“We fail to comprehend how owners of claims on money (that is, bondholders) can continue to ignore the fact that the goal of generating more inflation is aimed precisely at reducing the value of their capital. The opportunity, then, is to short bonds.”

– Paul Singer

Do you remember that feeling you had when you were a kid as you walked out of school and opened the door to summer? Yesterday, Susan’s oldest graduated from high school. I loved the closing commencement remarks, “now go forward and shine your light bright.” Caps in the air. What a feeling!

Man, I wish I could have that feeling again. Though it is nice to see it on the faces of our children. But alas, a family to raise, bills to pay, and inflation and bond yields on my mind. So back to work we go and fortunate that this is a fun business.

It’s been a wild week for bonds. The 10-year has gone from 1.92% to 2.40% since early April. A loss of 4.24%. Over the same period, the 30-year has gone from 2.62% to 3.11%. A loss of 9.51%. (Source: StockCharts.com)

I’m on record saying that the greatest bubble of all time is in the bond market. I believe that is where the greatest risks to your portfolio exist. Are we seeing warning shots across the bow? I think so.

So today, let’s take a look at the current state of inflation and the direction of interest rates and peek at a few processes that may help us better navigate the rough waters ahead. My gut says it will be the bond market that jerks the Fed’s chain. We’ll see. I do agree with Singer, “The Great (Greatest) Short” is in the bond market.

Included in this week’s On My Radar:

- Inflation and Interest Rates – Signs Point to Mild Disinflation (What I’m Watching)

- A Few Ideas on Managing Interest Rate Risk

- Investors Spent 75% of The Time Recovering From Loss (1900 to present)

- Trade Signals – Bond Yields a Mess, Equity Trend Positive, Sentiment Neutral

Inflation and Interest Rates – Signs Point to Mild Disinflation (What I’m Watching)

I sent a note to Ned Davis a few weeks ago asking him what indicators he looks at for inflation.

Ned replied with the following:

“This is a hard one for me. I think the most important indicator for the inflation super-cycle is the debt super-cycle, but it is very complicated. For something more current, I would look at our Inflation Timing Model. Other individual charts with great records I have found useful are E960A, E708A, E0720, E764 and DAVIS191. Obviously, looking at those charts suggests I think wage inflation is very important.”

Some chart code to dissect in that email so I’ll try to make some sense for you (and me).

First of all, what I like about NDR is their data approach to investment research. This business is confusing enough and often what many believe will happen is completely the opposite of what actually does happen. So into the data we dig.

