What The Great Recession Taught Me About Dividend Growth Investing

Ever since I first got interested in investing in stocks circa 1965 I have been confronted with a constant and persistent admonition about the next pending market crash. In those early days I contributed much of the negativity toward stocks to a lingering overhang from the Great Depression. Many of the people I was talking with had been literally traumatized by stern warnings from their parents or grandparents about the risk of investing in the stock market. Stocks were too risky for prudent people to invest in and serious money should never be invested there.

Now after working in the industry some five decades later, I still find that the attitudes of many investors have not changed very much. Of course the Great Recession of 2008 has served to perpetuate the negativity toward stocks in these more modern times. It seems the moniker that stocks are a risky asset class is firmly ingrained in the psyche of many people. Rarely a day goes by without my coming across an article, report or comment suggesting that the next market crash is imminent or just around the corner.

Making matters worse, at least from my perspective, is the litany of reasons offered as to why the market will surely and very soon collapse. To me, those reasons seem always to be related to exogenous forces that do not directly relate to a given company’s (stock’s) specific future business prospects. Of course, it’s alleged that they will or do, but I find them usually a matter of opinion and not supported by actual facts.

Typically these external factors are argued with predictions relating to esoteric discussions about the effects of Zirp, QE number something or other, debt levels, the future rise of interest rates, etc. Most unfortunately, they are delivered with the undertone suggesting a major economic collapse, and of course the demise of the value of our stock portfolios. Moreover, these predictions of impending doom imply, although they rarely say so directly, that common stock values are surely headed to zero. In other words, if we don’t heed their stern warnings, we are destined to lose all of our money.

However, somehow common stocks, especially high-quality dividend growth stocks, continue to provide prudent investors with solid long-term returns and a growing dividend income stream. The occasional disruption does come along from time to time, but rarely lasts as long as people fear. Moreover, these disruptions do not hurt prudent levelheaded investors, but only those that are fearful. In other words, smart investors persevere and hold on, and only those willing to sell perfectly valuable assets for less than their worth get hurt - in the long run.

Fellow Seeking Alpha Author Chowder recently penned a terrific article titled “Dividend Growth Investing Requires Perseverance” that speaks loudly to the point I was making in the above paragraph. If you haven’t read it, I highly suggest that you do. I especially enjoyed his sharing of one of my favorite Calvin Coolidge quotes, and I repeat it here:

"Nothing in this world can take the place of persistence. Talent will not; nothing is more common than unsuccessful people with talent. Genius will not; unrewarded genius is almost a proverb. Education will not; the world is full of educated derelicts. Persistence and determination alone are omnipotent. The slogan 'press on' has solved and always will solve the problems of the human race." - Calvin Coolidge.

However, as much as I admire the sentiment offered in Chowder’s article and as much as I believe in the validity of the Calvin Coolidge quote, I do feel compelled to offer a qualifier. Persistence is certainly a powerful and salient attribute to embrace - especially for retired investors. On the other hand, I also believe that it must be “intelligent” perseverance.

As it relates specifically to investing in dividend growth stocks, I refer to it as “intelligent patience.” In other words, perseverance and patience become intelligent when it is founded on sound and rational principles. Holding on to a lost cause turns persistence into mere stubbornness. Behaving in that way usually leads to a bad outcome. In contrast, expressing bravery (patience and persistence) to a worthy cause will lead to victory and success.

This then begs the question: When investing in common stocks, when and how can you determine that the cause is worthy, and therefore, validate the value and intelligence of being persistent and patient? The answer is quite simple and is revealed by what you focus on. When you are only focused on stock price you can be easily misled into making horrific investing mistakes. A dropping stock price engenders fear, which as we all know is a powerful emotion that can make smart people do dumb things like selling a valuable business at the bottom of a market for less than it’s worth. This is reactionary behavior rather than intelligent behavior.

What The Great Recession Taught Me About Dividend Growth Investing

Most investors take their lead from stock prices. If they buy a stock and it goes up, they consider it a good stock. If they buy a stock and it goes down, it’s a bad stock. In all fairness, for most investors, stock prices are all they have to judge their decisions by. However, there is a primary reason why I start this section out by discussing stock prices. Investors whose focus is solely on stock prices are not investors under my strictest definition of an investor. Instead, from my perspective, they are speculators in the stock market. Personally, I do not speculate in the stock market - never have and never will.

As it relates to common stocks, I consider someone a true investor when they are focused on becoming an owner/partner in a good business. Therefore, to my way of thinking, the true investor is primarily focused on the business they own. Consequently, they are positioning themselves to be owners of the business they invested in for a long time to come. Therefore, it logically follows that their primary attention is best placed on the operating results that their business generates on their behalf as owners.

Most importantly, the true investor that buys their investment from the stock market understands going in that it is an auction. As such, they understand that prices will fluctuate as other people place bid and ask orders continuously. However, since they have no intention of selling their business ownership in the near future, the daily, weekly, monthly or even yearly fluctuations in price are of no interest or concern to them. They are primarily interested in and concerned about how the business is doing, because from their perspective they own the business, not the stock.

At this point, I would like to turn our attention to the Great Recession and the lessons it taught about dividend growth investing. First of all, I believe that most everyone would agree that the Great Recession of 2008 was severe. In fact, it was one of the worst recessions our country ever experienced, with the exception of the Great Depression of 1929. Consequently, I don’t want any reader to think that I do not recognize and acknowledge just how bad those economic times were.

On the other hand, as it relates to high-quality blue-chip dividend growth stocks, I intend to demonstrate that the Great Recession was not as devastating, at least to the true investor, as many people believe. On the other hand, I will also demonstrate that the Great Recession was traumatic and in many cases catastrophic to those speculators that took their lead solely from stock price movement. In order to support my point, I will as usual turn to the F.A.S.T. Graphs™ earnings, dividends and price correlated fundamentals analyzer software tool.

Johnson & Johnson (JNJ)

AAA rated Johnson & Johnson is widely-held and highly-regarded as one of the highest quality dividend growth stocks on the planet. So first let’s look at how this blue-chip’s stock price performed during the Great Recession. I start out with stock price action because one of the most frequent comments I receive goes something like this:

“Should we be concerned that when the general market goes down it will take even well valued stocks down with it?” Or this: “Just as a rising tide tends to lift most/all boats, a falling tide tends to take most down with it. If the market tanks, even the best stocks are likely to be hit. Just my opinion.”

