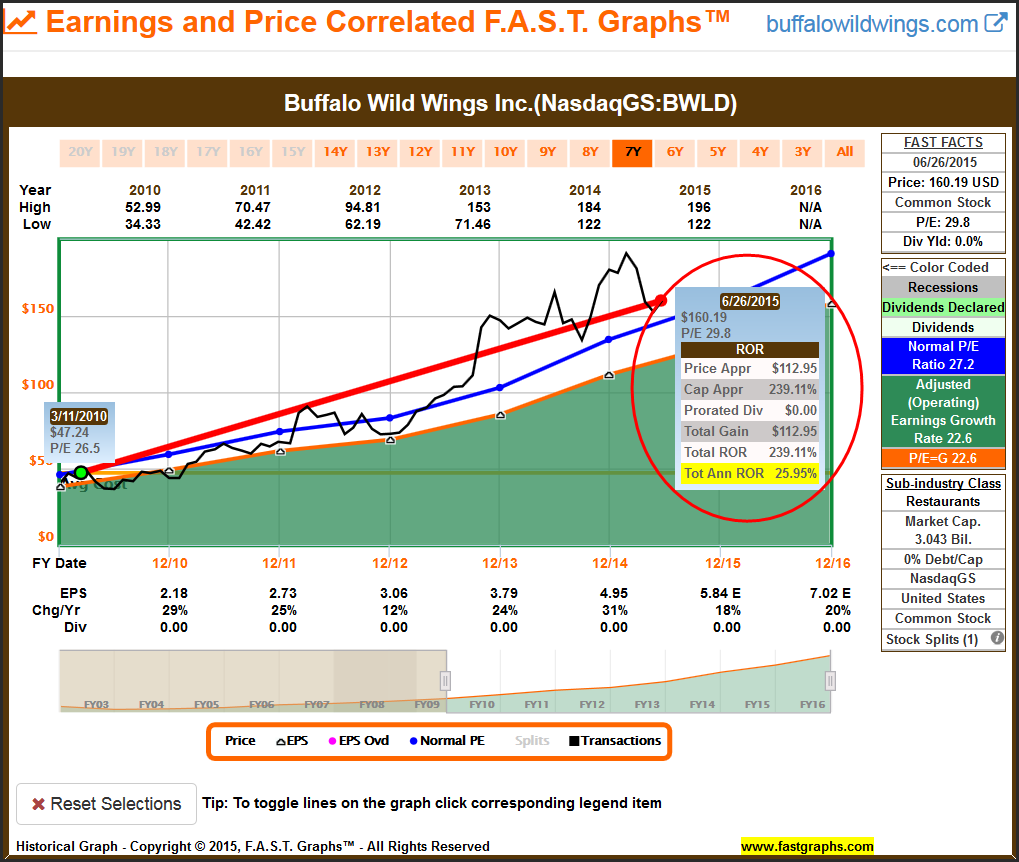

Buffalo Wild Wings Article

On March 12, 2010, I offered Buffalo Wild Wings (BWLD) as a high growth research candidate. The company has delivered on both earnings growth and price performance. However, I believe the company is currently overvalued.

