To be considered prudent investors we must recognize and accept the undeniable reality that all true investing is done in future time. Consequently, the key to long-term investment success is to forecast the future as accurately as we possibly can. Of course, we must simultaneously recognize and accept that forecasting the future can only be accomplished within a reasonable degree of accuracy. Forecasting the future, and investing for that matter, can never be a game of perfect. Nevertheless, our investing success will ultimately be achieved based on how good our forecasts turn out to be.

With those realities in mind, there are multiple degrees of difficulty associated with the process of forecasting. In other words, even though all forecasting is dealing with unknowns, there are certain things that are more knowable than others. Once again, nothing about the future is perfectly clear, but there are certain future trends that are more unmistakably defined, and therefore, easier to make reasonably accurate forecasts upon. The aging of our population, also referred to as the graying of America, is one important demographic that lends itself to reasonably accurate forecasts.

The consumption patterns of an aging population are knowable and thus provide clues to potentially growing and profitable industries. For example, healthcare is an obvious business segment that will be called upon to serve our rapidly increasing elderly population. Consequently, it seems rational to conclude that many businesses operating in healthcare are poised for rapid and large growth. As a result, investors looking for attractive long-term opportunities would be wise to evaluate and consider investing in businesses in the healthcare sector.

However, even though forecasting is the key to future investment success, it is not the only or final step in the successful investing equation. Even when you have great confidence that you have identified a growing industry to invest in, prudent investors must still be careful about the valuation they must pay in order to invest. Prudent investors understand that price is what you pay, but value is what you get. Prudent investors recognize that you can overpay for even the best business or the greatest growth opportunity.

Additionally, although forecasting is the key, there is still a great deal of value and importance that can be gained from reviewing history. In fact, I believe it is wise and prudent to look at history first, if for no other reason than determining whether or not an individual investment is worthy of the work required before conducting a forecasting effort.

Attractively Valued Healthcare REITs: Exciting Opportunities for the Retired Dividend Growth Investor

A high and growing dividend income stream is widely considered as the primary attraction for investing in Real Estate Investment Trusts (REITs). By law, REITs are required to pay out at least 90% of their taxable income to shareholders each year. Additionally, publicly traded equity REITs provide investors the opportunity to participate in the growth of the underlying real estate while simultaneously providing liquidity not commonly associated with real estate.

Generally speaking, REITs are available in two broad categories, equity REITs and mortgage REITs. Equity REITs are available that participate in almost all aspects of the economy. However, this article is specifically looking at equity REITs that serve the growing healthcare segment of our economy. But most importantly, this article will be reviewing healthcare REITs that are currently attractively valued.

REITs and Interest Rates

However, before I specifically cover the healthcare REITs suggested below, a few words regarding REITs and interest rates are in order. There are many people that suggest and/or believe that REITs are specifically an asset class that is highly vulnerable to the prospects of rising interest rates. Moreover, there are many people that are avoiding good investment opportunities over this same fear. I am not sure, but wonder, precisely what these people are suggesting. If it’s a total collapse, lose all your money type of scenario, then I personally believe these fears are drastically overblown.

Rising interest rates might have a negative effect on stock valuations, at least in the short run. On the other hand, well-run businesses, REITs included, have prospered under various interest rate scenarios. But most importantly, I believe it is illogical to assume that equity values, REITs included, are doomed to collapse when interest rates do in fact increase. Interestingly, there are those that contend that just the opposite might occur. Therefore, I offer the following contrarian views about the impact of interest rates on equities, REITs included (Bold emphasis added is mine):

From Investopedia:

“The Bottom Line

The interest rate, commonly bandied about by the media, has a wide and varied impact upon the economy. When it is raised, the general effect is a lessening of the amount of money in circulation, which works to keep inflation low. It also makes borrowing money more expensive, which affects how consumers and businesses spend their money; this increases expenses for companies, lowering earnings somewhat for those with debt to pay. Finally, it tends to make the stock market a slightly less attractive place to investment.

Keep in mind, however, that these factors and results are all interrelated. What is described above are very broad interactions, which can play out in innumerable ways. Interest rates are not the only determinant of stock prices and there are many considerations that go into stock prices and the general trend of the market - an increased interest rate is only one of them. One can never say with confidence, therefore, that an interest rate hike by the Fed will have an overall negative effect on stock prices.”

Here are a few excerpts from an article in the Wall Street Journal found here:

“Although bonds usually beat stocks when rates rise, they haven’t always. The most extreme exception: the period from 1979 through 1982, when then-Fed Chairman Paul Volcker was increasing rates to snuff out inflation. Stocks outperformed bonds by a wide margin during that time.

Of course, financial history never repeats itself exactly, although it does rhyme. And the Fed’s monetary policy is just one of a multitude of factors that influence the stock market, so you would be foolish to base your investment decisions on that alone—especially because the central bank’s predictions of what it will do don’t always come to pass.”

This next excerpt from the same Wall Street Journal article speaks to the importance of valuation:

“Considering that U.S. stocks aren’t far below their all-time peak prices and are selling for a historically high multiple of profits, the past effects of rising rates are another reason for investors to be cautious. Differences in future returns depend mainly on how cheap stocks are in the present. So a rise in interest rates, if it took stocks down a peg, could be welcome for long-term investors.”

The following excerpts from Business Insider Magazine on May 19 of this year, provides an interesting perspectives:

“But are rising interest rates bad for stocks? It might seem so. After all, higher rates mean higher borrowing costs for corporations.

However, history suggests otherwise.

We note that since 1998, changes in bond yields and equity performance have been positively correlated, (i.e. equities and bond yields have risen together), as we can see below," Credit Suisse's Andrew Garthwaite said in a note to clients on Friday.

There are a few theories to justify this trend.

Typically a rise in inflation expectations is positive for equities (with equities being an inflation hedge) when inflation expectations rise from sub 2% to over 2%," Garthwaite added. Keep in mind, the stock market includes companies like Wal-Mart, Apple, and ExxonMobil, all companies that pass inflation to their customers and receive it right back for their investors.

In his note to clients on Friday, BMO Capital Markets Brian Belski also discussed this relationship between rising rates and rising stock prices. He explained that rising rates are actually a sign of good things to come.

Some of the best and most consistent average returns have occurred when interest rates have risen from very low levels – as is currently the case," Belski said. "From our perspective, this means that the bond market is correctly anticipating future economic growth and staying ahead of inflation – things that typically benefit stock prices."