Now without question, those comments are most likely accurate and contain truth. In other words, in the short run, most stocks will rise and fall with the overall short-term behavior of the market. To paraphrase an old Ben Graham comment he allegedly once said, that everything he knows about the stock market can be summed up in two words - “it fluctuates.” But as I stated earlier, if I am not intending to sell the stock (the business) for years to come, my curt response is - so what! Stock prices will surely fluctuate in the short run, but in the long run my returns will be a function of the success of the business that I am an owner of. Therefore, I am most concerned with how the business is doing over worrying about short-term price volatility that I cannot predict or control anyway. Stated succinctly, I believe that all this fear about short-term price volatility is much ado about nothing.

This brings me to a few remarks regarding other price-focused comments that I often hear that frankly concern me. Many readers will talk about strategies where they implement stop losses, or follow a rule that if the stock falls a certain percentage, for example 10%, they immediately sell. I never understood the logic of those strategies because of my strong focus and commitment to valuation. If I was careful to only invest in a company when I calculated that its valuation was sound or attractive, then it seems straightforward to me that if the price fell from that level, the company has simply become more attractive at the lower price.

Consequently, instead of risk I see opportunity when that happens. I just don’t understand the logic, nor do I see the benefit of selling a perfectly valuable asset for less than it is worth simply because of fear. Furthermore, I understand that not all stock price drops are the same. I do become fearful when I see one of my holdings become dangerously overvalued. This is because if a company’s stock price drops from insanely high valuations, it may take years for it to recover - if ever. On the other hand, if a company’s stock falls from fair valuation, or better yet attractive valuation, recovery is usually very quick, and I contend inevitable.

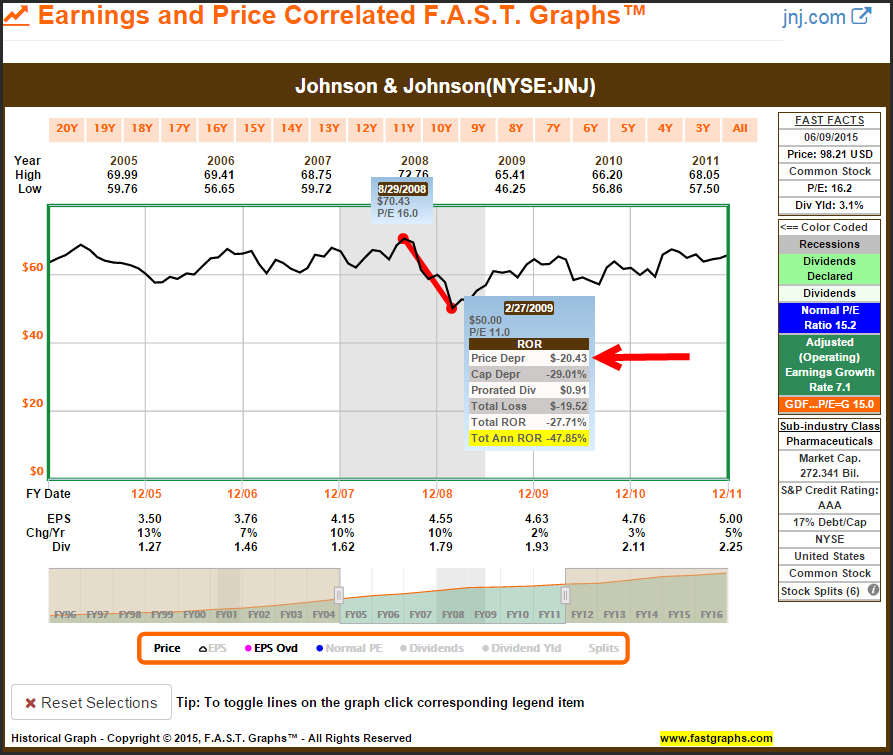

Let’s test these postulates by examining Johnson & Johnson’s (JNJ) stock price action in the real world scenario of one of the worst recessions in history. On August 29, 2008 Johnson & Johnson traded at $70.43, a high mark for the year. By February 27, 2009, Johnson & Johnson’s stock price fell to $50 per share, its low mark during the recession representing a 29% reduction in value. Although this was better than many stocks performed during the recession, it was clearly a large and frightening fall from grace. If all you had to go by was stock price, no one could blame you for becoming scared and disturbed because a 29% loss is significant.

However, if you were a business owner (true investor) that was focused on operating results (fundamentals) your view of Johnson & Johnson would be totally different. In fiscal year 2008 (the Great Recession) Johnson & Johnson grew their earnings by 10% and raised their dividend 11% from $1.62 the previous year to $1.79. For Johnson & Johnson the business, there really was no recession. But, as we saw above, the stock price did drop from its high mark to its low mark.