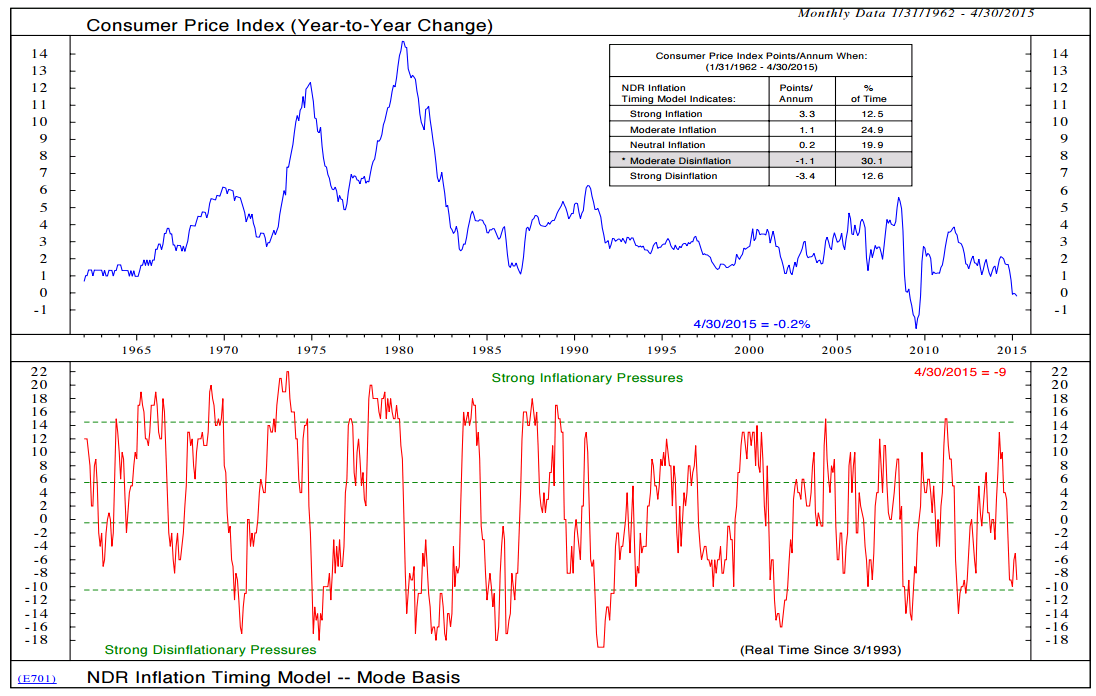

This first chart is NDR’s “Inflation Timing Model.” It shows that with overall inflationary pressures at -9, we are in a period of “moderate disinflation”. (Bottom section reading as of 4-30-15 is -9) Note the -1.1% decline in the CPI per annum when in the moderate disinflation zone.

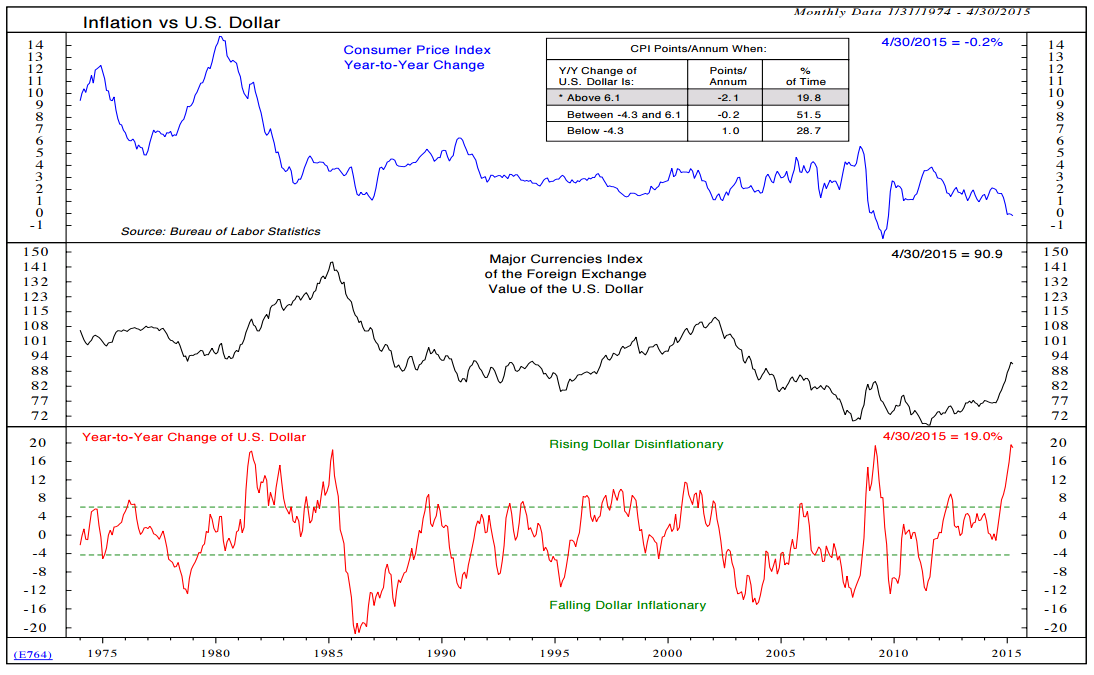

Next are two charts that show inflation to be low:

1) Inflation vs. U.S. Dollar:

Note in the bottom section of the next chart how disinflationary a rising dollar historically tends to be (bottom clip with stats on the current state shaded in the upper clip).