Reviewing the data since 1985, Belski found that the least favorable interest environments for stocks were when rates were low, below average, and declining.

This makes sense to us since lower interest rates are typically reflective of sluggish economic growth and vice versa," he said.”

This article from US News provided fascinating results of a study by J.P. Morgan Asset Management:

“However, J.P. Morgan Asset Management looked at the relationship between the 10-year Treasury yield and the Standard & Poor's 500 index over the past 50 years, and the results were not what I expected. Instead of seeing a negative relationship between the two, they actually found there was a fairly strong, positive relationship in certain situations.

When the 10-year Treasury yield was below 5 percent, rising interest rates were generally associated with rising stock prices. Why, you ask? If the economy has slowed down and the Federal Reserve is taking steps to try to revive it, they will lower interest rates for the reasons above. But once the Fed sees signs of a recovery, they will reverse their course and raise rates,which signals investors that the problems plaguing the economy are starting to ease. With interest rates as low as they are and the stock market as high as it is, it will be interesting to see if this relationship holds true moving forward.”

Finally, this article from Forbes speaks directly to the fears of rising interest rates relating specifically to all REITs and notably healthcare REITs:

“On the other hand, if and when the Fed raises rates it will be because the economic data continues to improve. An improving economy means more jobs. That bodes well for office-related REITs like BXP and VNO. Higher employment and lower oil prices mean consumers have more money to spend. That should be good for mall and retail-related REITs like SPG, GGP and PLD. A stronger consumer also means better demand for housing and storage, boosting the prospects of REITs like AVB, EQR and PSA. Meanwhile, healthcare continues to be a bright spot in the U.S. economy buoyed by an aging population and Obamacare initiatives. This benefits healthcare-related REITs like HCN, VTR and HCP.

That all sounds good in theory, but what actually happened the last time the Fed raised rates? Starting in June of 2004 and ending in August 2006, short-term rates were hiked 17 times from a starting point of 1.00 percent to a peak of 5.25 percent. Over this two-plus year period, GDP grew steadily and commercial property values increased. Importantly, REIT investors were rewarded with more than a 60 percent return over this time frame, beating the overall stock market’s 20 percent rise. When including the past 6 tightening cycles going back to 1977, research has shown that REIT stocks appreciated in all but one.

I hold that the upcoming tightening cycle should look similar to the last one with rates climbing only if the economy continues to strengthen. A stronger economy will stimulate demand for commercial real estate at a time when new supply remains modest since construction activity never really recovered from the sharp downturn in 2008 and 2009. Rising occupancy demand and limited new supply should benefit landlord pricing, allowing the REITs to continue to grow their cash flows and support increased dividends.

Putting it all together, the combination of a patient Fed, strong commercial real estate fundamentals and history on our side, means REIT investors should not blindly fear a rise in interest rates. They would be better served embracing the improved economic activity that accompanies it.”

As I stated many times, I believe in making investment decisions one company at a time, and specifically on the merits of the company or companies I am examining. Therefore, to summarize this section on REITs and interest rates, I offer one of my favorite Warren Buffett quotes as follows:

"If we find a company we like, the level of the market will not really impact our decisions. We will decide company by company. We spend essentially no time thinking about macroeconomic factors. In other words, if somebody handed us a prediction by the most revered intellectual on the subject, with figures for unemployment or interest rates, or whatever it might be for the next two years, we would not pay any attention to it. We simply try to focus on businesses that we think we understand and where we like the price and management."

Three Healthcare REITs To Buy Now

Regardless of the level of the stock market in the general sense, I believe that the following three healthcare REITs are attractive at their current valuations. As I often state, it is a market of stocks and not a stock market. All stocks do not move in tandem with the market, and these first three healthcare REITs have recently fallen in this rising market. Additionally, this recent weakness has brought them to what I consider to be very attractive valuations. But most importantly, this weakness has occurred in spite of strong fundamentals.

As usual, I will be turning to the F.A.S.T. Graphs™ fundamentals analyzer software tool to illustrate why I consider these healthcare REITs attractively valued today. REITs are best valued based on funds from operations (FFO) and/or adjusted funds from operations (AFFO). F.A.S.T. Graphs™ recently added the AFFO metric, therefore, with each of the following examples I will provide historical graphs utilizing both metrics.

Seeking Alpha’s resident REIT expert Brad Thomas recently sent me an email and had this to say regarding AFFO versus FFO. “I view AFFO as a better proxy of operating performance sustainability than FFO as it eliminates one-time impacts, as well as other non-cash items that may cause short-term fluctuations.” Although I don’t disagree, I believe the reader will find that both of these metrics provide very reliable real-world valuation metrics for REITs.

With each of the examples I suggest that the reader focuses on the consistency of each of these healthcare REITs’ FFO and AFFO generation. Most importantly, analyze how stock price has tracked and correlated to those metrics. In each case the best times and the worst times to invest money is clearly revealed.

HCP Inc (HCP)

My first fairly valued healthcare REIT candidate, HCP Inc, offers the highest current yield and one of the best valuations of the four I will be presenting. Therefore, it may have stronger appeal for those retired and/or dividend growth investors most interested in current income.

The following is a short business description taken directly for the company’s website:

“HCP, Inc. is a fully integrated real estate investment trust (REIT) that invests primarily in real estate serving the healthcare industry in the United States. HCP's portfolio of assets is diversified among five distinct sectors: senior housing, post-acute/skilled nursing, life science, medical office and hospital.

A publicly traded company since 1985, HCP: (i) was the first healthcare REIT selected to the S&P 500 index; (ii) has increased its dividend per share for 30 consecutive years; (iii) is the only REIT included in the S&P 500 Dividend Aristocrats index; and (iv) is a global leader in sustainability as a member of the CDP, Dow Jones and FTSE4Good sustainability leadership indices, as well as the GRESB Global Healthcare Sector Leader. For more information regarding HCP, visit the Company's website at www.hcpi.com.”

HCP Inc (HCP): Price and FFO Historical Correlation

HCP Inc: Price and AFFO Historical Correlation (Note that there is limited AFFO history for this REIT)

HCP Inc: Performance

When reviewing the performance of each of these healthcare REITs, I suggest placing special attention on the yield advantage over the S&P 500. Although HCP is not an especially fast-growing healthcare REIT, its high yield and consistent dividend record has produced significantly more income than the S&P 500 over the timeframe measured. Moreover, even though it underperformed the index on capital appreciation, the combination of capital appreciation and total cumulative income produced a higher total return in the aggregate.

