International investing was easy for U.S.-based investors for many years because the U.S. dollar was either declining in value or was stable. U.S. dollar-based investors’ non-US equity and fixed-income returns were generally enhanced by the falling dollar so that U.S. investors actually tended to outperform the local currency benchmarks. Of course, investment managers took credit for the resulting “alpha” despite that out performance was more likely attributable to currency than to asset selection.

Global investing has been subtly changing since 2008, but investors still seem stuck in the old weak dollar paradigm. A secularly strengthening dollar, which we foresee, could significantly alter global investment strategies. International investing was relatively easy, but could now become more difficult.

U.S. dollar-based investors might increasingly need to hedge currency exposure to alleviate the performance drag that could result from a stronger dollar. Interestingly, although global fixed-income managers have often hedged currencies, global equity managers have preferred to ride the wave of a weaker dollar and now seem somewhat unprepared for the potentially changing environment.

Dollar Insights

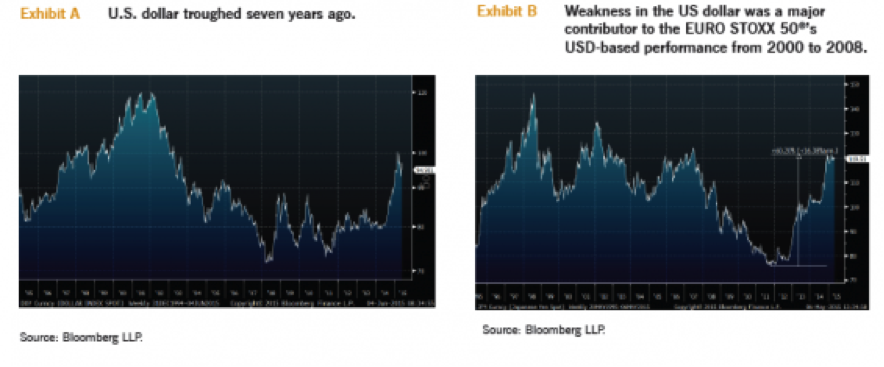

It is curious that investors seem generally unaware that the U.S. dollar’s value troughed … seven years ago! That’s right, seven years ago. Exhibit A shows the 20-year history of the DXY Index, which is a tradable index of six major currencies (euro 57%, Japanese yen 14%, British pound 12%, Canadian dollar 9%, Swedish krona 4% and Swiss franc 4%). We prefer this index to economic trade-based dollar indexes because this index is forward-looking and incorporates investors’ forecasts of the future.

Several Points

- The index’s low point was actually in the spring of 2008. Clearly the 2008-2011 period was extremely volatile, but the index’s low point was seven years ago (Exhibit A). The dollar appreciated substantially during the second half of the 1990s. However, non-U.S. investing was unpopular during that period because of the Asian and Russian crises and because the technology bubble made U.S. stocks extremely popular. Thus, the strong dollar didn’t necessarily have a meaningful impact on U.S. dollar-based investors’ returns because non-U.S. allocations were minimal.

