IN THIS ISSUE:

1. May Unemployment Report Was Better Than Expected

2. Consumer Spending Continues to Disappoint, Savings Rise

3. IMF Urges Fed Not to Raise Interest Rates Until Next Year

Overview

On Thursday of last week, the International Monetary Fund downgraded its forecast for US economic growth this year from 3.1% earlier in the year to only 2.5% now. That is not surprising in light of the mainly disappointing economic reports we’ve seen recently, and other forecasters have been revising their estimates lower as well.

Yet in addition to the downwardly revised growth forecast, the new IMF report openly called on the Federal Reserve to delay any interest rate hike until sometime next year. In all of my years of Fed-watching, I don’t remember the IMF ever trying to influence Fed monetary policy. This is an unusual development, and it will be very interesting to see how it plays out.

The question is whether Fed Chair Janet Yellen and her fellow members of the policy setting Committee pay much, if any, attention to what the IMF has to say. We all know that the Fed really wants to raise short-term rates to give it some ammunition for the next recession.

This apparent disagreement is between two of the most powerful women in the world – Christine Lagarde, head of the IMF, and Fed Chair Janet Yellen. This issue will be our main topic today.

But as we often do, let’s first take a look at Friday’s stronger than expected unemployment report for May and the latest disappointing report on consumer spending.

May Unemployment Report Was Better Than Expected

The official unemployment rate rose from 5.4% in April to 5.5% in May, as reported last Friday. Normally, that is not good news. But as I have tried to explain over the years, the monthly unemployment reports are always complicated, and sometimes what appears to be bad news is good news and vice-versa. Such was the case with last week’s jobs report. Let’s get to it.

The headline unemployment rate did rise from 5.4% to 5.5%. But this time, the unemployment rate rose slightly because more workers re-entered the workforce with new jobs, or at least were actively looking for new jobs. That’s a good thing.

The Bureau of Labor Statistics (BLS) reported that employers added 280,000 jobs in May, the most in five months, which helped to dispel fears that a 1Q slowdown (-0.7% GDP) would extend into the 2Q. The BLS also revised new jobs in April down to 221,000 from 223,000 previously reported.

Hourly earnings in May climbed from a year ago by the most since August 2013. Average hourly earnings increased by 3 cents to $24.87 in May. That represented a 0.3% rise month-over-month, slightly higher than the 0.2% pre-report estimate. Year-over-year earnings rose 2.3%, slightly above the 2.2% consensus estimate.

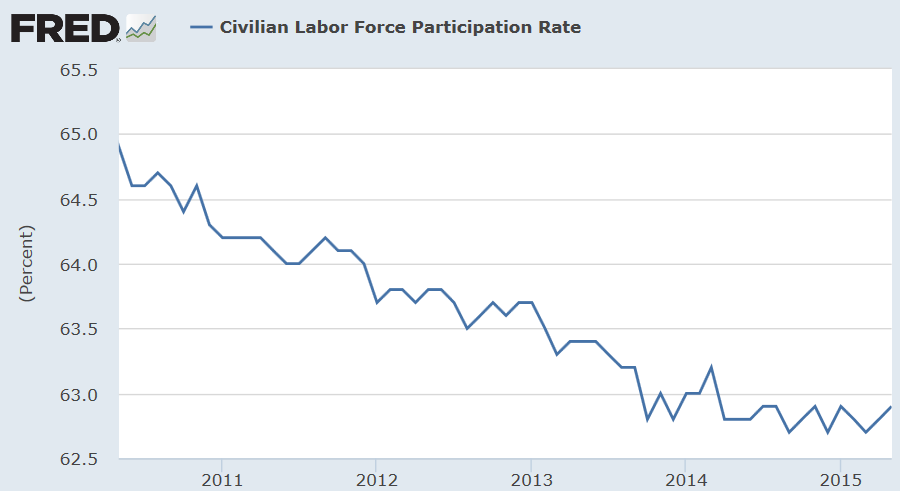

Lastly, the labor force participation rate rose to 62.9% in May, up from 62.8% in April and 62.7% in March. That is the second monthly increase in the percent of working age Americans who actually have jobs. While this indicator has a long way to go to get back to “normal,” it is headed in the right direction at least for now.

While the labor force participation rate has improved modestly over the last two months, we should always keep in mind that there are still almost 93 million working-age Americans not in the labor force. The month of May saw 92,986,000 people not participating in the workforce, down from 93,194,000 in April according to the BLS.

The BLS defines those not in the labor force as people ages 16 and older who are “neither employed nor made specific efforts to find employment sometime during the latest four-week period.” According to the BLS, the civilian labor force itself rose by 397,000, reaching 157,469,000 in May.

The takeaway from last Friday’s unemployment report is that we get these stronger than expected reports from time to time, but we need to see a trend of better than expected reports to draw any meaningful conclusions. No single good report should, by itself, cause us to draw conclusions that the economy is really getting better.

We should also keep in mind that with each new report, there are always revisions to the two previous reports, and they may be revised higher or lower. The point is, it takes several months to confirm a trend – up or down. At this point, we just don’t know if we’ve turned the corner and the economy is finally ready to shift into a higher gear.

Consumer Spending Continues to Disappoint, Savings Rise

Unfortunately, US consumers continue to pocket their gasoline savings rather than spend it in the economy. Consumer spending was flat in April (0.0%) – the weakest performance in three months – after a revised 0.5% increase in March, the Commerce Department reported last week. The March increase was the biggest gain since last August.