HCP Inc: Forecasting Calculators

As I indicated in the introduction, forecasting the future is the key to investment success. Although the leading analysts following the company and reporting to S&P Capital IQ continue to expect a moderately low future FFO growth, HCP’s high current yield and low valuation suggest very attractive future total return.

HCP Inc: Analyst Scorecard

My confidence is high regarding the potential accuracy of the above forecasts as supported by the Analyst Scorecard. In the past, the record of leading analysts when making one year forward and two year forward forecasts for HCP’s FFO growth has been extraordinarily accurate.

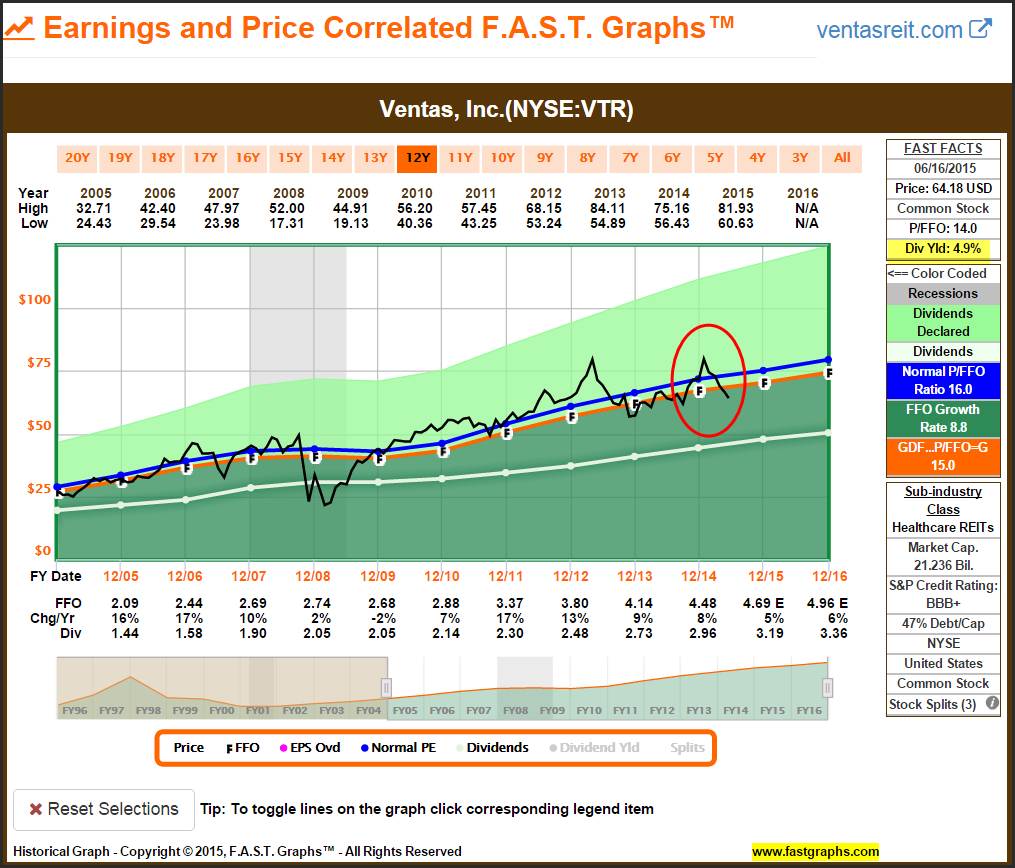

Ventas Inc (VTR): Price and FFO Historical Correlation

The following is a short business description taken directly for the company’s website:

“Ventas, Inc. (NYSE: VTR), an S&P 500 company, is a leading real estate investment trust (REIT), with a highly diversified portfolio of more than 1,600 seniors housing and healthcare properties in the United States, Canada and the United Kingdom. Approximately 75% of our NOI is derived from private pay, non-government sources.”