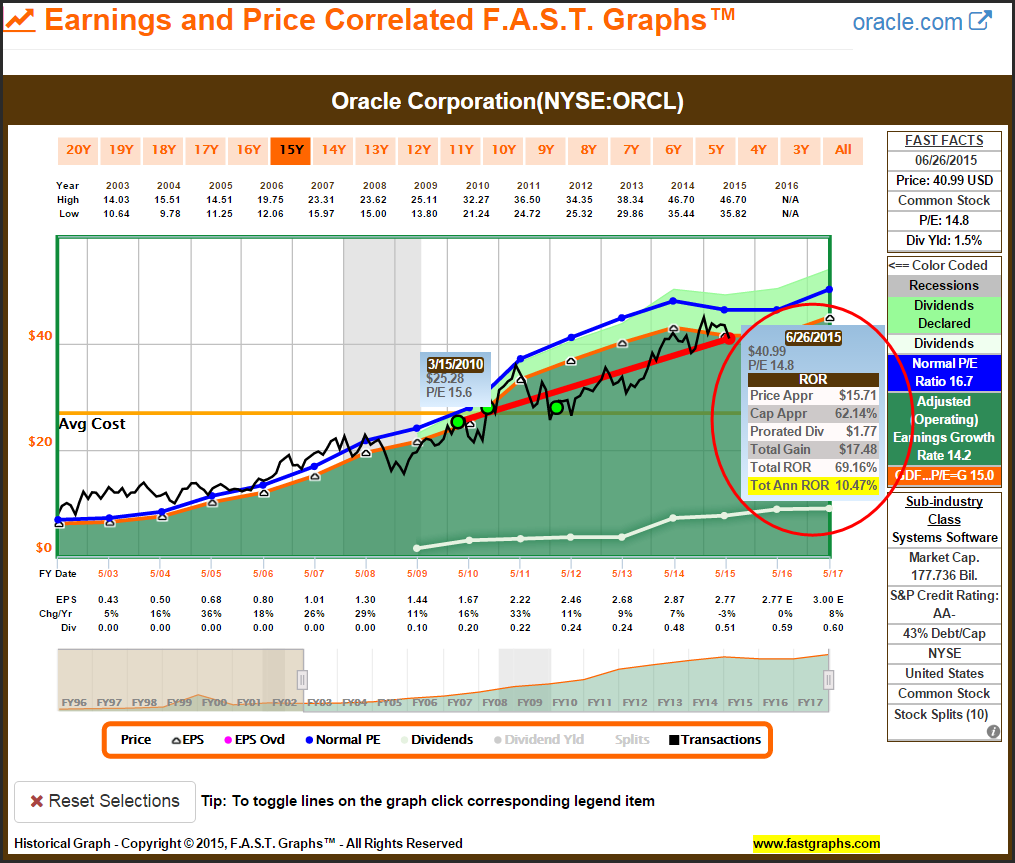

Oracle Article

On March 16, I presented Oracle (ORCL) as an above-average growth stock with a modest dividend yield. This was just after they had acquired Sun Microsystems.

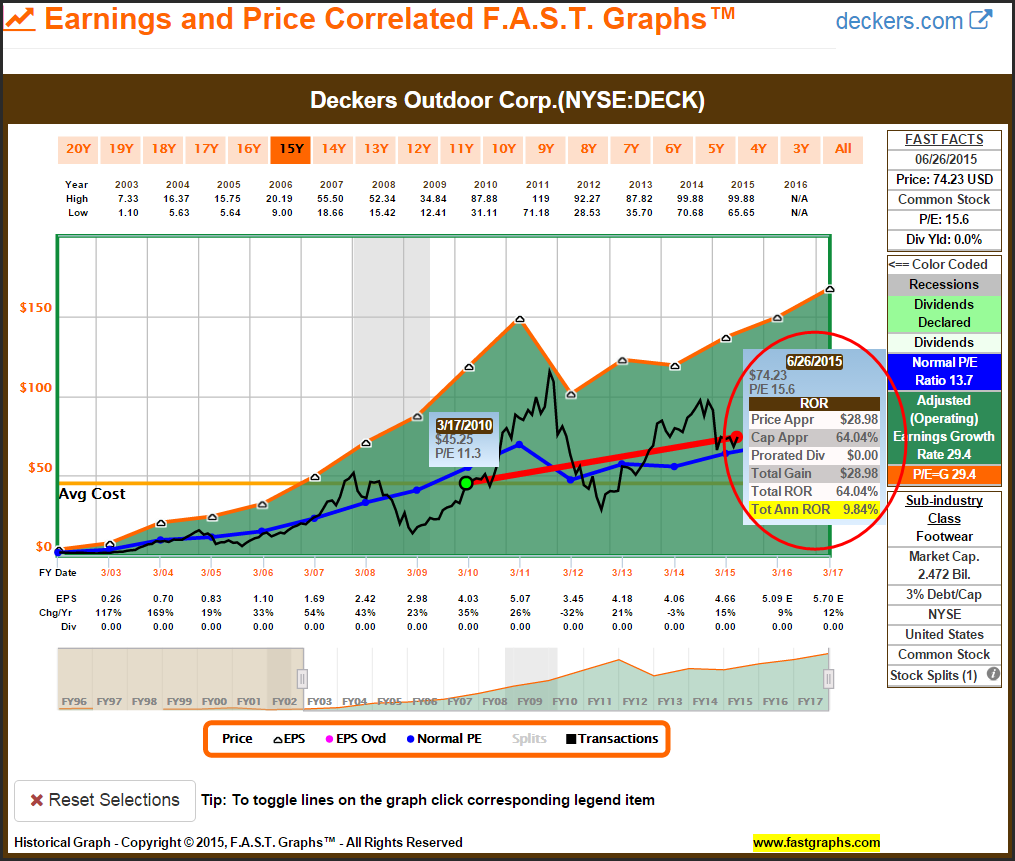

Deckers Outdoor Corp (DECK) Article

Deckers represented another offering to the growth stock investor. Interestingly, earnings and price performance for the years immediately following publication were exceptional, as indicated in the first graph below.

Additionally, as depicted by the next earnings and price correlated graph calculating performance on Deckers to date illustrates the risk associated with investing in high growth stocks. Price volatility has been extreme as a result of an earnings hiccup in fiscal year 2012.

GameStop Corp (GME)

On March 25, 2010, I was attracted to GameStop based on extremely low valuation. This company has been much maligned by Wall Street. However, the company has continued to produce solid earnings and has since morphed into an attractively-valued dividend growth stock.

