I believe that one of the most important attributes that a successful investor must possess is optimism. Any serious student of financial history would recognize and acknowledge that economically speaking, things are good much more often than they are bad. In the general sense, common stocks have risen far more often than they have fallen. That is not to say that bad times never come, because they most assuredly do. However, even during bad times optimism has served investors better than pessimism. The rational optimist recognizes that bad times are only temporary, and better times are sure to follow.

Consequently, the rational optimist sees the future opportunity that bad times provide and behaves accordingly by investing aggressively. In contrast, the more emotionally-driven pessimist sees only risk, which all too often provokes them to flee their investments and suffer unnecessary losses as a result. A paper loss is most often temporary, and only becomes real if you take it. This is especially true when the underlying fundamentals of the business support a higher valuation. When this is true, I contend there are only two rational choices. Hold onto your intrinsically more valuable assets recognizing that they will recover or if you have the wherewithal, aggressively add to your holdings and exploit other people’s folly.

Although my educational background is in economics and finance, I also completed a minor in psychology. How people behave and think has always been a fascination to me. However, I was more interested in finance, especially investing, which is why I made it my career. Nevertheless, my interest in psychology led me to interesting observations about how people think and behave. Many times in my life I have encountered people that possess mountains of wonderful blessings to be thankful for, but who also have a thimble full of problems or life issues. Invariably, or at least all too often, they will turn their backs on their mountains of blessings and obsess on the fewer problems they have.

Moreover, in my personal experience there is a rather disturbing differentiation between pessimists and optimists that I have personally observed and often encountered. Optimists tend to be happier and usually kinder when dealing with others. In contrast, pessimists tend to be gloomy and often meaner when dealing with others. If you don’t believe me, try presenting an optimistic article, as I often have, and see the responses you get.

As a case in point on July 25, 2010, shortly after the Great Recession had ended, I posted an article titled “S&P 500: The Optimists Argument” and I opened it with the following :

“The American Dream"

I believe we live in the greatest country in the world. Furthermore, I believe our country has the long-term track record to back up those beliefs. Therefore, I am very frustrated by the perma-pessimists, doom and gloomers and naysayers who are quick to write our country and its future prosperity off.

To be sure, we are facing many severe economic challenges and problems. On the other hand, this is nothing new, as we have faced similar and even greater challenges many times in the past. Yet through it all, thanks mostly to our diverse and courageous people, we have not only persevered, we have prospered and grown as well.

The American people have a legacy of optimism regarding the future which is more commonly known as "the American dream." This optimistic viewpoint has served as a beacon to the rest of the world leading many to immigrate into our great country in order to participate in our great social experiment based on free enterprise.

Winston Churchill is credited with a quote that I believe sums up my point succinctly: "A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty." Yes, as I already stated, we are facing many difficulties, however, I remain confident that our people and our economy will rise to the challenge and, as a result, new opportunities will emerge out of these crises.

There are numerous pundits, including the majority of mainstream media that seem to take great glee in writing frightening stories with extremely negative headlines that I believe serve no real purpose other than shaking people's confidence in our economy and their future.”

It’s important to consider that those words were written in July 2010, more than a year after the Great Recession had ended. Later in this article I will provide a link to the above article and include a few comments from readers that it generated. I believe you will find they support my above statement about the perils of writing a positive article.

Related Attributes of Successful Investors

Additional attributes of successful investors that go hand-in-hand with optimism are embracing a long-term view and tempering optimism with realism. Although successful investors have a strong faith in our economic future, they are also smart enough to make realistic assessments about important fundamental metrics such as current valuation.

Optimism and faith in our future are important and profitable attributes to have, but blind faith can lead to denial, and as such, can be financially dangerous. Similar to fear and greed, denial is an emotional response. In contrast, rational optimism is supported by analysis based on an intelligent assessment of the facts. Even more importantly, rational optimists conduct continuous monitoring and evaluation of their past behaviors and decisions in order to learn as much as they can from the past.

Friends and Family Call Me a Perpetual Optimist

All of my life, my closest friends and family have called me the perpetual optimist. In many cases it was meant as a criticism, but in others as a compliment. Personally, I have always considered it a compliment. In truth, I have always felt that my optimistic viewpoint about life and as it pertains to this article, about the economic strength of our country, was a blessing. However, as it specifically relates to investing, my optimistic viewpoint should also lead to profitable transactions. Fortunately for me, that has proven to be the case over the long run. All of my transactions have not been profitable, but on balance, my optimism, my long-term approach and my focus on valuation have served me quite well.

The Proof Is In the Pudding

To be crystal clear, the primary thesis behind this series of articles is that optimism is an important attribute for successful investing. A secondary thesis behind this series of articles is that successful investing implies taking a long-term view when investing in common stocks. By long term, I am referring to investing in and owning a business for a minimum of a normal business cycle of 3-5 years, but preferably longer. As Ben Graham so eloquently put it “in the short run the market is a voting machine, but in the long run it’s a weighing machine.”

In conjunction with my primary and secondary thesis referenced above, is the importance of monitoring and evaluating past decisions, because only then can one determine whether or not optimism is justified. As I was contemplating this, it occurred to me that I have been publishing articles on financial blogs such as Seeking Alpha since June 11, 2009. Therefore, that timeframe of almost exactly 6 years qualifies under my definition of long-term stated above. My how time flies when you’re having fun!

Consequently, this provided a venue that would allow me to monitor and evaluate the validity of my optimism and long-term view. Thanks to the convenience and calculating power provided by F.A.S.T. Graphs™ I could offer my loyal readers a rather comprehensive perspective of how my work and positive attitude has panned out. Therefore, what follows is a wide ranging look back at my first year’s worth of offerings where I presented fairly valued research candidates for readers to consider. In this Part 1, I will cover my recommendations through the end of 2009. In Part 2, I will complete the analysis with a review of recommendations made through June of 2010.

A couple of caveats about this exercise are in order. What I am presenting here is a factual performance calculation based on the closing price of each company one day prior to the article’s publication. However, since F.A.S.T. Graphs™ only reports monthly closing prices on the historical graphs, my calculations will be close but not perfectly accurate. In other words, my starting calculation will be presented on the last trading day of the month prior to or directly after the date the article was published. This gets me within two weeks of when the article was originally presented. However, these calculations are precise enough for the reader to receive a general perspective of the outcome of my recommended research candidates.

Importantly, I only present articles where I covered a single company in my first year of writing. However, I also include a few examples where I wrote about the S&P 500 index as a proxy for the market. These articles are especially interesting because they highlight the pushback I received from strong reactions of readers that held a more pessimistic view of the market and our economy. On these S&P 500 index articles specifically, I will include a few comments that answer the question posed in the title of this article. In short, what has a pessimistic view of our market and economy cost them? The answer is vividly revealed by the S&P 500 articles and performance calculations below.

At this point it’s important for me to interject that this is not an exercise meant to brag about how smart I have been. As I previously stated, not all of my research candidate recommendations were profitable. I have included the good, the bad and the ugly. On the other hand, I believe this exercise supports the importance of optimism as it pertains to investing in common stocks. On balance, and as you will soon see, my optimistic recommendations worked out pretty well.

To be fair, I will also add that I did not own all of these recommended research candidates, but I did own most of them. Furthermore, these calculations do not include specific times where I sold. In other words, this is not a precise presentation of portfolio performance; instead, it is simply reviewing the record produced by the individual research candidates based on the publication date of articles. Readers of these articles were free to either ignore, buy and/or sell any of these offerings based on their own needs or views.

On the other hand, I do feel that readers of my work deserve to see what my research recommendations could have produced had they acted upon them. For the reader’s convenience, the heading on each offering provides a link to the original article. But most importantly, I believe this exercise offers important lessons about the importance of only investing when fair valuation is manifest. The importance of valuation, over all other reasons, is why I offer this rather extensive review and look back at my work.

As the reader reviews the following, I ask that they keep in mind that each of these articles were published in the years just after the Great Recession. This is important because it was clearly a time of rampant pessimism on many people’s part.

On each research candidate published in an article I will present two identical graphs. The first graph will be without the calculations applied because they cover up portions of the graph. I’m doing this because I want the reader to be able to clearly see valuation represented by the earnings and price relationship, as well as all the metrics produced in the FAST FACTS boxes to the right.

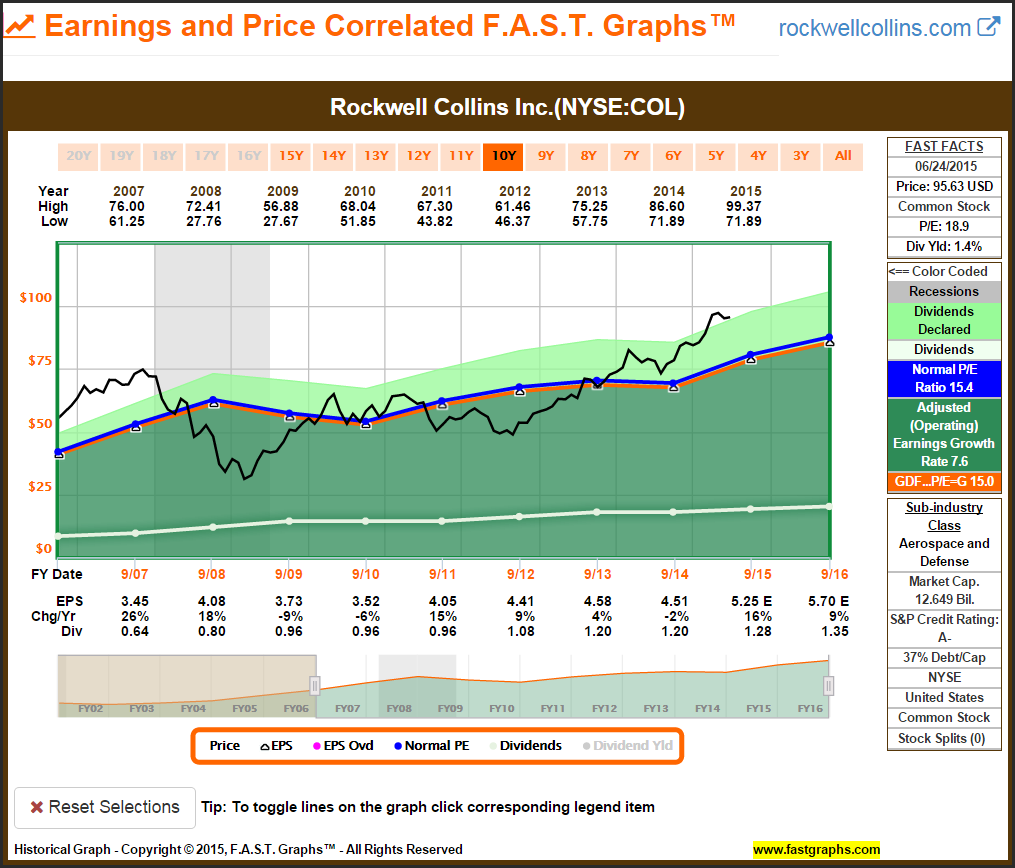

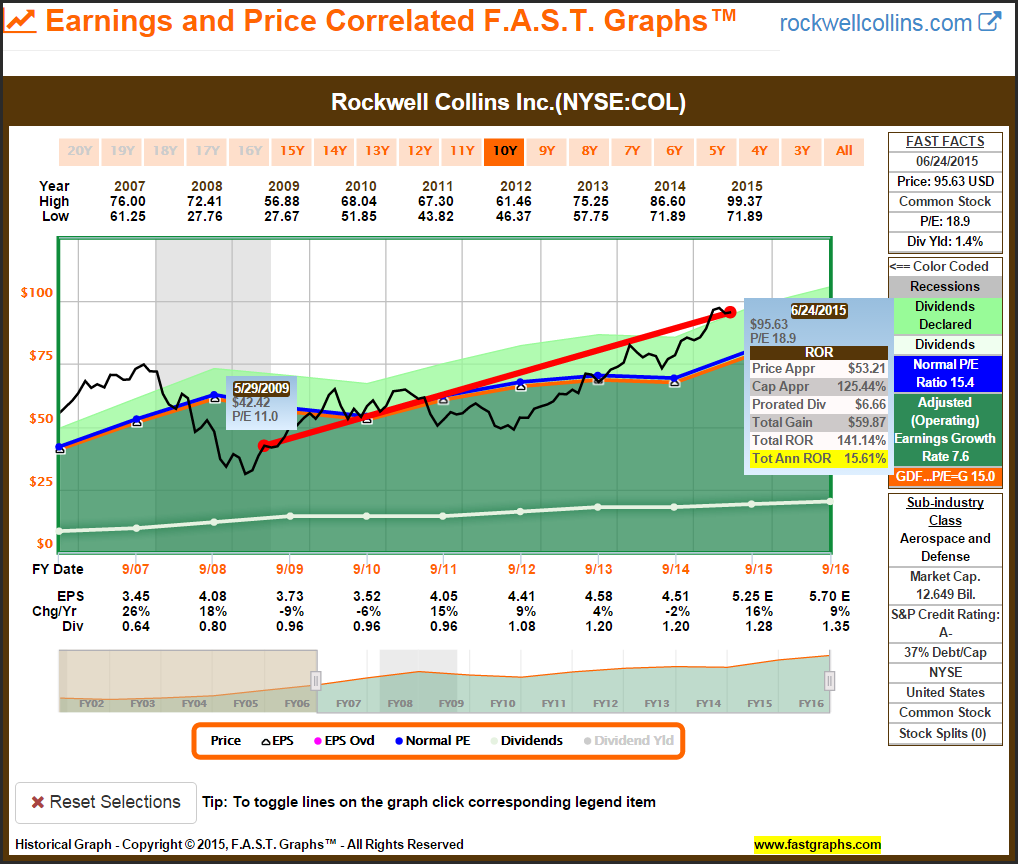

My first article on Rockwell Collins published June 11, 2009

The first article I ever published was on Rockwell Collins (COL), a high-quality semi-cyclical dividend growth stock in the aerospace and defense industry. Even though earnings had weakened during the recession, I felt the valuation represented a compelling opportunity. Clearly this offering has worked out over the long run. However, short-term volatility between when I originally wrote the article and today should be recognized. Additionally, current high valuation has contributed to the results and should not go unnoticed.