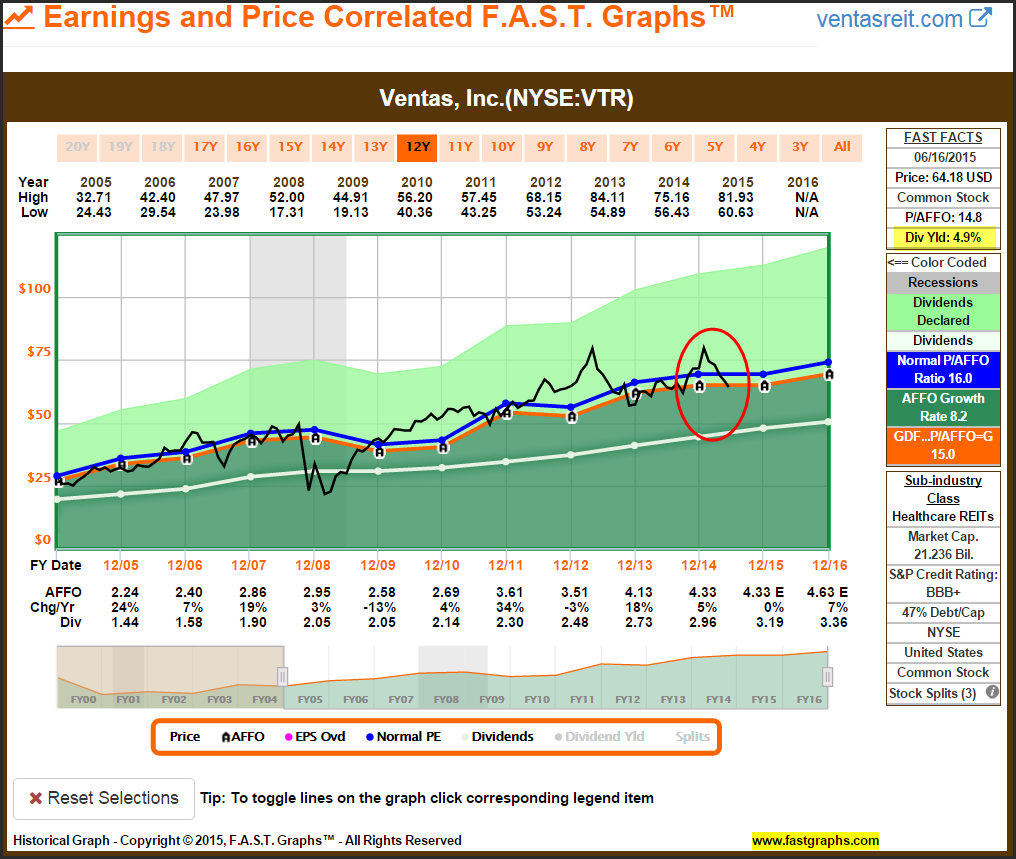

Ventas Inc: Price and AFFO Historical Correlation

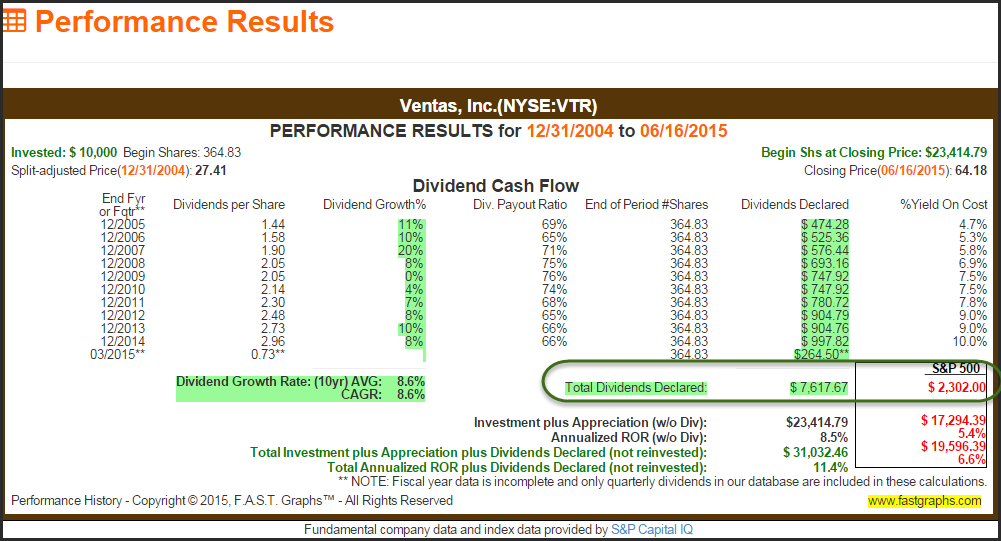

Ventas Inc: Performance

When reviewing the performance of Ventas, we once again see the yield attraction of high quality REITs. However, with this example we also have capital appreciation that outperformed the S&P 500 as well.

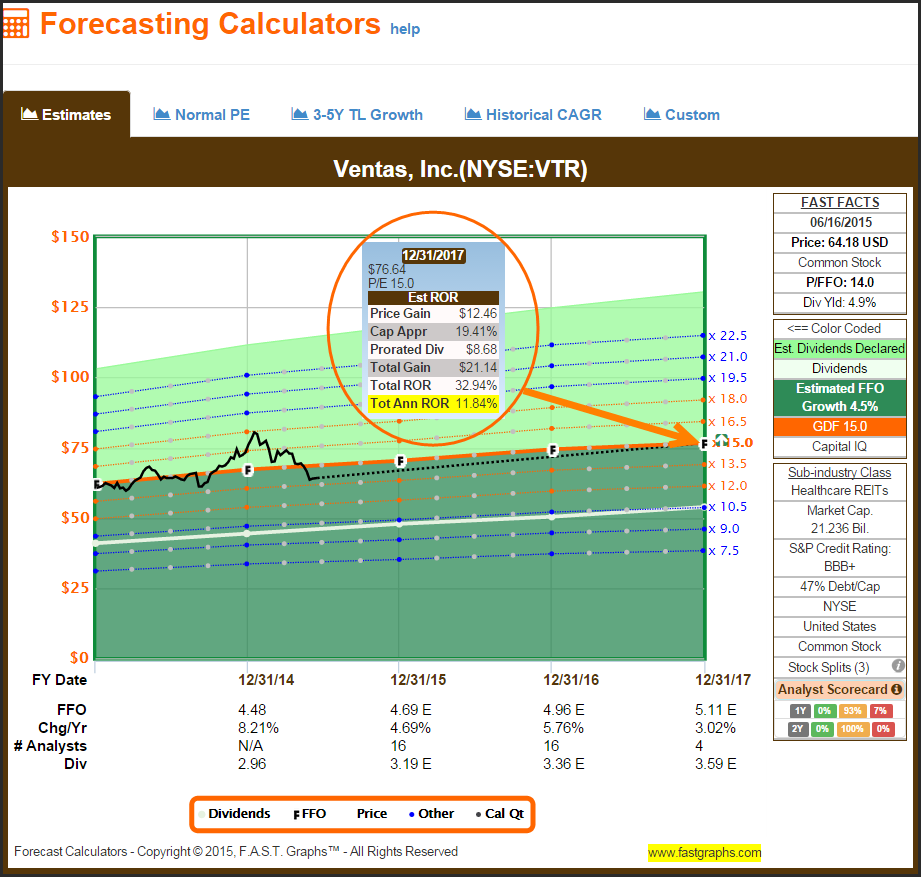

Ventas Inc: Forecasting Calculators

Ventas has moved into moderately undervalued territory, and based on consensus forecasts provides the opportunity for double-digit total returns out to fiscal year-end 2017.

Ventas Inc: Analyst Scorecard

My confidence is high regarding the potential accuracy of the above forecasts as supported by the Analyst Scorecard. In the past, the record of leading analysts when making one year forward and two year forward forecasts for Ventas’ FFO growth has been extraordinarily accurate.

