I had one of those days recently when nothing went right. I went to the wrong location for a meeting and had to scramble to reach the correct destination. My slides were a mess, and questions were asked that I could not answer. Later on, a project status meeting showed my assignments drifting from green to yellow, and yellow to red. When I finally returned to my office, there were six auditors waiting to speak with me. Oh, and my son called to request rent money that was due in 24 hours.

When I got home that evening, dejected and disheveled, I suggested to my wife that I was contemplating retirement. “Well, I don’t want you around all the time,” she said warmly. That was the perfect coda to a perfectly awful day.

Happily, things have stabilized on all fronts since then, so there is no rush to prepare for retirement. But other members of the Baby Boom generation are looking ahead more anxiously to retirement, and many are realizing that public and private preparations for their golden years are inadequate. This situation promises to have significant consequences for the American economy in the years ahead.

Projecting demographics is among the more manageable aspects of economic forecasting. So we have known for decades that the post-World War II generation would be reaching the end of their working lives right about now. Given that long lead time, one would think that retirement regimes would be comfortably ready to meet their obligations. Instead, many public pension systems are dramatically underfunded.

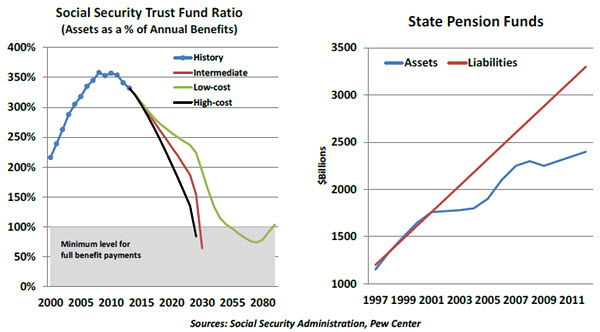

Reserves in the nation’s Social Security system are projected to be depleted in less than 20 years, triggering a reduction in scheduled payments. And the shortcomings of state and local pension systems are prompting some very difficult discussions between governments and beneficiaries.

We have arrived at this point because of flaws in design and behavior. As an example, the Social Security trust fund is a “pay-as-you-go” system whose reserves can only be invested in U.S. Treasury securities. This is an asset allocation that few would recommend for long-term goals. Other nations have established large asset pools to provide retirement benefits; these funds are open to a broad range of investments and are largely closed to political influence.

At the state and local level, generous pension accounting rules and (in some cases) a lack of discipline in making scheduled contributions have created deep funding shortfalls. These deficits have created uncertainty over the tax environment in some communities, which can hinder economic development.

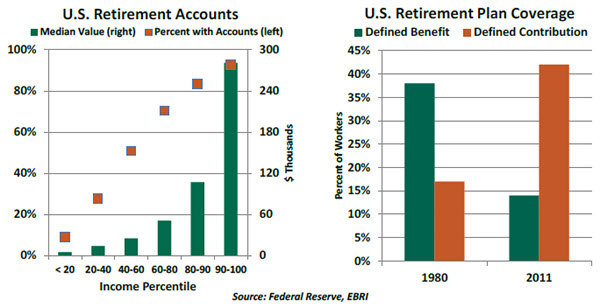

Private-sector preparedness for retirement is uneven. Evidence from the Federal Reserve’s most recent Survey of Consumer Finances reveals that while some households are in a very good position, many have few resources set aside for retirement.

Again, here, flaws in both design and behavior have brought us to this point. In 1980, almost 40% of the American working-age population was covered by a pension plan. Employers liked them because they engendered loyalty and could be traded off against wage increases. Employees liked them because they were a form of enforced saving that relieved them of the responsibility and risk involved with long-term investing.

Since then, retirement benefits in the United States have moved decisively toward defined contribution (DC) structures like 401(k) plans. DC plans can be transported as employees change jobs, a quality that matches well with today’s more flexible labor force. But many studies suggest that workers often make poor choices about their level of contribution and their investment allocations.

Outside of these plans, many families had been relying on their home equity as a source of retirement saving. While home values have improved modestly since the 2008 crisis, more than 10% of homeowners are still “under water”: the value of their property is less than the loans taken out against it.

As an added complication, retirement horizons have been lengthening as people live longer. Those who reach 65 in the United States today can expect to live about 20 more years, on average. Many will need financial resources that last until they are well into their 90s.

One reaction to all of this is that Americans are working longer than they used to. The labor force participation rate among people over the age of 65 has risen from 11% in 1991 to 19% today. Some simply want to work longer and are healthy enough to do so. But others, undoubtedly, remain at work because they cannot afford to retire.

Another reaction is the heighted level of emotion that surrounds any discussion of entitlement reform. For one-third of current retirees, Social Security benefits represent at least 90 percent of their income. And those benefits are far from generous: the average retiree is getting about $16,000 annually, which isn’t much above the poverty line.

Solutions are elusive. We cannot turn back the clock and increase our saving rates or invest with the benefit of hindsight. But from here forward, we need to take a hard look at the structure of public and private retirement systems and reinforce financial literacy among beneficiaries.

With the benefit of some calm, I was able to engage my wife more productively in a discussion about retirement. Unfortunately, a review of my investment spreadsheet indicated that I will have to work until I am 92 before I can quit. I am afraid that you, our readers, will be putting up with me for a long time to come.

Impressive U.S. Job Growth Raises Probability of Fed Hike

The May employment report confirms our suspicion that the weakness in retail sales in the first four months of the year understated the fundamental strength of the economy.