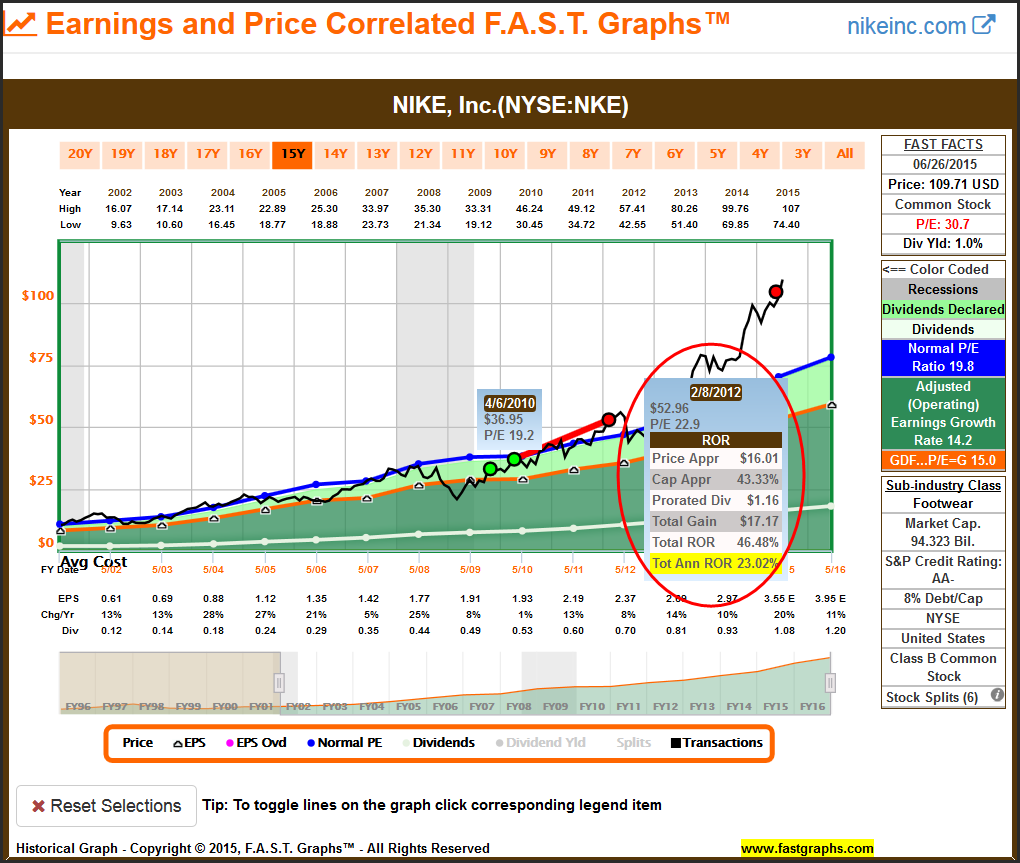

Nike (NKE) Article

I recently published an article on Nike where I asked if we could trust its current stock price. The article received significant pushback from Nike fans. In the article I stated that Nike was one of my favorite companies, and it still is. The only thing I don’t like about Nike is its current high valuation. This article published on April 8, 2010, illustrates that I truly like Nike when its valuation was sound.

Ross Stores (ROST) Article

Ross Stores was offered as a quintessential example of a consistent earnings and dividend producer. Performance has been exceptional, although I consider the company overvalued currently.