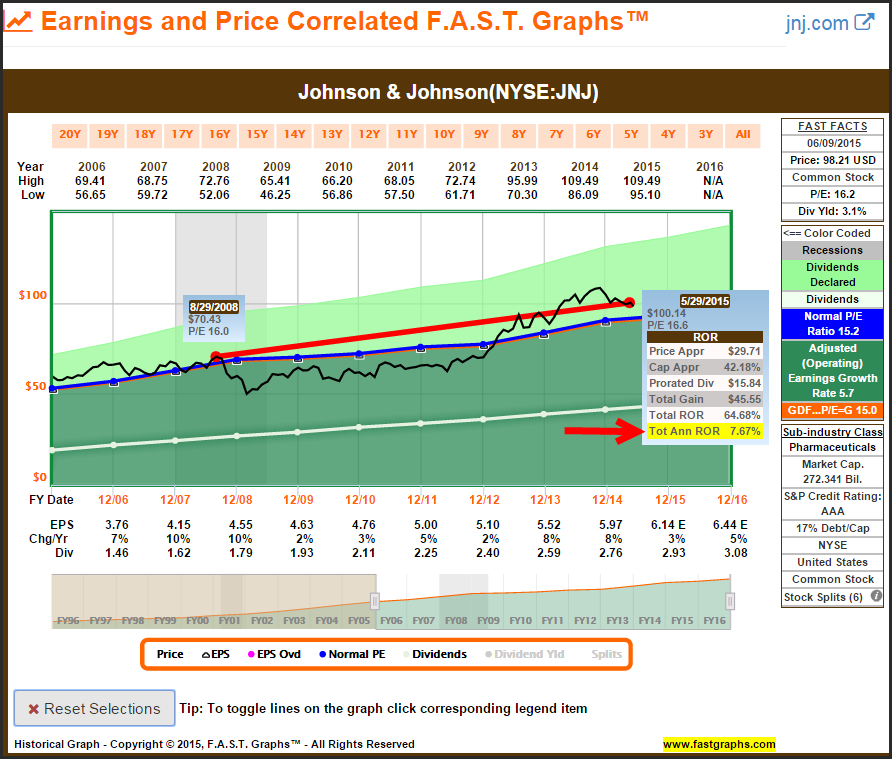

Now, if we bring price back into the equation, we discover that Johnson & Johnson was actually reasonably valued (perhaps a smidge overvalued) at its high mark during the Great Recession. Therefore, if we had followed the strategies of selling referenced above, we would have lost a significant amount of money on Johnson & Johnson. However, if we would have simply focused on the business instead and held onto our shares, our long-term return would be an acceptable 7.35% per annum when considering the quality of this company. It should also be noted that we would have also received almost $16 per share of dividend income, which contributed significantly to our total return.

Furthermore, if we recognized the opportunity that the recessionary price drop created, we could have exploited other people’s folly. Instead of losing money by selling, we could have bought Johnson & Johnson and increased our long-term total return on our new purchase to just short of 14% per annum. Once again, I just don’t see the logic of selling a perfectly valuable asset for less than it’s worth. Buying more when the opportunity presents itself makes more sense to me. Of course, that opportunity only becomes apparent if you’re focused on the business instead of the price.

The Coca-Cola Company (KO)

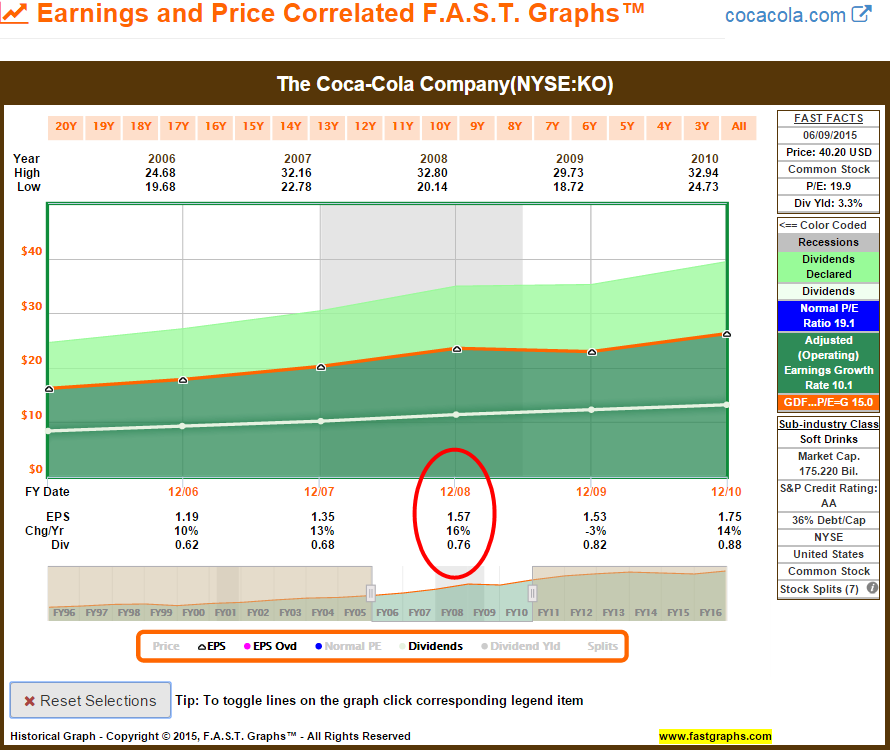

With my second example I will look at the highly regarded AA rated blue-chip dividend growth stock Coca-Cola. I chose this example because it offers additional lessons about dividend growth stock investing and recessions that we didn’t see with Johnson & Johnson. For starters, Coca-Cola’s stock price began falling at approximately the same time we entered the recession. Nevertheless, in a similar fashion to Johnson & Johnson, Coca-Cola’s stock price fell approximately 34%, but actually held up better than most companies which on average fell approximately 50%. Regardless, a 34% drop in value is significant.

From the perspective of business results, Coca-Cola also performed admirably during the recession. Earnings grew by 16% in 2008 and their dividend increased 12%. On that basis, the recession year 2008 was actually a good year for Coca-Cola owners.

