“The probability of loss is no more measurable than the probability of rain. It can be modeled, and it can be estimated (and by experts pretty well), but it cannot be known.” – Howard Marks, Chairman, Oaktree Capital

I enjoyed that quote as well as the piece Marks wrote titled, Risk Revisited Again. The reality is that because our investment time horizons are finite, we run the risk of running out of time. We just might not make back what we lose in a major market downturn. Some form of risk management is prudent, if not mandatory.

Within the math is the painful fact that gains and losses are not symmetric. Unfortunately, it takes a 100 percent gain to recover from a 50 percent loss. Thirty years have taught me that many, if not most, individual investors lack this basic but important understanding.

My mother hoped I’d be a doctor, accountant or lawyer. Not in the cards for me. As I listened recently to my electrician explain something I really didn’t care to understand, my eyes glazed over with polite disinterest. I imagine many people feel the same way about investing.

Understanding the power of compounding interest is perhaps the most important learning on the path to investment success. It involves minimizing loss and, fortunately, there are processes that are simple that can help us do just that.

So with an eye on compound interest and investment process, let’s forget about overvaluations, excessive debt, underfunded pensions and all things Greece for today and take a look at a few simple trend following strategies that have worked well over time. Downside portfolio risk can be managed.

Included in this week’s On My Radar:

- Understanding Price Momentum – A Simple Moving Average Risk Management Process

- Three-Way Asset Strategy (Stocks, Bonds and Gold)

- Watching Out For Number Two – Don’t Fight The Tape Or The Fed Update

- Trade Signals – Daily Trading Sentiment Reaches Extreme Pessimism – Signaling Buy – 06-18-2015

Understanding Price Momentum – A Simple Moving Average Risk Management Process

Price behavior alone can tell us a lot about supply and demand. When there are more buyers than sellers, prices move higher. When selling overpowers buying demand, the price declines.

Imbalances build up – when confidence in the market is gained, investors tend to allocate greater percentages of their investable net worth to stocks. Further, margin is used that allows the more aggressive investor to buy even more stock. When the trend changes, margin calls can kick in which result in forced selling and more margin calls. A spiral of selling can occur – such as what happened in the 2000 tech bubble collapse and the 2007 great financial crisis.

We can think it won’t happen again, but it will. While can measure the degree of risk, the timing is nearly impossible to predict.

So let’s take a look at several simple ideas that can help you stay in sync with the primary trend. I do believe you can let the cyclical trend, as they say, “be your friend.”

