The weather is warming in the Northern hemisphere, and with it comes what clothiers call “swimsuit season.” I have a friend who has been working to get ready for the beach, but weeks of gym sessions had yet to move the needle.

Then, by chance, he weighed himself in a new location and discovered that 10 pounds had miraculously melted away. It turns out that his home unit had been poorly calibrated, and he had been making satisfactory progress all along. He promptly went home and threw his scale out the window.

To some, the world economy has been struggling to make satisfactory progress, giving currency to adherents of “secular stagnation.” But what if the scale we use to measure growth is wrong and output is actually much better than currently estimated? This possibility would be a game-changer for markets and policymakers.

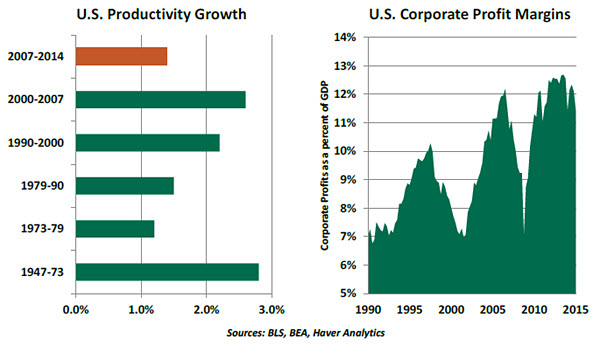

Much has been made of the recent slowing in productivity growth. In the United States, output per hour has been expanding at its slowest pace in at least 25 years. This decline feeds into the dire warnings of those who fear “secular stagnation” and predict a slow-growth future. Insufficient investment in infrastructure, equipment and human capital has been blamed for this disappointing outcome.

But there is a paradox. Corporate profit margins, while enduring cyclical fluctuations, have reached new peaks since the 2008 recession. Somehow, firms are achieving improved productivity that is not showing up in the national income accounts.

So what is going on? The following examples point to a possible explanation.

- Thirty years ago, an oil exploration company would have to drill a number of trial wells to locate reserves. That activity would require a good bit of equipment and the services of both geologists and roughnecks. All of these would contribute to gross domestic product (GDP).

Today, satellite imaging is used to pinpoint the most-opportune deposits and the best places to harvest them. Applying this technology has reduced the number of people and rigs needed to achieve the same output.

To utilize this modern capability, the exploration company pays a licensing fee to access the satellite and buys software and hardware to analyze the output. Those costs have become the contributors to GDP, even though the value they are producing might be significantly higher.

- Thirty years ago, a patient with a knee injury would require a full reconstruction. The procedure was extensive, and a week of hospitalization was normal. Today, arthroscopy is used extensively for more-minor damage. The procedure is minimally invasive and is often done on an outpatient basis.

Output for medical services is measured based on billings. Modern procedures that reduce hospitalization can, therefore, reduce the contribution of the sector to GDP even though the patient outcomes are as good or better.

There are legions of examples like these, where the application of technology has enhanced productivity in a way that is poorly captured when GDP is compiled. As we discussed in one of our View from Here essays, assessing economic output amid technological advance is very difficult.

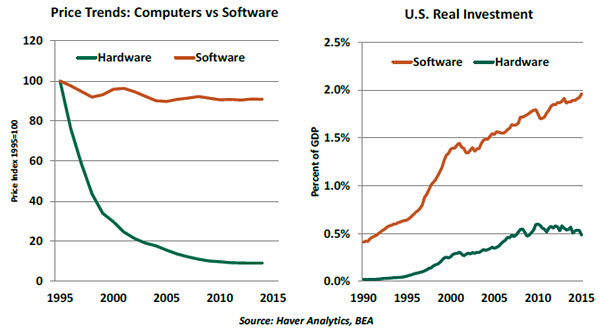

As another example, prices of computers have fallen for decades. But even at reduced prices, today’s devices are considerably more powerful than their predecessors. Statisticians can use increases in chip speeds (among other metrics) to arrive at a true cost of computing, which shows a pronounced deflationary trend.