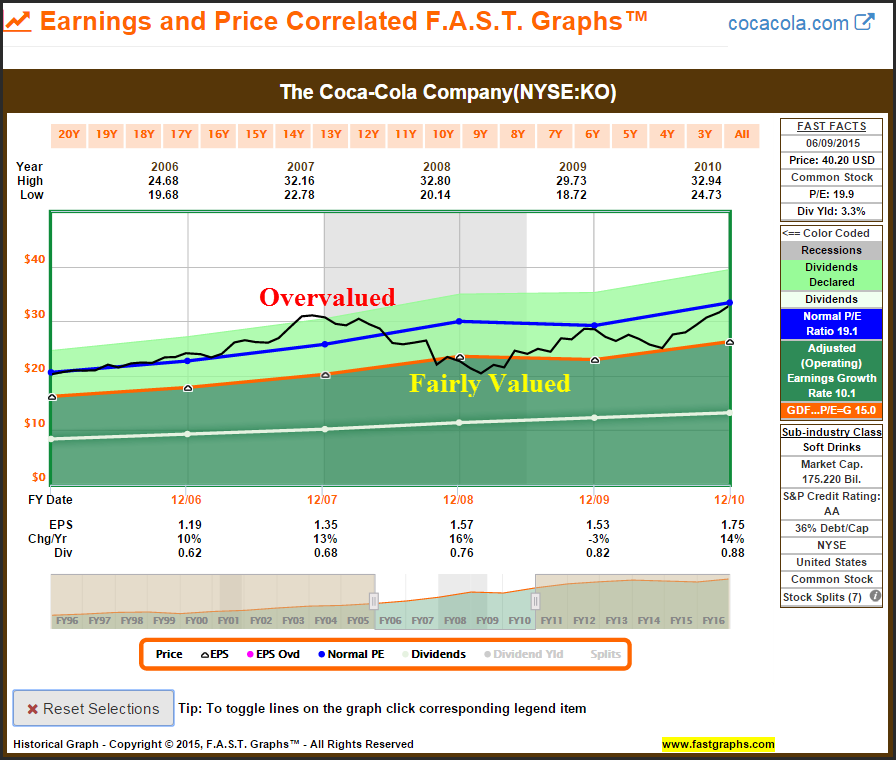

However, when we look at both stock price valuations and business results simultaneously, the additional lessons referenced above are revealed. Coca-Cola’s stock price was actually overvalued as we entered the Great Recession of 2008, even if you’re willing to award them the normal quality premium valuation of a P/E ratio of 19 to 20 (the dark blue line on the graph).

There are two simple lessons that I believe this example provides. First of all, the company’s stock price falling from a high valuation (overvaluation) is more dangerous than what we saw with Johnson & Johnson where price fell from being fairly valued to becoming undervalued. In contrast, Coca-Cola’s stock price fell from being overvalued to becoming fairly valued.

The second lesson that I personally find very interesting and important, is that Coca-Cola’s stock price held up extremely well once it entered fair valuation territory (the orange line on the graph) even though the recession continued for several months thereafter. Not all price drops are the same.

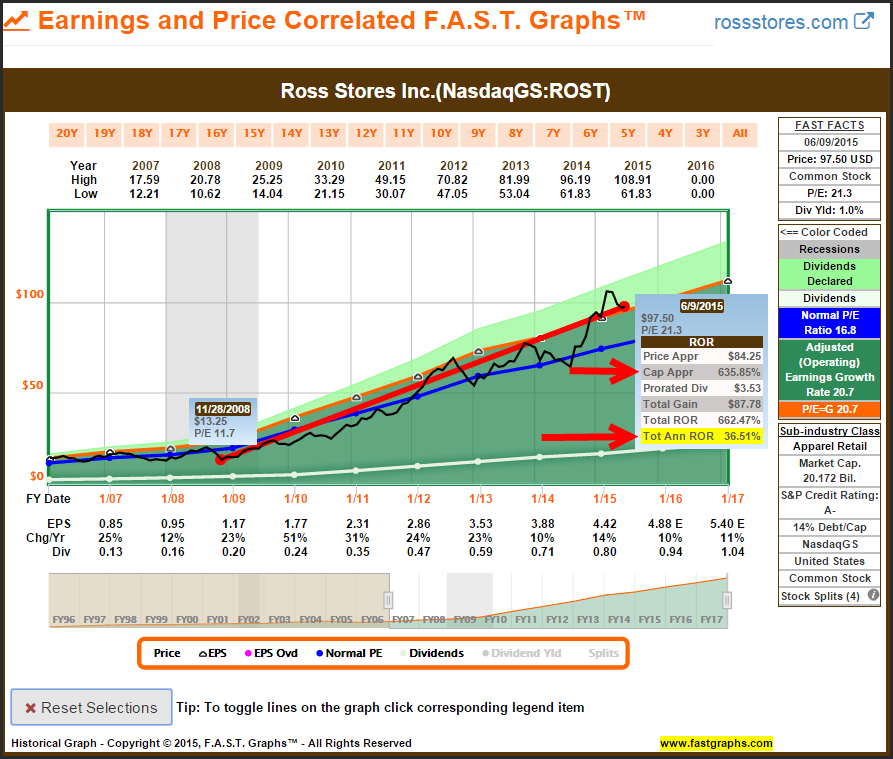

Ross Stores Inc. (ROST)

With my third example, I will examine A- rated Ross Stores, a fast-growing off-price apparel and home fashion retailer. Arguably, recessions could even be considered economic periods of opportunity for Ross Stores. Nevertheless, since “a falling tide drops all boats” Ross Stores experienced a 34% price drop from its high to low price during the Great Recession. However, even when looking only at the company’s stock price, we discover that the price drop was swift but short, and total recovery occurred even before the recession ended.

When we turn our attention to operating results only without stock price to contaminate our perspective, we discover that there was no recessionary pressure on Ross Stores’ business. Fiscal year 2008 was solid with a 12% earnings growth rate, and fiscal years 2009 and 2010 could be considered extraordinary. Dividend growth exceeding 20% each year followed suit.

This next graph illustrates what I believe is the folly of selling a great business simply because the price drops by a certain percentage. If you had placed a stop loss on Ross Stores of say even 20%, you would have clearly been selling a very valuable asset for less than it was truly worth. Instead of protecting your money, you would have simply denied yourself the opportunity to grow your money over six-fold or given up a 36.5% annual compound rate of return.

Several More High-Profile Dividend Growth Stock Examples

In order to more strongly drive this point home, I offer several additional examples of high profile dividend growth stocks that maintained strong and healthy operating results through the Great Recession. With these examples, I will let the graphs speak for themselves. They are offered in the same format and sequence as the examples above. In order to benefit from this exercise, I suggest that the reader focuses on the earnings and dividend records of each company prior to, during and following the Great Recession.