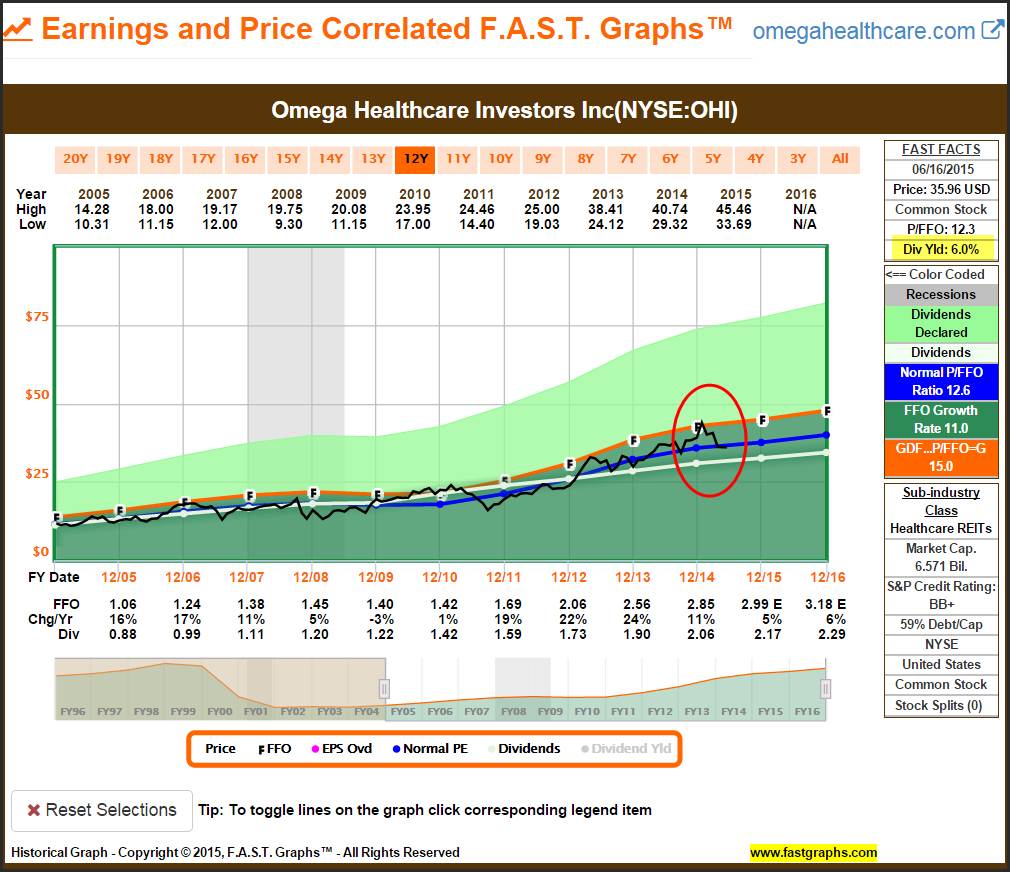

Omega Healthcare Investors Inc (OHI): Price and FFO Historical Correlation

The following is a short business description taken directly for the company’s website:

“Omega Healthcare Investors, Inc. (NYSE:OHI)is a Real Estate Investment Trust ("REIT") providing financing and capital to the long-term healthcare industry with a particular focus on skilled nursing facilities located in the United States.”

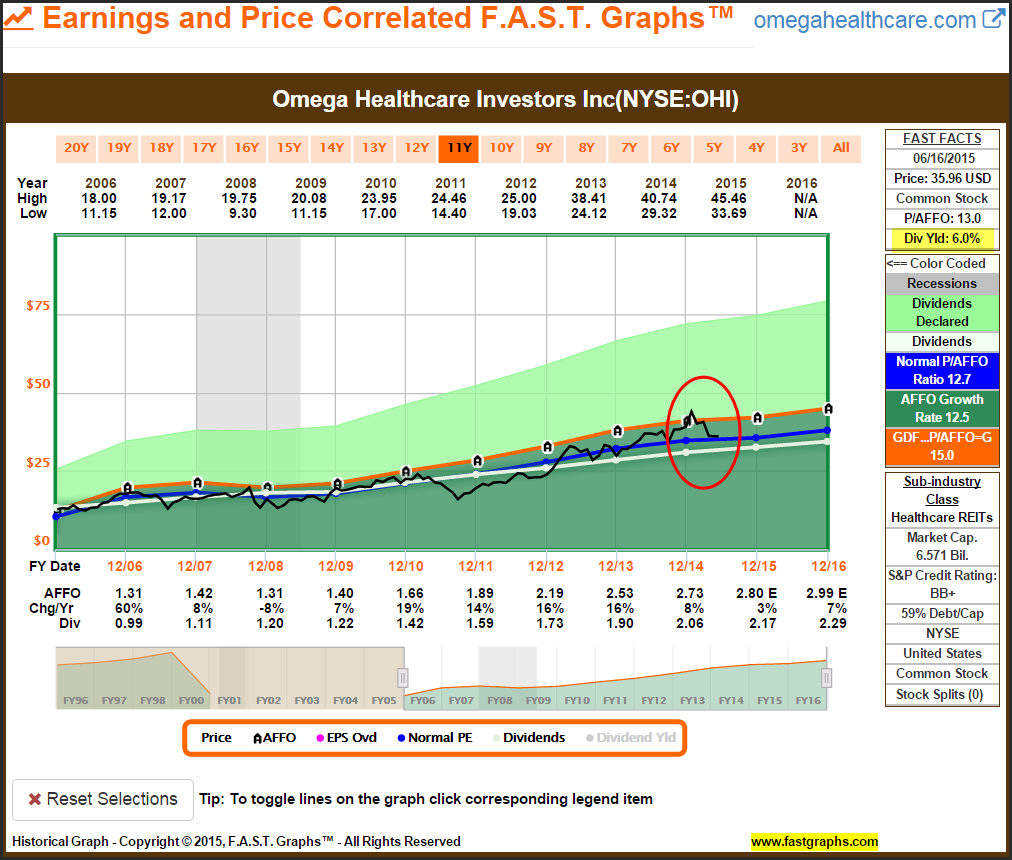

Omega Healthcare Investors Inc: Price and AFFO Historical Correlation

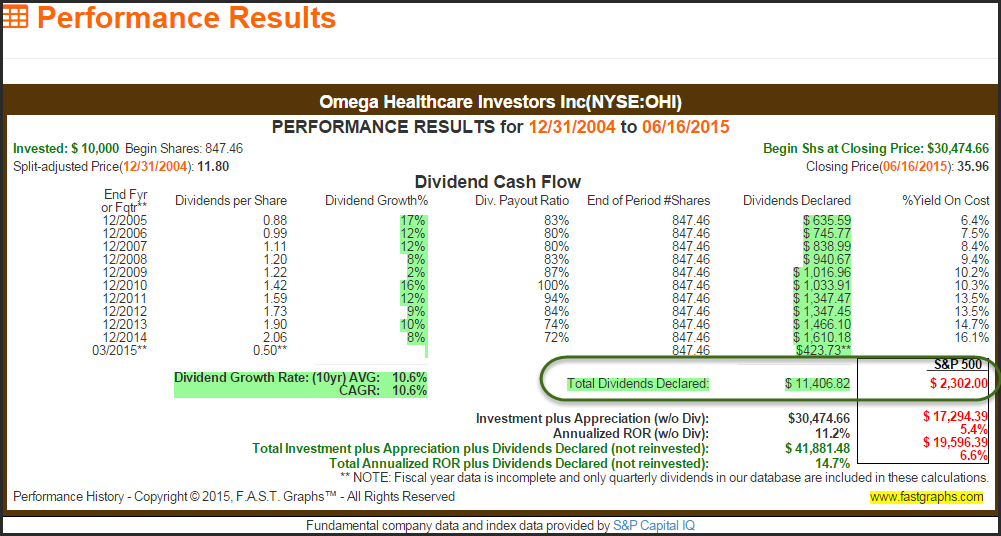

Omega Healthcare Investors Inc: Performance

Of all the heathcare REITs covered, Omega has generated the highest total annual return advantage over the S&P 500. More importantly for the income-oriented investor, total cumulative dividend income versus the S&P 500 has been orders of magnitude greater.