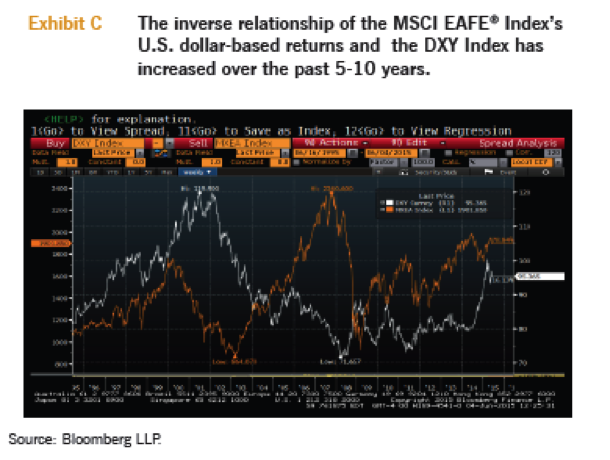

- The dollar depreciated substantially from 2002 to 2008 and moved sideways, with considerable volatility, from 2008-2011. The secular weakness in the dollar undoubtedly added to non-U.S. equity and fixed-income returns for an extended period of time. For example, Exhibit B shows the returns of the EURO STOXX 50® Index from 2000-2008. In U.S. dollar terms, the index’s total return was 65% over the period, but it was only 13% in Euro terms. The weakness in the U.S. dollar contributed 52 percentage points to the USD-based return, i.e., the vast majority of the overall return was simply attributable to currency.

- As we wrote last month in “Time to look at South Korea,” the dollar’s recent strength could be the beginning of a secular period of dollar appreciation. However, unlike the late-1990s period, investors have now fully embraced global investing. For example, the American Association of Individual Investors’ (AAII) “suggested allocation” for a “moderate” investor currently advocates a 20% exposure to non-U.S. stocks. Because of the acceptance of non-U.S. investing, a secular period of U.S. dollar appreciation today might substantially hinder overall portfolio returns more than in the past. Exhibit C shows the relationship through time of the MSCI EAFE® Index’s U.S. dollar-based returns and the DXY Index. The correlation over the 20-year period is -51%, but the correlation increases to -71% based on the last 10 years and it is nearly -80% over the last five years.

The world changes; your portfolio should, too.

Investors, equity investors in particular, need to be increasingly aware of the currency exposures within their portfolios. As mentioned, most equity managers tend to ignore currency because there has been no need to hedge for many years. Quite to the contrary, currency was a hidden source of alpha for which equity managers sometimes took credit.

However, the world may be changing, and if we are correct regarding our thesis that global overcapacity will cause a worldwide fight for market share, then extrapolation of past global equity strategies might be a considerable detriment to overall portfolio performance.

We feel our portfolios are uniquely structured to account for this changing world.

Index Definitions

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indexes. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indexes are not actively managed and investors cannot invest directly in the indices.

U.S. Dollar: InterContinental Exchange (ICE) U.S. Dollar Index (DXY).The ICE U.S. Dollar Index, indicating the general international value of the USD, averages the exchange rates between the USD and six major world currencies, using rates supplied by some 500 banks.

EAFE®:MSCI Europe, Australasia, Far East (EAFE®) The MSCI EAFE® Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity market performance of developed markets excluding the US and Canada.

EURO STOXX 50®:The EURO STOXX 50® Index, provides a blue chip representation of supersector leaders in the eurozone. The index covers 50 stocks from 12 eurozone countries.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any fund.

This information was prepared by and has been reprinted with the permission of Richard Bernstein Advisors LLC. The views expressed herein are those of Richard Bernstein Advisors LLC. Information provided and views expressed are current only through the month stated on top of each page. The opinions herein are not necessarily those of the Eaton Vance organization and may change at any time without notice. The information contained herein has been provided for informational and illustrative purposes only and is not intended to be, nor should it be considered, investment advice or a recommendation to buy or sell any particular security. Investors should consult an investment professional prior to making any investment decision. While information is believed to be reliable, no assurance is being provided as to its accuracy or completeness.

The information in this material may not be relied upon as an indication of trading intent on behalf of any Eaton Vance Fund. It is not to be construed as representative of any Fund’s underlying allocation. This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial advisor and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk and ability to withstand a potential loss of some or all of an investment’s value.

About Risk

Equity investing is subject to stock market volatility. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, established companies. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging or frontier countries, these risks may be more significant. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, established companies. Investing involves risks including possible loss of principal.

Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment’s value. Past performance is, of course, no guarantee of future results.

Richard Bernstein Advisors LLC serves as subadvisor to three Eaton Vance mutual funds.

Richard Bernstein is chief executive officer of Richard Bernstein Advisors LLC, a registered investment advisor.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com