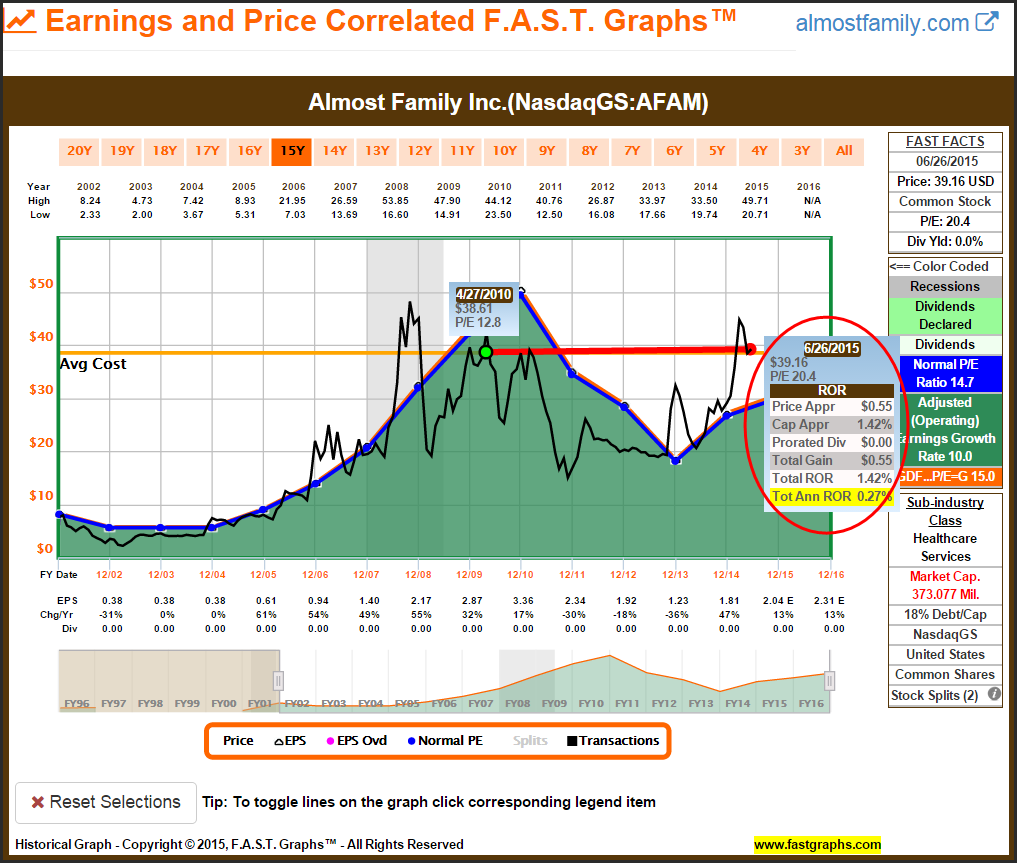

Almost Family Inc (AFAM) Article

On April 28, I presented Almost Family Inc as an attractively-valued growth stock in the healthcare sector. This represents another example of the risks associated with investing in pure growth stocks.

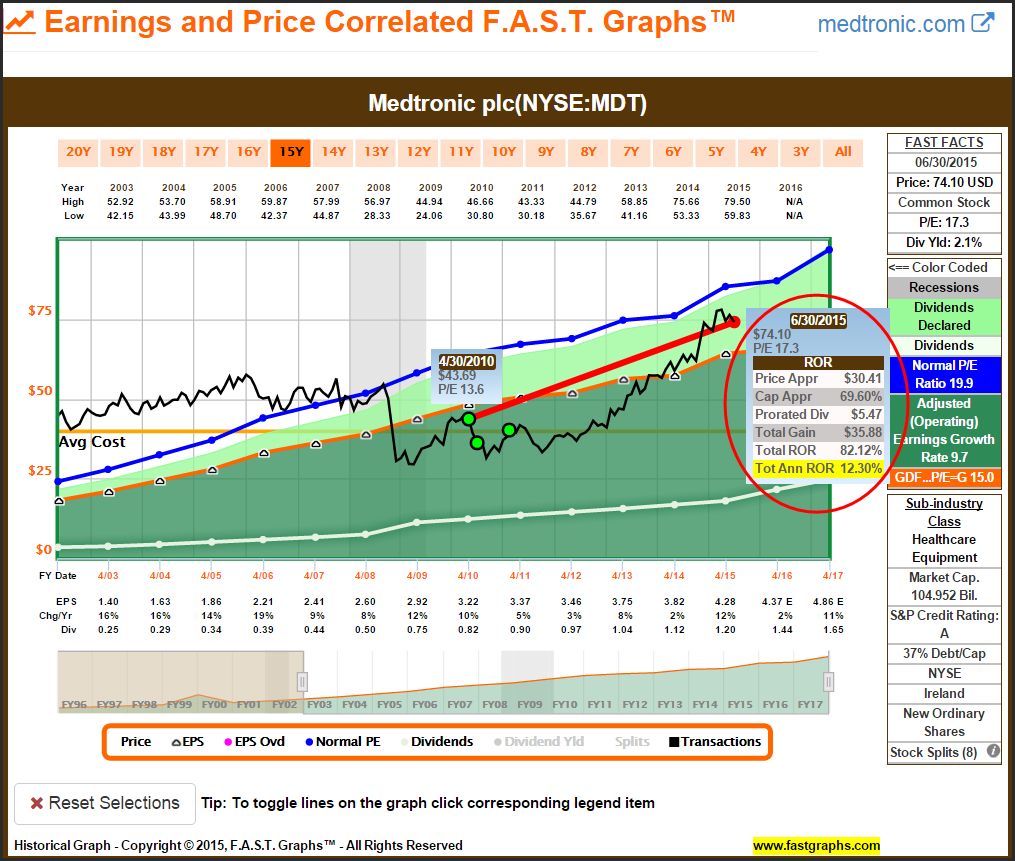

Medtronic Article

Medtronic (MDT) was a blue-chip dividend growth stock that I waited years to find at attractive valuation. As indicated by the additional green dots on the graph, I continued to write about this company as it remained undervalued over the next few years. Since that time performance and dividend growth has been very attractive.

Cognizant Technology Solutions (CTSH)

On May 10, 2010, I published a second article on Cognizant as a high-quality growth stock. This represents an example where growth stock investing can be attractive.