The unchanged reading for consumer spending in April was not a big surprise given weakness previously reported in retail sales and auto sales for the month. Economists, however, continue to forecast that spending will rebound in coming months. Solid gains in employment and incomes should translate into more confident consumers who are willing to spend more. But that remains to be seen.

Consumer spending slowed to growth of just 1.8% in the 1Q, down from spending growth of 4.4% in the 4Q. The frigid cold in many parts of the country kept shoppers away from the malls. With the arrival of spring and warmer weather, analysts are looking for spending to rebound.

The weakness in April, the first month in the new quarter, reflected big declines in spending on both durable goods such as autos and nondurable goods such as clothing and food. Spending on services, which includes utility bills and rent, edged up 0.2%.

With income growing and spending flat, the personal saving rate jumped to 5.6% of after-tax incomes – the second highest level since December 2012 – according to data from the Fed. The personal savings rate was only about 3% before the Great Recession began.

Economists had believed that consumers would start spending the savings they have accumulated from the big drop in gas prices. While the cost of filling up the tank has risen a bit in recent weeks, prices are still nearly $1 below the levels of a year ago. Consumer spending is closely watched because it accounts for70% of economic activity.

“The April income and spending figures are another reminder that even though their incomes are rising at a healthy pace, households are still reluctant to boost spending more freely,” said Paul Ashworth, chief US economist at Capital Economics.

Now let’s turn to our main topic today.

IMF Urges Fed Not to Raise Interest Rates Until Next Year

The International Monetary Fund (IMF) cut its forecast for US economic growth in 2015 last Thursday and simultaneously called on the Federal Reserve to delay its much expected Fed Funds rate hike until sometime next year. In all my years of Fed watching, I don’t recall the IMF ever openly attempting to influence Fed monetary policy.

For those not familiar with the IMF, the International Monetary Fund is a global organization headquartered in Washington, D.C. representing 188 countries. The IMF works to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth and reduce poverty around the world.

Formed in 1944 at the Bretton Woods Conference, the IMF came into formal existence in 1945 with 29 member countries with the goal of reconstructing the international payment system. Member countries contribute funds (dues) to a pool through a quota system, from which countries with payment imbalances can borrow.

Through this pool of funds, and other activities such as statistics keeping and analysis, surveillance of its members’ economies and the demand for self-correcting policies, the IMF works to improve the economies of its member countries. The IMF is considered by many (including your editor) to be a liberal-leaning organization – it is a big proponent of global warming, now better known as “climate change.”

Getting back to last Thursday’s report, the IMF reduced its forecast for US economic growth in 2015 from 3.1% as recently as April to 2.5%. It cited several negative developments including the severe winter weather, the strong US dollar, the West Coast port dispute and collapsing oil prices as reasons for the growth downgrade.

As a result of these negative developments, the IMF said it believes that risks are rising in the US financial system, most notably in the insurance industry and in riskier assets such as stocks. The IMF obviously is concerned that higher short-term interest rates would pose even greater risks for the financial system in general. Thus, the call on the Fed to delay interest rate liftoff until sometime next year.

The IMF warned that regardless of when the Fed raises rates, the increase could trigger “significant and abrupt rebalancing of international portfolios with market volatility and financial stability.” Inflation also could rise faster than expected, potentially provoking a sudden shift upward in borrowing costs, the IMF added.

“In either case, asset price volatility could last more than just a few days and have larger-than-anticipated negative effects on financial conditions, growth, labor markets, and inflation outcomes around the world,” the IMF said. “Spillovers to economies with close trade and financial linkages could be substantial.”

Last week’s IMF report also noted that a Fed rate hike this year could lead to a sharp appreciation of the dollar, which would badly hit emerging countries with large amounts of dollar-denominated debt. If the Fed raises rates this year, some analysts fear a wave of defaults which, in the most exposed countries, could lead to another serious global financial crisis.

But is Fed Chair Janet Yellen Listening? Maybe, Maybe Not

The IMF’s Managing Director Christine Lagarde told reporters last week: “We believe that a rate hike would be better off in early 2016.” Yet she declined to say whether she had discussed the IMF’s effort to influence US monetary policy with Janet Yellen. But she insisted the IMF’s view was not at odds with that of Ms. Yellen, who has said that the Fed would raise rates only when economic data was right.

However, the conclusions of last week’s IMF report seem to go against what Fed Chair Yellen said just last month in a speech she gave in Rhode Island. Yellen sees signs of a recovery in the economy and believes the Fed will be able to raise rates sometime later this year. Most experts believe the Fed will raise rates in September, but the IMF recommendation to hold off will likely re-open the debate.

Thursday’s IMF report is another worrisome sign that the US economy is stalling. Although the IMF still expects America's economy to grow this year at a rate of 2.5%, that is little improved over last year’s growth of 2.4%. The hope was that America would have a breakout year in 2015. As noted above, the IMF projected 3.1% growth for the US in April, but now the global agency sees too many factors holding the economy back.

The Fed hasn’t raised rates in almost a decade and the FOMC would clearly like to begin the process of “normalization” to get rates higher in advance of the next recession. In Yellen’s mind, a rate hike would show that the Fed is confident enough about the economy’s health to take off the training wheels (zero interest rates) that have been in place since the financial crisis began in 2008.

A spokesperson for the Federal Reserve declined to comment on the IMF’s report, but it may be safe to assume that Janet Yellen didn’t appreciate the IMF sticking its nose in the Fed’s business.

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.