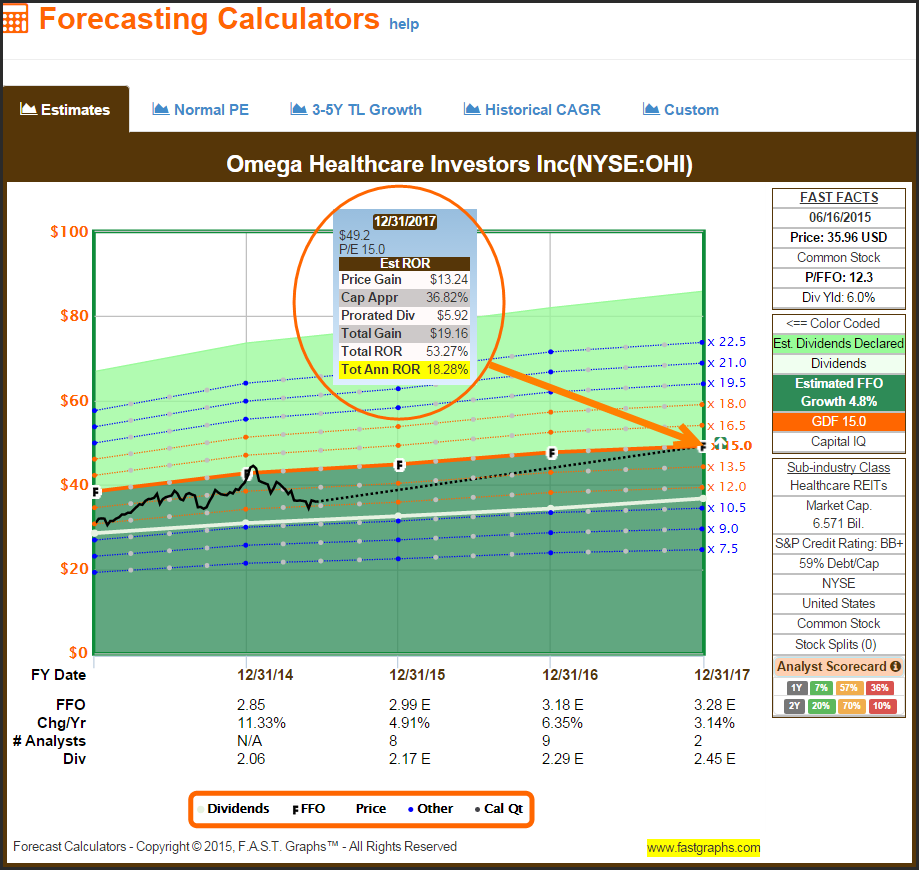

Omega Healthcare Investors Inc: Forecasting Calculators

Omega appears extremely attractive at current valuations. Attractive valuation plus high current yield present the opportunity for significantly above-average future returns out to fiscal year-end 2017.

Omega Healthcare Investors Inc: Analyst Scorecard

My confidence is high regarding the potential accuracy of the above forecasts as supported by the Analyst Scorecard. In the past, the record of leading analysts when making one year forward and two year forward forecasts for Omega’s FFO growth has been mostly accurate or above. Although the record is not quite as good for the one year forward forecast, it is still high enough to provide confidence.

One Healthcare REIT Worth Waiting For

My fourth healthcare REIT candidate has come down in value in a similar fashion to the other three. However, I do not consider it as attractive as the others. Therefore, I would suggest that prospective investors wait for a slightly better valuation. On the other hand, this healthcare REIT is not dangerously overvalued, just moderately so.