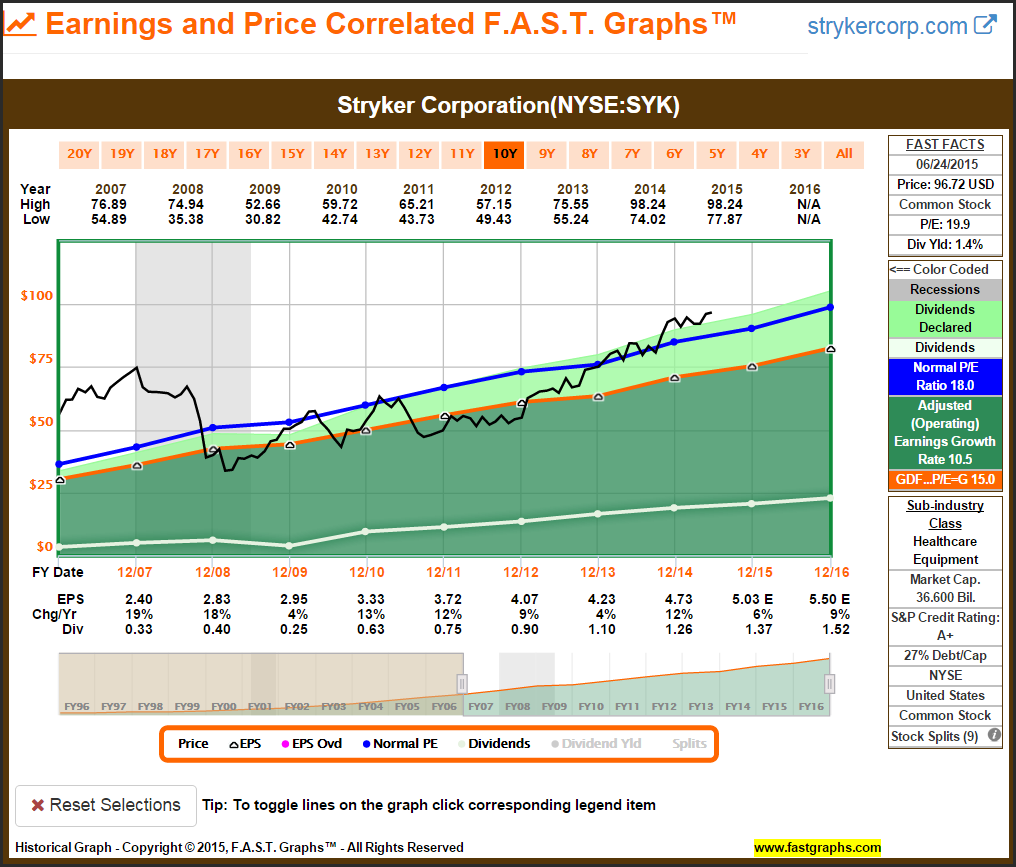

Stryker Article Published June 15, 2009

Stryker (SYK) was a company I had waited years to find at attractive valuation. The results were clearly worth waiting for.

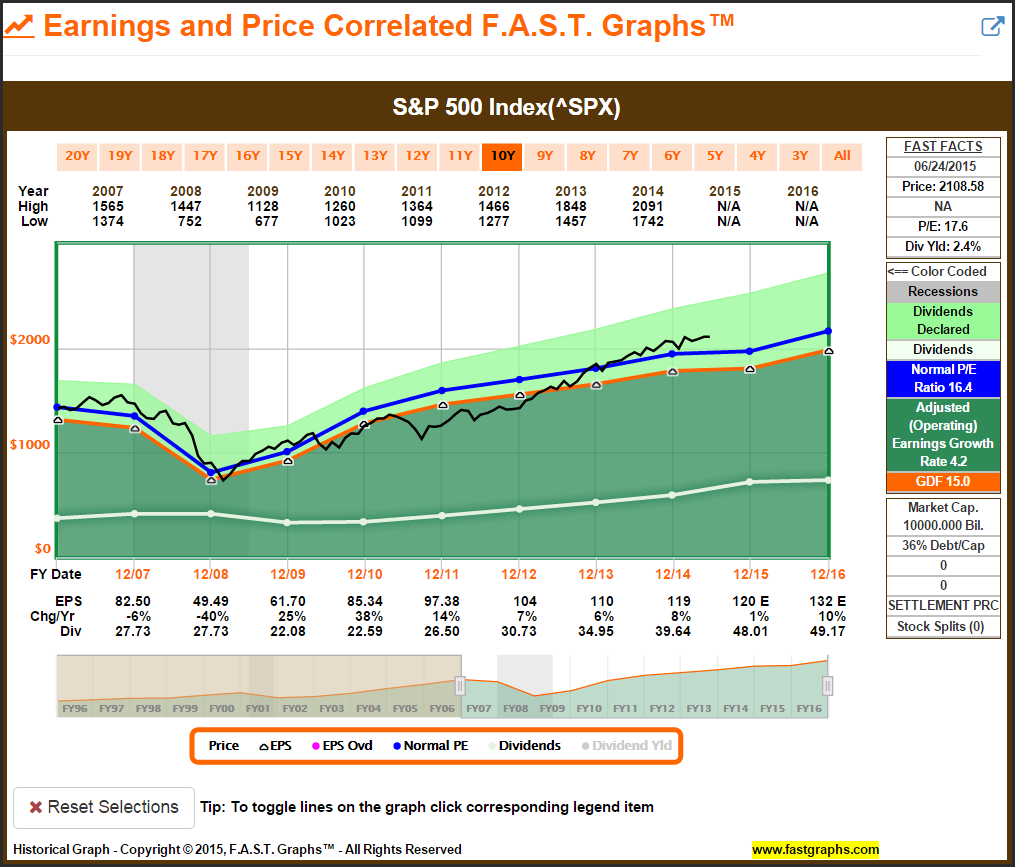

S&P 500 Index Article Published June 18, 2009

On June 18, 2009, I presented an optimistic view of the future potential returns on the S&P 500 based on attractive valuation, coupled with strong forecasts for earnings growth. Many people were not of the mind to accept a positive recommendation on the S&P 500, as evidenced by the pushback I received. I have included a few examples of negative comments following the graphs.

“I could not laugh lauder (I assume he meant louder) to such a well-written piece of rubbish.”

“Your thinking is not faulty but your timing and sense of history are.

You fail to understand the basic premise of the economic era we are in: we are massively overleveraged and we are a long way from deleveraging. In fact, our debt load actually increased last year.

It IS a better time to invest than a year ago but will it have been a good time to invest 5 years from now? My opinion is that the answer is no, but it might be a good time to invest (in the stock market) between now and then.”

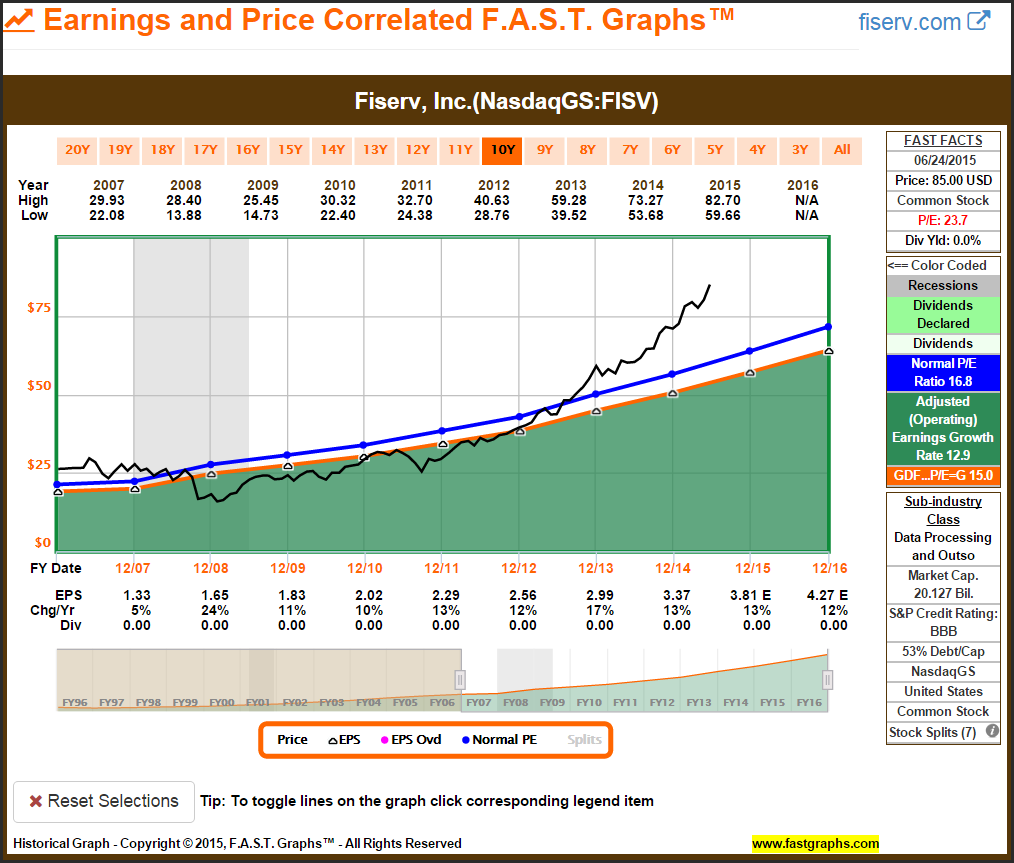

Fiserv Article Published June 19, 2009

When I wrote about Fiserv (FISV) on June 19, 2009 the article was oriented towards growth investors. Although this represents one of my best long-term performers, the extremely high current valuation was a major contributor to those results. I don’t believe in taking credit for the market’s current irrational pricing of this research candidate.

L-3 Communications article published on June 25, 2009

When I wrote about L-3 Communications (LLL) on June 25, 2009, I expected strong earnings growth for the next few years, which did happen. However, since 2012 earnings have been rather flat. Nevertheless, significant undervaluation overcame poor operating performance.

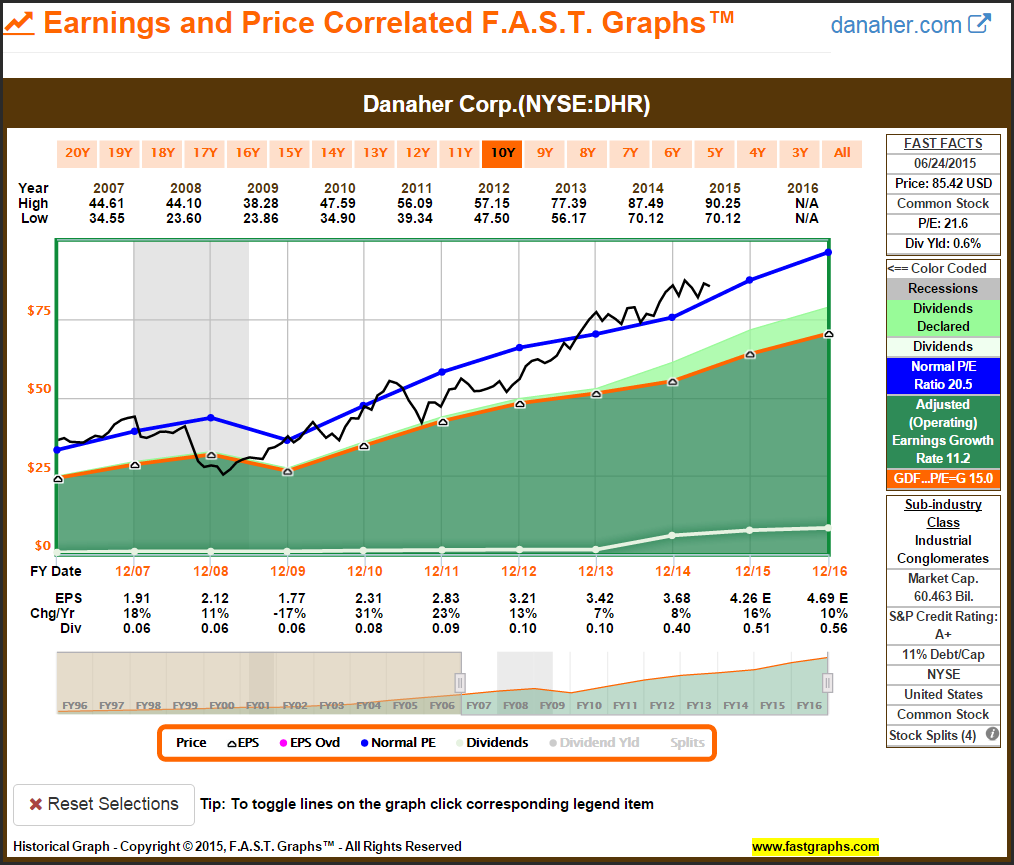

Danaher Corp article published on July 8, 2009

When I wrote about Danaher (DHR) on July 8, 2009, it was offered as a growth stock opportunity available at fair value. Although this research candidate has performed quite well, the continuous high valuation that the market has been applying is a concern.