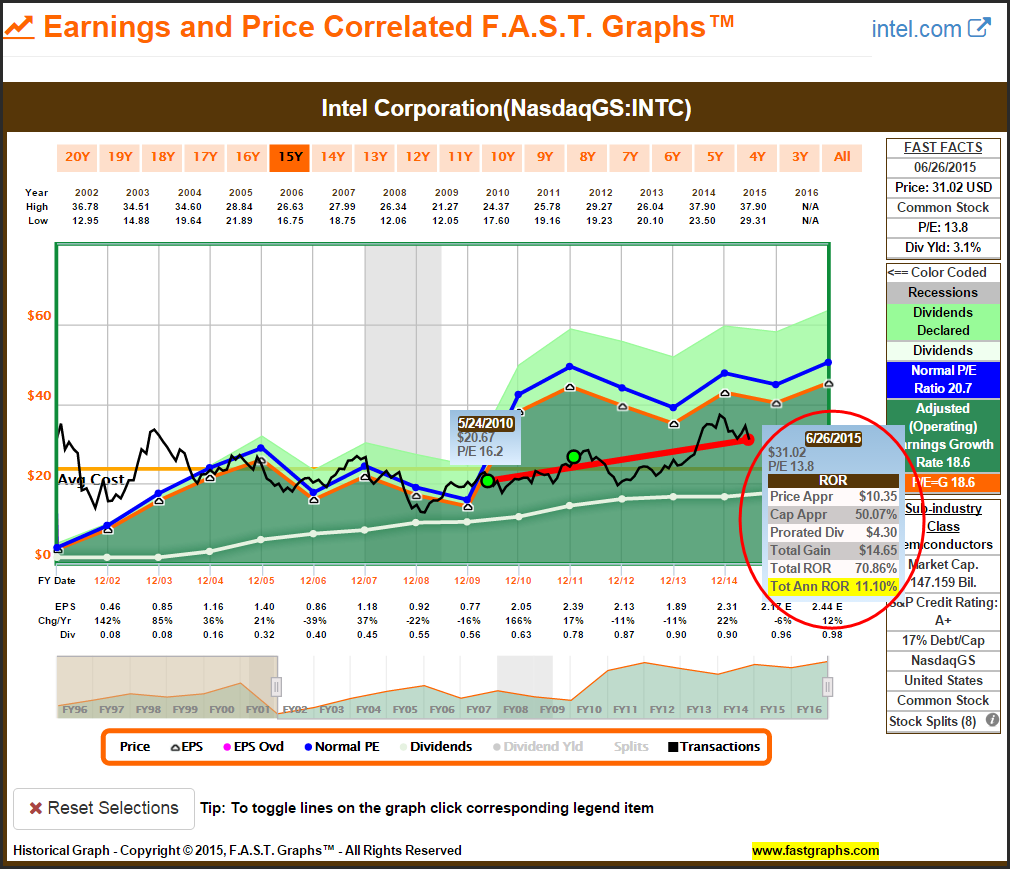

Intel Corporation (INTC) Article

Intel was offered as an undervalued tech stock that was morphing from a quasi-cyclical growth company to a dividend growth stock. I felt the company was undervalued at the time I published the article.

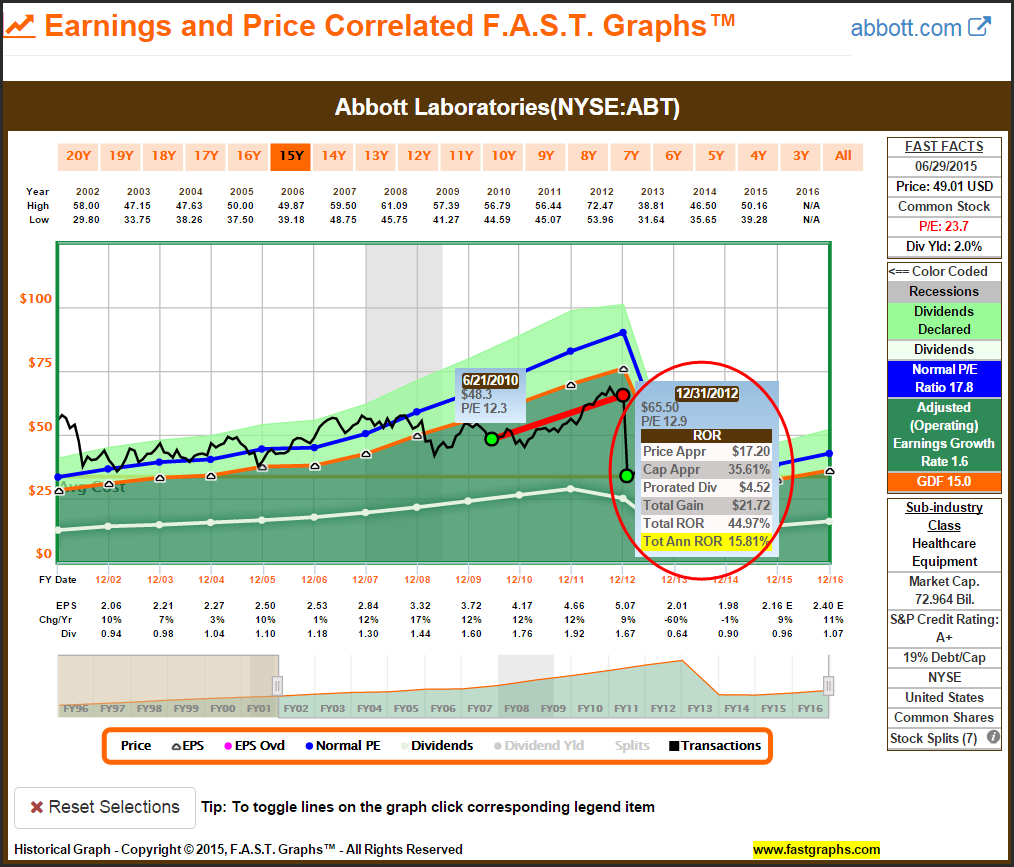

Abbott Laboratories (ABT) Article

Abbott Labs was presented as a high-quality blue-chip dividend growth stock on sale. Subsequent to the article originally being published, the company split into two separate entities. Consequently, the first Abbott graph calculates performance from the time the article was published to the spin-off date indicated by the red dot on the first graph.