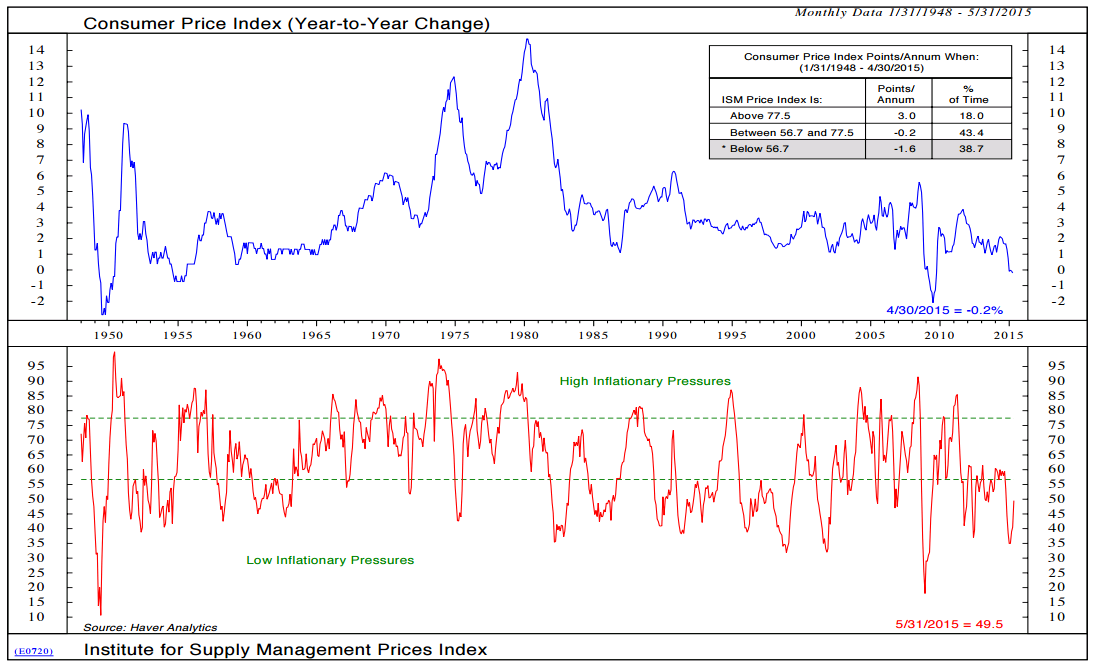

2) Consumer Price Index (Year-to-Year Change).

2) Consumer Price Index (Year-to-Year Change).

Here, too, we see low inflationary pressure today.

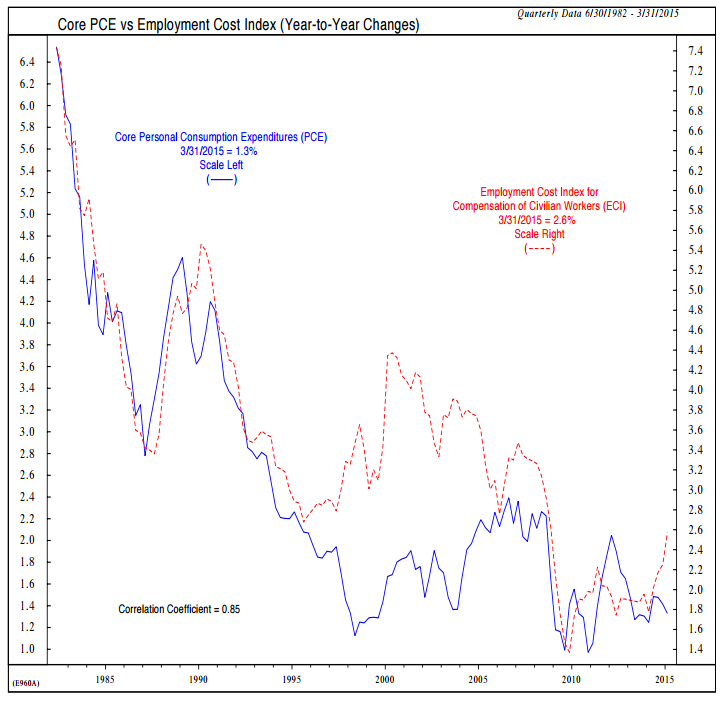

However, there are some signs that core CPI inflation is turning. Ned noted that over the last four months, year-over-year core CPI inflation has gone from 1.65% (January 2014 to January 2015), 1.70% (February to February), 1.75% (March to March), and the latest reading was 1.81% in (April to April).

Service inflation is running at 2.3%, shelter inflation is running 3% and CPI for medical care is 2.9%. As Ned shares, “Shelter and medical care are of course big deals.”

So which is it? Deflation, disinflation or inflation. It still looks like disinflation with signs of inflation on the horizon. Wages are important and with a high .85 correlation to Core PCE, you can see a big uptick since late 2014 below (dotted red line). Note how closely the blue line (Personal Consumption Expenditures) follows the dotted red line. Kind of a good news (wages are going up), bad news thing (inflation).