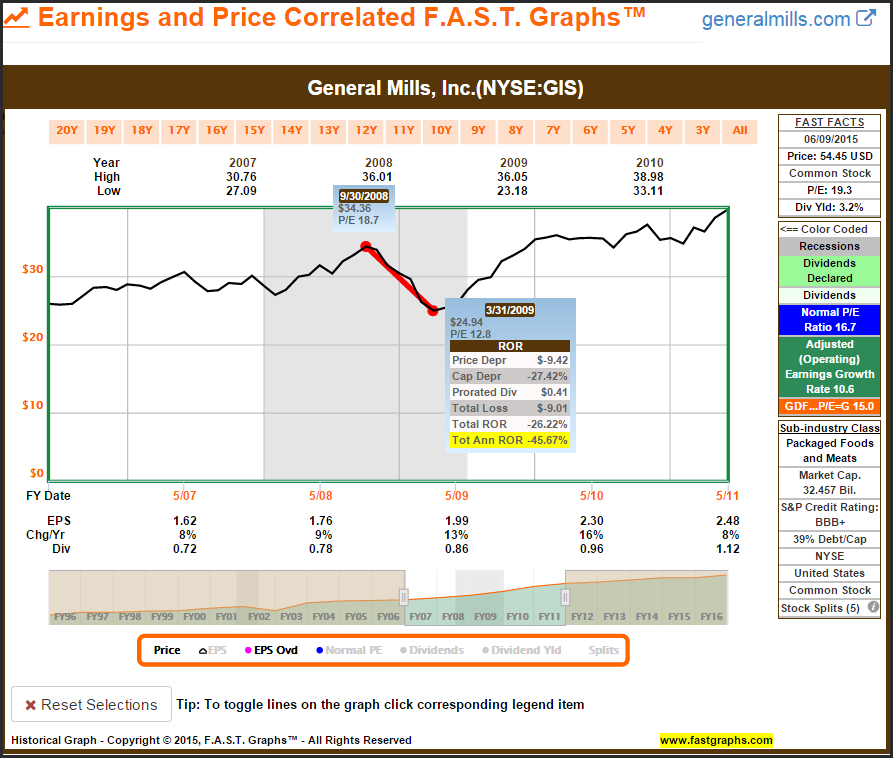

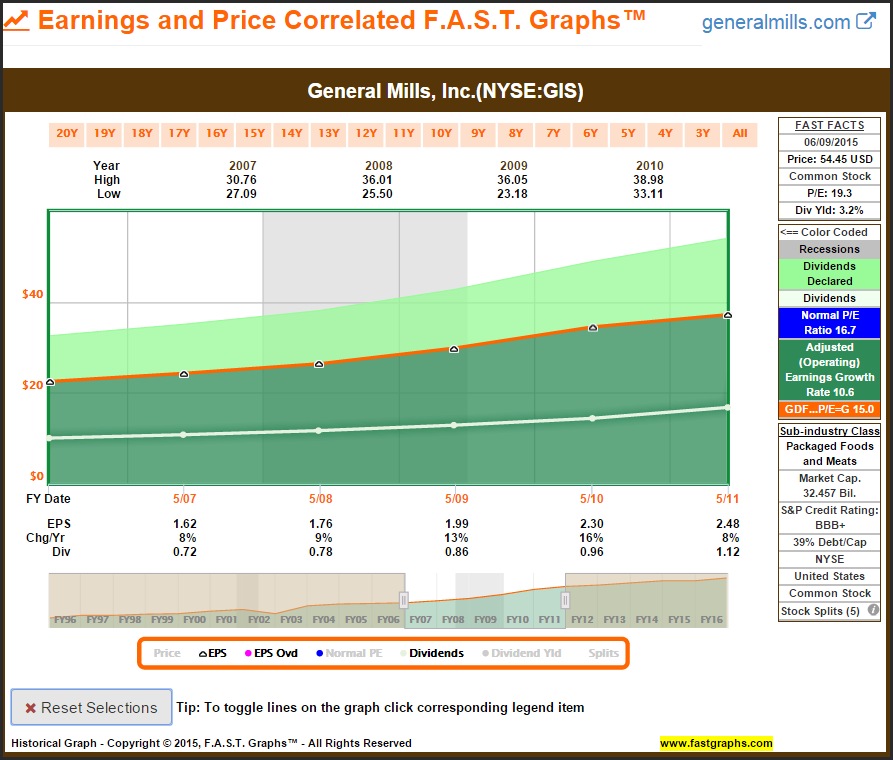

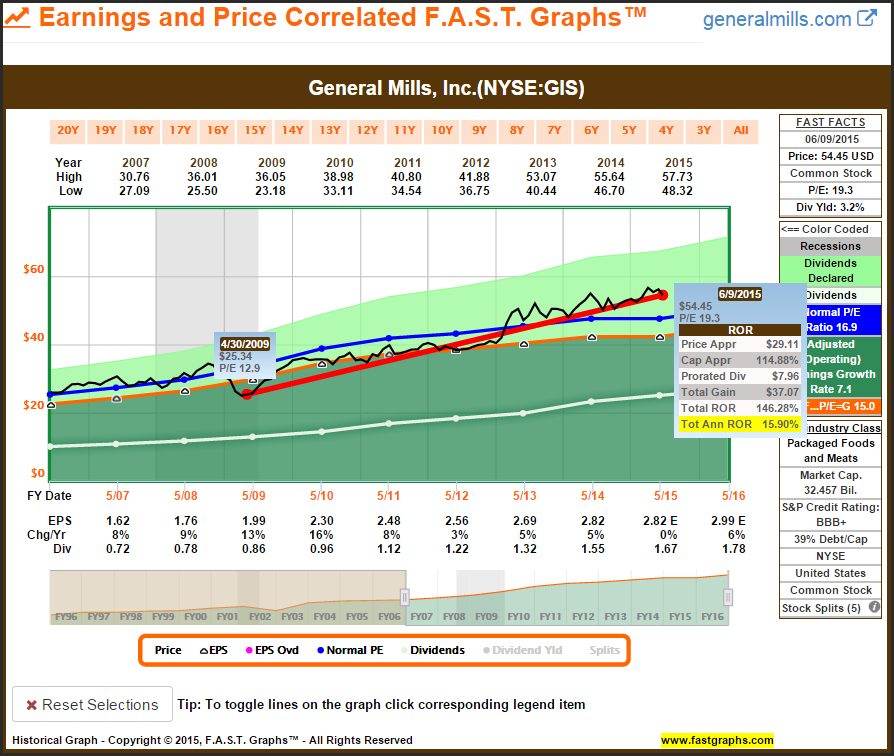

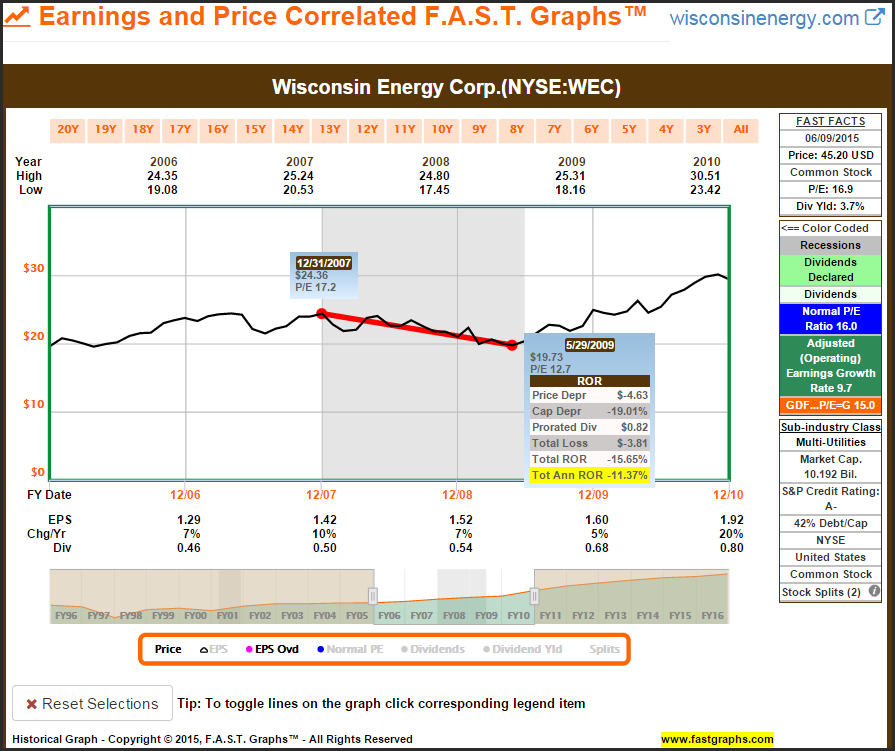

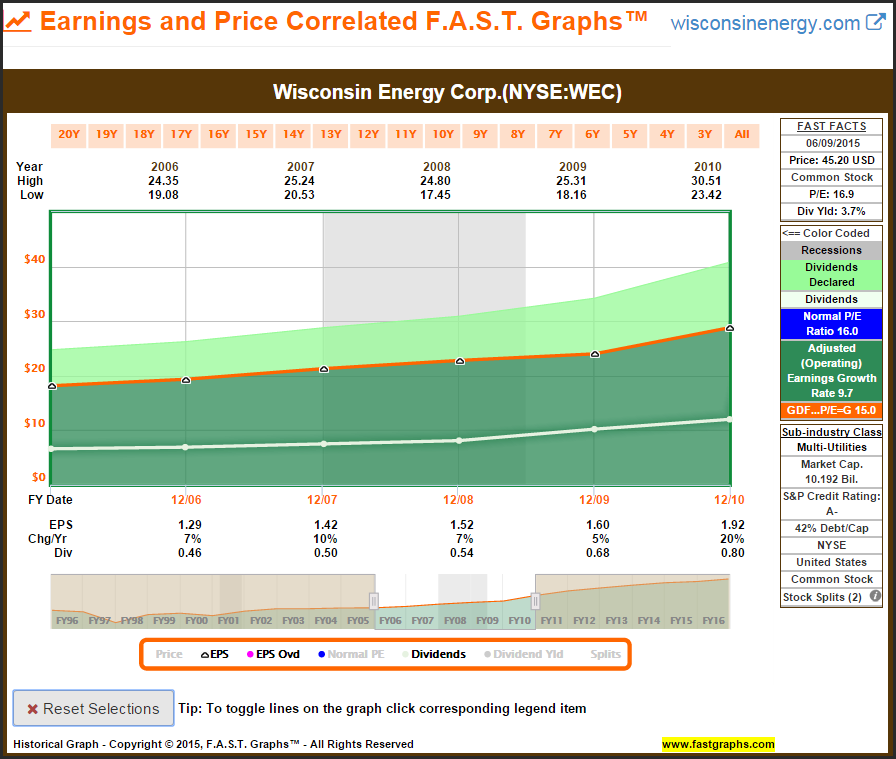

From my perspective, the most important lesson that these and the above examples provide is the power and protection of sound valuation. Notice that none of these companies would have presented significant price loss or stress when they were trading at fair valuation (price touching the orange line). If their valuations were high coming into the recession, the price drops were more pronounced. However, measured from any point when fair valuation was present, virtually eliminated any significant price reductions.