The unemployment rate was up one notch at 5.5%, down from 6.3% a year ago. The participation rate increased one-tenth to 62.9%, which changes the interpretation of a higher unemployment rate as it moved up largely because of an increase in the labor force (+397,000). The broad measure of unemployment, which includes the marginally attached and those working part-time but who would prefer full-time jobs, held steady at 10.8%.

The share of long-term unemployment inched down to 28.6%, a new cycle low, and the median duration of unemployment at 11.6 weeks is another new low mark for the cycle. Taken together, these data from the household survey suggest that labor market conditions showed further improvements since the last Fed meeting.

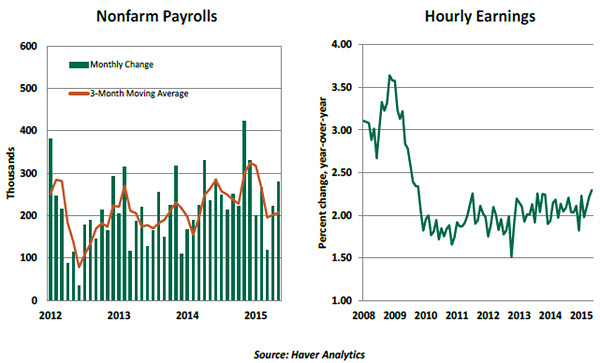

Payroll employment rose 280,000 in May, with revisions of the prior two months adding another 32,000 to the job rolls. The 3-month moving average at 207,000 is double what is necessary to match labor force growth.

Looking at the major components, goods sector employment advanced 6,000 in May, reflecting gains in construction (+17,000) and factory jobs (+7,000). The mining component (which captures employment in the oil and gas industry) fell 17,000, which is the fifth consecutive monthly drop. In the service sector (+256,000), hiring in the leisure and hospitality sector, health care, professional and business services, and retail posted relatively large increases in employment.

Average hourly earnings increased 0.3% in May, putting the year-to-year gain at 2.3%, the best in the cycle. Historically speaking, wage acceleration commenced after the jobless rate touched the 5.5% mark during the last two business cycles. Therefore, as the expansion continues and slack in the labor market diminishes, it should not be surprising to see further increases in compensation. The upward trend of wages will help to normalize inflation, thereby adding support for a potential tightening of monetary policy.

The Federal Reserve’s forward guidance noted that additional improvement in hiring was one of the requirements to trigger a normalization of interest rates. The May employment report offers adequate evidence for the Fed to be “reasonably confident” about labor market developments. We remain quite confident in our anticipation that the Federal Open Market Committee will announce a small increase in interest rates in September.

First Quarter U.S. GDP Estimate – Technicalities Part of the Weakness

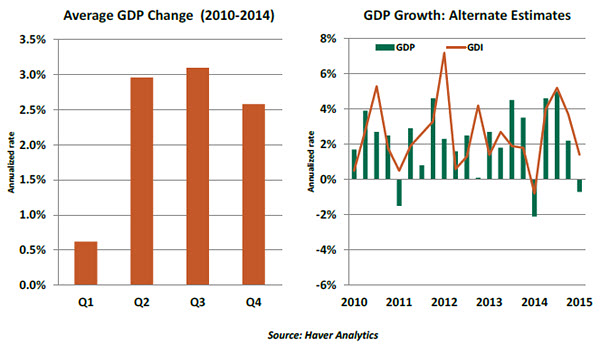

Last week, the Bureau of Economic Analysis (BEA) reported that real gross domestic product (GDP) declined at an annualized 0.7% rate in the first quarter. The critical question is whether this is a seasonal aberration or a lasting slowing of business conditions. In our view, it is the former.

Economic activity can show seasonal movements at the same time each year. Retail sales in the holiday season shoot up, heating bills increase in the winter, and construction activity is stronger in some months of the year than others. Statisticians remove these regularly occurring fluctuations with seasonal adjustment methods. The objective of seasonal adjustment is to enable identifying cyclical and trend movements of economic activity and make it easier to understand the underlying pace of activity.

Yet even after these calibrations are applied, U.S. real GDP growth averaged 0.6% in the first quarter during 2010-2014 compared with significantly stronger growth in the subsequent three quarters. Putting it differently, after seasonal adjustments the BEA carries out for GDP data, first quarter GDP numbers still show a seasonal pattern, which is called “residual seasonality.”

Experts have noted that certain types of construction, exports and defense procurement are all demonstrating seasonal behavior that the BEA does not currently adjust for. To correct for this, the Federal Reserve Bank of San Francisco has re-estimated GDP numbers with another round of seasonal adjustments and found that first quarter real GDP growth was 1.6 percentage points stronger than originally estimated.

As another piece of evidence, gross domestic income (GDI), also a measure of economic growth, shows less-weak first quarter readings. Conceptually, GDI and GDP are equal; GDP measures economic activity by adding up all the spending in the economy, while GDI measures it by adding all the incomes generated from producing GDP. The GDP estimates are from survey data that are aggregated from the bottom-up; aggregating series does not guarantee that residual seasonality will not occur. The GDI numbers are administrative data from firms with fewer measurement errors, and residual seasonality is smaller.

The official GDP statistics will undergo a benchmark revision in July, and many expect that the disappointment of this year’s first three months will diminish on further review. On more than one level, we are glad that winter is over.

(c) Northern Trust