In its 2nd estimate of 1Q15 GDP growth, the Bureau of Economic Analysis published its preliminary estimate of corporate profits. No surprise, profits fell sharply in the quarter, reflecting the impact of a stronger dollar, adverse weather, and possibly statistical noise and seasonal adjustment issues. Profits are a key driver of new hiring and capital spending. Looking ahead, a lot will depend on currency market developments.

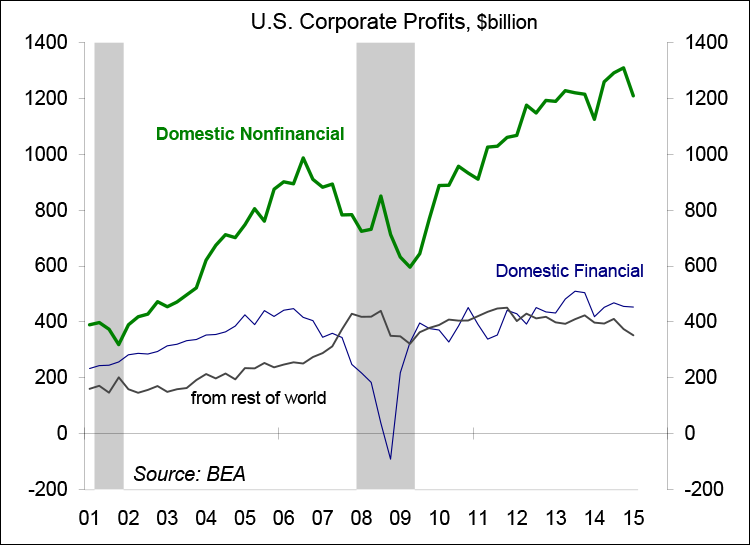

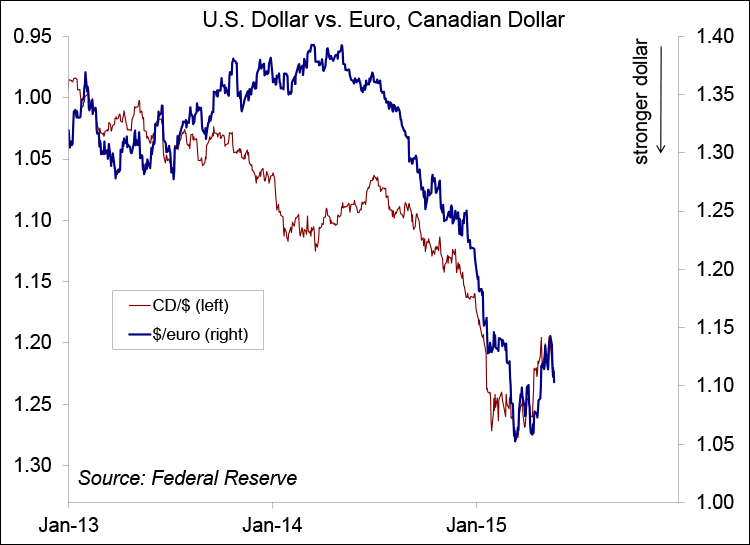

The government’s preliminary estimate of corporate profits, which includes privately held corporations, fell 5.9% q/q in the first quarter, reflecting weakness abroad (profits from the rest of the world fell 6.0% q/q, down 11.5% y/y) and at home (domestic nonfinancial profits fell 7.7%, up 7.5% y/y). The strong dollar played a part in that, restraining exports and reducing the dollar-value of overseas earnings.

A number of foreign-trade accounting issues add confusion. Goods and services produced here and sold abroad are considered exports (adding to GDP). Goods and services produced abroad and sold here count as imports (subtracting from GDP), regardless of whether they are produced by a U.S. firm or a foreign one. Foreign companies producing and selling here count as domestic consumption or business investment, not as foreign trade. For example, Japanese and German car companies make some models in the U.S., which count as domestic demand. It gets more complicated when you consider that parts often come from many places and are assembled in pieces both here and abroad. The key issue is where the value added takes place. An iPhone assembled in China counts as domestic consumption and imports – the wholesale cost is counted as imports and the difference between the retail price and the wholesale price is considered domestic consumption. Note that a company may overstate its import wholesale costs in order to reduce U.S. taxes, distorting the picture.

Corporate profits and cash flows have historically been key drivers of business fixed investment. Recessions are often preceded by a drop in profits. Longer term, there’s a seesawing pattern in the share of national income going to labor compensation and the share going to corporate profits. The share going to labor has been at the low end of the range in recent years, but ought to increase as the job market tightens.

Much of the weakness in corporate profits in the last two quarters has been due to the stronger dollar (the more troublesome aspect has been the speed at which the dollar has strengthened). The dollar began to soften in mid-March, reflecting a substantially less aggressive outlook for Fed policy (a consequence of disappointing economic growth in the first quarter). The exchange rate of the dollar is likely to be range-bound in the near term, but will depend critically on the U.S. economic outlook (which may be subject to some statistical distortions) and developments overseas. If the dollar remains relatively stable, the impact on corporate profits should wane.