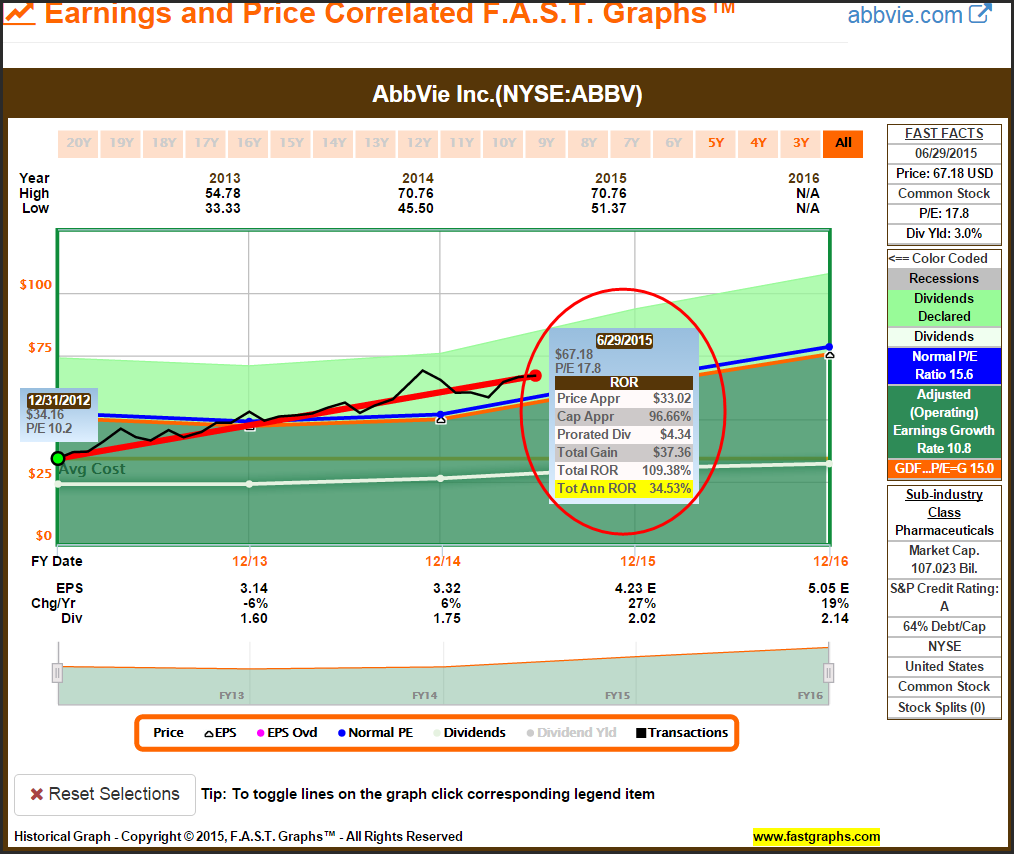

This second graph calculates performance of Abbott after AbbVie (ABBV) was spun-off. In order to get a complete comparison of how the Abbott Lab research recommendation performed, you have to include both calculations. Note the apparent big price drop is not an actual fall in price. Instead, it simply represents the resetting from the combined company to the single company.

To complete a full analysis of the Abbott recommendation, you have to also include the performance of AbbVie post spin-off.