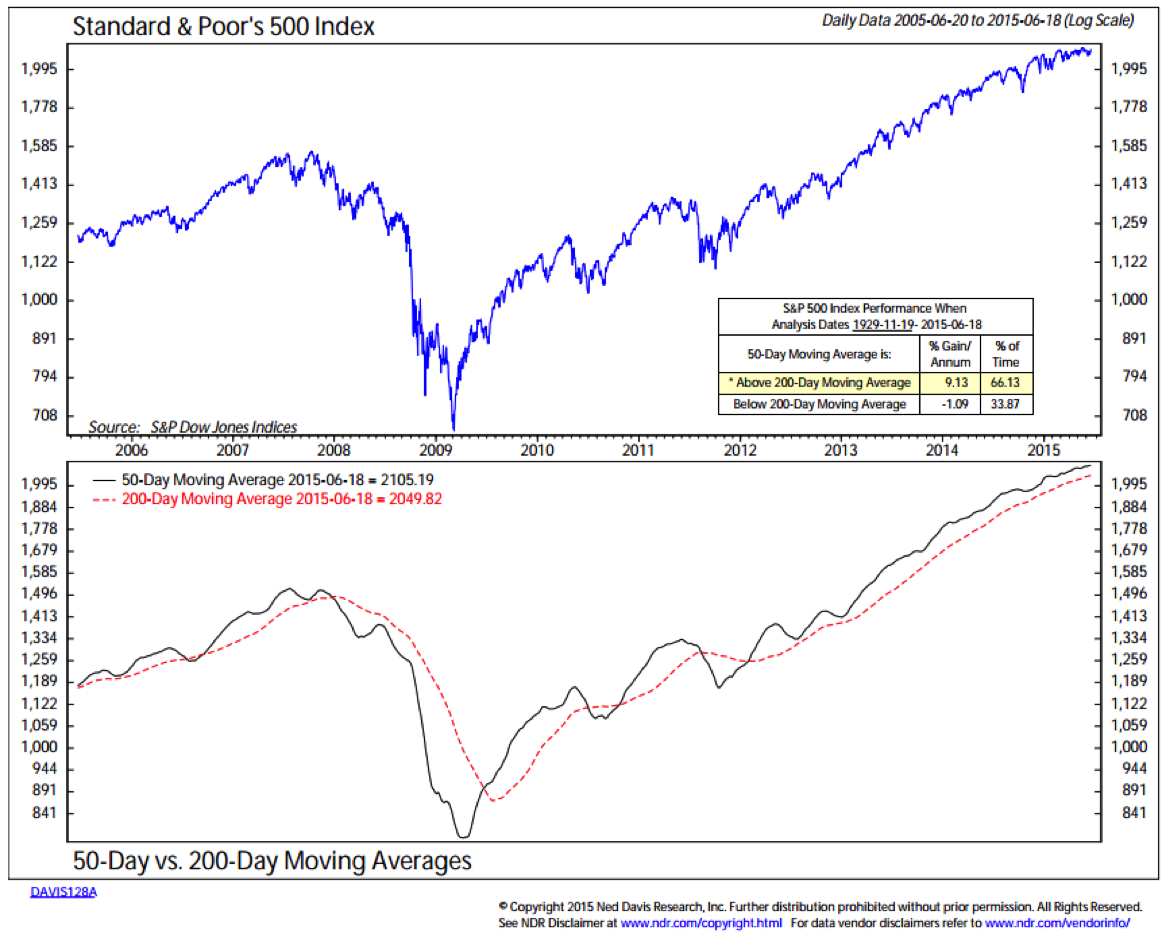

The first chart that follows looks at the S&P 500 index 50-day moving average price line and compares it to its longer 200-day moving average price line. Here the trend is identified to be higher when the shorter-term moving average price trend (black line) is higher than the longer-term 200 day moving average price trend (dotted red line). The concept is simple and you can see the performance results highlighted in yellow.

As noted, overcoming a 50% decline requires a 100% subsequent return. It also takes years to recover from such losses. Long-term thinking can be emotionally impossible if such decline happens near retirement. Logic and discipline tossed aside. It may be equally emotional for the younger investor as well.

Take a look at the chart again. Note how the 50-day over 200-day moving average cross helped one avoid the 2008 market meltdown and also allowed participation in the recovery. That is the general idea with risk management. There are hundreds of academic studies on price momentum. Tested many ways and in multiple markets over hundreds of years. It is essentially simple and it works but here is the hard part.

Imagine all the great news that was in the press when that 50-day crossed lower in late 2007. Then it was the Goldilocks economy and Greenspan’s “there is no bubble in the housing market”, etc. And what about the buy signal in mid-2009. Then we were all faced with the near collapse of the entire financial system. Price was telling us something important at both points in time. The hard part is finding a process you can follow and sticking to it. There are other approaches and the one that personally suites me best is NDR’s Big Mo. You can find it each week on our website here or below in the Trade Signals section. We’ve don’t a great deal of work to create a daily version of the model and I’ll be sharing that with you soon.

Like most portfolios, I imagine that your portfolio owns a number of diverse investments. Exposure to large cap stocks might be just one of the risk exposures you own. Of course, how you size the risks you take is also important. Understanding how different risks correlate with each other is an important step in building your total portfolio. I believe something really good happens when you combine non-correlating risk together. Send me a note if you’d like a free copy of my white paper titled, Understanding Correlation and Diversification.