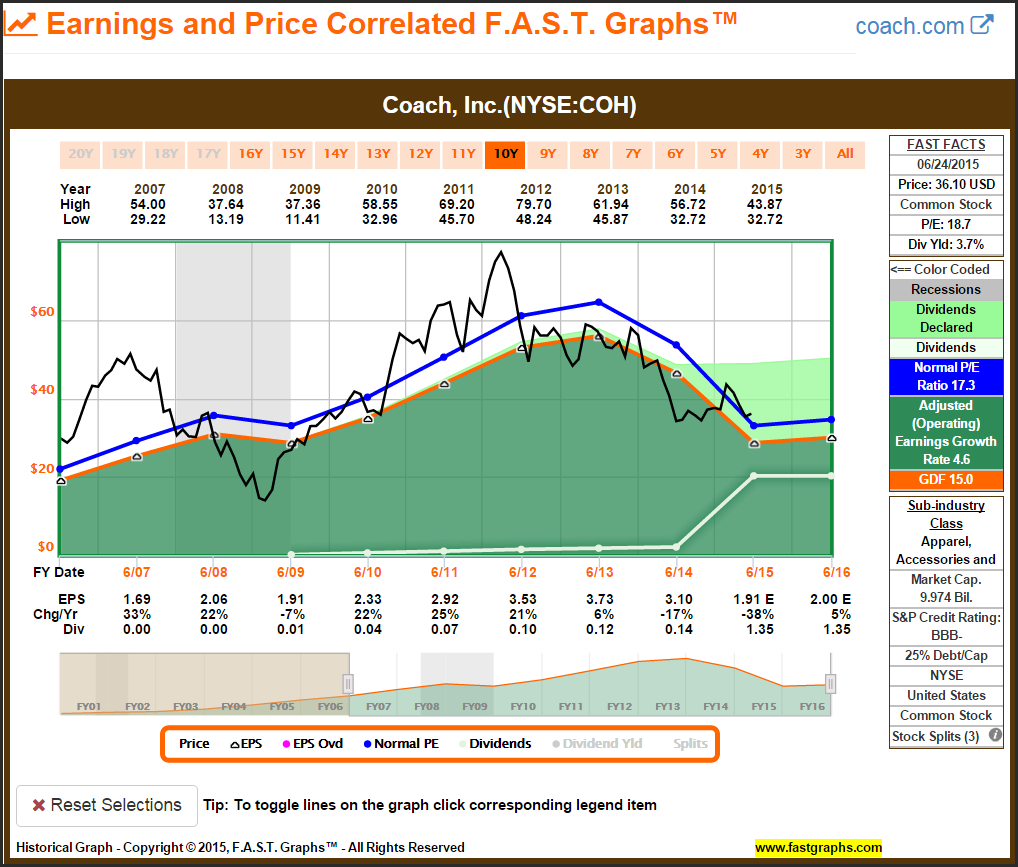

Coach article published on July 16, 2009

When I wrote about Coach (COH) on July 16, 2009, it was offered as a high growth opportunity. The company performed extremely well for the next several years, but I eventually sold based on excessive valuation. Nevertheless, this example clearly illustrates the importance of the earnings and price relationship long term.

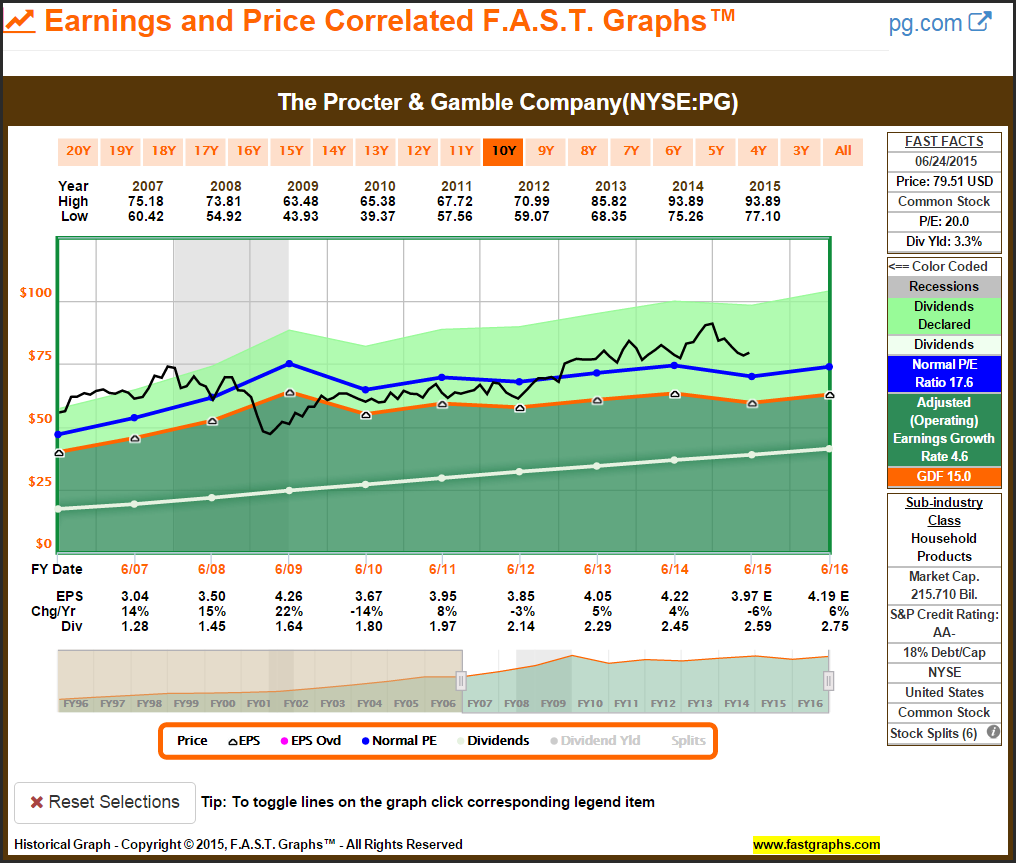

Procter & Gamble article published on July 22, 2009

On July 22, 2009, I presented my first recommendation on the blue-chip dividend growth stock Procter & Gamble (PG). It was offered as an opportunity to invest in a Dividend Champion/Aristocrat at a very attractive valuation that was rare to find.

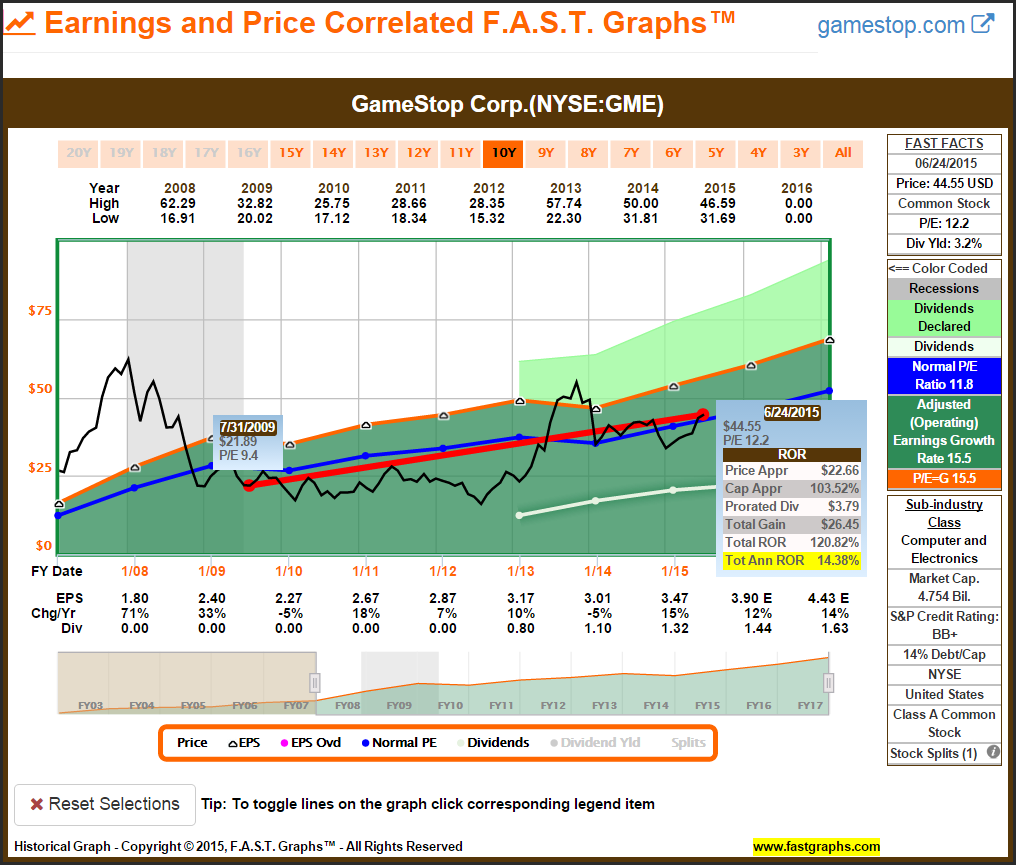

GameStop article published on July 29, 2009

When I wrote about GameStop (GME) on July 29, 2009, it was offered as an above-average growing company available at a low valuation. I got a lot of pushback on this particular example. Nevertheless, it’s interesting to see that the company has subsequently morphed into an above-average yielding dividend growth stock.

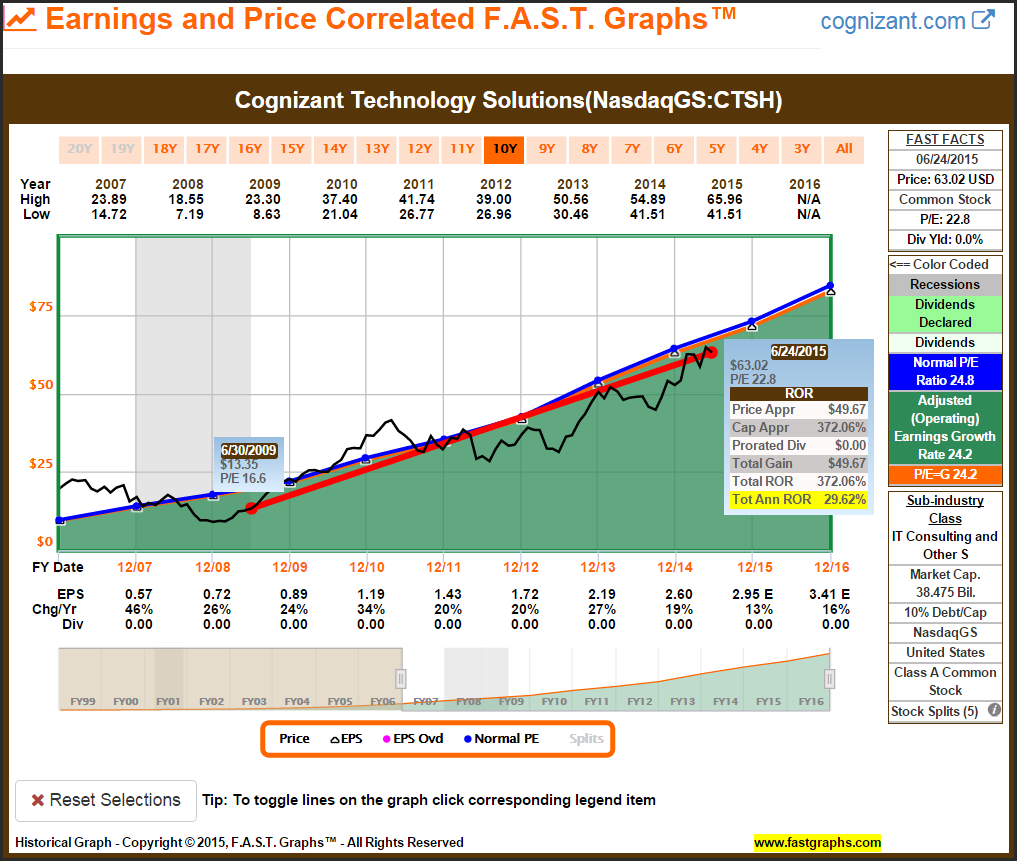

Cognizant article published on August 7, 2009

When I wrote about Cognizant (CTSH) on August 7, 2009, it was offered as a very attractive growth stock. This has been one of my best performers, but best of all, its performance was generated based on expected operating results.