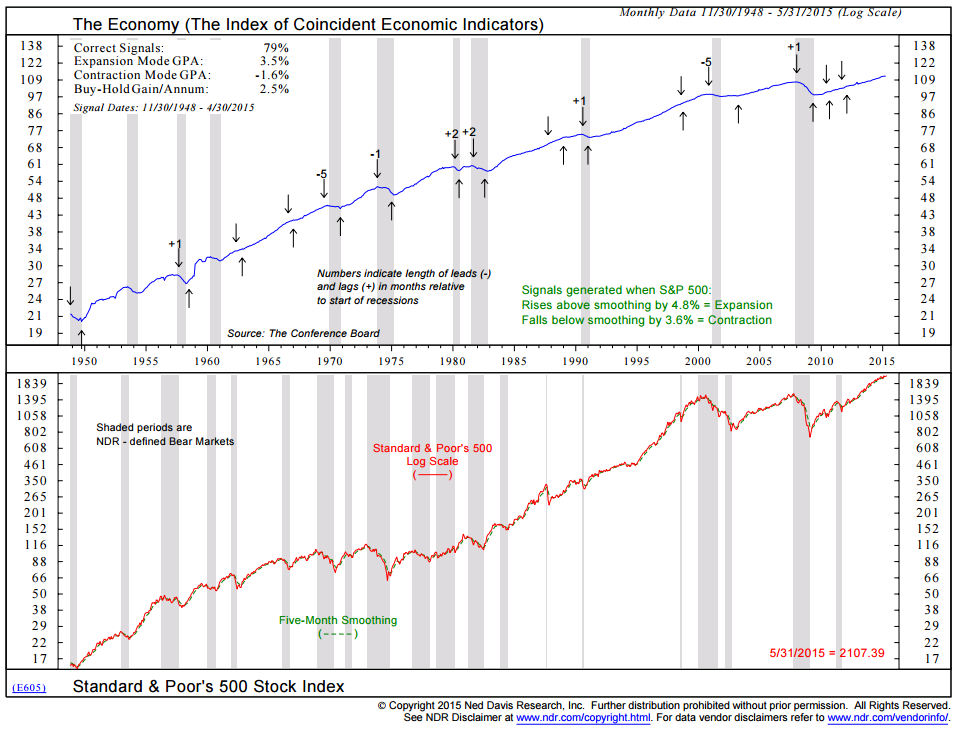

Each week in Trade Signals I post my favorite “Recession Watch” chart. It is titled The Economy (The Index of Coincident Economic Indicators) yet I follow it because it has done a great job historically at signaling periods of recession starts. I share it next.

Note the down arrows signal recession and most have been correct. The -1 or +2 tell you how many months before (a minus number) or how many months after (a plus number) the actual recession occurred. Recessions are only known many months after they actually start due to the delay in reported economic figures. So it is ahead of time that we are after and this process has done a great job calling recessions. Also, while not all signals have proven correct, those that missed didn’t keep you out of sync for long.

With a 79% correct signal history and the major declines in equities and high yield bonds that accompany recessionary periods, I believe this chart can help us in our portfolio risk management process.

In short summary, no major inflation at this time but some clouds are gathering. Also, there are no signs of recession at this time. That is good news.

A Few Ideas on Managing Interest Rate Risk

So let’s next look at a few ideas that may help you identify the price trend and position in a way that allows you to participate and protect.

As for interest rates, I believe there are a few processes we can follow to help us position properly. None are perfect, yet, nor were all of the Wall Street economists who felt interest rates would rise in 2014 predicting a move from 3% (as measured by the 10-year Treasury) to 3.25% by that year-end. It fooled them all – interest rates moved lower and finished the year at 2.2%. They missed the fourth best year in bond history.

Idea #1:

