Policywise, not much is expected out of this week’s meeting of the Federal Open Market Committee. The FOMC is unlikely to provide a clear signal on the precise timing of the initial increase in short-term interest rates. However, there should be plenty of information in the Fed’s revised economic projections and in Fed Chair Janet Yellen’s press conference.

The split between the Fed’s hawks and doves is widely overstated. Monetary policy decisions are generally arrived at through a broad consensus. Contrary to a recent op-ed in The Wall Street Journal, monetary policy is determined by the FOMC, not the Board of Governors. Recall that the FOMC sets the target range for the federal funds rate (the overnight lending rate). The Fed’s Board of Governors sets the primary credit rate (the “discount rate,” the rate the Fed charges banks for short-term borrowing) following a request by one or more district banks for a change (which may or may not be approved). The FOMC is made up of the five (normally seven) Fed governors, the president of the New York Fed, and four of the 11 other district banks (who rotate on and off each year). All 17 senior Fed officials participate at FOMC meetings, but only FOMC members get to vote on monetary policy. Still, the FOMC tends to be dominated by the board of governors and the governors tend to be dominated by the views of the Fed chair.

In their public speeches, senior Fed officials have clearly laid out the conditions that would lead to an initial rate hike, but also have listed a few caveats:

1) Officials want to see further improvement in the job market and they should expect that improvement to continue (however, judging how much slack remains and how rapidly that slack is being taken up are open questions, subject to different opinions);

2) Officials need to be “reasonably confident” that inflation will move back toward the 2% goal (the FOMC can hike well before reaching that goal, but the Fed’s track record on forecasting inflation hasn’t been good);

3) The timing of the first rate hike is much less important than the pace of tightening after the initial move (and that pace is expected to be very gradual);

4) Fed officials are aware of possible liquidity issues in the bond market, which could lead to excessive volatility in response to the Fed’s initial move (further reinforcing expectations that the Fed will move slowly);

5) Fed officials are aware of possible adverse reactions in emerging economies (as we saw in 2013’s taper tantrum – the FOMC will do what it has to do, but it also has to take into account the possible feedback from more unsettled reactions abroad).

The Labor Market Conditions Index, a composite of 24 indicators, suggests that slack is being taken up at a relatively rapid pace, but we still have a while to go before constraints hit. The May CPI report (due Thursday) is expected to show consumer price inflation at close to 0% over the last 12 months. Core inflation has remained low. Pipeline pressures are virtually nonexistent. The labor market is the widest channel for inflation pressure. Wage growth appears to have picked up, but not a lot and these figures are tentative. Moreover, Fed officials should be willing to tolerate a moderate pickup in wage growth.

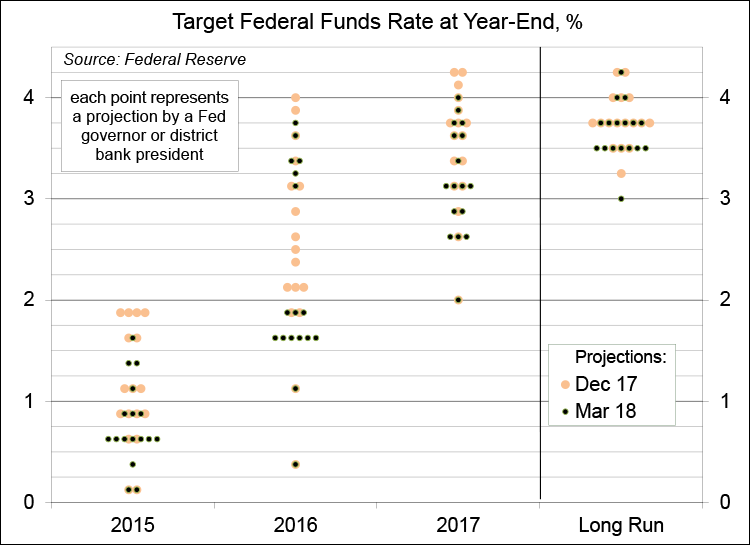

In March, Fed officials lowered their GDP growth projections. Forecasts of the appropriate year-end level of the federal funds rate edged lower. The less aggressive Fed policy outlook contributed to a reversal in the dollar.

Janet Yellen has cautioned against reading too much into minor movements in the dots. Indeed, there is a huge amount of uncertainty in each individual dot (that is, forecast). Market estimates of the path of short-term interest rates, such as seen in the federal funds futures, are more gradual than the most dovish Fed official. Why is that? The Fed’s forecasts reflect the most likely path seen by each Fed official. The market’s forecast is a risk-adjusted expectation. The Fed’s April survey of primary dealers showed that many expected that the Fed might be forced to return to the 0% lower bound after the initial hike.

FOMC members will likely want to see further evidence of a rebound in growth and then, beyond that, further evidence that growth will remain strong. This would put September as the most likely starting point (provided the data are in line with expectations), but the precise timing will depend on the data. The more important issue is the pace of tightening after the first move. In her speech of May 22, Fed Chair Yellen said that she expects that “it will be several years before the federal funds rate would be back to its normal, longer-run level.”