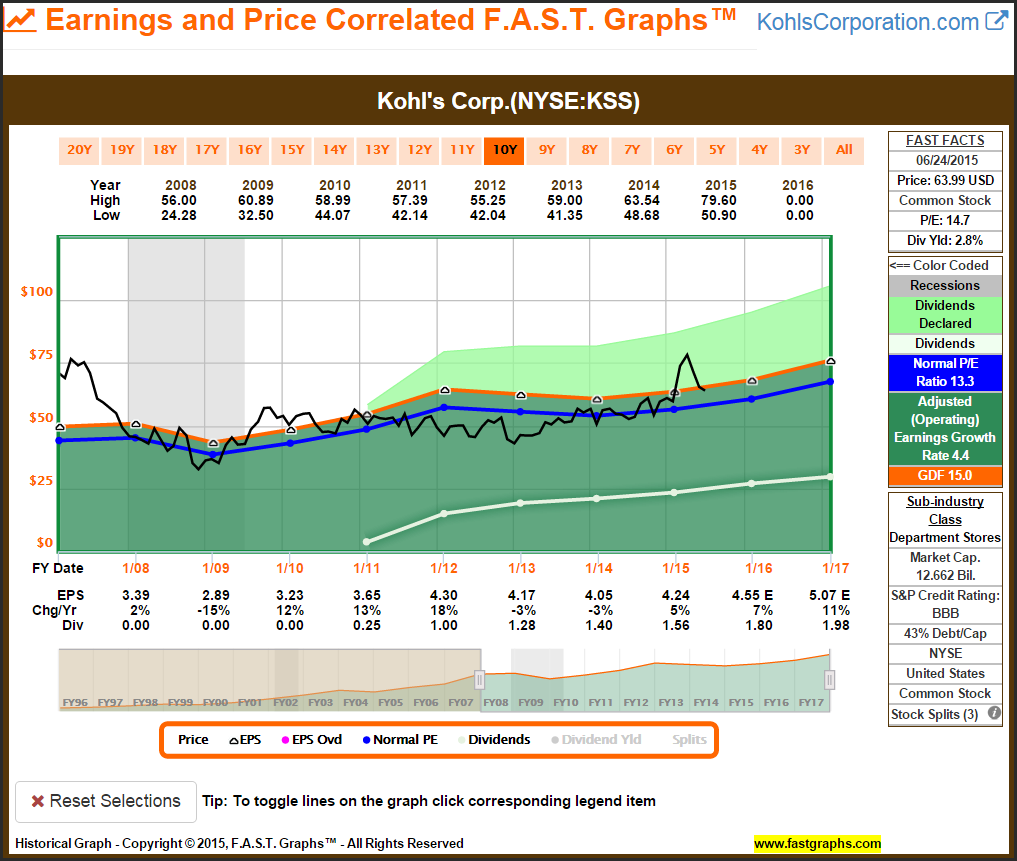

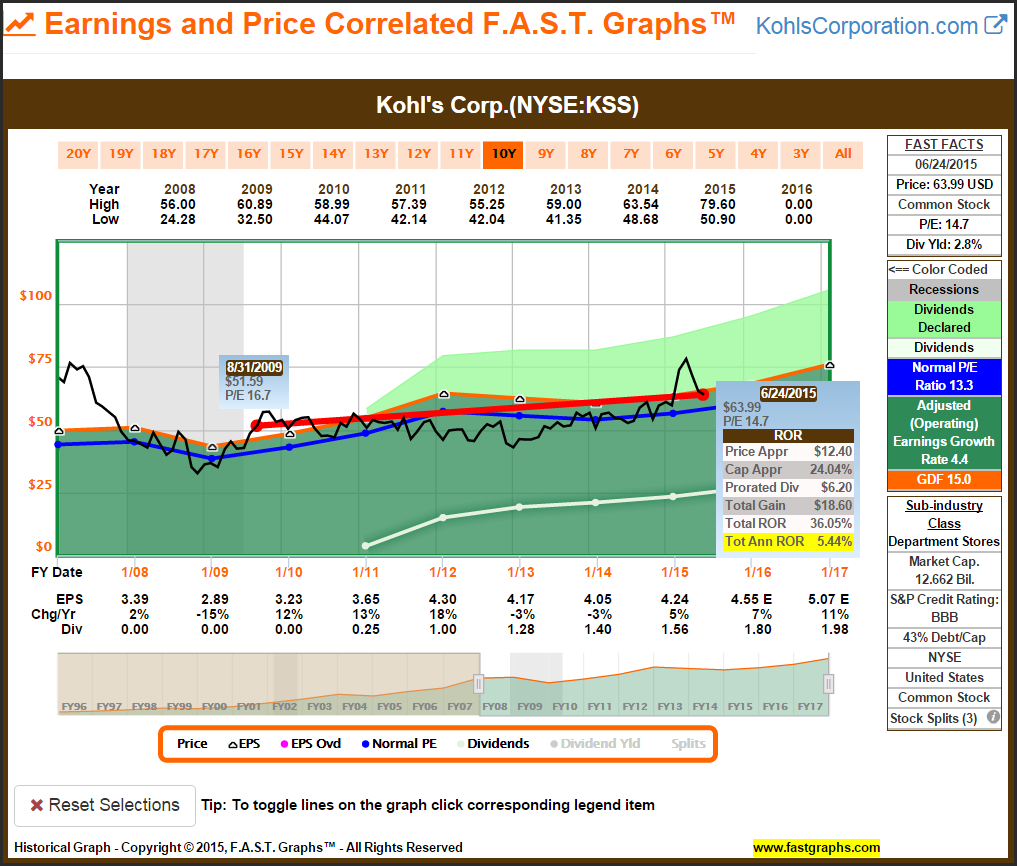

Kohl’s article published on August 14, 2009

As the title of the article written on August 14, 2009 on Kohl’s (KSS) indicates, it was offered as a moderately priced research candidate. Since that time the company has morphed into a dividend growth stock.

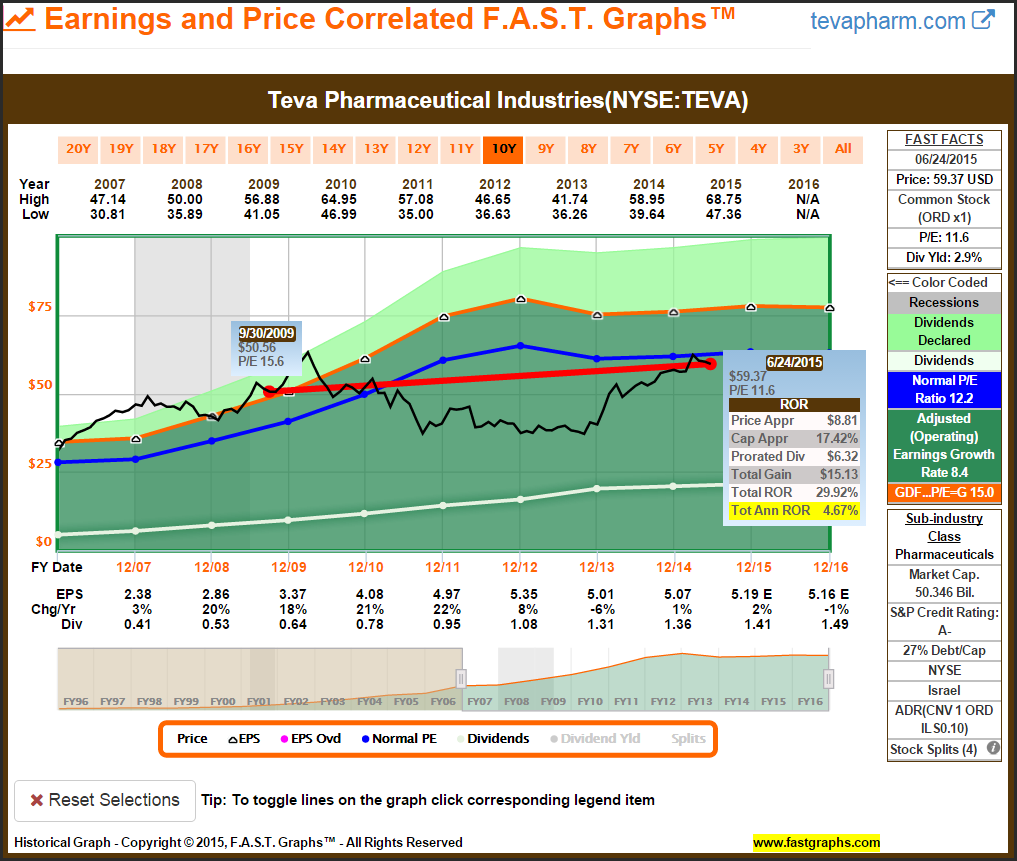

Teva Pharmaceutical article published on August 20, 2009

When I originally wrote about Teva (TEVA) on August 20, 2009, I was expecting strong earnings growth, which I got for the next two to three years. However, since 2012, earnings have been lackluster. However, the company did raise their payout ratio, which generated a decent level of income. Nevertheless, this has been one of my more disappointing offerings.

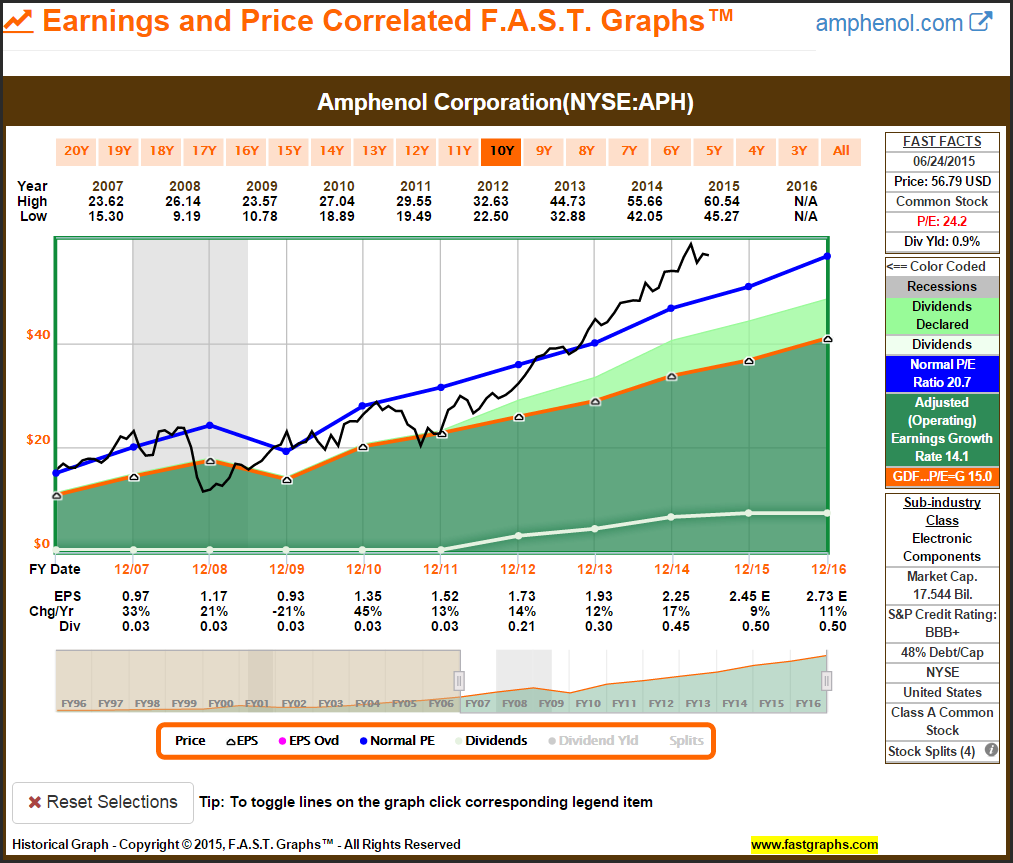

Amphenol Corporation article published on August 27, 2009

When I wrote about Amphenol (APH) on August 27, 2009, it was offered as an attractively-valued growth stock. Although this has been one of my better total return performers, I can’t take credit for the excessive valuation that the stock has been awarded by the market.

Charles Schwab article published on September 4, 2009

When I wrote about Charles Schwab (SCHW) on September 4, 2009, I expected better operating results going forward. Even though this recommendation has performed reasonably well, I consider it one of my mistakes.