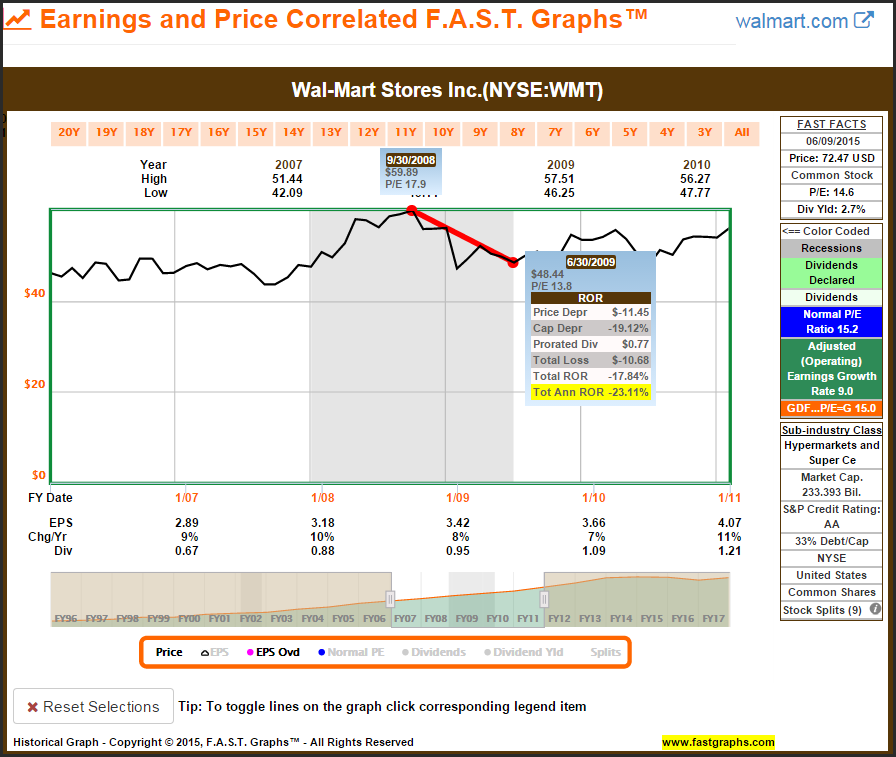

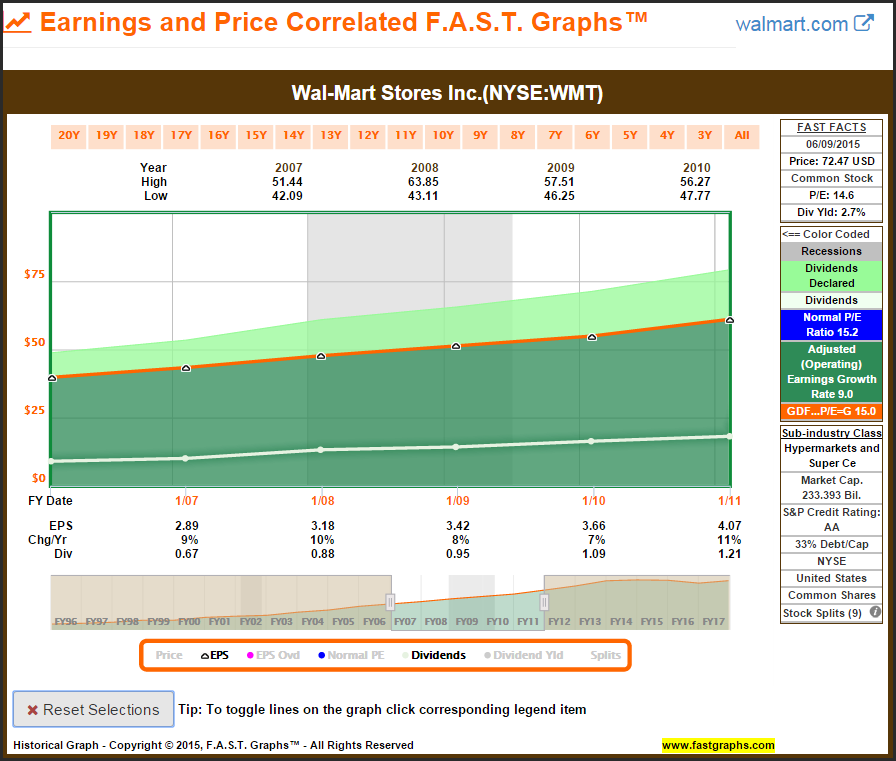

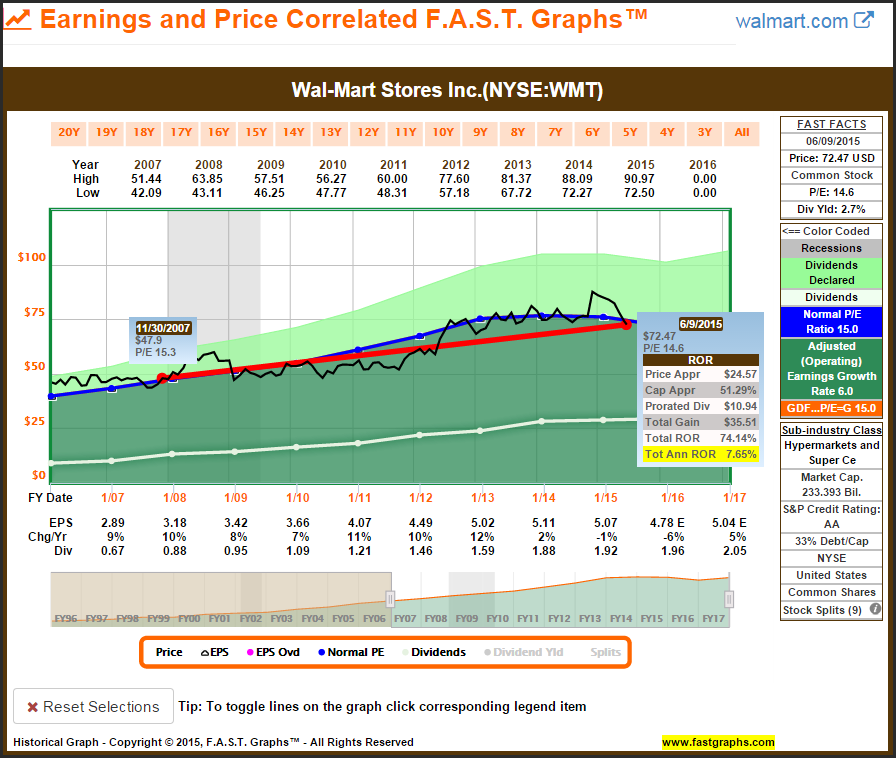

Wal-Mart Stores Inc (WMT)

General Mills Inc (GIS)

Wisconsin Energy Corp (WEC)