As another example, prices of computers have fallen for decades. But even at reduced prices, today’s devices are considerably more powerful than their predecessors. Statisticians can use increases in chip speeds (among other metrics) to arrive at a true cost of computing, which shows a pronounced deflationary trend.

As another example, prices of computers have fallen for decades. But even at reduced prices, today’s devices are considerably more powerful than their predecessors. Statisticians can use increases in chip speeds (among other metrics) to arrive at a true cost of computing, which shows a pronounced deflationary trend.

Interestingly, though, the price index for software has not fallen nearly as quickly as it has for hardware. It is probably fair to say that that the features of the programs we use today are light-years ahead of what was cutting-edge 20 years ago. As a result, we may not be giving proper credit to the value software provides. This is a significant limitation, given that software investments have grown to 2% of U.S. real GDP, four times larger than in 1990.

Those who measure our economy have been trying valiantly to keep pace with this evolution. The need for valor has been increased by the paltry levels of funding offered to the statistical agencies. Some incremental funding might help to better measure what a product or service does as opposed to what it costs.

Those who measure our economy have been trying valiantly to keep pace with this evolution. The need for valor has been increased by the paltry levels of funding offered to the statistical agencies. Some incremental funding might help to better measure what a product or service does as opposed to what it costs.

The implications of all this are profound. If output is understated, then so is productivity. If productivity is understated, our potential for growth is higher and the momentum behind the secular stagnation theory is greatly diminished. While countries should still consider strategic investments in their economic infrastructure, fears that we are doomed to a sluggish future may be overblown.

Many who watch their weight are prone to shopping around for the friendliest scale. It is poor practice to favor a measurement regime just because it produces the happiest outcome. But when methods produce results that are clearly counterintuitive, it may be time to throw them out the window.

Cuba: Can the Revolution Evolve?

The recent thaw in relations between the United States and Cuba has investors buzzing about potential opportunities in the Caribbean nation. Does reality match the hype?

President Raúl Castro has begun a gradual economic liberalization since taking the reins from brother Fidel in 2006. Yet Cuba remains largely a centrally planned economy; the public sector represents 75% of both GDP and jobs. While commodities like sugar, tobacco and nickel are important, they comprise just 30% of all exports. Services account for the remaining 70%; the nation welcomes tourists from Canada and Europe while sending its doctors and teachers to less-developed economies. Cuba depends heavily on its ally Venezuela, which accounts for 14% of exports and 37% of imports in 2013, including heavily subsidized oil.

With GDP per capita of roughly $6,000 on a purchasing price parity basis, Cubans are relatively poor and depend on remittances from abroad (6.5% of GDP in 2013). Official unemployment is low at 3.6% but is likely understated. Despite its poverty, the workforce is healthy and highly educated, boasting one of the highest literacy rates in the world. Self-employment is on the rise and represents 8.6% of jobs, up from 2.8% in 2009.

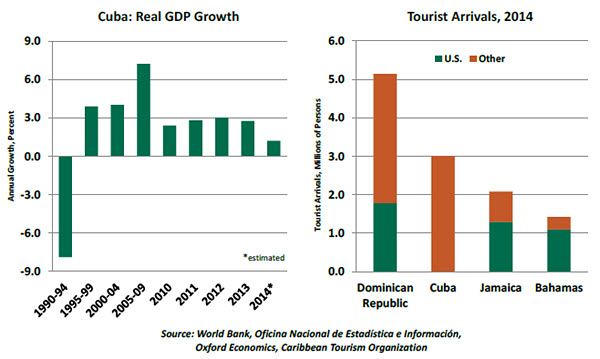

After contracting nearly 30% after the Soviet Union’s fall, Cuban real GDP growth rebounded from 1995-2008. Since then, the economy has decelerated significantly, eking out growth of just 1.2% last year. Investment is a meager 9% of GDP. Most worrying to Havana is Venezuela’s economic crisis; imports of subsidized oil have already been cut by 25% and could certainly be reduced further.

Cuba has begun to turn elsewhere. The U.K., France, Russia and Japan have all signed investment agreements with the Castro government. Locked out of international financing since its 1986 debt moratorium, the government is attempting to make its return to markets. Long Cuba’s largest creditor, Russia wrote off 90% of its debt last year. This week, Cuba agreed to eventually pay off $15 billion to Paris Club members.

