There was nothing unexpected in the Fed’s monetary policy statement or in the revised economic projections of senior officials. Chair Yellen covered no new ground in her press conference. However, many investors appear to be unsure of the monetary policy outlook and the implications for the financial markets. So, to clear things up...

The Fed’s decision to begin raising short-term interest rates and the pace of tightening beyond that first move will be data-dependent. The focus is on the job market and the inflation outlook. Job market conditions have improved significantly. Monthly growth in nonfarm payrolls has slowed somewhat (a 210,000 average over the last three months, vs. 280,000 in the second half of last year), but is still well above the pace consistent with trend labor force growth. Over the long term, this pace of job growth is unsustainable (as we’d eventually run out of people), but it is clearly welcome over the intermediate period, as excess slack generated from the recession is taken up.

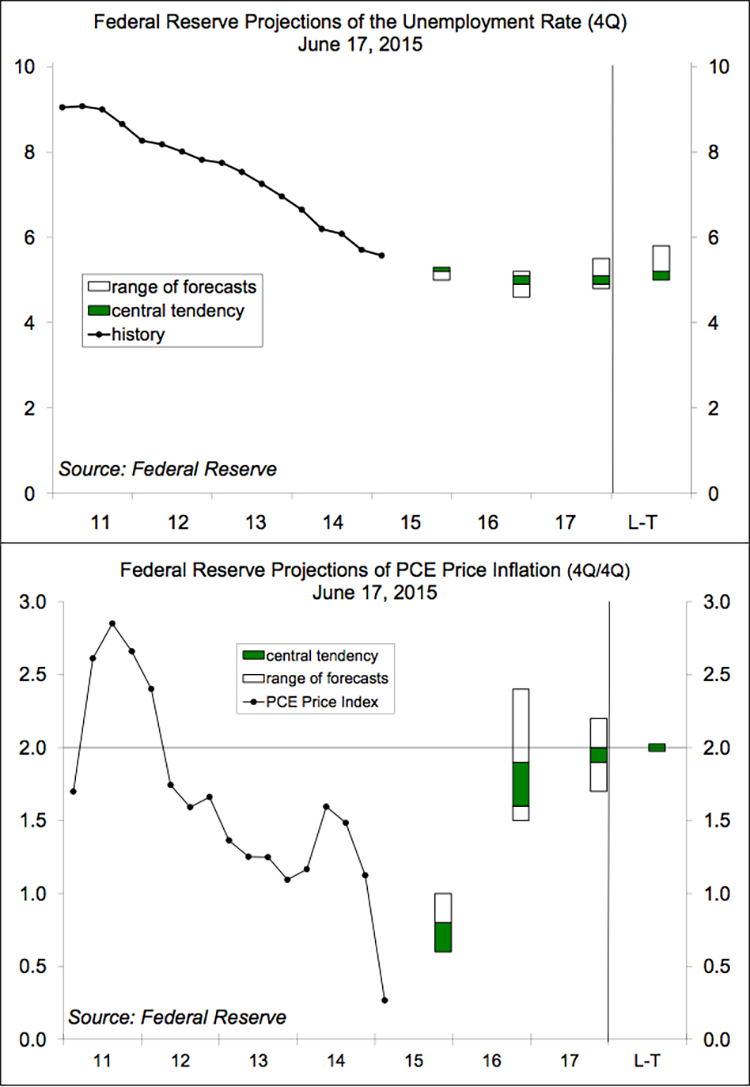

The Fed expects the unemployment rate to edge lower and then stabilize at around 5% over the next two years. Implicit in this forecast is an expectation of a long-awaited rebound in labor force participation. To gauge the amount of slack in the job market, the Fed will continue to examine a wide range of labor market indicators, including participation rates, part-timers wanting full-time employment, quit rates, and wages.

The Fed sees the recent modest trend in inflation as reflecting the transitory impact of low energy prices and a strong dollar. According to Yellen, “inflation is likely to run at a low level for a substantial period of time.” However, oil prices and the dollar have stabilized in the last few months. As transitory impacts fade, inflation should move up. Continued economic growth should eventually put some upward pressure on inflation. Year-over-year growth in wages has ticked higher recently, but as Yellen noted, these signs are “tentative” and “not yet definitive.”

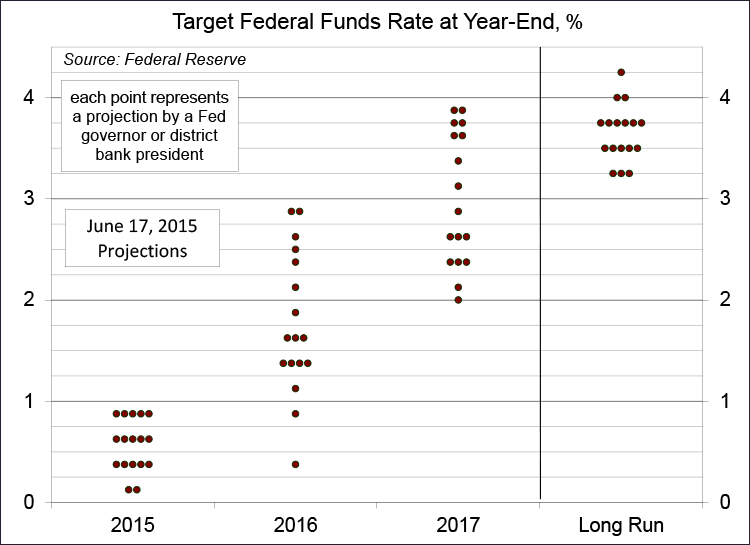

As expected, the dots in the dot plot generally moved lower (relative to the mid-March projections). All but two of the 17 senior Fed officials expect an initial rate hike this year. The difference in the dots largely reflects the difference in economic expectations among the various Fed officials. Some are more optimistic than others. However, there is a lot of uncertainty around each dot and the policy views of each Fed official will evolve according to the incoming economic data.

In her press conference, Yellen emphasized that, for the financial markets, the timing of the initial Fed hike should be less important than the pace of tightening beyond that first move. That trajectory is expected to be very gradual, but it could move higher, if economic growth is stronger and inflation moves higher than expected, or lower and less steep, if conditions were to prove weaker. The Fed will not commit to a mechanical rule on the pace of tightening. However, Fed projections are consistent with about 25 basis points per quarter.