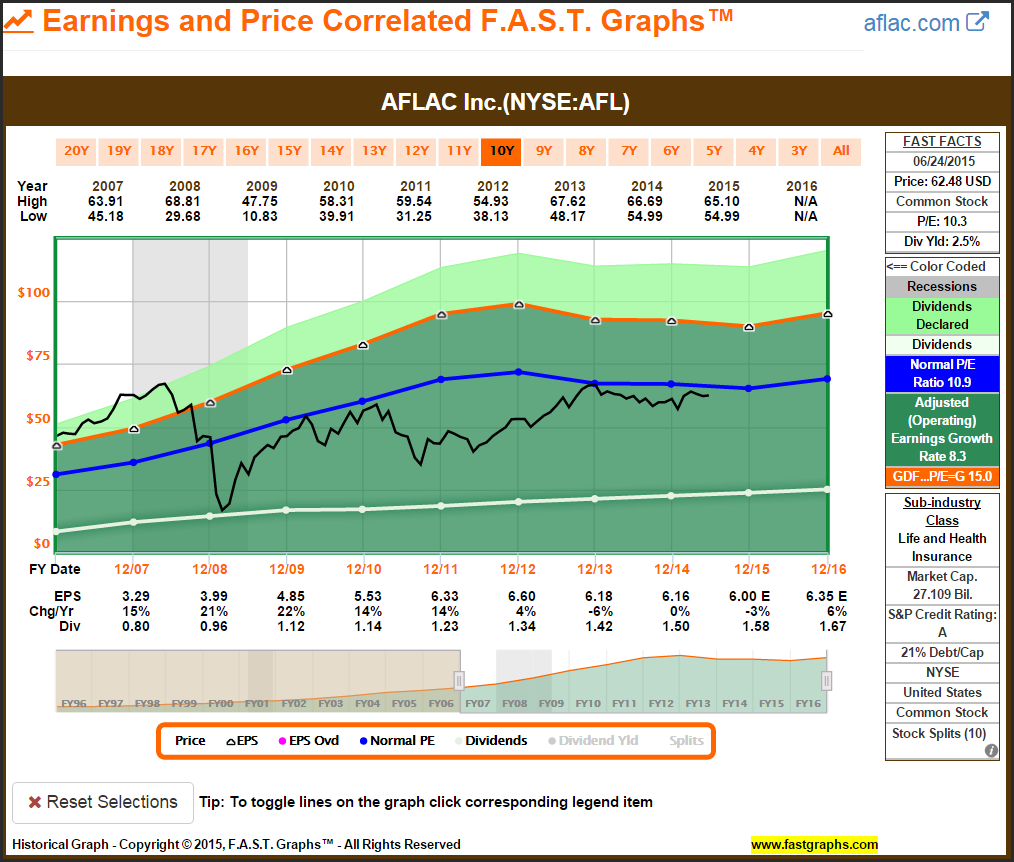

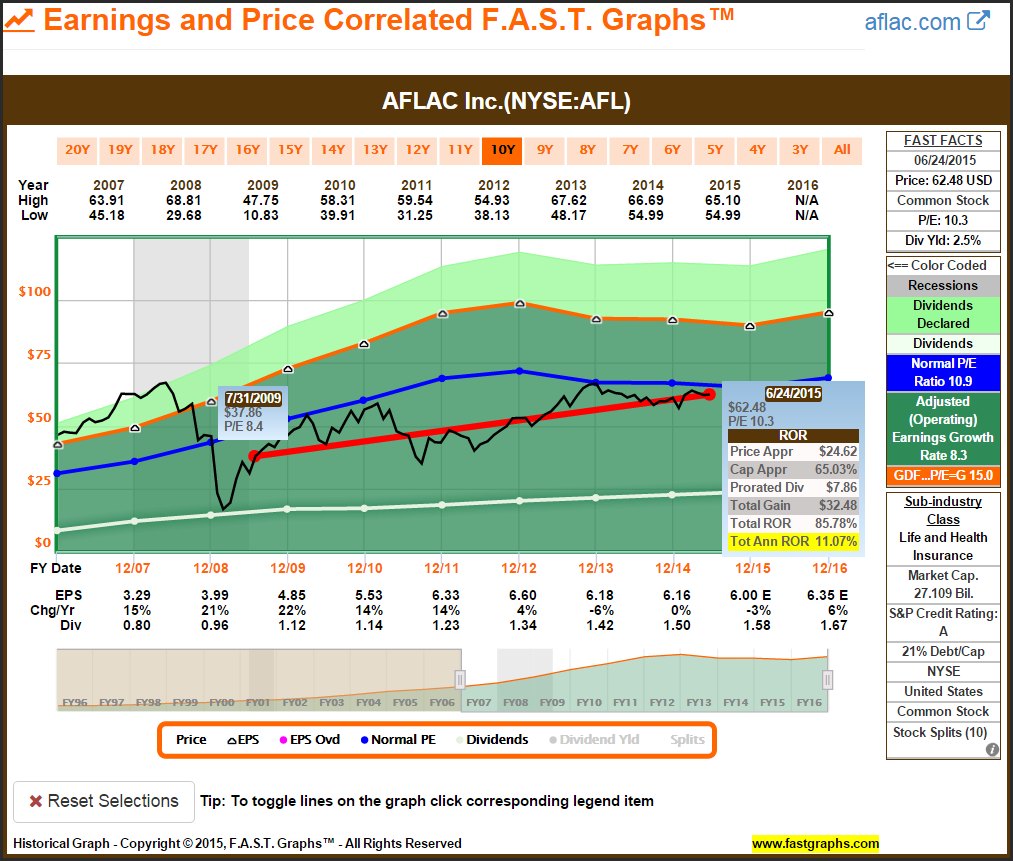

Aflac article published on September 11, 2009

When I wrote about Aflac (AFL) on September 11, 2009, it was offered as an extremely attractive blue-chip dividend growth stock. Even though the market continues to undervalue Aflac, thanks to the power of low valuation, long-term results have been acceptable. I am still waiting for the market to recognize the value in this one.

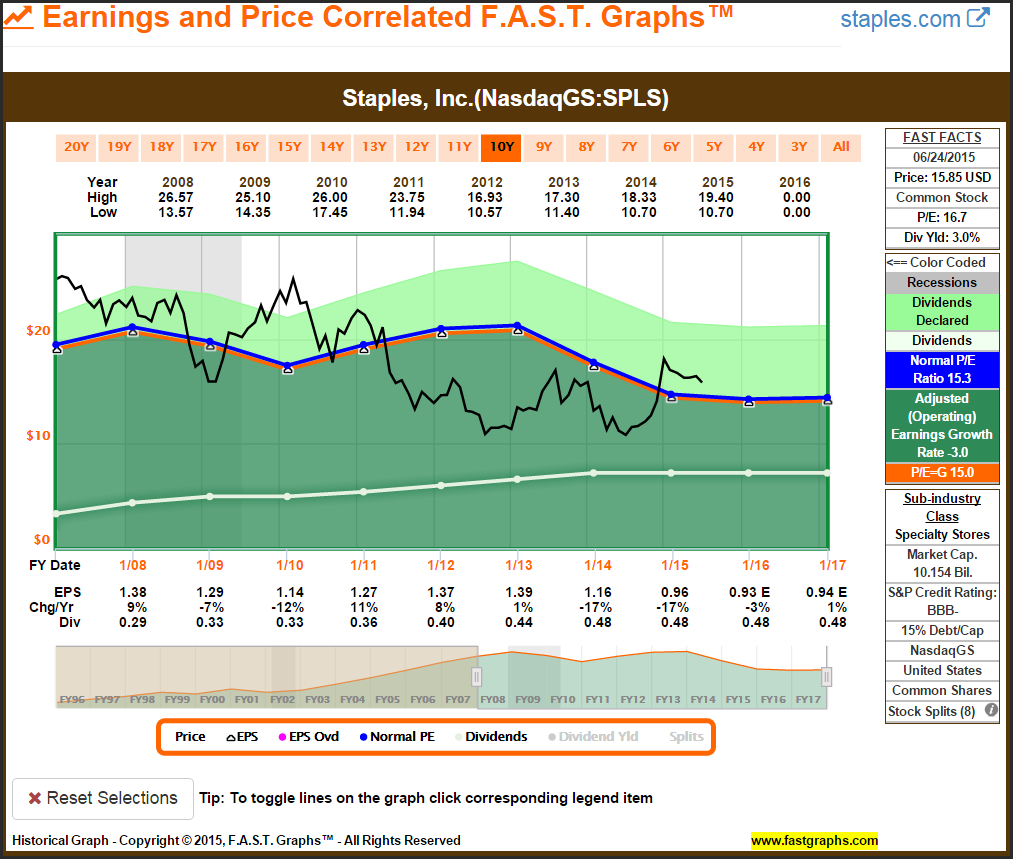

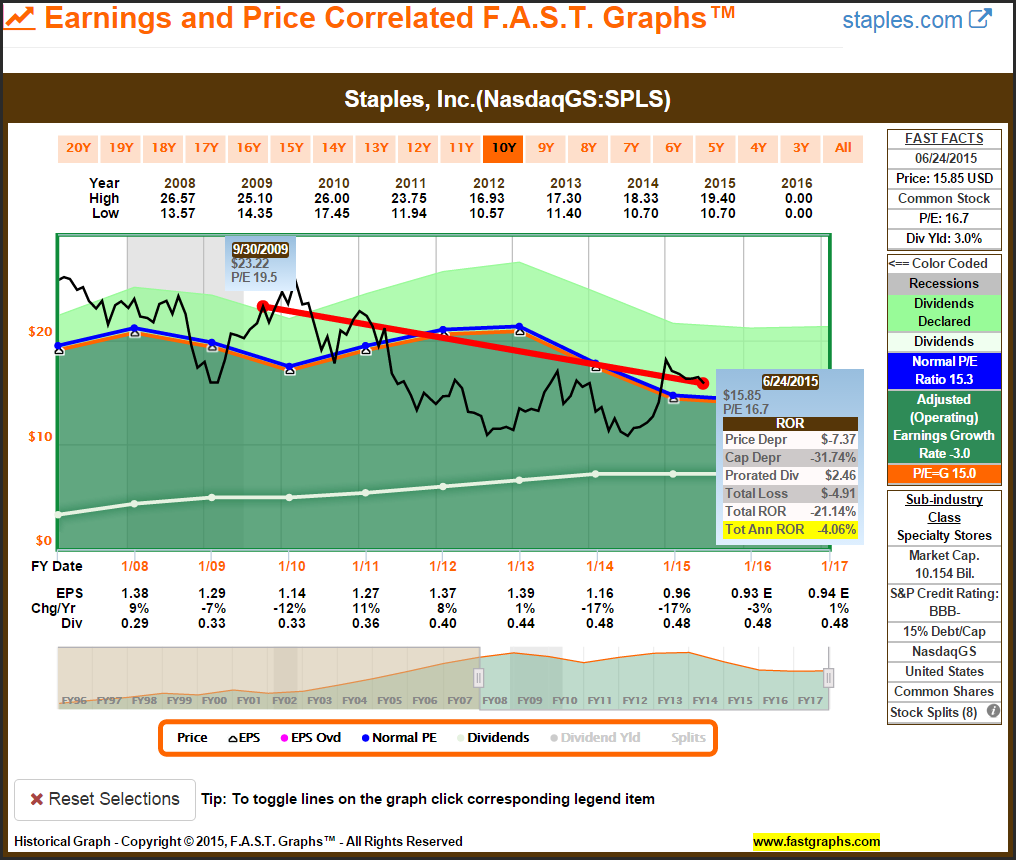

Staples article published on September 18, 2009

When I wrote about Staples (SPLS) on September 18, 2009, I expected better things from the company. This is one that I was long in, but my original optimism soon turned to realism and I accepted my losses and moved on.

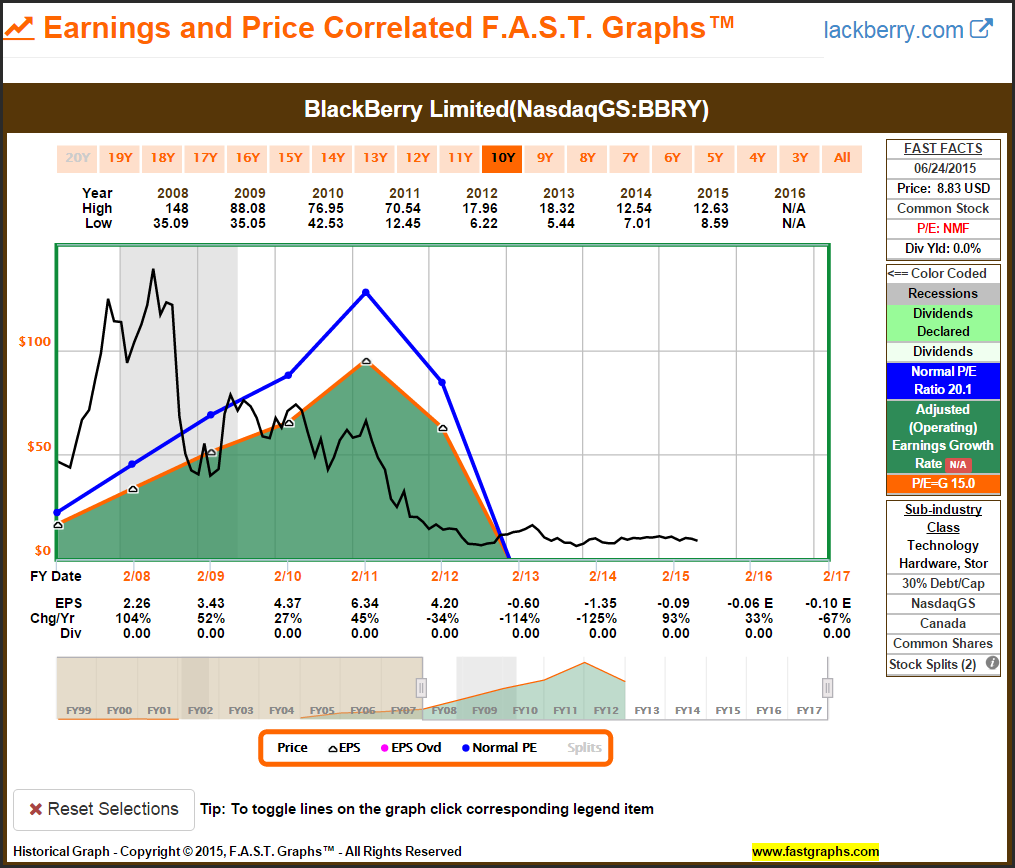

Research In Motion article published on September 27, 2009

When I wrote about Research in Motion, now known as BlackBerry (BBRY), on September 27, 2009, it was offered as a growth stock opportunity in the bourgeoning Smartphone market. Although this has clearly been a mistake, I continue to hold the stock. I will admit that this is a case where I let optimism become stubbornness. However, as you will see later, I also invested in Google for the same reasons. Not shown in this article is that I also hold a large position in Apple. Growth stock investing is riskier, and BlackBerry serves as a strong reminder to that reality.