The excitement surrounding Cuba is understandable, given its enormous economic potential. Infrastructure is poor; with just 5% internet penetration, telecommunications is ripe for development. A 20 billion barrel deep-water oil reserve discovered in 2008 is still untapped. U.S. visitors would be a boon for Cuban tourism. Washington still prohibits tourist visits in the narrow sense, but a new general travel license announced in January allows visits under a relatively broad range of motives.

The excitement surrounding Cuba is understandable, given its enormous economic potential. Infrastructure is poor; with just 5% internet penetration, telecommunications is ripe for development. A 20 billion barrel deep-water oil reserve discovered in 2008 is still untapped. U.S. visitors would be a boon for Cuban tourism. Washington still prohibits tourist visits in the narrow sense, but a new general travel license announced in January allows visits under a relatively broad range of motives.

Yet despite recent progress, Cuba remains a difficult place to invest. Local law is complex and administered unevenly. Foreign investors must partner with state-owned enterprises to navigate the thick layers of bureaucracy. Employee selection and compensation is determined by the state employment office. And a long history of expropriation scares many away.

Another major obstacle is the Banco Central de Cuba’s outdated currency regime. Cuba’s two official currencies – the peso (CUP) and the convertible peso (CUC, a dollar substitute used in tourist areas) – are fixed at CUP24/CUC and CUC1/USD, respectively. The government plans to unify the currencies by 2016, but doing so equates to a 96% devaluation and could cause financial turmoil if executed too swiftly.

Cuba’s prospects also depend on continued normalization in relations with Washington. Full diplomatic ties have yet to be established, and a lifting of the U.S. trade embargo still faces strong opposition in Congress. The process promises to be gradual.

So Cuba may one day regain its reputation as an investor’s paradise. We advise patience, however. And a cigar and a mojito on the beach while you wait.

Views from the Small World

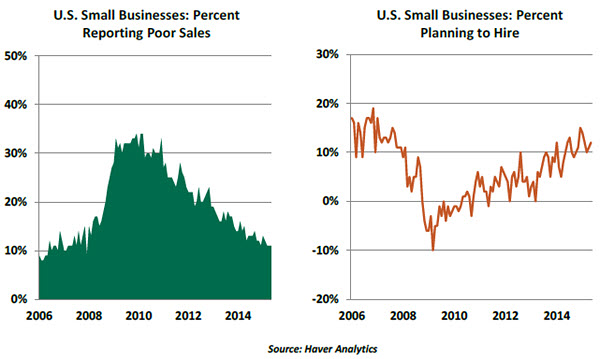

Although neighborhood book stores and other mom-and-pop establishments are not as prevalent as they were in the past, America’s small business community remains a vibrant one. By some measures, small businesses account for the largest gain in net jobs in the last three businesses cycles. And so their views on the economy deserve our attention.

Each month, the National Federation of Independent Businesses surveys its members about their attitudes and concerns. Responses to the most recent survey compared with those at the beginning of the recovery offer useful insights. The latest Small Business Optimism Index moved up to 98.3, the second-best mark in the present recovery. The index has yet to reach the high of the previous expansion, but there is meaningful improvement evident on many fronts.

During the deepest phase of the recession, 34% of firms reported poor sales as their single most-important concern, but only 11% are anxious about sales now. Hiring plans have improved steadily since 2009.

Government requirements (regulations) and taxes are the two major concerns of small businesses today. The percentage of firms holding this opinion is approaching record highs, particularly the view about regulation. This perception must change to retain the dynamism of this sector. Quality of labor is one of the keys to enhance productivity and contain wage growth. About 25% of survey respondents indicated that employment compensation moved up over the last three months, the strongest level for the current expansion. At the same time, the percent of small businesses concerned about the quality of labor is close to the levels seen prior to the onset of the crisis. This implies that additional wage gains are likely in the near term.

Surveys can never take the place of hard data. But current reflections from America’s small business community align with what we are seeing in the economic reports and should be a source of optimism during the quarters ahead.

(c) Northern Trust