The author Charles Seife referred to zero as “A Dangerous Concept.” It troubled early Christians because it represented a void; if used as a divisor, it became the gateway to the infinite.

Central banks around the world have held interest rates at or near zero for quite a while. This action was justified in the wake of the financial crisis. But there are those who think that zero, in this setting, has become a dangerous concept.

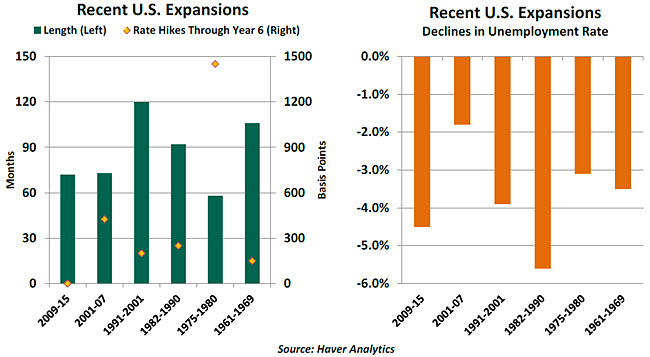

In the United States, the Federal Reserve’s benchmark interest rates reached the zero lower bound at the end of 2008, and they have remained there ever since. The expansion that began shortly thereafter has now lasted six years, one of the longest in the last half-century. It is the first expansion of this length to proceed without even a single firming of monetary policy.

American unemployment has declined from a peak of 10% to the current reading of 5.5%, a very significant improvement. The Fed’s economic projections, updated this week, suggest that a range of 5.0% to 5.2% is consistent with full employment. The jobless rate has a number of limitations, but other indicators confirm that the labor market is performing well. Wage gains are improving, “discouraged” workers are re-entering the labor force, and more people are quitting jobs to accept better ones.

Despite all this progress, there is concern in some corners that the expansion remains somewhat fragile. Economic growth since 2009 has been unsteady, with bursts of energy punctuated by intervals of retreat. And progress has been uneven, with some households and industries advancing more firmly than others.

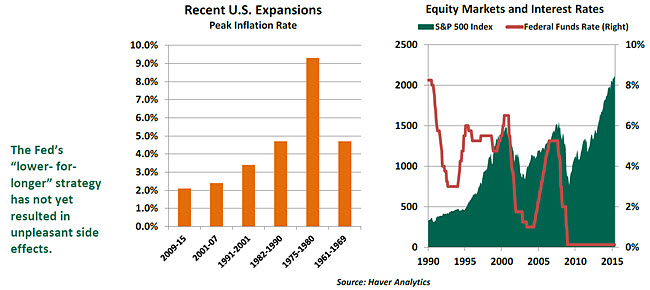

To its proponents, the “lower-for-longer” interest rate strategy will make retreat less likely. Letting the labor market run hot might boost wages, and thereby spread economic bounty more widely. The risk of doing so seems modest; inflation (using the Fed’s favored measure) has fallen short of its target for 39 consecutive months and currently stands at just 1.2%.

To this point, flooding the financial system with reserves has not placed undue pressure on the price level, partly because a good portion of those reserves remain unlent. And there is ample global capacity in markets for labor and raw materials, so inflation is unlikely to become entirely unmoored.

The Federal Reserve did not attempt to conceal its hope that very low interest rates would have a favorable impact on equity markets. Encouraging investors to re-risk their portfolios can abet economic growth, and strong markets can create wealth effects. Eventually, it was hoped, profits would improve and share prices could be justified more on fundamentals than easy monetary policy.

That seems to be the case today in the United States; our investment strategists are not uncomfortable about current equity market levels. Past cycles demonstrate that markets can progress even when central bank rates are rising.

But just because we have not yet seen excesses of inflation or asset prices does not mean that they won’t eventually develop. The Fed has expressed confidence in its ability to move proactively on these fronts if needed. Diagnosing these dangers is difficult, however, and some of the macroprudential means of regaining control are untested.

Low interest rates have harmed savers. Not everyone has extensive equity holdings, and those living on fixed incomes have seen their earnings diminish. The good news is that low interest rates have kept public borrowing costs in check, even as indebtedness has exploded. The bad news is that a certain level of fiscal complacency may be settling in, an orientation that could become very expensive when interest rates eventually return to normal.