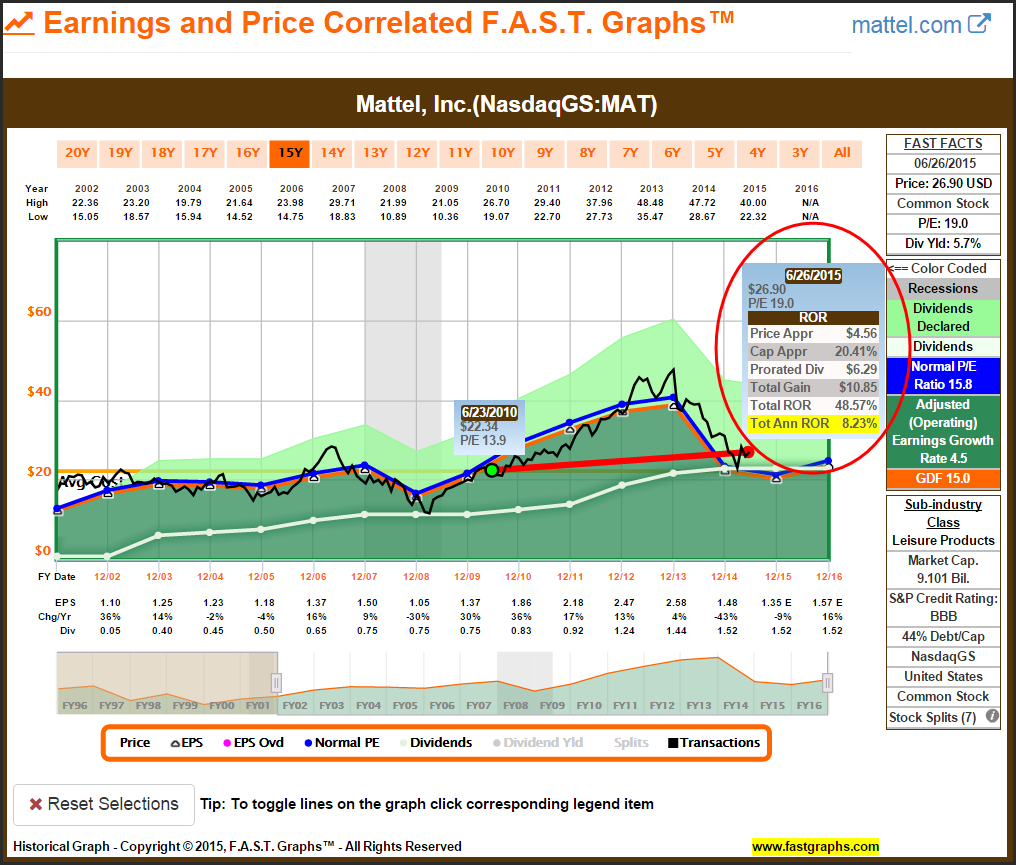

Mattel Inc (MAT) Article

The Mattel research recommendation worked out quite well for several years following the publication of the article. However, this example represents the importance of continuous monitoring and due diligence.

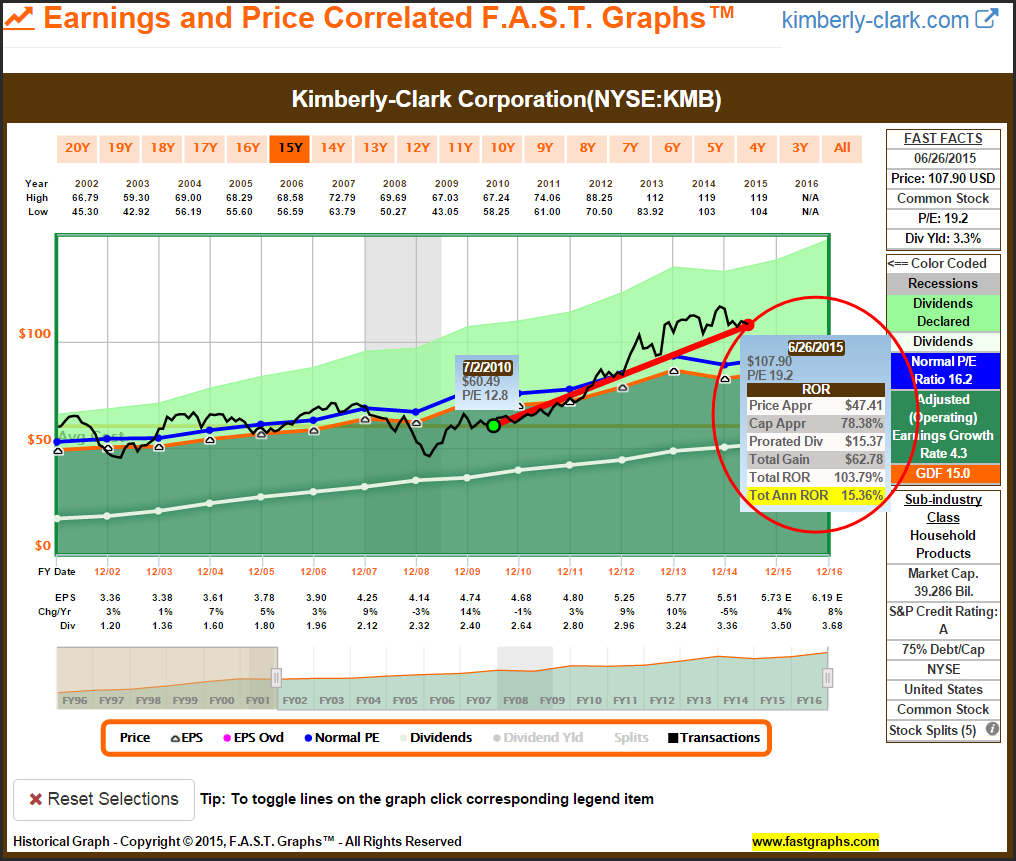

Kimberly-Clark Corporation (KMB) Article

Kimberly-Clark was offered as an undervalued blue-chip dividend growth stock in July 2010. Although performance has been excellent, I do consider the company moderately overvalued currently.