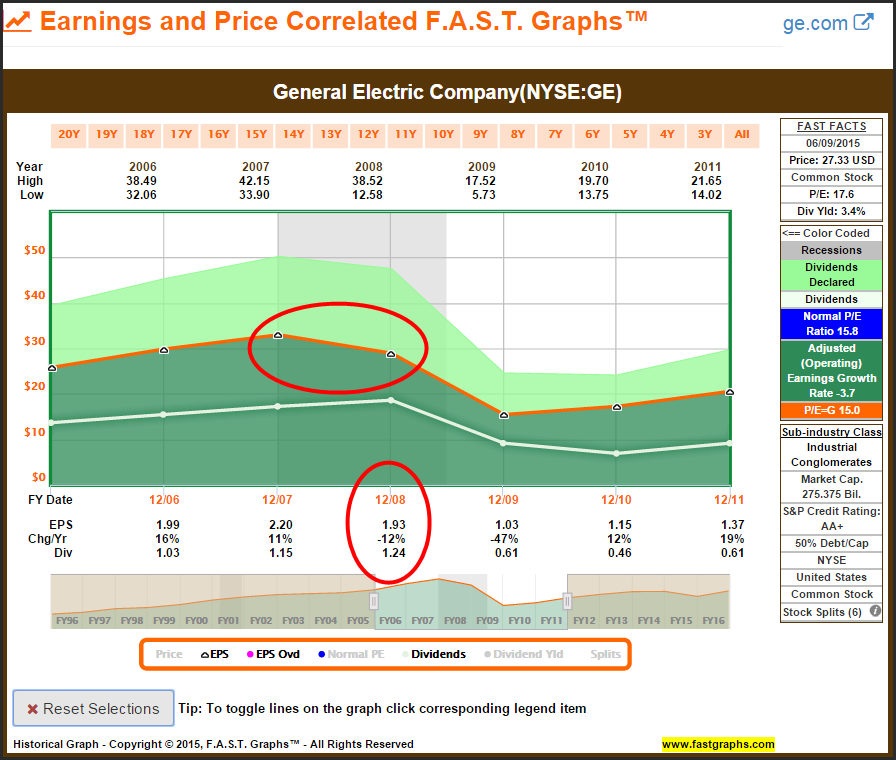

General Electric Company (GE) - When Persistence Would Be Stubbornness

In order to offer a fair and balanced perspective, my next example represents a company where a stop loss would have served investors well. Not all price drops are the same, and in the case of General Electric, when we look at stock price only we discover that the drop was approximately 63%. That is significantly more severe than we saw with the previous examples. Nevertheless, even when only viewing this company based on stock price alone we are alerted to the reality that something is materially different than what we saw with the others.

When we turn our attention to operating results without stock price, we discover that fiscal year 2008 brought a decline in earnings. Although I am not suggesting that a couple of down quarters in a row should automatically generate a sell decision, I am suggesting that it should have instigated some concern and scrutiny. In other words, I believe that deteriorating fundamentals should generate a careful and close examination of the company’s business prospects and health. This is a classic example of when persistence would have been ill advised. Holding on to General Electric throughout the Great Recession would have indicated stubbornness, not intelligent patience.

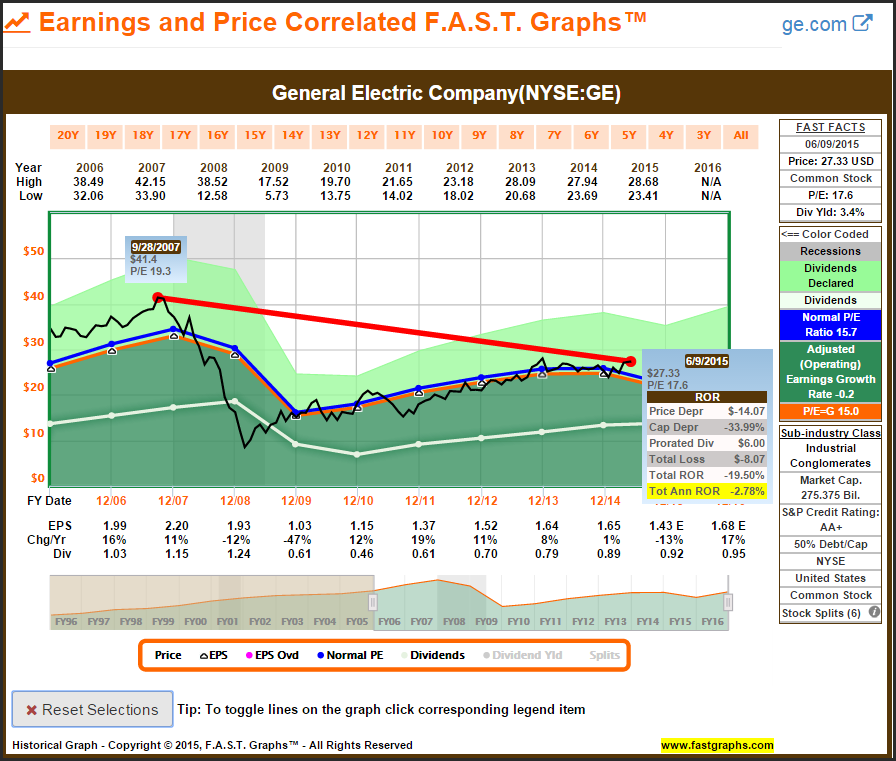

To be clear, I believe that if a company’s stock price is dropping while fundamentals remain strong, your correct course of action is to stay the course. On the other hand, your best course of action would be to recognize the opportunity and add to your position. However, if a company’s stock price is dropping as a result of fundamental deterioration, holding on is your worst course of action. Not all stock price drops are the same. As the following calculation illustrates, shareholders that held onto General Electric would still be experiencing losses today. That would simply be stubborn, not persistent.

Summary and Conclusions

This article was inspired out of my concern for the many people that have commented on my previous articles that are so worried about a potential market crash that they are afraid to invest in good investments, even when the opportunities are attractive. They will argue that even good stocks will drop during a bad market, and I concede that may, in fact, be true. However, neither they nor I can predict when that event might occur. It might happen tomorrow, or it might happen several years from now. But most importantly, I believe that if you exercise the discipline to only invest when valuation is sound or more attractive, a future market drop is really a nonevent.

Bear markets do come along from time to time, but all bear markets end with a bull market. If history is any guide at all, bull markets last and run significantly longer than bear markets. Our most recent recession, and the ensuing bull market we have been in since, support that thesis. I believe that people fear stock price drops and stock price volatility much more than it is warranted. I can only assume that this fear comes with an underlying belief that a bear market or market crash would lose them all of their money, or at the least have a long-term devastating impact on their financial futures. Personally, my experience tells me that those are exaggerated fears.

Finally, I do believe that all sound and prudent investing strategies share common principles. All true investors invest in businesses for the long term. All true investors attempt to focus primarily on the intrinsic value of those businesses, with an objective of finding a bargain to provide a margin of safety. All true investors have learned to trust their own judgments and have the conviction to be willing to go against the crowd. And all true investors have learned the importance of intelligent patience. They are patient because they understand the businesses they invest in, and this is where the intelligence stems from. To these true investors, short-term price volatility simply comes with the territory but is nothing to be fearful of in the longer run.

Disclosure: Long WMT,ROST,GIS,GE,JNJ,KO at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.