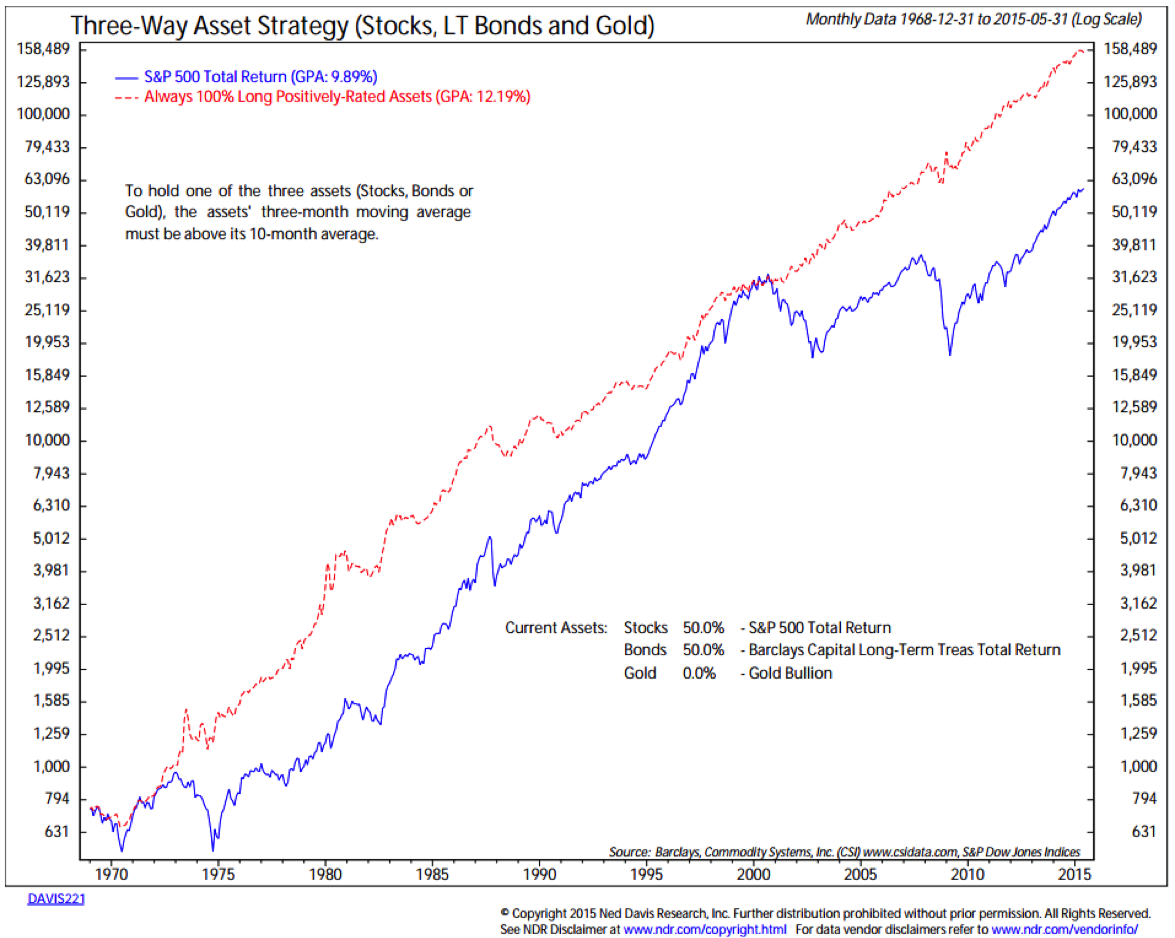

Stepping towards that direction, let’s next take a look at a broader risk that might fit into a portfolio. It is an asset strategy (The Three-Way Asset Strategy) that combines the S&P 500 Index, Long-Term Government Bonds and Gold and utilizes a moving average crossover to determine what is owned and when.

Three-Way Asset Strategy (Stocks, Bonds and Gold)

The concept here is simple and often simple is best. The red line shows the performance from 1968 to present when holding the asset classes (S&P 500, long-term bonds and gold) when the 3-month moving average is above its 10-month moving average. It shows how a simple three-way model can do well against the stock market as represented by the Standard and Poor’s 500 Total Return Index.

Here is how it works:

- The concept is to stay fully invested in any of the three assets provided each asset’s 3-month MA is above its 10-month MA.

- If, for example, gold is the only asset with its 3-month above its 10-month, then the model will be 100% long gold. If stocks and bonds, than 50% is positioned in each. If all three are in a positive up trend, than 1/3rdis allocated to each.

- It’s that simple. The model’s returns are better and much less volatile than the S&P itself.

The assets used in the Three-Way Asset Strategy are the S&P 500 Total Return Index for stocks, Barclays Capital Long-Term Treasury Total Return Index for bonds, and Gold Spot for gold.

Source: NDR – thank you for doing great work. Also, a special thank you to Meb Faber for sending me the NDR chart.

Some advisors might consider a strategy such as this as a core holding within a portfolio. My intent today is to show how consistently price momentum can be used to help mitigate loss and when combined together with other types of strategies, may further enhance return and reduce risk. It’s about risk mitigation in a way that allows the power of compound interest to work its magic over time.

Now, if you are more of a speculator and less of an investor, forget what I’m saying and find yourself highly concentrated bets. My two cents on speculative bets: short yen – long dollar (for now), Japanese stocks (currency hedged), short European Banks (a coming sovereign debt crisis), short high yield bonds (soon –default crisis). But venture forward at great risk. While I have conviction, some or all of these bets could be wrong or at least look wrong for a long time before they might prove correct. How long was the short sub-prime bet wrong before it turned right?

There is investing and there is betting. Investing is about combining a number of probable investment processes and diverse risks, speculating is going after the big bets. It’s one path or the other. Personally, I favor investing and the power of compound interest over time.