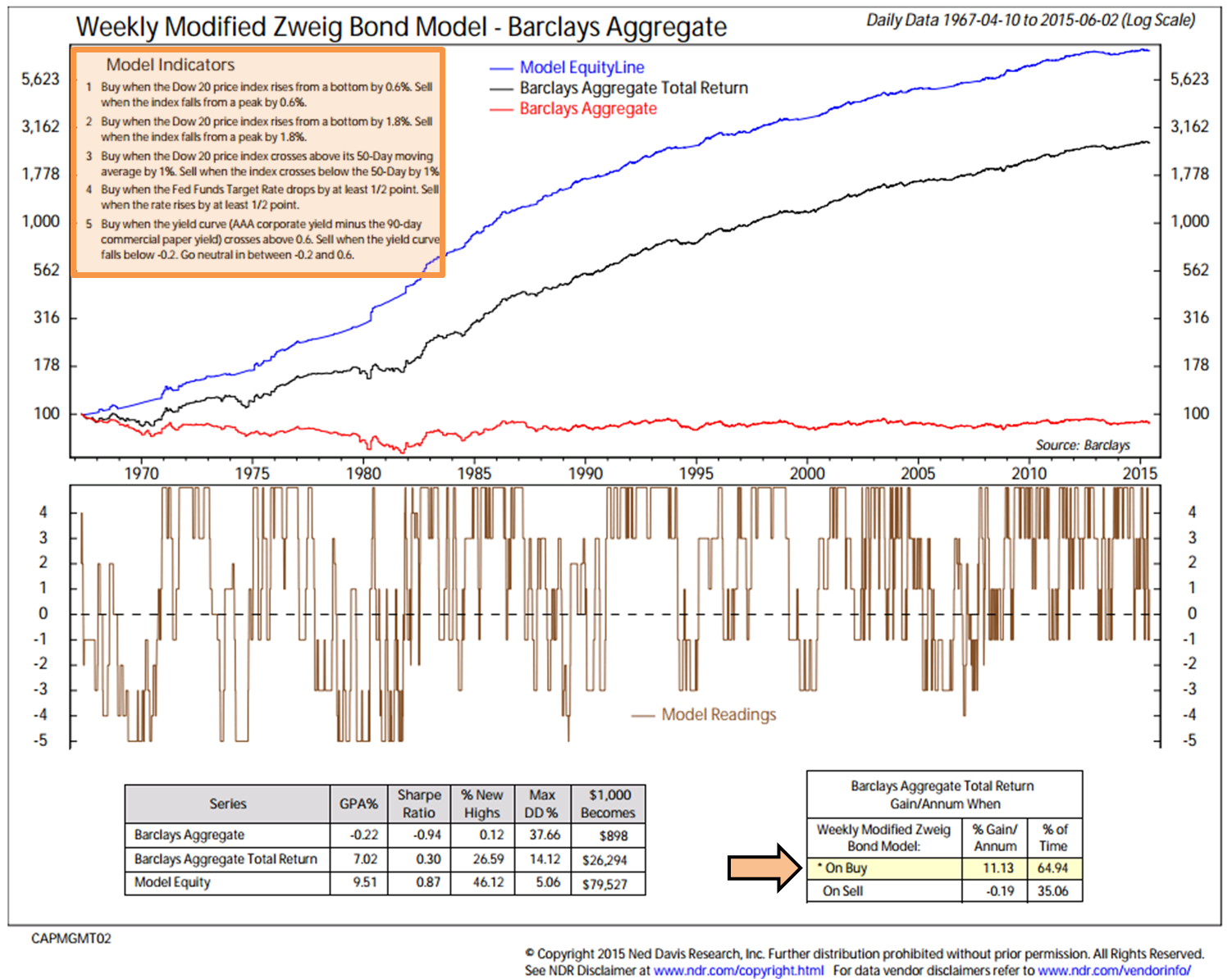

Each week I post the Zweig Bond Model. The data is evaluated weekly and the model is updated after every Friday’s close. It helped me stay long bonds in 2014 despite the consensus opinion to the contrary. The model turned negative in early April (timely) suggesting to shorten maturity exposure to something like a short-term Treasury Bill ETF (“BIL”) and remained in a sell until last Monday. Based on the price action this past week, it will likely move back to a sell next Monday. A rough head fake but that can happen. The goal it to get the major trend moves right.

Note the process highlighted in orange and the historical performance On Buy and On Sell signals (see orange arrow).

I often look to moving averages to keep me up-to-date with the trend. Another way to manage risk is to lengthen maturities when the 13-week EMA is above the 34-week EMA. See Trade Signals (link below) for a deeper explanation. There are other approaches – my favorite is the Zweig Bond Model Trend Signal.