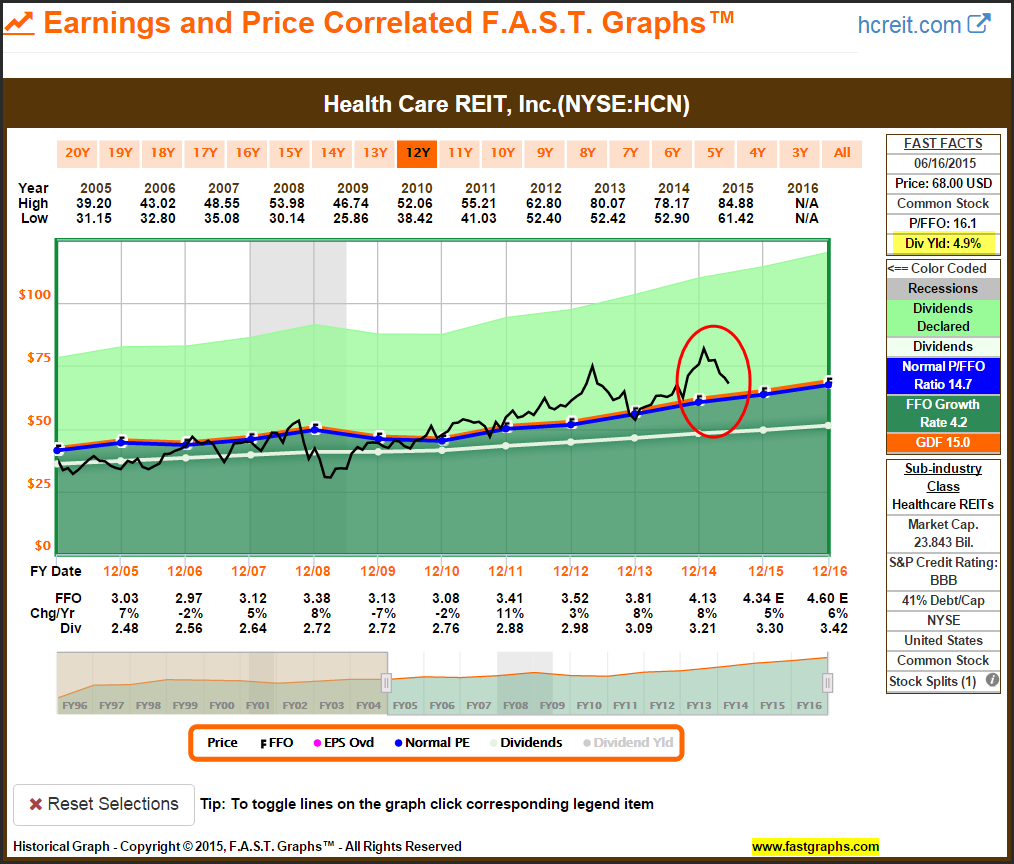

Health Care REIT Inc (HCN): Price and FFO Historical Correlation

The following is a short business description taken directly for the company’s website:

“HCN, an S&P 500 company with headquarters in Toledo, Ohio, is a real estate investment trust that invests across the full spectrum of seniors housing and health care real estate. The company also provides an extensive array of property management and development services. As of March 31, 2015, the company’s broadly diversified portfolio consisted of 1,384 properties in 46 states, the United Kingdom and Canada.”

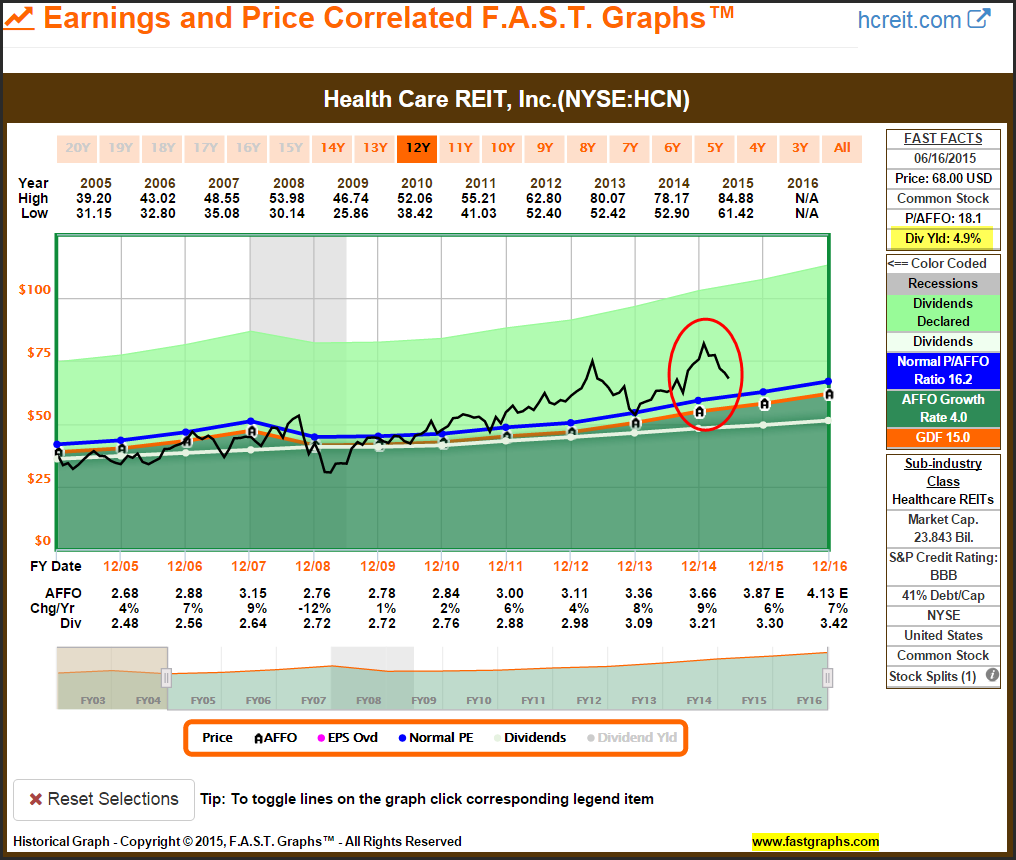

Health Care REIT Inc: Price and AFFO Historical Correlation

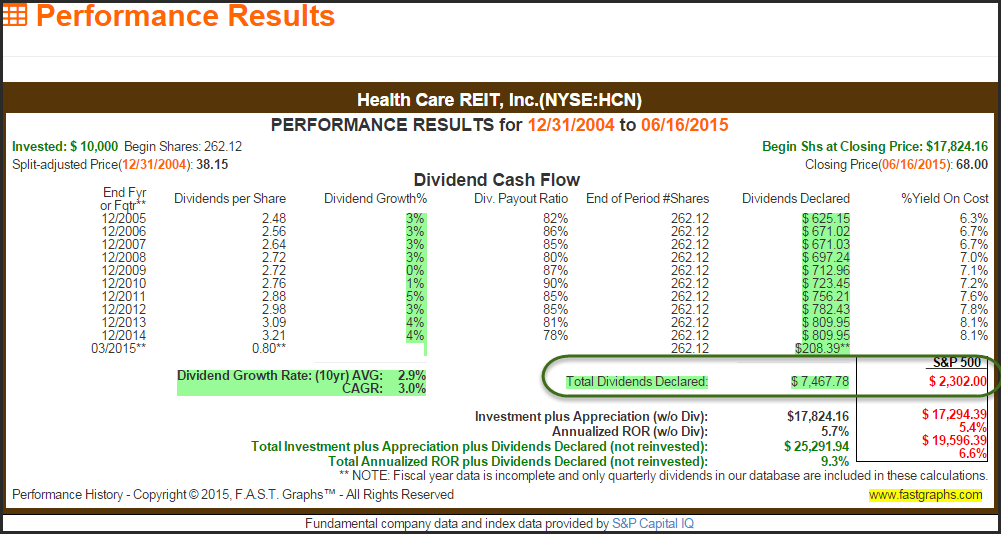

Health Care REIT Inc: Performance

Once again we see a significant total cumulative dividend income advantage over the S&P 500. However, I feel it’s important to point out that capital appreciation that is slightly better than the S&P 500 is partially attributed to moderate current overvaluation. Nevertheless, it should also be considered that the S&P 500 is also overvalued.