Automatic Data Processing (ADP) Article

Automatic Data Processing has a long history of commanding a premium valuation. Consequently, I was attracted to the company on July 13, 2010, when valuation was historically low.

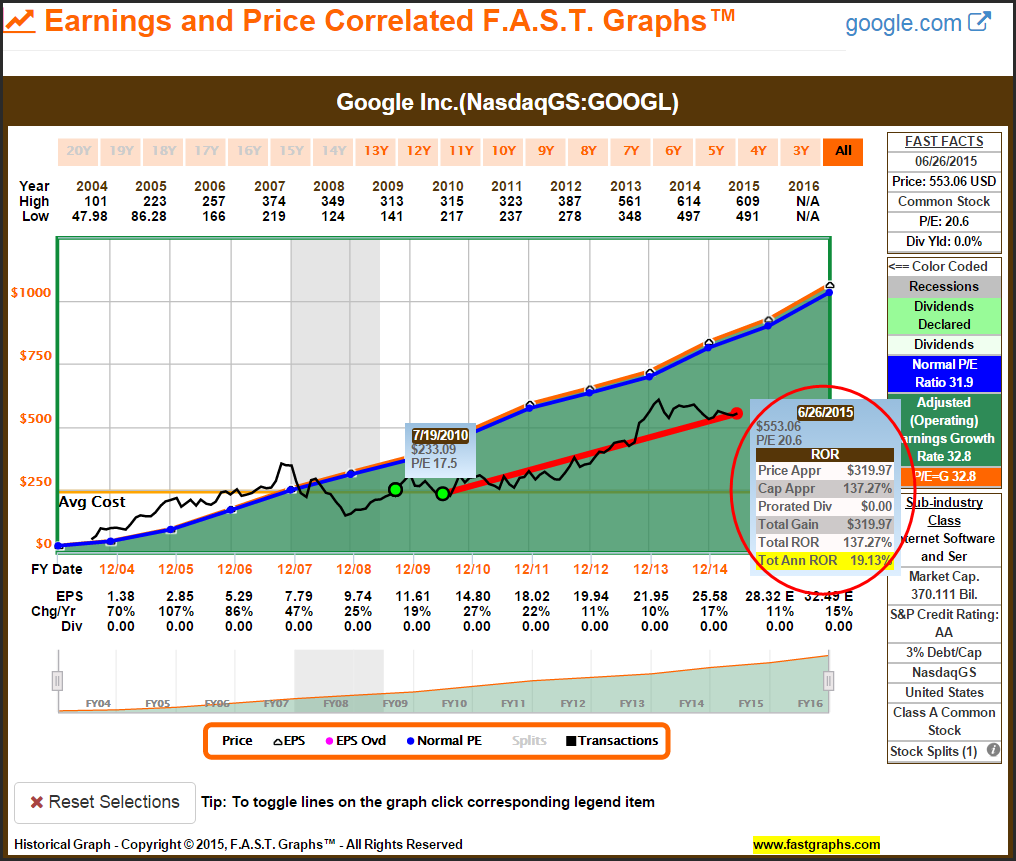

Google Inc (GOOGL) Article

After my growth stock recommendation Google had fallen modestly from my first article in 2009, I considered it even more attractively valued. Over the long-term, both Google recommendations have performed well.

S&P 500 Index Article

Finally, on July 25, I published another optimistic article on the S&P 500. Once again, I received significant pushback as evidenced by the comments included after the following graph.

“I think that when SA editors assigned the title for this (which they do), they should have called it something like "Needs An OpTOMITRist Argument". My pessimism made me a fortune in 2008, and I am continually given Every reason to expect the next few years to be more like 2008b than 2009/10.

But I'm glad this fellow exists, as I have to buy my puts from someone.”

“You're never going to get a bull to admit that ridiculous stimulus cannot be repeated and surely can't be counted on for next earnings let alone growth from these levels”

“Well Chuck, I'm very frustrated with the nonsensical cheerleading in the face of real structural imbalances of our economy. Going from one fiat bubble to another is nothing to be proud of as an American or to base long term economic prosperity on.”

Summary and Conclusions

This series of articles was presented as a review and accountability of my first year’s worth of publishing. Importantly, this provides an appropriate long-term period of time in order to access results. However, my intention was not to boast about how well my work has panned out. More importantly, I felt this review contains important lessons on valuation and performance reporting.

Although some of these selections have produced extraordinary results, it’s vitally important to recognize that much of it has come from current overvaluation. This represents what I mean when I say that measuring performance without simultaneously measuring valuation is a job half done. Just looking at numbers is not enough. In my opinion, it’s more important to understand how and why those numbers were generated.

I hope this series of articles provided the reader deeper insights into understanding and evaluating performance measurements.

Disclosure: Long AFL, FISV, HPQ, PEP, AAPL, SYY, KMB, KSS, ABBV, ABT, MDT, ROST, ADP, UNH, ORCL, MCD, DECK, CTSH, INTC, GOOGL at the time of writing.

The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.