Some have contended that the Fed is damaging psychology by keeping interest rates so low. This could be seen as conceding that the economy still needs significant help. An increase would therefore be a vote of confidence that would actually have a positive influence on spending and investment. Psychology can be a powerful factor in decision-making, but the notion that higher interest rates would be better for growth strains the sensibilities of the classically trained.  The psychology may actually work in the opposite direction. A small increase in short-term interest rates should not mean the difference between solvency and insolvency for large numbers of borrowers. And 25 basis points should not shift perceptions of equity markets from fairly valued to overvalued. Yet there is a palpable anxiety that moving away from zero might be destabilizing, which has been reflected in elevated levels of market volatility any time the Fed has hinted that change is in the offing.

The psychology may actually work in the opposite direction. A small increase in short-term interest rates should not mean the difference between solvency and insolvency for large numbers of borrowers. And 25 basis points should not shift perceptions of equity markets from fairly valued to overvalued. Yet there is a palpable anxiety that moving away from zero might be destabilizing, which has been reflected in elevated levels of market volatility any time the Fed has hinted that change is in the offing.

Policymakers can never be certain about reactions to policy changes, but it may be time to see if conditions can progress without the same level of monetary assistance. A small change would still leave interest rates at extraordinarily low levels, and the Fed’s balance sheet is likely to remain large for a long time. We’d all like to see if the economy and the financial markets can demonstrate that they are not addicted to nearly free credit.

Mathematically, straying from a position close to zero represents a significant change in percentage terms. But in the present economic context, the danger of moving away from zero seems modest, and the danger of staying there will inevitably rise. When it comes to interest rates, something is better than nothing.

Japan: Glimmers of Hope

Is it possible Abenomics is actually working? Data out of Japan certainly seem to suggest that it is. Gross domestic product (GDP) growth is promising, private investment is rising, and wages are finally showing substantive gains. A tour of Japan’s recent progress reveals undeniable progress but also real challenges.

First-quarter GDP surprised to the upside, as the economy recorded a 1% quarterly expansion. However, as is usually the case, the devil is in the details. Instead of showing that domestic demand had finally emerged from the doldrums it retreated to after last year’s tax increase, the strong GDP reading was largely a result of inventory gains.

Second-quarter GDP will not be able to rely on inventory accumulation, but promising (although still-tepid) consumption and capital expenditure expansion should be helpful. Export growth has been positive, but the slowdown in Chinese demand that has hampered the rest of the region could be heading toward Japan.

The Bank of Japan (BOJ) has finally admitted that the country will not achieve 2% inflation within the timeframe of “about two years” set in April 2013. The new timetable gives the BOJ until the end of 2016. Inflation readings will remain anemic for the rest of the year, but a dip into negative territory is unlikely unless oil price gains are reversed. The bank’s view that trend inflation is improving was borne out by the April core consumer price index (CPI), which registered a 0.3% increase.

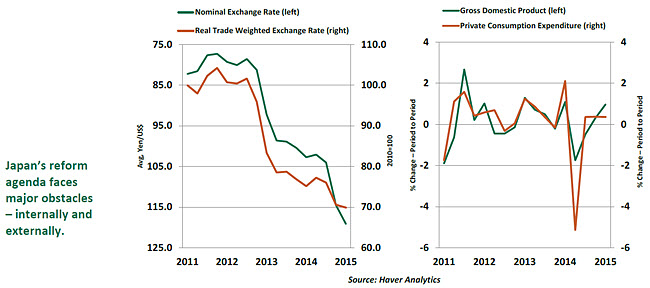

Yen weakness is also a constant topic of discussion these days. Most recently, the conversation has revolved around whether or not BOJ Governor Haruhiko Kuroda purposely intervened in the currency markets when he remarked that the yen was unlikely to fall further. It is more likely that the governor misspoke, yet his comments – and those of other bank officials – confirm that that the BOJ believes the yen should settle into equilibrium in the ¥120-125/$US level.