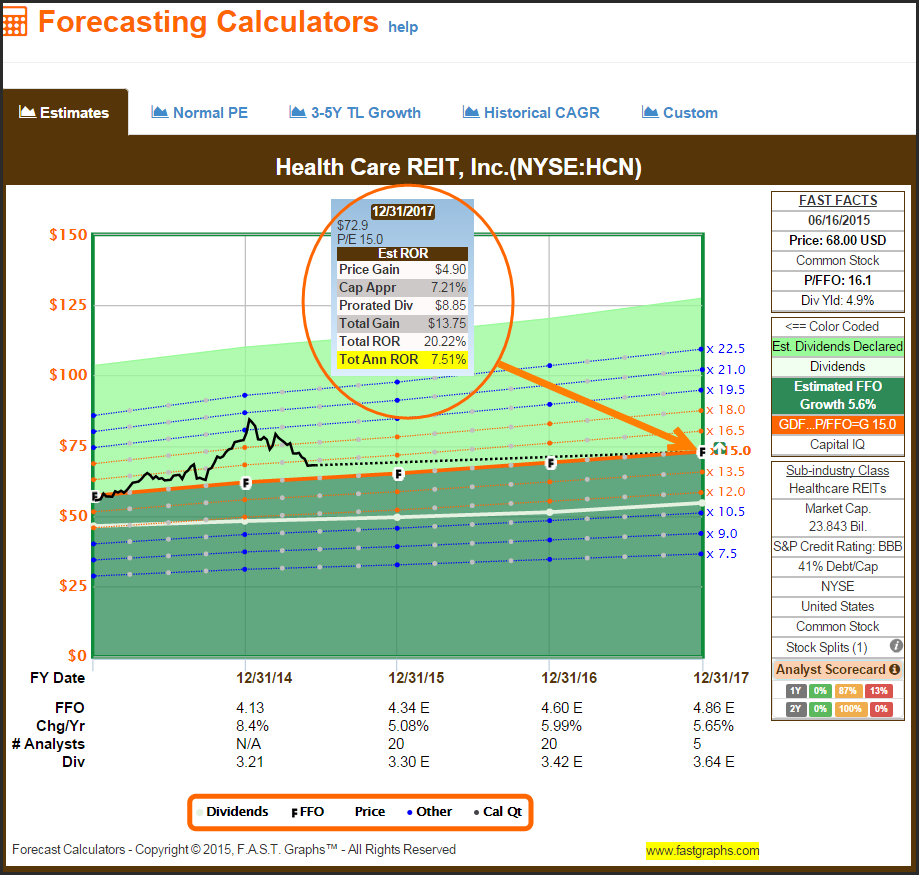

Health Care REIT Inc: Forecasting Calculators

Moderate overvaluation on Health Care REIT Inc reduces the potential total return out to fiscal year-end 2017 to single digits. Although the prospects for future growth are aligned with the other REITs covered, the significance of valuation is exposed.

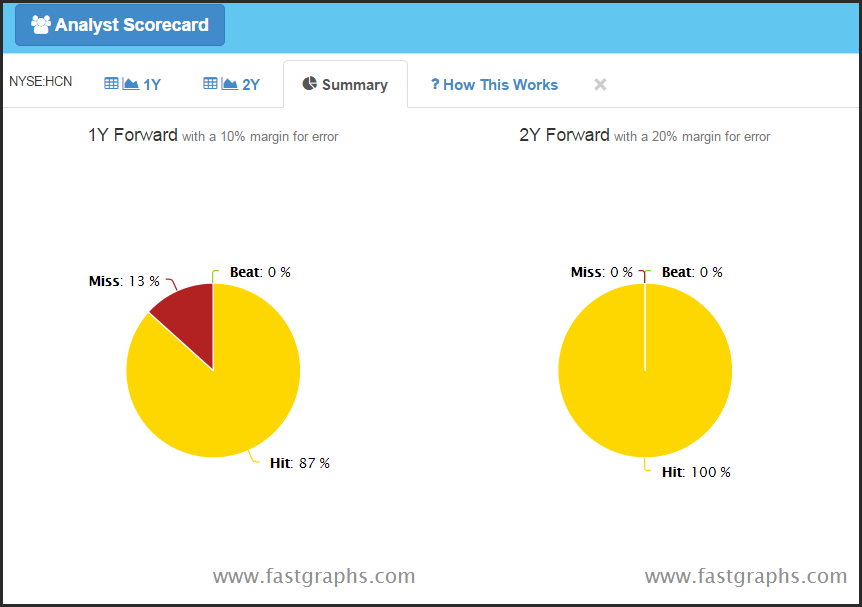

Health Care REIT Inc: Analyst Scorecard

My confidence is high regarding the potential accuracy of the above forecasts as supported by the Analyst Scorecard. In the past, the record of leading analysts when making one year forward and two year forward forecasts for Health Care REIT Inc’s FFO growth has been extraordinarily accurate.

Summary and Conclusions

The four healthcare REITs covered in this article have come off of highs established early in the year. Perhaps some of that recent weakness can be attributed to growing concerns that the Fed may raise interest rates soon. This seems like a logical assumption because there are many that believe that REITs are especially vulnerable to rising rates. However, regardless of whether that's true or not, I believe that most of the recent weakness in REITs is attributed to moderate overvaluation that was present early in the year.

Moreover, I believe that the powerful demographic force of our aging population supports the prospects for long-term growth of the businesses of healthcare REITs. More importantly, I contend that these demographic forces will overcome any potential short-term effects that higher interest rates might bring. Consistent with the views of others that I shared in the article, there are many considerations that drive the movement of stock prices, and interest rates represent only one.

As regular readers of my work will attest, I believe you make your money on the buy side. In the long run the rate of return you can expect from investing in a business will be driven by two important factors. First, and perhaps foremost, the long-term rate of change of earnings and cash flow growth (FFO and AFFO in the case of REITs) will generate and correlate to your future return. Second, the valuation you pay to buy that growth will determine whether you participate in all of that growth, some of that growth, or best of all, a return in excess of that growth.

Simply stated, if you invest at fair valuation you are well-positioned to participate in all of the company’s growth, if you overpay you are positioned to participate in only some of that growth, but if you invest when the valuation is low your return will be higher than the company's business growth. I believe that three of the healthcare REITs covered in this article are undervalued, and the fourth moderately overvalued, but worth consideration if, and when, valuation comes into alignment.

Disclosure: Long OHI at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.