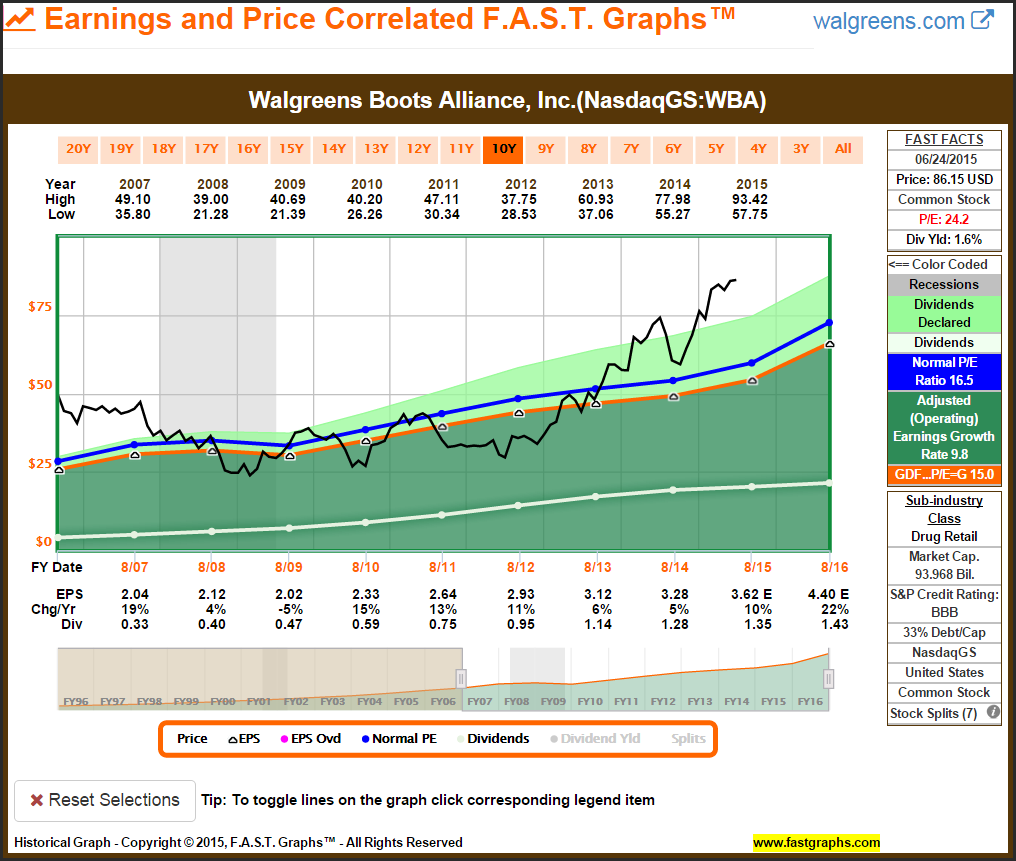

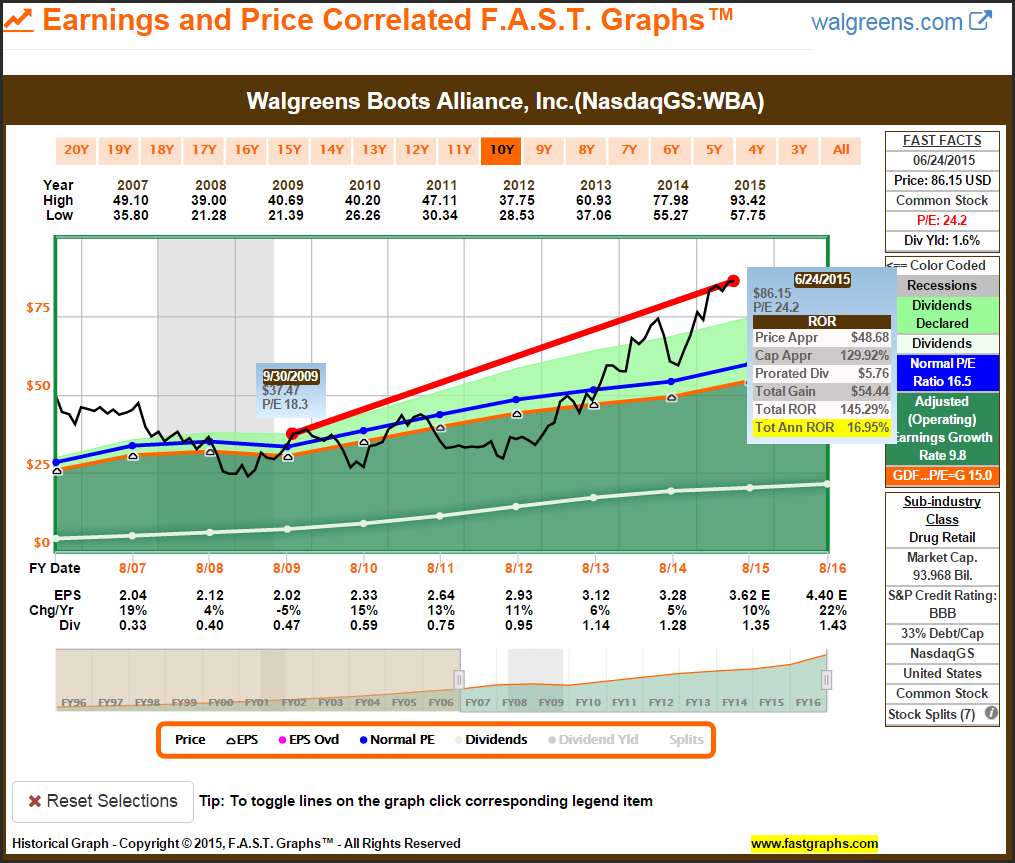

Walgreens article published on September 30, 2009

When I wrote about Walgreens (WBA) on September 30, 2009, I was concerned about moderate overvaluation, and I was right short term. However, long term this has proven to be an excellent performer, but I do consider it significantly overvalued.

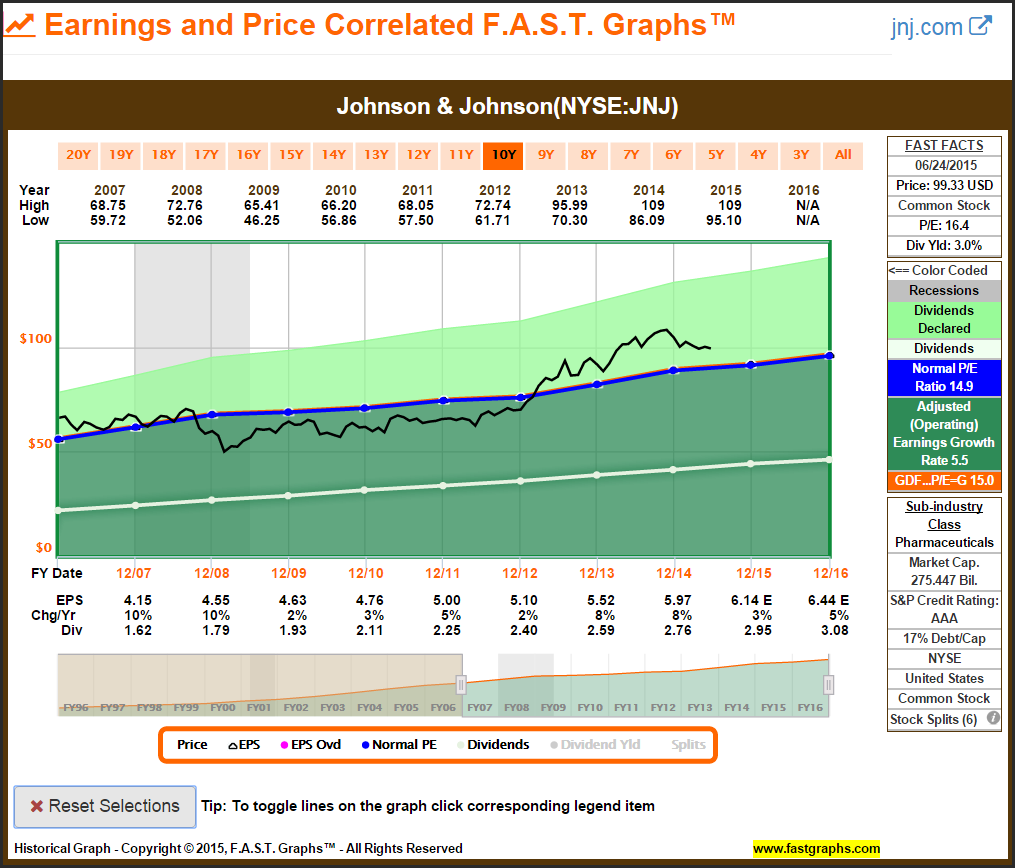

Johnson & Johnson article published on October 1, 2009

When I saw AAA rated Johnson & Johnson (JNJ) available at a P/E ratio below 15, I jumped at the opportunity. This is a classic example of how attractive valuation can provide a strong total return, even with a low growth dividend paying stalwart.

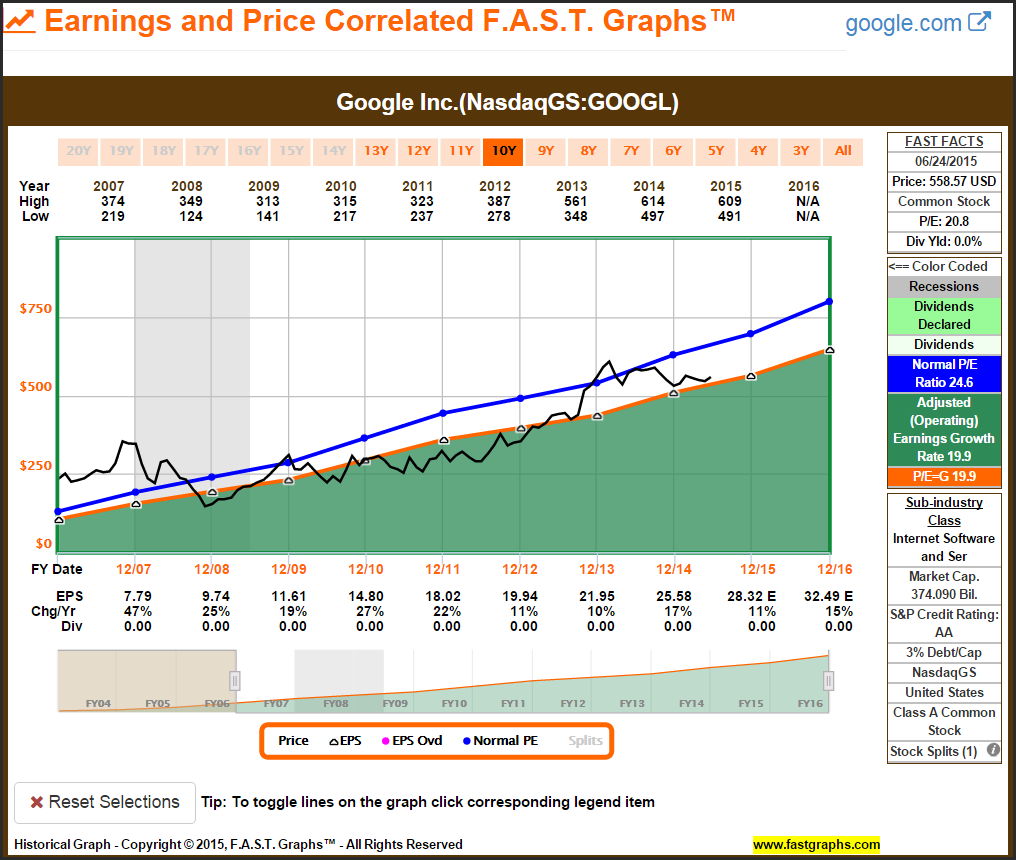

Google article published on October 8, 2009

On October 8, 2009, I presented Google (GOOGL) as an attractively valued growth stock with a bright future. This example has worked out as planned and took some of the sting out of the BlackBerry mistake.

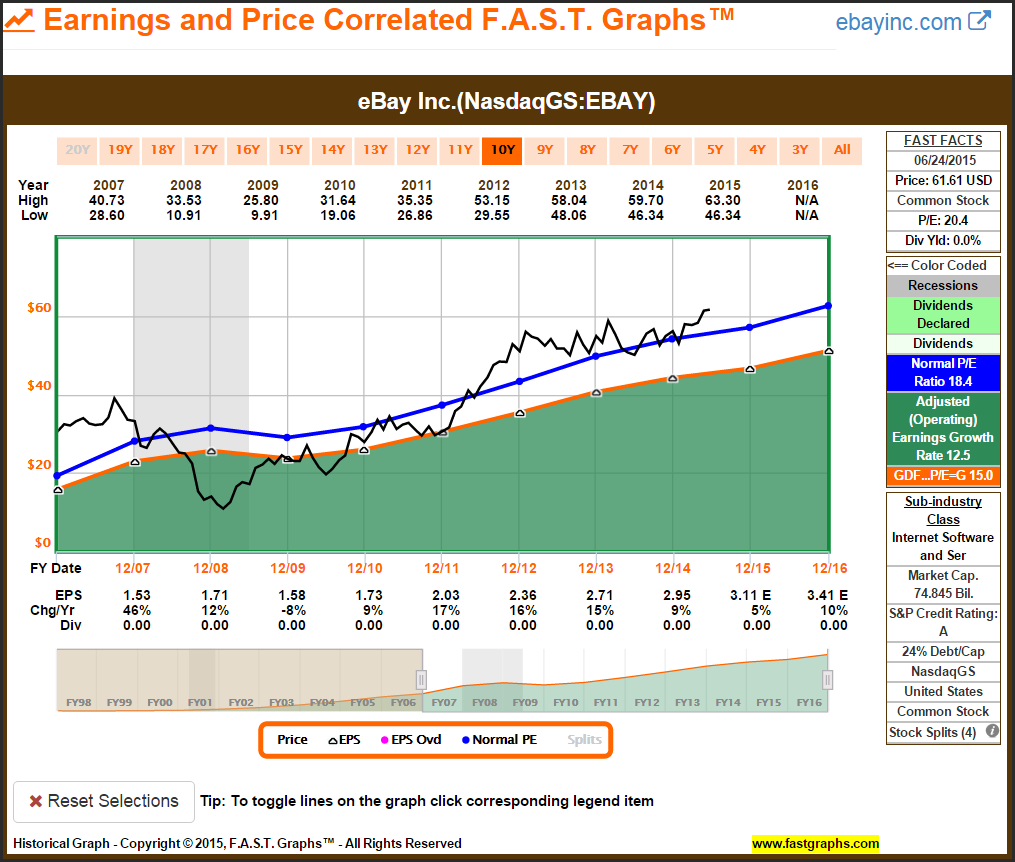

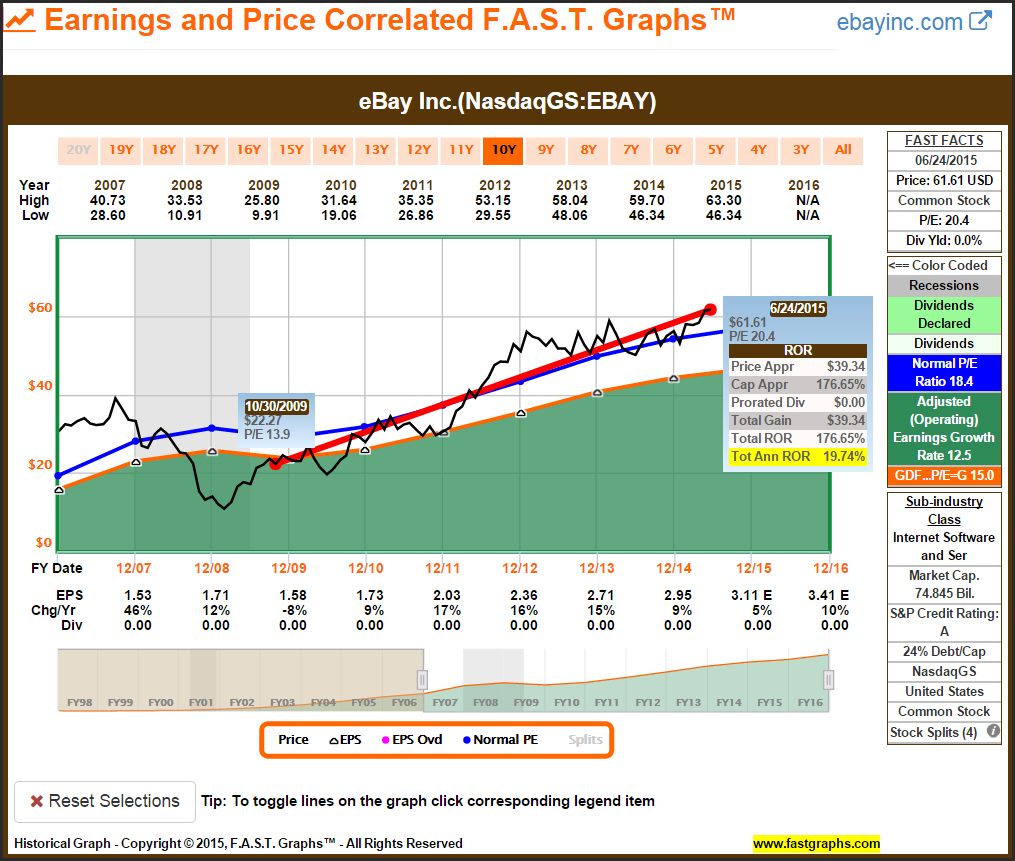

eBay article published on October 15, 2009

On October 15, 2009, I presented eBay (EBAY) as an attractively-valued growth stock. Although this research candidate has performed extremely well, I am not pleased with its current high valuation.