The central bank’s preference for currency stability, acceptance of weak CPI readings and signs of a nascent economic recovery could doom any additional stimulus in the short term. Previously, odds pointed to the BOJ adding to its Quantitative and Qualitative Easing program in October, but this now seems remote unless there is a significant downturn.

The government has also achieved a number of fiscal objectives. This includes remaining on course to halve its primary budget deficit by the end of fiscal year 2015. However, major reforms, including implementing the second phase of the consumption tax hike, will be needed to achieve a primary budget surplus by 2020.

Japan’s reform program faces two major risks at the moment – one internal and the other external. First, Prime Minister Shinzo Abe’s insistence on taking up unpopular national security reforms risks mudding his message and derailing the economic program.

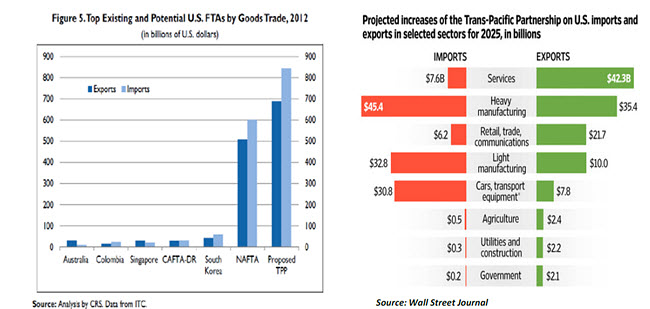

Second, the United States placed the landmark Trans-Pacific Partnership (TPP) in limbo with its failure to secure the required congressional approvals. The agreement is a key part of the structural arrow of Abenomics, with the terms of entry acting as an impetus toward greater market liberalization and deregulation. In addition, Abe has expended a lot of political capital to secure domestic acquiescence. The risk of a delayed or rejected agreement includes further erosion in his popularity, but also – and more importantly – a slowdown in reform momentum.

Japan’s progress to date is nothing to sniff at, but a lot of work remains. Agricultural reform, improved corporate governance and rising female workforce participation were once almost unthinkable goals. Now the government must achieve other Herculean feats, such as sustained inflation, solid economic growth and fiscal consolidation.

The Trials and Tribulations of Trade

The recent debate in the U.S. Congress is emblematic of rising global apathy (or even antipathy) toward deepening trade ties. A proposal to give the president fast-track trade promotion authority (TPA) to complete the TPP generated substantial opposition, and it is unclear whether the effort can be put back on track.

The objections raised are familiar ones. The main fear is that exposing workers to competition from overseas will result in lost jobs and lower wages. This fear is exacerbated by the fact that parties to the agreement may not be on a level playing field. Unless environmental rules, labor laws, and other regulation are symmetric across signatories, accusations of unfair dealing will inevitably arise. Because TPP is the largest free-trade agreement ever attempted by the United States, these issues have been magnified.  Consideration of TPA was tied to Trade Adjustment Assistance (TAA), a program that provides benefits to those who can demonstrate that free trade cost them their jobs. The TAA was expanded in the wake of the North American Free Trade Agreement (NAFTA), and most assume that it would be expanded again if the TPP was approved. The debate over the magnitude of any expansion centers on the proper balance of transition assistance and personal initiative.

Consideration of TPA was tied to Trade Adjustment Assistance (TAA), a program that provides benefits to those who can demonstrate that free trade cost them their jobs. The TAA was expanded in the wake of the North American Free Trade Agreement (NAFTA), and most assume that it would be expanded again if the TPP was approved. The debate over the magnitude of any expansion centers on the proper balance of transition assistance and personal initiative.

Almost lost in the debate are a couple of points which should not be overlooked.

- Free trade results in a wider selection and lower prices for consumers. Lower prices mean higher real wages. The benefits are difficult to estimate, but they accrue disproportionately to families in the lower-income quintiles.

- While all the focus is on the jobs that might leave the United States, the door can swing both ways. There are millions of Americans who work here for foreign companies, so our international employment deficit is not nearly as large as some suspect.

Each trade agreement is different, and the TPP is very complex. But before we reject it for good, we should conduct a complete and objective accounting.

(c) Northern Trust