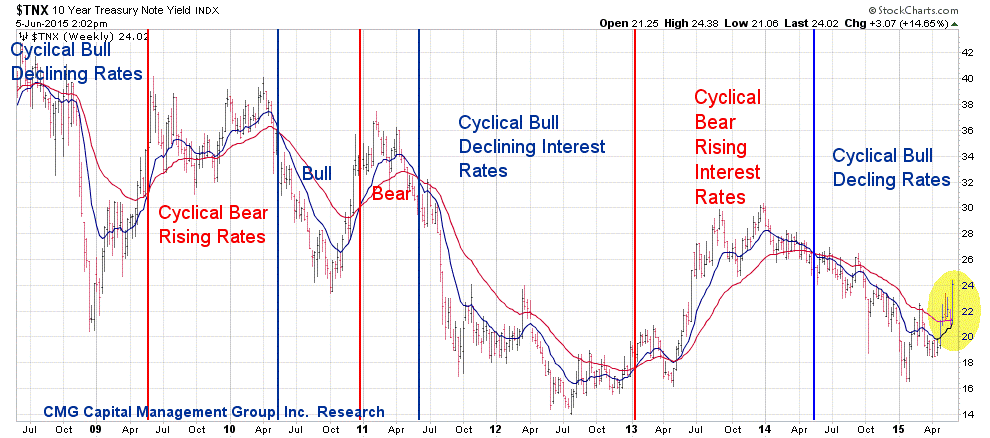

Note next how the trend in the 10-year Treasury Note Yield is about to move to a “Cyclical Bear or Rising Interest Rate” period (yellow highlight).

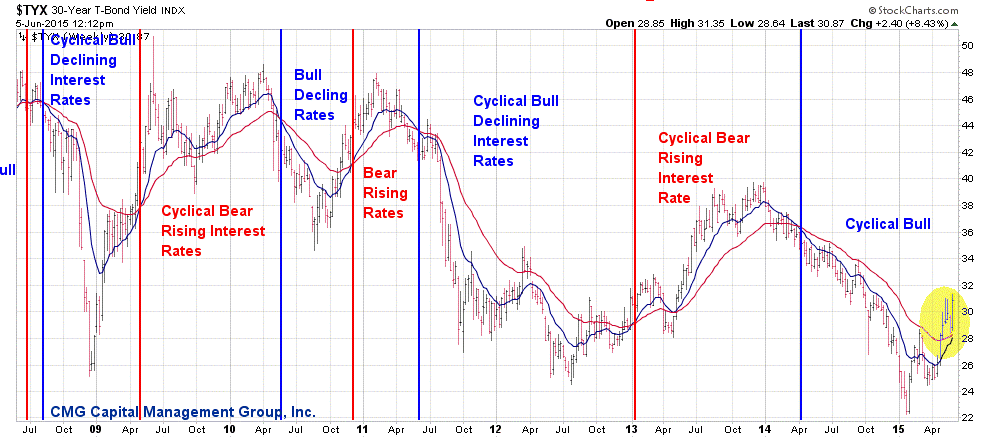

Same with the 30-year Treasury bond:

Why is this so important? We are at historically low interest rates. When rates rise, the risk to portfolios is significant. If our starting place was much higher interest rates, the risk dynamic would not be as severe.

If the greatest short of all time is in the bond market, then we can position to profit, we can position to side-step the decline in the bond market’s losses, or we can get run over.

I favor a process with a high probability win rate. I really don’t know nor do I believe anyone else knows the timing of higher interest rates. What I do believe is that the global central banks intend to and will create inflation. With unprecedented action comes unintended consequences. So defend ourselves we must.

Finally, as it relates to bonds, it looks like high yield bonds are turning lower. I shared some ideas on how to participate and protect in a webinar recently titled, The Opportunity of a Lifetime – Just Not Yet. Click here to access the video.

Investors Spend 75% of The Time Recovering from Loss (1900 to present)

We put together an educational piece for our advisor clients to use, if they wish, in their work with clients. It is titled The Merciless Mathematics of Loss. The piece begins with:

One of our advisors asked to see the data post the great depression in the 1930s. A great question as that period took 25 years to recover from the loss (1929 to 1954). So I shot an email over to my research support team at NDR.

- NDR first looked at the period 1900 to present (updated as the quote above is several years old). It shows that the market spent 74.1% recouping losses and just 25.9% of the time making new highs.

- If we start the data in 1954, it shows that the market spends about 33% of the time making new highs and 67% of the time in bear markets or recovering from loss.

While I think 25 years recovering from loss is abnormal, recall that it has taken 15 years to recover from the 2000 tech wreak.

So let’s settle on somewhere between 67% and 74% of the time. Either way, it is for this reason that investing is so hard for so many.

Trade Signals – Bond Yields a Mess, Equity Trend Positive, Sentiment Neutral

Note today the Zweig Bond Model’s “Buy” signal for bonds. The data takes into account price activity and is updated weekly based on Friday’s closing data. The last three days have been wild. The yield on the 10-year Treasury has gone from 2.09% to 2.36% in just two days. I suspect that the Zweig Bond Model will switch back to a sell after today’s up move in yields (decline in price).

Click here for the updated trend and sentiment charts.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Captial Management Group

© CMG Capital Management Group