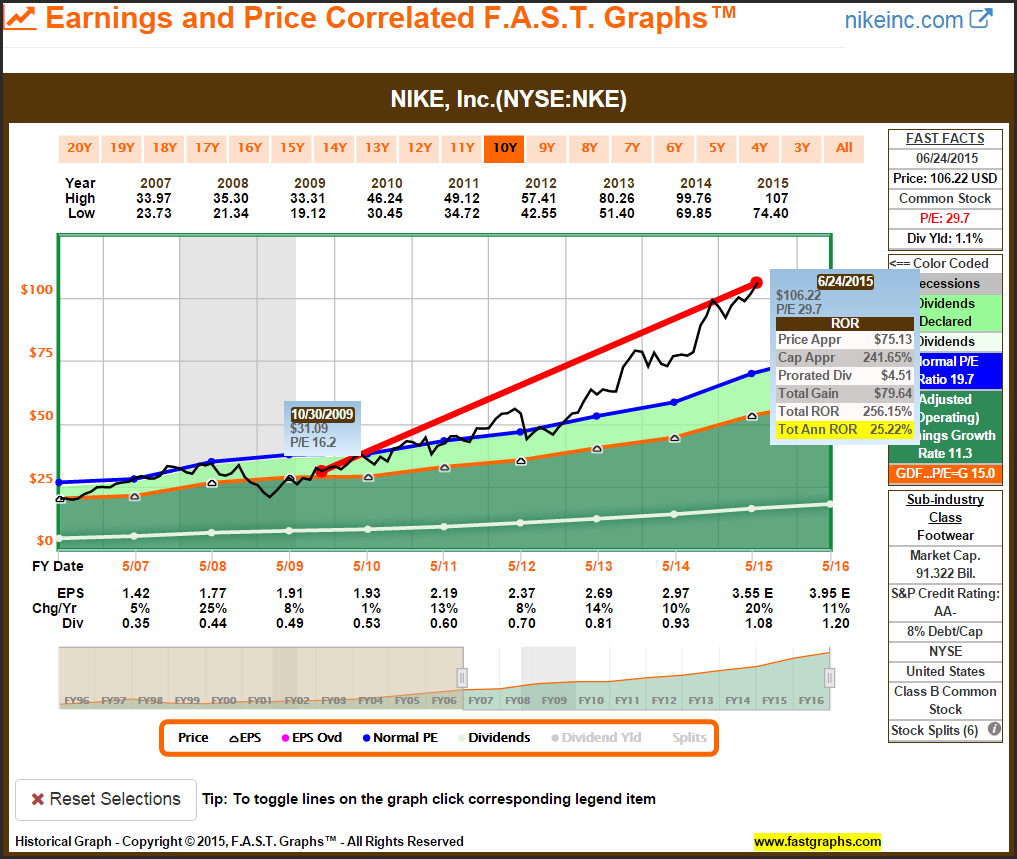

Nike article published on October 20, 2009

On October 20, 2009, Nike (NKE) was presented as an attractively-valued blue-chip dividend growth stock. Although performance has been exceptional, I remain concerned with its current high valuation, which I wrote about in a recent article.

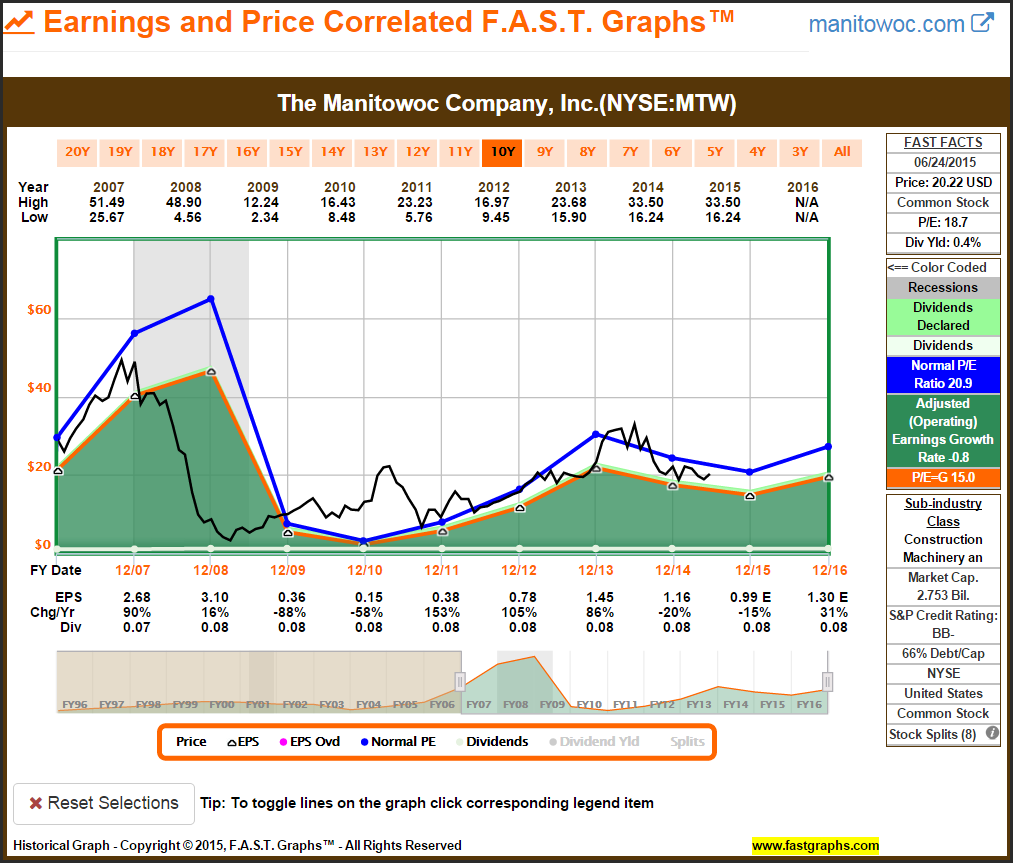

Manitowoc article published on October 29, 2009

On October 29, 2009, I presented The Manitowoc Company (MTW) as an opportunity to invest in a cyclical with recovery potential. Long-term this research candidate has done well. However, it does not possess the consistent characteristics that I typically look for.

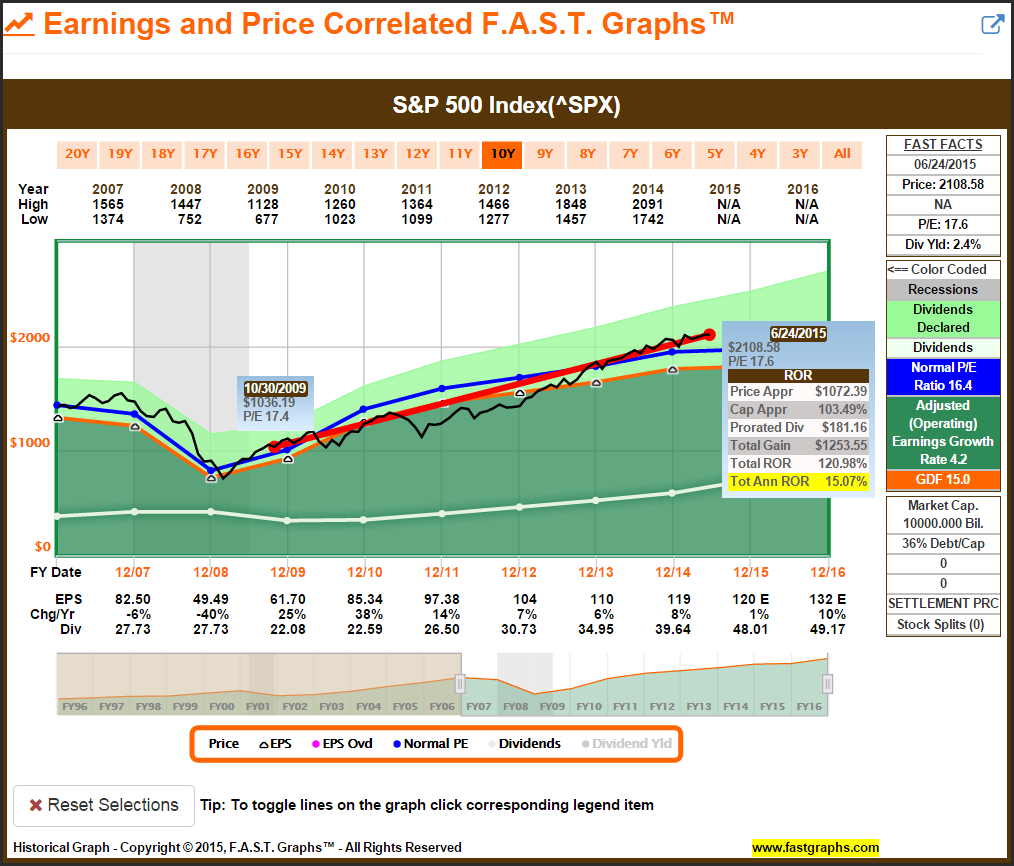

S&P 500 article published on October 29, 2009

On October 29, 2009, I revisited the S&P 500 suggesting that future returns could be extraordinary based on estimated earnings growth and attractive valuation. As the comments following the graphs illustrate, people do not like positive offerings. I believe this represents another example of what a pessimistic attitude can cost.

“If 6.5% over the next 2 years can be called Extraordinary - then yes. I won't even say what the return will be over the next 5 years - Let me just say that will be negative.”

“Extraordinary is a given. Just not Good.”