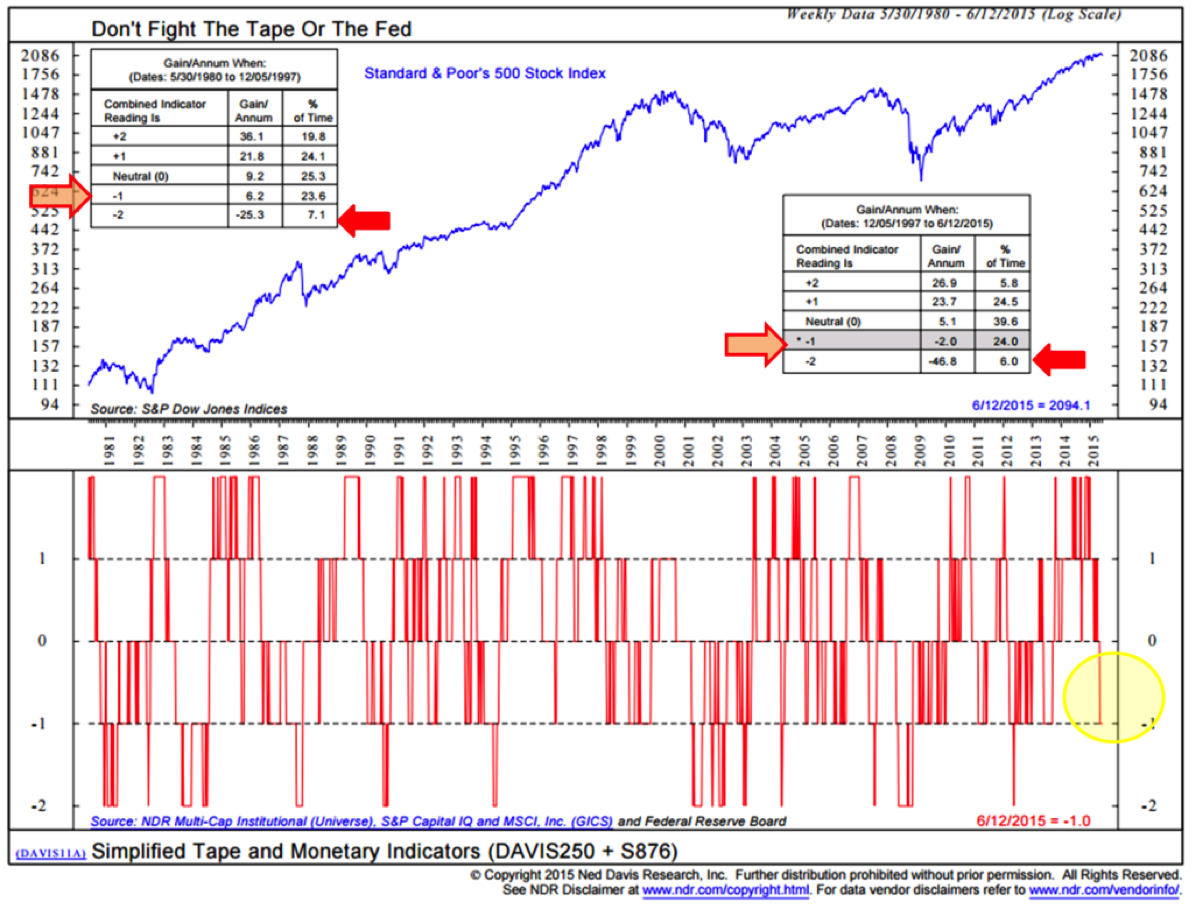

Watching Out For Number Two – Don’t Fight The Tape Or The Fed Update

I posted this chart last week. Given that it’s very close to a number two signal, I will continue to post each week. There is no change. I’m still watching out for a -2 (orange arrow). I believe it is something important we should keep our eye on. Click here for more.

Trade Signals – Daily Trading Sentiment Reaches Extreme Pessimism – Signaling Buy – 06-18-2015

Short-term Investment Sentiment has reached Extreme Pessimism – suggesting a bullish equity investment posture. Interestingly, investor sentiment, as measured by NDR’s Daily Trading Sentiment Composite, has been in the extreme pessimism zone about 26% of the time. During which the S&P 500 Index has gained 33% per annum (12-30-1994 to present. Note data in the chart below). During periods of extreme optimism (about 28% of the time) the S&P 500 Index declined nearly 11% per annum. Data shows the crowd is usually wrong at sentiment extremes. I like combining investor sentiment with trend evidence. My favorite measure Big Mo, while weakening, remains in a buy signal. Also, the 13/34-Week EMA remains bullish as you’ll see in the following charts. Further, volume demand continues to be stronger than supply. This too supports a bullish view.

Yet, overall, risk remains high. Though short-term bullish, it is important to keep in mind that the cyclical bull is aged, overvalued and we are near a change in Fed policy. Hedge your equity exposure and look to trend evidence to help you mitigate downside loss.

As for bonds, it has been a wild few months. The Zweig Bond Model (a trend based process) remains in a “SELL” – continuing to suggest that short-term bond maturities are favored over long-term maturities.

Click here to view all of the most recent Trade Signals.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities. Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures StrategyFundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Captial Management Group

© CMG Capital Management Group