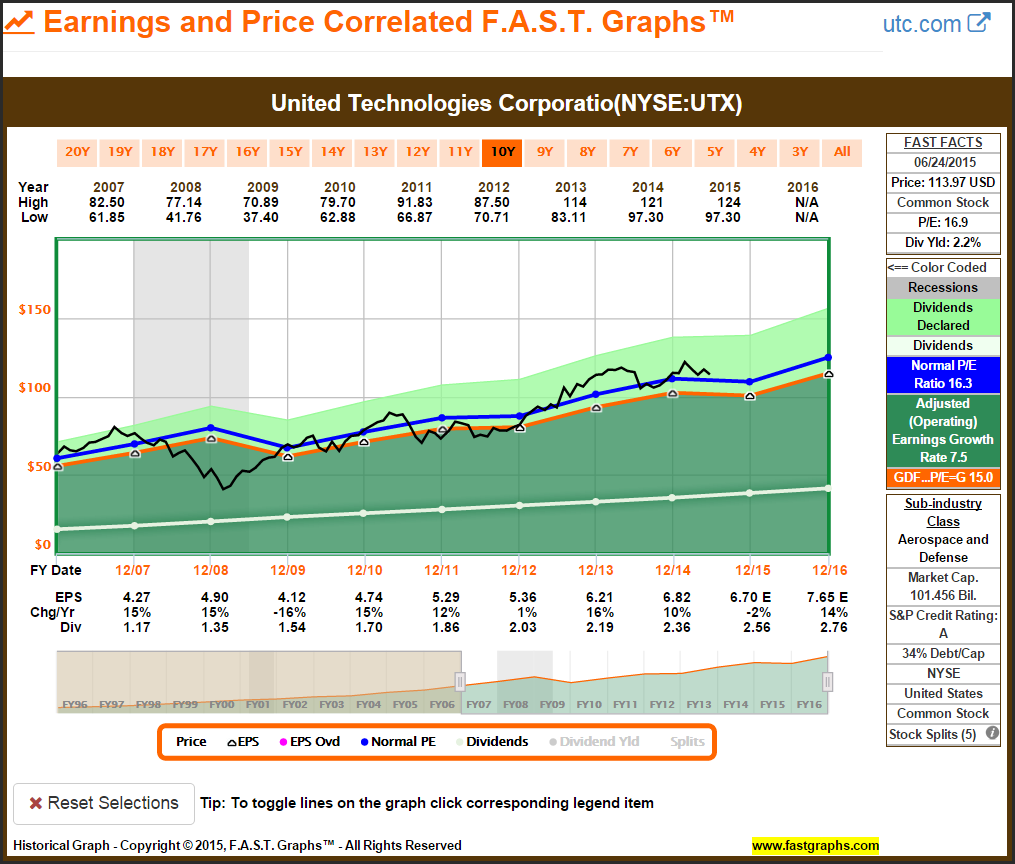

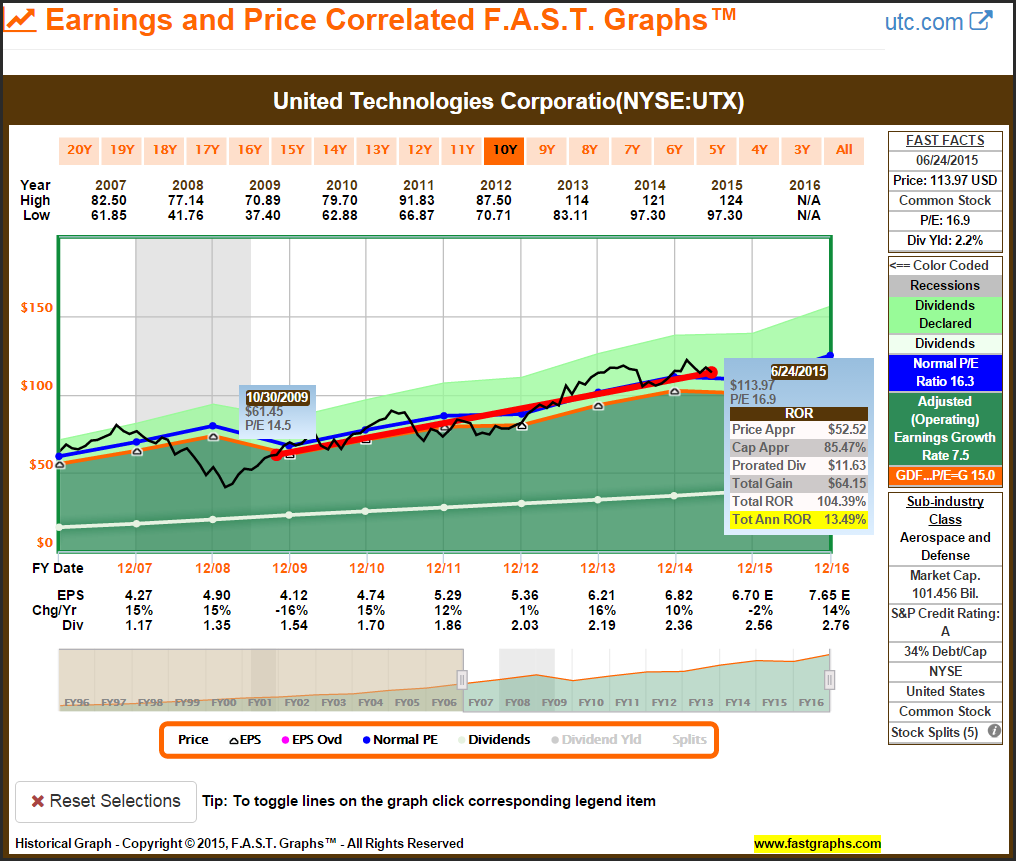

United Technologies article published on November 8, 2009

On November 8, 2009, I wrote about United Technologies (UTX) as an attractive dividend growth stock in the aerospace and defense sector. Long term it has performed well and I continue to hold this position.

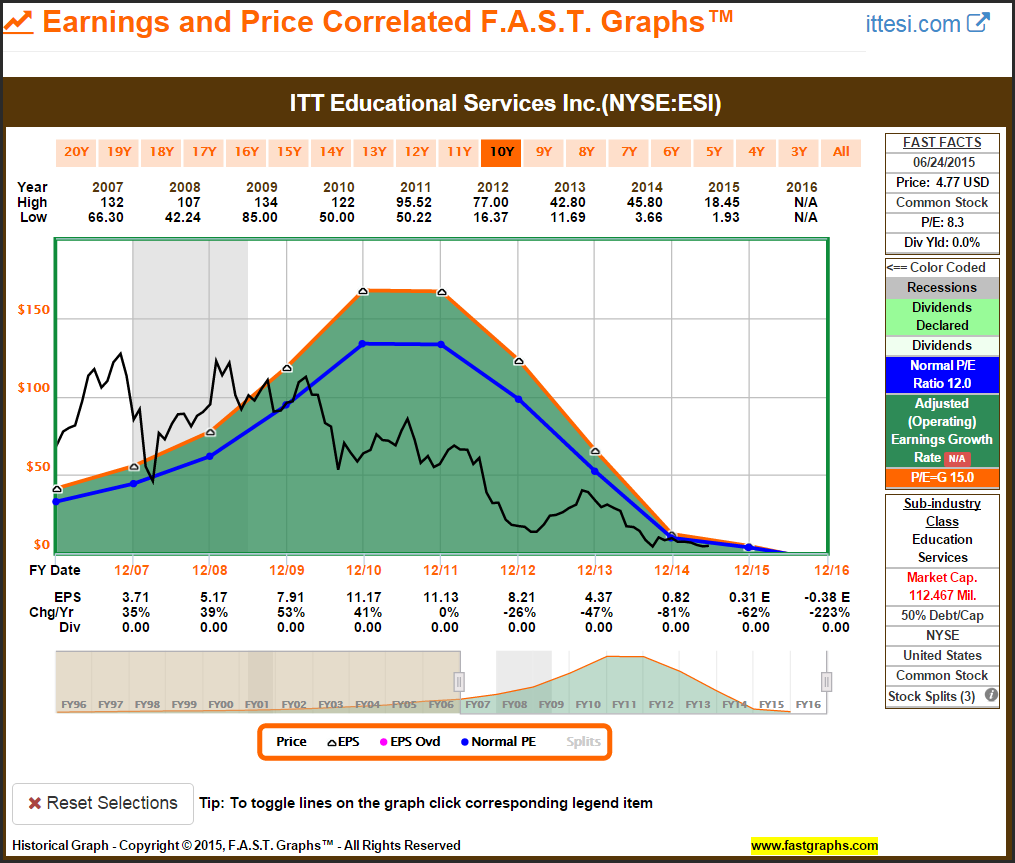

ITT Educational Services article published on November 12, 2009

On November 12, 2009, I wrote about ITT Educational Services (ESI) as an attractively-valued aggressive growth stock. Fortunately I cut my losses based on aggressive government intervention with this whole industry. Nevertheless, we see another classic example of the earnings and price relationship. In the long run, where earnings go, stock price is sure to follow.

Stryker Corporation article published on December 11, 2009

On December 11, 2009, I revisited Stryker Corporation (SYK). Consistent earnings and dividend growth provided attractive long-term returns; however, current valuation is high.

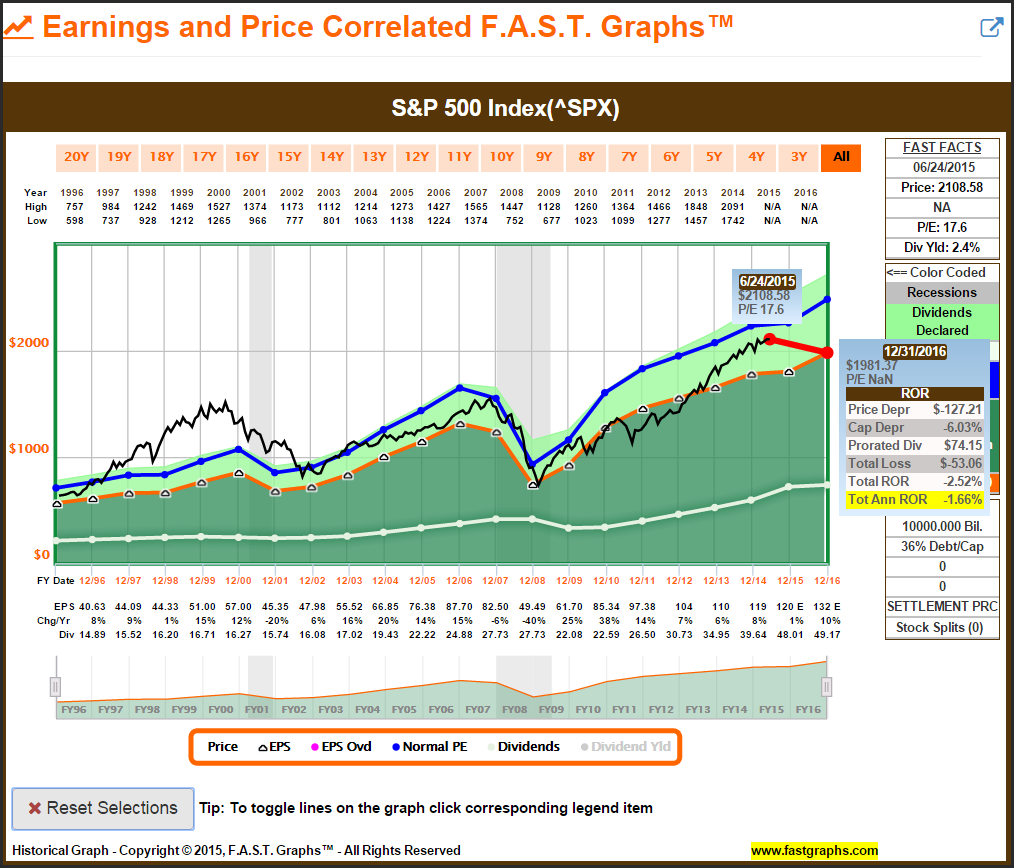

I Remain An Optimist- But I’m Also A Realist

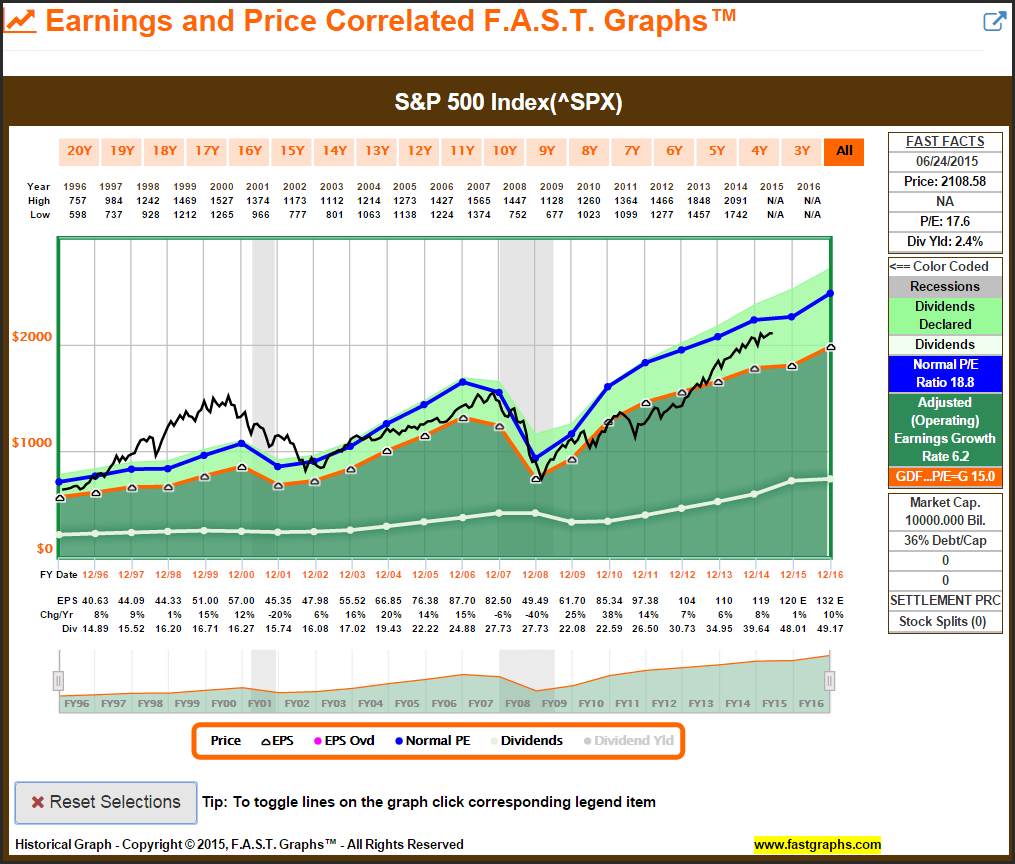

As a bonus addendum to this article I offer the following F.A.S.T. Graphs™ on the S&P 500. Although I remain optimistic about our country, our economy, and its continued long-term prosperity, I am also realistic about current valuations. I believe the following earnings and price correlated graph clearly illustrates that the valuation of the S&P 500 has become significantly higher than it was during the years immediately following the Great Recession. In other words, the opportunities I saw when I published the articles on the S&P 500 presented above, are not as attractive today as they were then.

Summary and Conclusions

Since most of my recent work has been oriented towards investors in retirement I would like to conclude Part 1 with some comments about optimism as a person gets older. Speaking from my own experience and perspective, maintaining an optimistic attitude about my portfolio, and life in general for that matter, is now more difficult than it was when I was younger. I do not believe that I am unique in that respect. However, I also believe that remaining optimistic is even more important for investors in or near retirement than it even is for younger investors.

With the above said, I offer the following caveats relating to the rather meager opportunities to find attractively-valued dividend growth stocks in today’s more fully valued market. It is an undeniable fact that most best-of-breed dividend paying stalwarts have become fully valued. Not all of them, but unfortunately many of them. Consequently, even though I support maintaining an optimistic posture, I also support applying common sense and being realistic. Being disciplined with valuation in the market environment we have today is more important than it has been in several years. Good value is there to be found, but at the same time, it’s now harder to find. Proceed courageously, but be prudent and cautious as you do.

In Part 2, I will continue with visiting the recommendations I offered in 2010 through June in order to cover my complete first year authoring articles.

Disclosure: Long SYK,LLL,PG,CTSH,KSS,AFL,JNJ,GOOGL,UTX at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.